TMUS - Crown Castle: Slow Growth Outlook Provides A Buying Opportunity

Summary

- This article is the first in a series on a portfolio designed to produce maximum long-term income through dividend growth.

- I examine CCI's business outlook and dividend strength to determine whether it is a buy at current levels.

- With mobile carriers reducing capex and churn from the Sprint/T-Mobile merger, CCI investors should expect low single-digit growth until interest rates fall and the economic picture improves.

- I believe the bad news has largely been priced in and rate CCI a buy.

I maintain two 25-position, equal-weight dividend growth portfolios for my personal investing goals, one with an offensive orientation (my "Ultra High DGI" portfolio) and one with a defensive orientation (my "Defensive DGI" portfolio). Each portfolio has been painstakingly constructed and backtested to maximize risk-adjusted returns and dividend growth based on its respective aim, with the defensive portfolio seeking to minimize drawdowns during difficult periods and thus be as "recession-proof" as possible, and the offensive portfolio seeking to maximize long-term dividend and capital growth.

This article marks the first entry for my Ultra High DGI Portfolio, beginning with the second-largest U.S. cell tower REIT, Crown Castle Inc. ( CCI ).

First, A Caveat For REIT Enthusiasts

I'll begin with the caveat that REITs are not my main area of coverage, so for those investors who focus primarily on REIT investing, please note that I'm writing this analysis from the perspective of a dividend growth investor who typically only includes blue chip REITs in my portfolios when they meet certain criteria that traditional stocks can't, and often do not include them at all. I have nothing against them and respect their wide moats and strong wealth compounding potential, but often their share price volatility and economic sensitivity prevents them from having the best long-term risk-adjusted return metrics in the overall stock universe.

For example, my Defensive DGI Portfolio, which seeks to minimize drawdowns over time, contains zero REIT holdings but is significantly overweight utilities. In contrast, my Ultra High DGI Portfolio, which primarily aims to maximize quarterly income by retirement (in my case that's around 20 years), contains only one utility company ( NEP ) but is significantly overweight REITs, mainly because the portfolio was constructed recently while REITs have been trading at some of their lowest valuations and highest yields in years.

CCI: Low Growth Outlook, But That's OK

Crown Castle Inc. is one of the three largest cell phone tower real estate investment trusts in North America, along with American Tower ( AMT ) and SBA Communications ( SBAC ). In addition to owning and leasing space on traditional cell towers, CCI has a significant focus on small cells, which are smaller fiber-connected antennas that amplify tower signals and expand wireless data capacity, particularly in urban areas with high usage and complicated topographies. CCI also owns a number of dark fiber networks and provides various installation and monitoring services for internet access, networking, and security.

Since inception, CCI, AMT, and SBAC have mostly tracked each other in total returns, with SBAC currently enjoying the fastest growth rate but paying a lower (and quickly growing) dividend that was instituted in 2019. SBAC is a wonderful company and by many measures the best-performing cell tower REIT, but even at its astronomical dividend growth target of 20% per year, its 0.97% current yield would take over 8 years to reach a yield-on-cost matching CCI's current 4.30% yield -- at which point CCI's yield-on-cost would be 7.39% at its current 7% dividend CAGR. Comparing these three companies might be the focus of another article, but because my Ultra High DGI Portfolio contains both AMT and CCI and much of my focus is on CCI's current yield and income growth potential, I'll omit SBAC from my comparisons here.

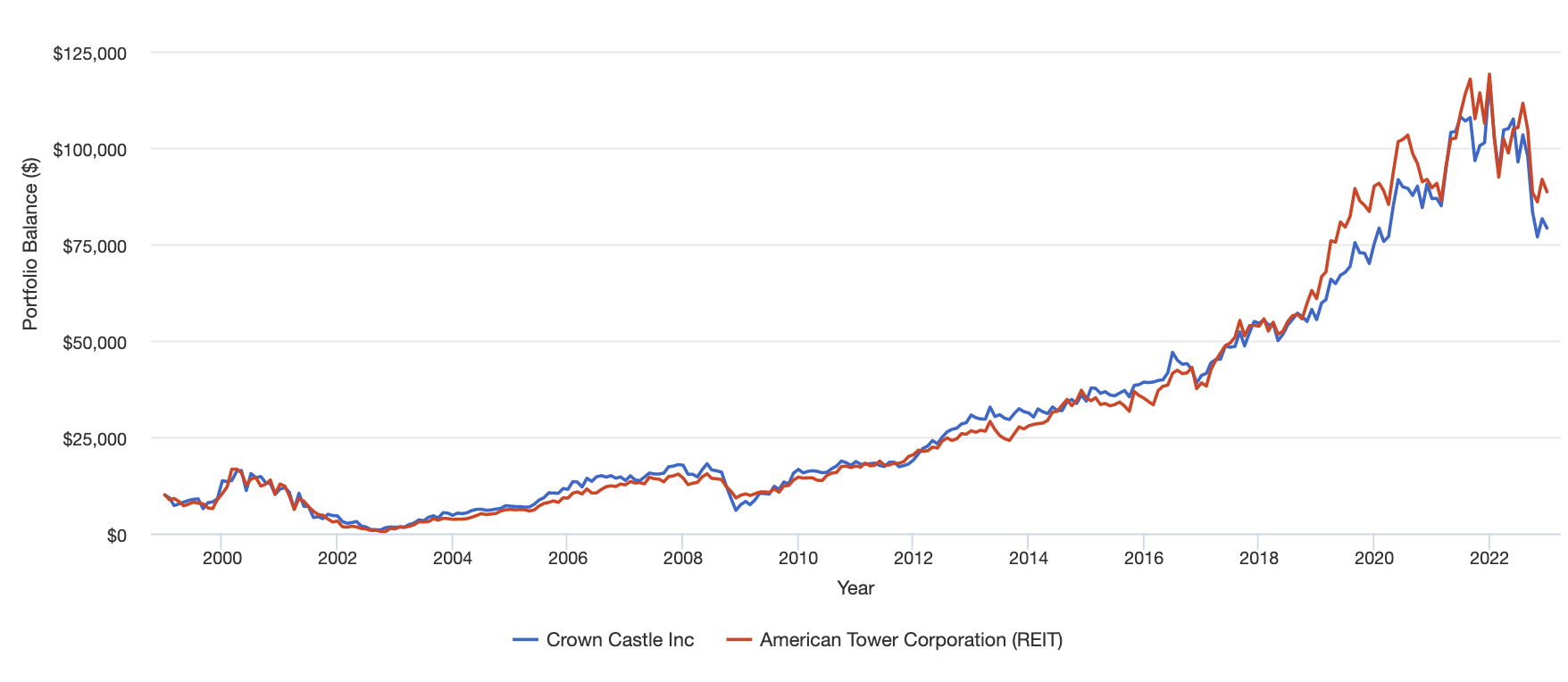

Speaking of AMT, let's take a look at how extremely closely CCI and AMT have tracked each other since CCI's inception with dividends reinvested:

CCI vs AMT Total Return Chart (portfoliovisualizer.com)

{kind=link}

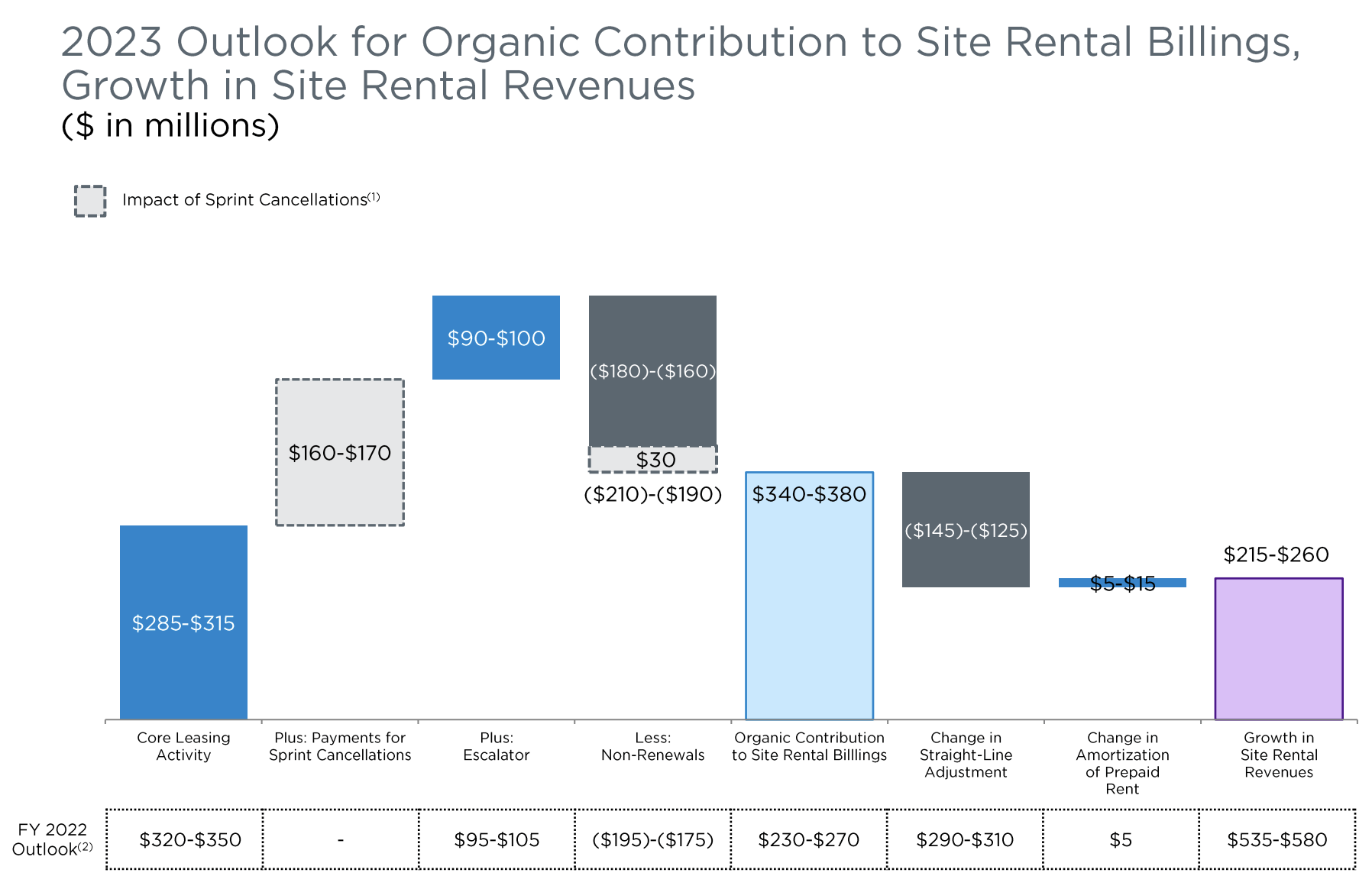

As we can see, CCI has either kept pace with or slightly outperformed AMT for most of its history up until 2019, at which point AMT pulled ahead, most likely due to CCI's slowing growth rate. CCI's bet on fiber-connected small cells, 5G, and the Internet of Things ('IoT') hasn't played out as optimistically as the company originally hoped for, with carriers taking longer than expected to build out their 5G networks and now planning to reduce capex in 2023 in the face of drastically higher interest rates and a deteriorating economic outlook. Furthermore, T-Mobile's ( TMUS ) acquisition of Sprint and its subsequent network consolidation led to churn on CCI's large tower rental revenue and the cancellation of a large and highly publicized order of small cells ordered by T-Mobile prior to the merger. In its latest 2023 outlook, CCI estimates the negative net impact from the Sprint cancellations at $160-170M.

{kind=link}

Fortunately, at the beginning of 2022 CCI was able to work out a new 12-year agreement with T-Mobile that included annual $10M cancellation payments to help offset the Sprint losses, $250 million in site rental revenue in 2022, as well as a new order for 35,000 small cells. This comes on top of their 2021 deal with Verizon ( VZ ) for an initial order of 15,000 small cells to build out VZ's 5G infrastructure. So while CCI's business momentum took a large hit and will be digesting about $45 million from Sprint's small cell churn in 2023 and an estimated $200M in reduced site rental revenue in 2025, it managed to save face and limit what was initially estimated to be a $500M loss.

In short, CCI's small cell business outlook and the financial impact from Sprint appear better than they did at the end of 2021, but of course they are still not great, and any silver linings have been more than overshadowed by the horrible macro environment of 2022, which decimated CCI's share price, taking it from a high of $209 at the end of 2021 to a low of $122 in October 2022. Shares have since rebounded quite nicely and now sit at $146.

{kind=link}

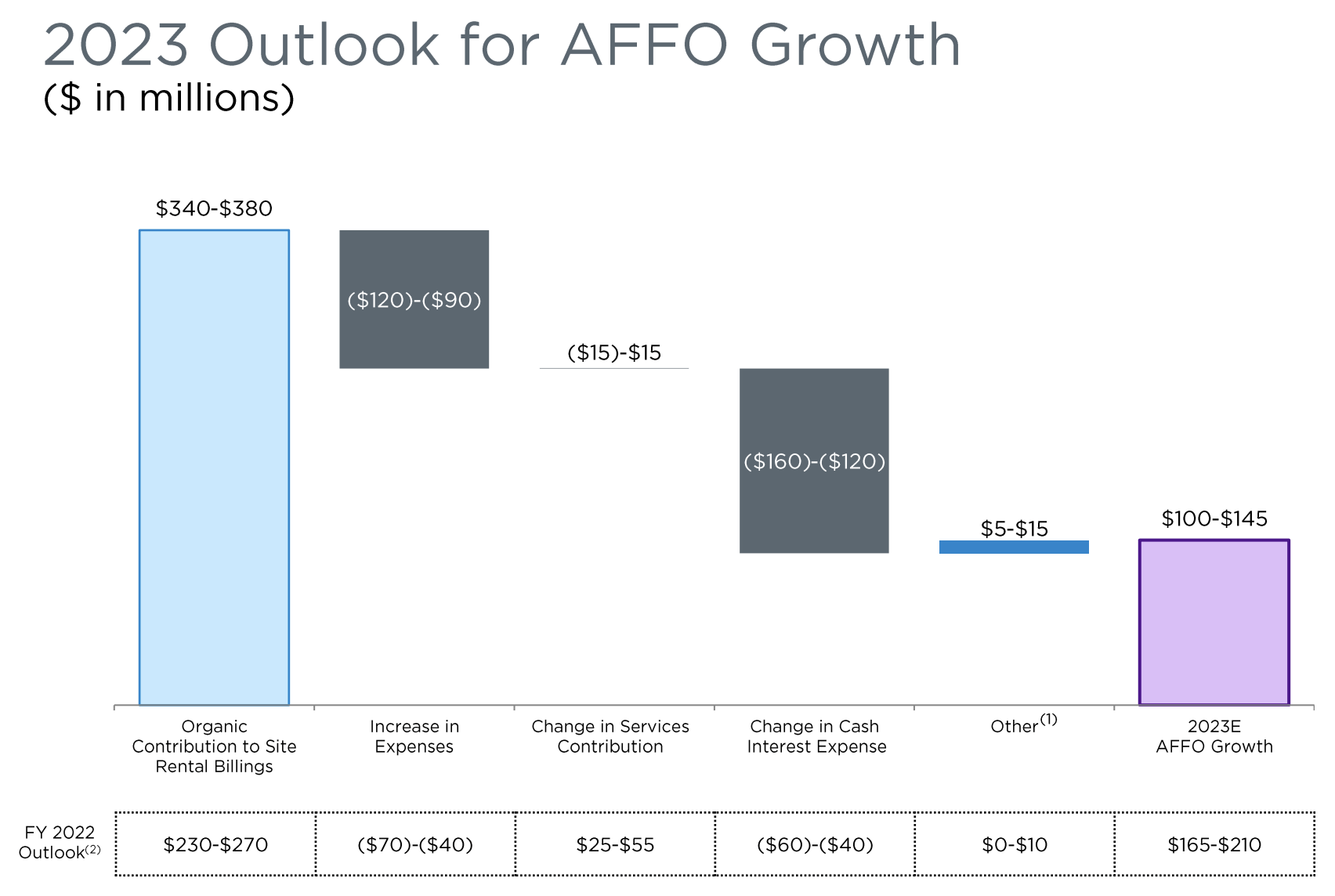

Looking above at the breakdown of its projected 4% AFFO growth in 2023, it's obvious that inflation and high interest rates are going to eat into CCI's net margins and limit its growth potential until the macro environment improves and rates and inflation fall again. 2025 will be another difficult year with the Sprint churn, but both management and the market have already set low expectations for the stock, halving its projected AFFO growth from historical levels and nearly halving its share price from peak to trough. And now that inflation seems to be declining, hopefully CCI's increase in expenses might subside faster than its large increase in interest expense.

But considering high inflation and reduced capex expectations from carriers, I think CCI's 2022-2023 outlook of 10% combined AFFO growth is perfectly respectable and a positive outcome for investors considering what might have been had the new agreement with T-Mobile not materialized.

{kind=link}

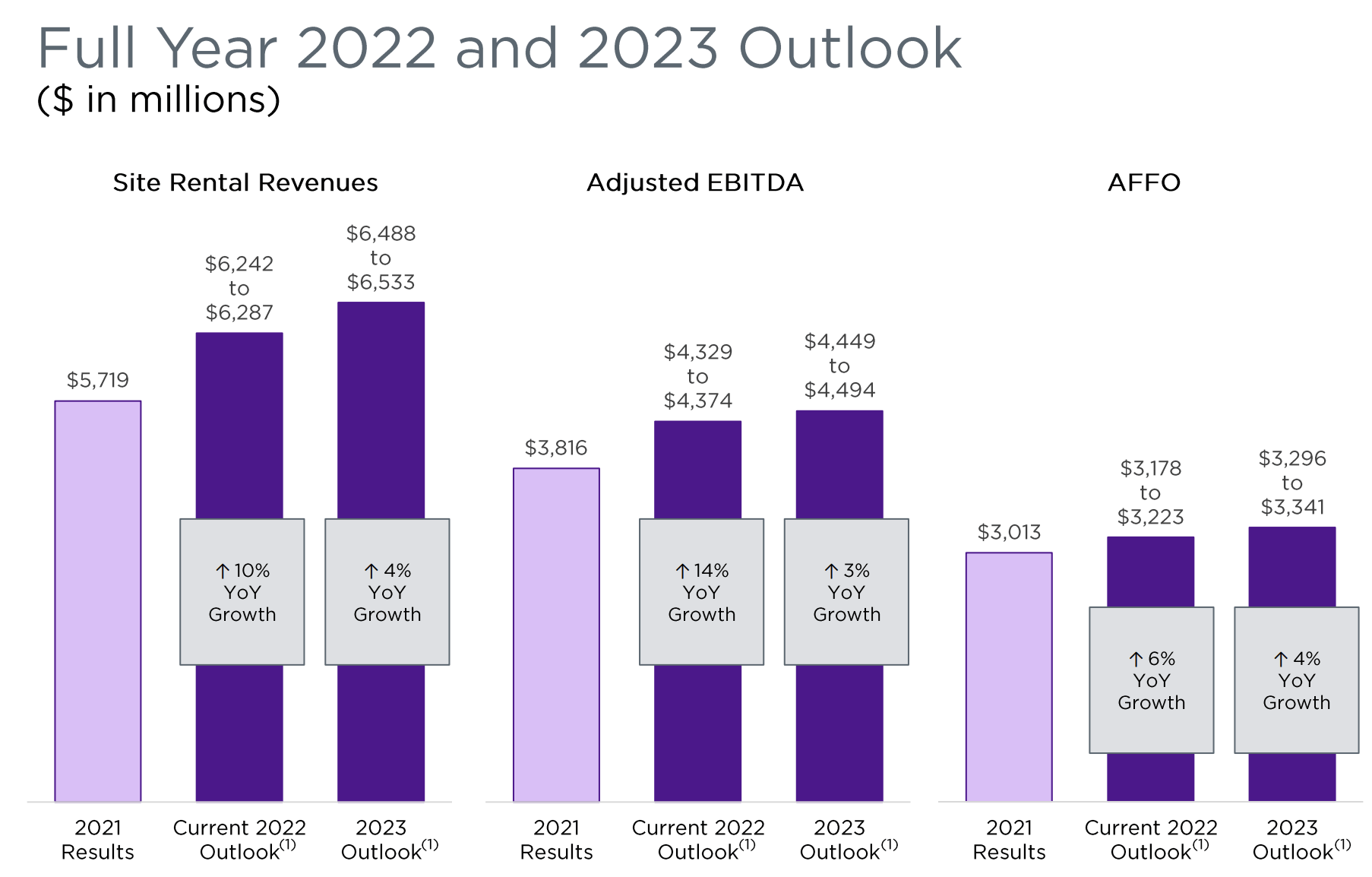

Note that the company's current 2022 outlook from its Q3 report is higher than the company's 2022 outlook from a year ago while its 2023 outlook is unchanged. This gives me some confidence that management is being conservative with its projections, and we may see a bit of upside to the 2023 outlook if the macro picture improves (i.e., if the Fed signals an end to interest rate hikes sometime in 2023).

Finding A Bottom Via Dividend Growth

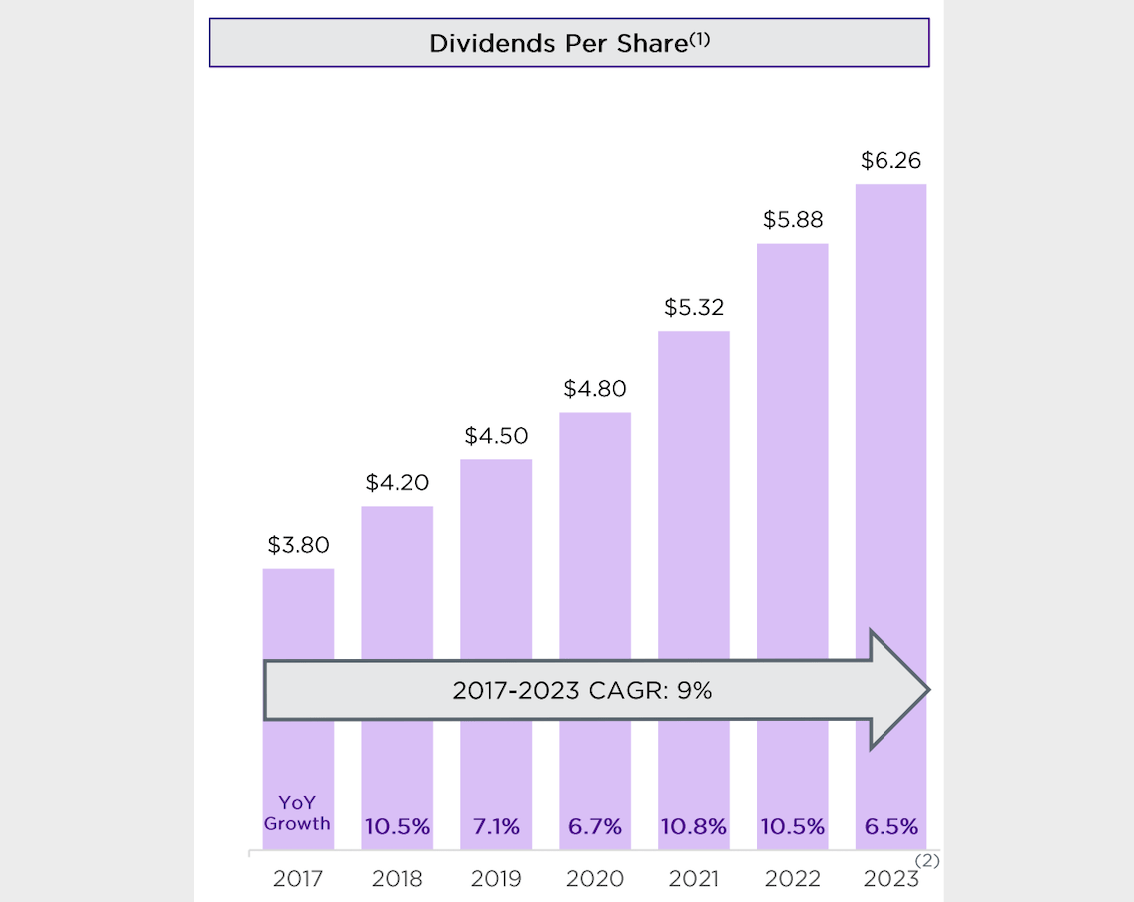

Since most of the revenue loss from the Sprint churn will be absorbed in 2025, CCI has already forecast that 2025's dividend growth will be below its 7-8% annual target. It's latest dividend hike in October was also technically lower than this range at 6.5%, but in line with its historical raises and quite welcome after a tough year, with CCI's forward yield jumping from 4.94% at the time of the announcement to its current level of 4.3%. This year's raise was especially strong in light of the fact that the previous two raises were 11% each in 2021 and 2020.

{kind=link}

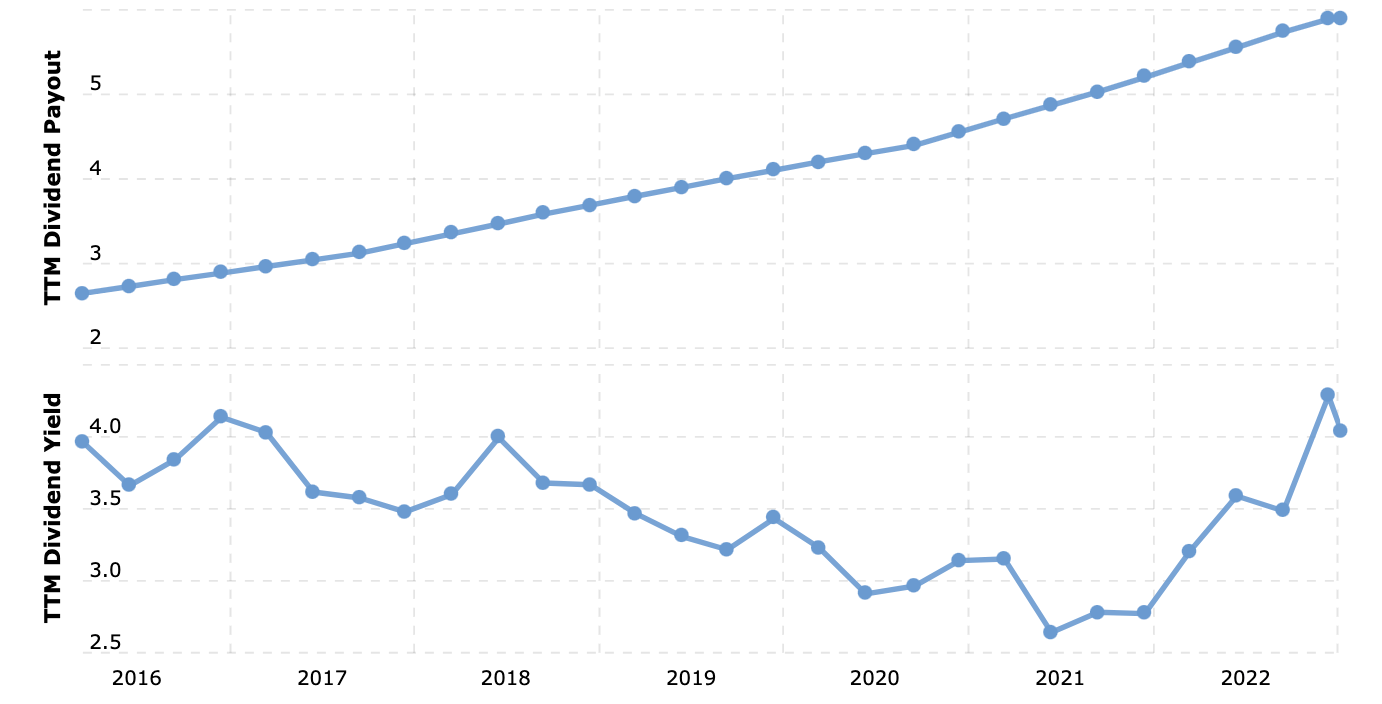

With the terminal Fed funds rate now projected at 5.25%, I think CCI's yield and share price likely bottomed in October. While Treasury yields may be "risk-free", they do not offer dividend growth, so one way to value dividend growth stocks as interest rates rise is to ask how long you would have to hold the stock to earn a superior yield on cost compared to the Fed funds rate. I don't think it's entirely a coincidence that CCI bottomed at almost the exact price ($120) where its then-current yield of 5% multiplied by its expected ~6% dividend growth rate equaled a one-year projected yield on cost (5.3%) that exceeds the terminal fed funds rate.

CCI Historical Yield (macrotrends.com)

{kind=link}

Although its yield is no longer hovering around 5% like it was in October, CCI's current yield of 4.3% is still near the upper end of its historical range (not surprising given higher interest rates), and its forward AFFO payout ratio of 82%, while admittedly a bit high, is still perfectly acceptable for a 4%+-yielding REIT and should be sustainable given the lower dividend CAGR the company has forecast through 2026 combined with its projected AFFO growth of 4%.

{kind=link}

Over the years, CCI's management has shown that it is both conservative in its projections and dedicated to keeping its dividend growth at the highest sustainable rate, so I trust that once they make it through this difficult low-growth period the dividend will rise along with the company's growth rate as it has in the past.

Conclusion

In such a difficult environment for tech-exposed real estate subsectors like cell towers, data centers, and office buildings, I think the fact that CCI is projecting any growth at all in 2023 should give investors confidence that the company can weather the current storm. Despite reduced carrier capex for the next year or two, 5G and fiber networks will continue to be built out, and the world's need for wireless data capacity and connectivity is only increasing, so CCI still has a long growth runway ahead of it.

Fighting headwinds from Sprint, inflation, and interest rates won't be easy, and it seems that 4% forward AFFO growth and 4-6% dividend growth may be the norm until 2026. Still, I think that the stock is attractive at current levels with a 4.3% yield, and rate CCI a long-term buy for income investors with a tolerance for volatility.

For further details see:

Crown Castle: Slow Growth Outlook Provides A Buying Opportunity