GRFS - CSL Limited: Well Placed To Execute Growth Plans And Generate Shareholder Value

2023-04-12 10:50:20 ET

Summary

- CSL Limited is one of the largest global biotechnology companies globally that specializes in the research, development, and manufacturing of plasma-based therapies, vaccines, and other pharmaceutical products.

- The combination of long-term revenue reacceleration, margin expansion, capacity expansion, and great execution led to shareholder value creation. The resilient nature of the company's products protects it from macro downturns.

- I expect a pivot towards higher growth and profitability that will yield a ~20% return going forward. CSL benefits from long-term competitive advantages and stands out as the best-in-class.

- My bullish thesis forecasts a 20% upside from today's price.

Editor's note: Seeking Alpha is proud to welcome Conviction Research as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Thesis

CSL Limited (CSLLY) leads and will continue to lead the oligopolistic plasma market while it reaccelerates revenue growth and returns on capital. A series of obstacles discussed below have caused returns and growth to suffer but the evidence presented makes an argument for a pivot toward higher growth and capital efficiency going forward. This combination should yield a ~20% return going forward.

Company Overview

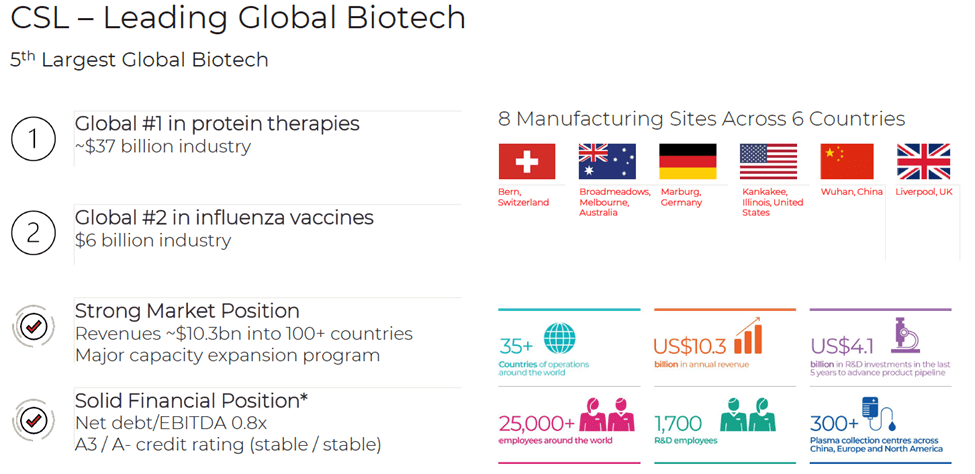

CSL Limited is one of the largest global biotechnology companies that specializes in the research, development, and manufacturing of plasma-based therapies, vaccines, and other pharmaceutical products. The company was founded in Australia in 1916 and has since expanded to become a major player in the global biotech industry, with operations in over 30 countries. It operates two segments, the largest is CSL Behring ( 81% of FY 22 revenue ) which uses plasma-derived proteins to treat conditions including immunodeficiencies, neurological and bleeding disorders. The second segment, CSL Seqirus ( 19% of FY22 revenue ), was acquired by CSL in 2015 and is the second-largest influenza business in the world. Although CSL was founded in Australia, approximately half of CSL's revenue is derived from the US, roughly a quarter from Europe and the rest is diversified.

CSL's primary focus is on the production of plasma-based therapies, which are derived from human plasma, a component of blood. Plasma therapies are used to treat a range of medical conditions, including bleeding disorders, immune deficiencies, and neurological conditions. CSL's plasma-based therapies include immunoglobulins, albumin, and coagulation factors.

Immunoglobulins (IgG, IgA, IgM, IgD and IgE) are the most prominent driver of sales for CSL and this market is structurally growing due to improved affordability and better capability to diagnose conditions.

{kind=link}

Industry backdrop

CSL is one of three leaders (Takeda Pharma (TAK) & Grifols S.A. (GRFS)) that operate in an oligopolistic market structure that is highly vertically integrated. Combine, the three leaders make up roughly 80% of the global plasma market . The main challenge all three leaders face is plasma collection where shortages occur, especially during the COVID-19 pandemic. CSL's plasma collection centers account for 30% of centers globally .

The plasma industry is a highly regulated field while also being an important part of the healthcare sector, with plasma-derived therapies being used to treat a wide range of medical conditions. Plasma is the liquid component of blood, and it contains a variety of proteins and other substances that are essential for maintaining health. Plasma is collected from healthy donors, and the proteins are then isolated and purified to create plasma-derived therapies.

The global plasma industry has been experiencing steady growth in recent years, driven by increasing demand for plasma-derived therapies and the development of new treatments. While the COVID-19 pandemic has disrupted some aspects of the plasma industry, the long-term growth prospects for the sector remain positive.

Long-term competitive Advantage

CSL's sustained track record of high returns on capital (15%+) demonstrates its ability to maintain its competitive advantages over peers and entrants in the market. The barriers to entry into this business are high mainly due to scale advantage forged by extensive coverage of plasma collection centres and the intellectual property developed over years of high-quality R&D. Another contributing factor to the economic moat is the complexity of the fractionation process. Plasma fractionation is a process that involves separating different components of blood plasma, which is the clear liquid portion of blood, into individual protein products. The process starts with the collection of blood from donors, which is then centrifuged to separate the plasma from the blood cells. The plasma is then subjected to a series of purification steps to isolate specific proteins, such as immunoglobulins, clotting factors, albumin, and others. As you can imagine, plasma fractionation is highly regulated and subject to strict quality control standards to ensure the safety and efficacy of the end product.

What will drive shareholder value in the future

According to CSL's management , Plasma collections continue to rise and have already surpassed pre-pandemic levels by 10%. As discussed earlier, volume is imperative in this business and I forecast a 2.5-3.5% increase in gross margins as a result of CSL's pricing power and the reduction of cost per litre of plasma. CSL put the following three initiatives in motion to reaccelerate its gross margins: 1) Donor mix management, 2) Improvement in plasma fixed cost per unit and 3) Improvement in efficiencies (such as digital and time it takes to donate). In fact, CSL's new technologies allow for ~30% lower donation time and use technology to optimize the yield per donor. The market is keeping a close eye on the plasma business margins as well as collection levels in the forthcoming quarters.

The plasma industry has faced supply constraints and CSL is bringing more base-fractionation capacity online. This will likely lead to an increase in market share up to ~38% and further contribute to its cost leadership in plasma product margins. Commonly in the plasma business, donors are under-employed (roughly 75% of them) and this ensures consistent willingness of donors to continue donating as the additional income is valuable, more so in difficult economic conditions.

Revenue growth will be supported by the actualization of an underpenetrated market. Demand for IG is rising structurally as it's used to treat new diseases. In fact, several market research providers such as Allied Market Research forecast the industry to grow ~9% annually until 2031.

I expect CSL's acquisition of Vifor to be value accretive for shareholders as it integrates well with the business and brings synergies to the model.

Company Performance:

BBG consensus Estimates BBG consensus estimates

{kind=link}

{kind=link}

*All figures are in unless stated otherwise.

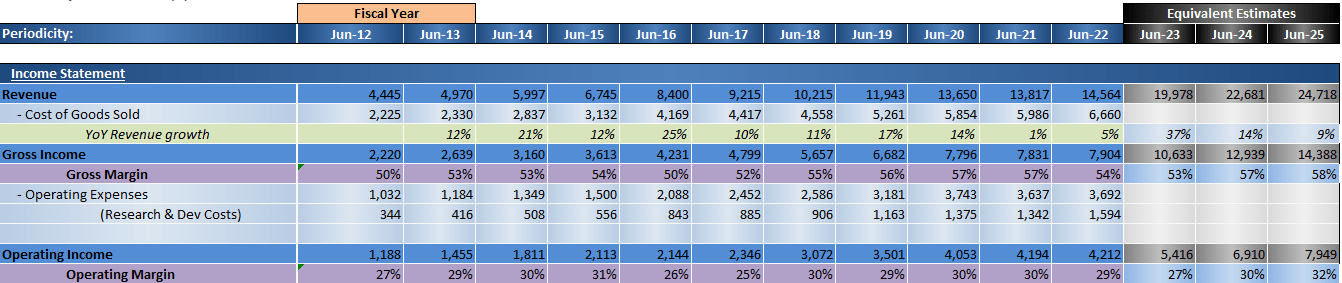

Over the past 5 years CSL has grown revenue at a cadence of 9%, EPS by 11% and FCF by ~20% per annum. BBG consensus estimates are in line with my expectations for revenue, profitability and FCF growth. The main reasons cited for these optimistic statements are: First, improvements in growth after covid ramifications. Second, margin improvements from capacity improvements, easing supply chain bottlenecks and improved efficiencies. Finally, FCF will begin to improve next year as capital expenditures will normalise.

CSL generates sufficient cash flow to fund business operations, expansion and shareholder returns. Importantly though, cash conversion suffered over the past 5 years due to the company's more demanding working capital requirements driven by capacity expansion and R&D spending. Excess cash is being returned to shareholders mainly through dividends, with a payout ratio of ~45% over the past 10 years. After the acquisition of Vifor Pharma, leverage rose to ~2x EV/EBITDA which is above the company's very healthy target of 1-1.5x. The target is expected to be reached in 2025.

CSL's resilient business model is supported by strong capital allocation decisions made by its remarkably experienced management team. The new CEO, Paul McKenzie (ex-COO since 2019 and previously at Biogen) is deeply experienced in the field and I believe is capable to steer the company successfully.

CSL is consistently investing about 10% of its revenue in R&D to protect itself from emerging technologies that could disrupt its model but has also been active on the acquisitive front. Besides the recent Vifor acquisition, CSL also bought the gene therapy platform Calimmune in 2018 and UniQure haemophilia B gene therapy player in 2020.

CSL has exhibited consistently best-in-class economics. The company extracts 12 products from plasma and it generated $540 of revenue per litre in 2022. This is a fraction of the potential $5,000 it could earn if it continues to expand the product range and end-market treatments pick up in demand. Additionally, among the top 3 players, CSL has the best Gross Profit per litre by a wide gap of over 40%.

Besides best-in-class economics, CSL has a competitive advantage flywheel that helps grow its advantage over competitors. The flywheel is as follows: Higher margin due to scale benefits ->competitive pricing under a leading brand name -> more capital for R&D than competitors -> rich pipeline of new products -> FCF growth -> shareholder returns

CSL's investments in capacity and innovation have resulted in a growing number of collection centres combined with more efficient collection. CSL operates 330 plasma centres and will continue expanding its capacity. Capex will continue to grow 9% per annum which will support double-digit revenue growth and mid-teens EPS growth moving forward.

Valuation

DCF Valuation

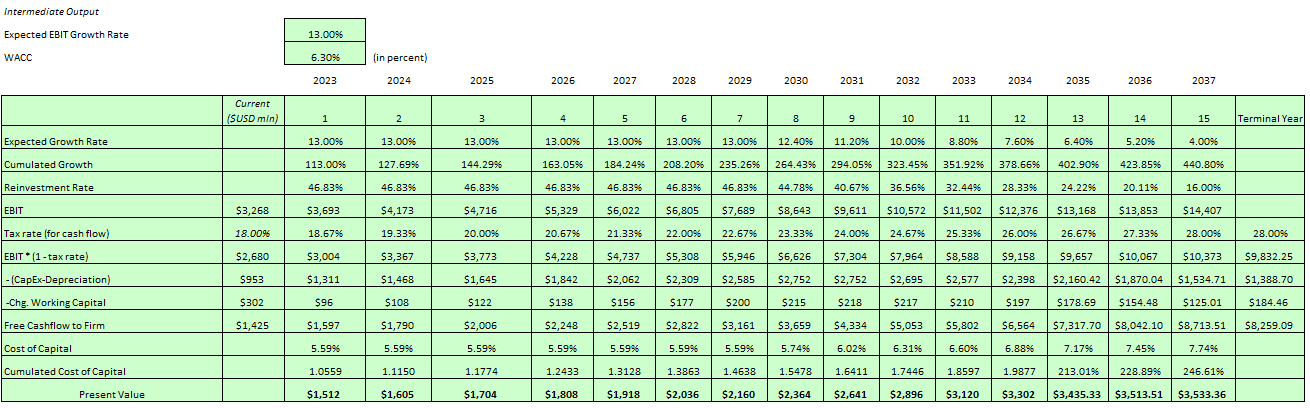

The topics discussed above set the foundations for my modelling assumptions going forward. In summary, my conviction about CSL's competitive position permits long-dated projections about growth, margins and returns going forward. In this case, I model 13% EBIT growth 10 years out, with a continuation of a relatively levered balance sheet (as the current management guides it). My projections diverge from consensus when it comes to the capital intensity of the business. In my opinion, improving supply conditions will trigger angst about oversupply and worries about destruction in pricing. Then, the entire industry will delay immediate plans for big capacity expansions subsequently reflecting positively on returns. Find a snapshot of the DCF and the main assumptions below:

*Note that all figures are in USD and the current exchange rate for AUD/USD is 0.6653. The target price is calculated in and translated into .

Author's Projections

{kind=link}

Assumption reasoning and target price

13% EBIT growth: The revenue growth drivers cited above and CSL's growth plans underpin my assumption for ~11% revenue growth. On top of that, CSL will return to adding incremental profitability via its efficiency improvements and volume recovery. The combination will yield positive incremental contributions to gross and EBIT margins alike to reach 13% EBIT growth annually.

WACC Calculation

Author's calculations

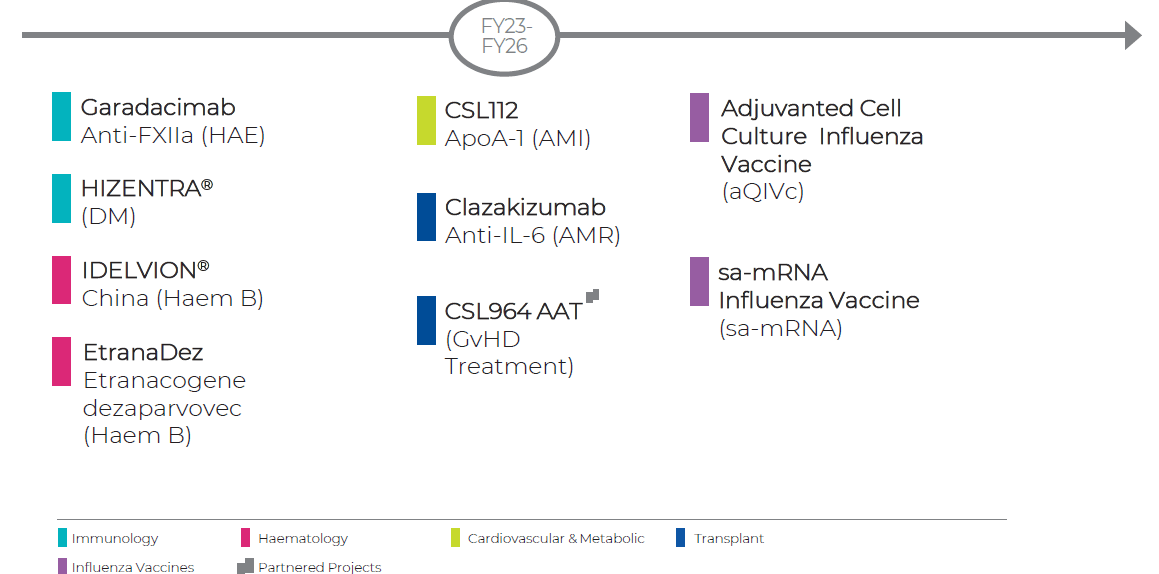

I expect R&D to continue taking up 10% of revenue as it has in the past 7 years. The company has a healthy mix of projects in its pipeline across several product lines as depicted below. In my assumptions, I account for the continuation of a rich pipeline as it will fuel top-line growth.

{kind=link}

Capital expenditure accelerated from roughly 6% of revenue in 2015 to 10% in 2022. Capex fuels the collection centre's growth and will play a crucial role in reinforcing CSL's competitive position as well as growth. However, I expect a normalisation of Capex spending compared to the last three years (Capex was 10%, 12% & 13% of sales in 2022, 2021 & 2020). This is reflected in my assumptions and will consequently boost FCF from 2024 onwards.

The above assumptions yield a target price of ~$358 implying a ~20% upside from current levels.

Relative Valuation

CSL trades at a significant premium to peers considering its solid leadership position and the barriers to entry discussed earlier. It's rare to find companies of CSL's calibre trading at a significant discount, and this is no exception. The table below illustrates CSL's current premium to peers. Across all 12-month forward-looking valuation metrics listed below, CSL is trading at a significant premium. This premium is justified by CSL's market leadership and its ability to generate superior operational and capital efficiency. I expect this gap to competitors to widen going forward and the company to continue dominating the plasma industry. The fundamentals underpinning CSL's valuation support the chunky premium over its peers and don't overshadow my conviction in the long-term prospects.

{kind=link}

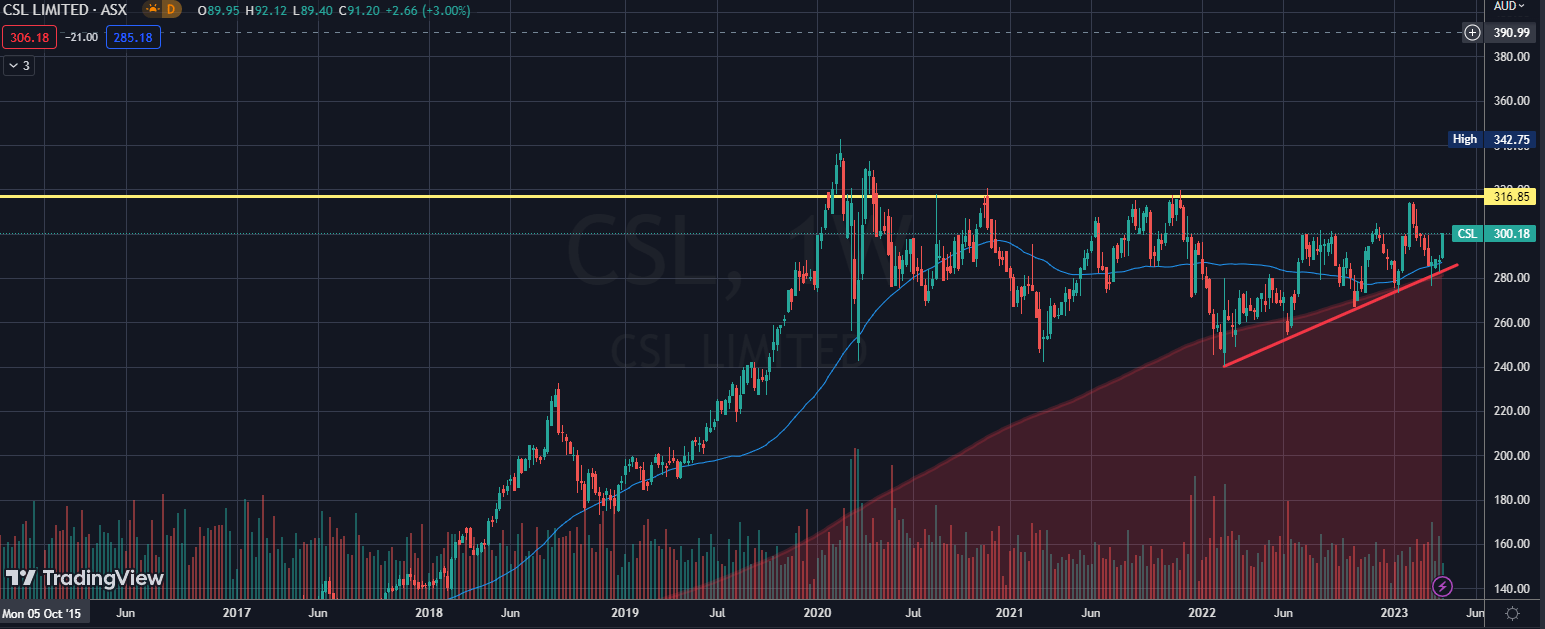

Technical Analysis

The trendline, 50MA & 200MA will likely act as support for the continuation of CSL's long-term trajectory. The medium-trend trendline (in red) proved to be a strong support throughout 2022 and will likely continue. Recently it bounced off the trendline with strong buying volume, and that is another good sign. It will be important to keep an eye on the yellow resistance line at about $318 which crippled the bullish activity over the past 40 months. The ascending trendline, strong buyer volume, fundamental strength and 200MA make me optimistic about a breakout above $320.

{kind=link}

Risks

CSL invests significant capital in R&D for projects in its core business line, plasma, as well as many other areas to enhance growth and diversify revenue. I expect CSL to invest between $5 billion and $7 billion in R&D. In case competitors such as Grifols have better success in their R&D pipeline, this will likely narrow the profitability gap and CSL will be caught on the back foot.

Competitive pressures are likely to continue as peers such as Grifols plan to expand their network of collection centres to over 500 by 2026. If the capacity expansion continues for a prolonged period at its current pace, prices per litre (plasma) will fall and this will have a negative impact on the profitability across all peers in the industry.

The new CEO faces a difficult challenge in integrating the Vifor Acquisition and executing the outlined growth plans. Vifor is CSL's largest acquisition to date and management is tasked to integrate the businesses in a value-adding manner. Any indication of long cost drags may weigh on profitability and pose a risk to my thesis.

Conclusion

I have conviction in the ability of CSL's management to execute their growth strategy, further expand profit margins and fend off competitive pressures as they have done for over two decades. The thesis presented above supports double-digit revenue growth, mid-teen EPS growth and strong FCF growth to ~$5.3 billion in 2025. My target price using a DCF approach is $358, implying a ~20% upside from current levels.

For further details see:

CSL Limited: Well Placed To Execute Growth Plans And Generate Shareholder Value