ET - CTR: An Enormous 7.06% Yield At A Cheap Price

2023-07-03 14:26:22 ET

Summary

- Midstream companies are excellent assets for income investors due to their high yields and stable cash flows backed by long-term contracts.

- ClearBridge MLP and Midstream TR Fund Inc. is a closed-end fund that invests in a portfolio of these companies and provides a way to include midstream master limited partnerships in a retirement account.

- There are some reasons to expect energy prices to improve in the near future, which could have a beneficial effect on the fund's assets.

- The fund can easily sustain its current 7.06% yield going forward.

- The fund is trading at an enormous discount.

For a very long time now, master limited partnerships have been a popular investment for those that are seeking to earn a high level of income from their portfolios. This makes a great deal of sense as these companies typically enjoy remarkably stable cash flows over time and pay out a substantial percentage of their cash flows as distributions to their unitholders. In addition to the high yields, the distributions enjoy certain tax advantages that effectively make them even more attractive than other companies that may have similar yields. Unfortunately, these nice things come with a problem as including these assets in a tax-advantaged account like an individual retirement account can expose the investor to certain tax consequences despite the inherent protection of the account.

Fortunately, there are a few ways around this problem. One of the best ways is to purchase shares of a closed-end fund, or CEF, that specializes in master limited partnerships. These funds are typically structured as corporations, so all tax problems are handled on the corporate level. This allows them to be put into tax-advantaged accounts just like anything else. In addition to this, these funds provide investors with a diversified portfolio of assets with one simple purchase, which is a very nice advantage over just purchasing companies individually. Finally, closed-end funds are able to employ certain strategies that can boost their effective yields well beyond that of any of the underlying assets. When we consider that many master limited partnerships have higher yields than just about anything else in the market, to begin with, we can see a lot of income potential here.

In this article, we will discuss the ClearBridge MLP and Midstream TR Fund Inc. ( CTR ), which is one CEF that falls into this category. As of the time of writing, this fund yields 7.06%, which is reasonable but admittedly not jaw-dropping for this sector. We have discussed this fund before (see here and here ), so this report will primarily address the changes that have occurred since then. As is the case with most midstream funds, this fund is currently trading at an enormous discount to its intrinsic value so it makes a rather appealing case for a value investor. Let us proceed onward and see if this fund could be a good fit for your portfolio today.

About The Fund

According to the fund's webpage , the ClearBridge MLP and Midstream Total Return Fund has the stated objective of providing its investors with a combination of income and capital appreciation. This objective fits pretty well with the "total return" component of the fund's name. It also makes a lot of sense for a fund that invests in the common equity of midstream companies and master limited partnerships. As we can clearly see here, the fund's portfolio currently consists entirely of common equity, along with only a small allocation to cash:

CEF Connect

The reason that this objective is not surprising is that common equity is a total return vehicle. After all, investors typically purchase common equity in order to receive income via the dividends and distributions that these securities pay out as well as benefit from capital gains as the issuing company grows and prospers. In the case of midstream companies, the dividends and distributions are typically a large reason why investors purchase these entities as their growth tends to be lower than companies in certain other sectors. The fund itself realizes this, as it does specifically state that it will aim to deliver its total returns primarily through the distributions that it collects from its portfolio companies and then pay them out to the shareholders. Most closed-end funds pay out their capital gains too, aiming to keep a relatively steady asset base. Master limited partnerships are interesting here, too, because the distributions can be considered capital gains in certain circumstances, so naturally the fund aims to pay out a large percentage of those.

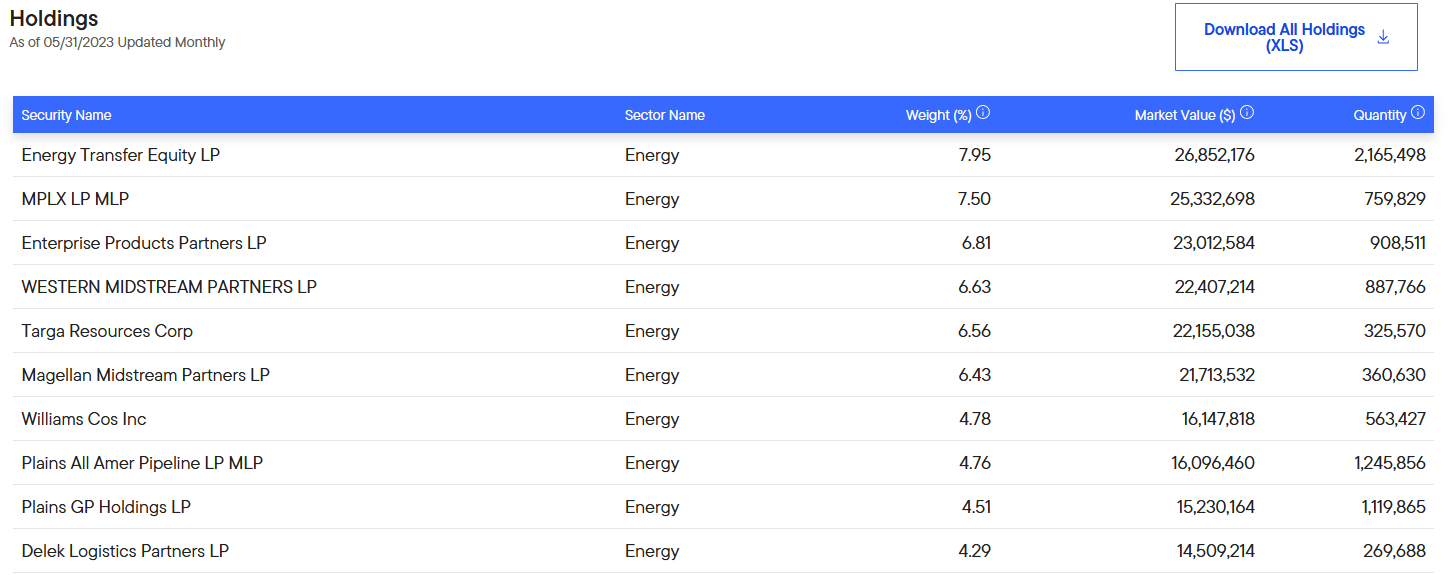

As my regular readers are no doubt well aware, I have devoted a considerable amount of time and effort to discussing midstream master limited partnerships here at Seeking Alpha and elsewhere. As such, the majority of the fund's largest positions will be familiar to most readers. Here they are:

{kind=link}

I have discussed the majority of these companies numerous times in the past, so they should undoubtedly be familiar to most of you. In fact, the only company here that I have never discussed is Western Midstream Partners ( WES ), but it is a very common holding among the largest positions in most midstream funds. I have also never specifically discussed Plains GP Holdings ( PAGP ), but that is simply the general partner of Plains All American Pipeline ( PAA ) so it is pretty similar to the latter company. For the most part, this list includes most of the best companies in the industry but I will admit that I would rather see Crestwood Equity Partners ( CEQP ) in place of one of the Plains All American companies. As it stands right now, Plains All American Pipeline and its general partner account for the single largest position in the fund, but it is certainly not a better investment than Energy Transfer ( ET ) or MPLX LP ( MPLX ). This is something that the fund will hopefully correct at some point.

In the introduction to this article, I stated that midstream companies and master limited partnerships tend to enjoy remarkably stable cash flows over time. This comes from the basic business model that these companies employ. In short, these companies enter into long-term contracts with their customers under which the company provides transportation for hydrocarbon resources on behalf of the customers. In exchange, the customer compensates the midstream company based on the volume of resources that are transported, not their value. This provides a great deal of protection against commodity price fluctuations, especially since most of these contracts specify a certain minimum volume of resources that must be transported or paid for anyway. This business model is the reason why most of these companies did not actually see their cash flows decline during 2020 despite the fact that West Texas Intermediate crude oil prices went negative very briefly. I mentioned this in multiple previous articles.

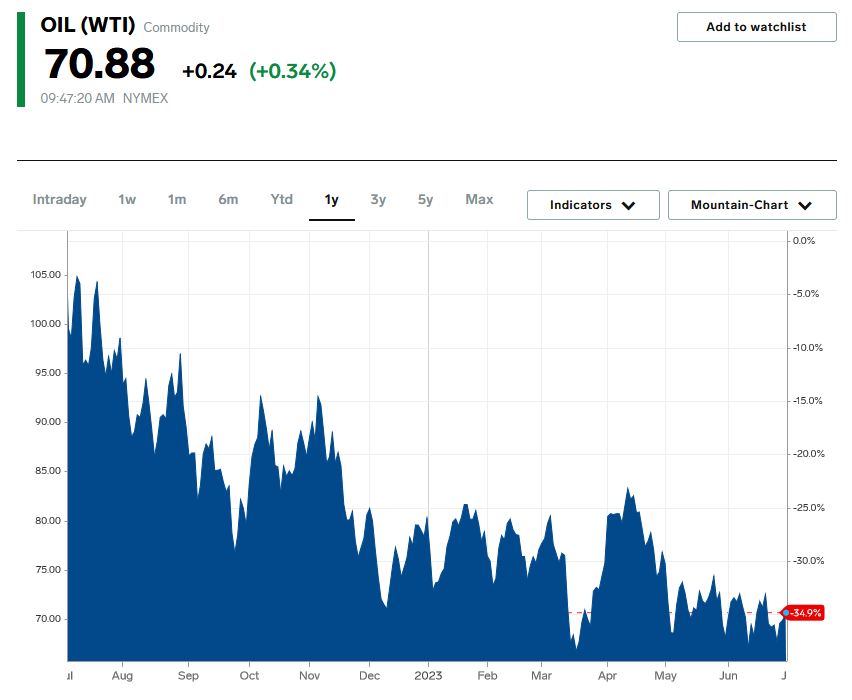

With that said, we do see the market prices of many of these companies move in correlation to energy prices. This is important because crude oil prices have generally been much weaker this year than they were last year. As we can see here, the price of West Texas Intermediate crude oil is down 34.90% over the past twelve months:

{kind=link}

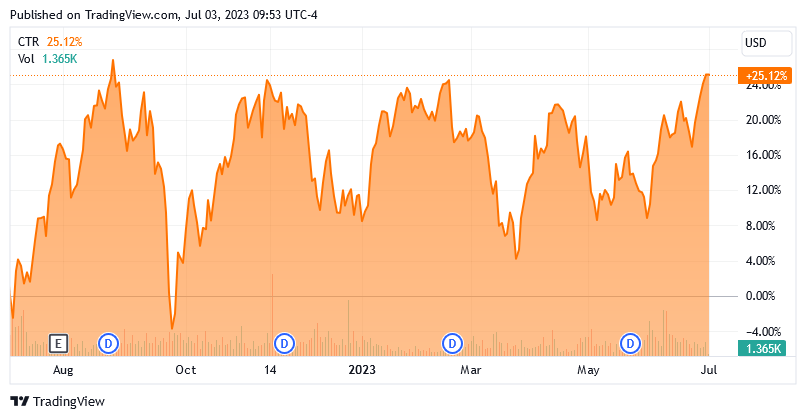

However, this has not had a noticeable effect on the share price of the ClearBridge MLP and Midstream Total Return Fund. In fact, the fund is up a whopping 25.12% over the time period:

{kind=link}

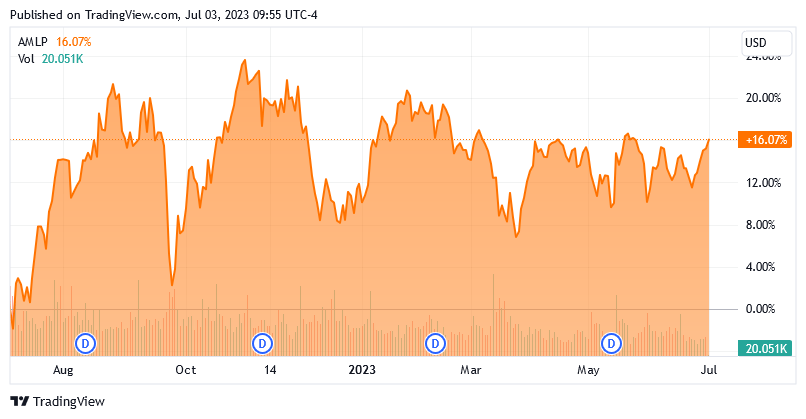

This is probably because the fund has been steadily increasing its distribution on a quarterly basis over the same period and was massively sold off during 2020 when anything related to the energy sector was considered toxic. We see the same thing with the Alerian MLP Index ( AMLP ), which is up 16.07% over the same period:

{kind=link}

This sort of thing is unusual though as normally these companies do tend to trade in line with energy prices. While it is possible that the market has realized that their cash flows are independent of energy prices, that seems unlikely. It is also possible that a rush to yield is going on right now, but that is highly unlikely considering that safe money market funds are yielding above 5% right now, so a 7% or 8% yield from a midstream company should not be as appealing as it once was.

With that said, there are some forces trying to force crude oil prices up, which may be causing some expectations that the sector will grow. Early today, Saudi Arabia announced that it will be extending its production cuts until at least August. I discussed these cuts in a blog post earlier this year. In short, Saudi Arabia seems to be trying to force crude oil up above $70 per barrel by reducing its production by one million barrels per day starting this month. It certainly had an impact this morning, as crude oil prices jumped in pre-market trading:

Zero Hedge

Saudi Arabia is hardly alone in this attempt to pressure prices upward. Russia also announced this morning that it will be reducing its exports of crude oil. As I have noted before, the sanctions on Russia had little impact on crude oil prices because China, India, and a few other nations have been ignoring the sanctions and purchasing Russian crude oil anyway. The aim here is to prevent the world from being oversupplied with crude oil. If it works, we could see oil prices continue upwards and that will probably benefit the fund despite the fact that midstream companies do not see their cash flows increase very much with energy prices.

With that said, we might see increased growth rates from the companies in the fund's portfolio if energy prices do increase on a sustained basis. This comes from the fact that upstream energy companies will frequently boost their production in order to take advantage of high energy prices. This will result in increased volume for midstream companies because it is pointless to increase production if there is no way to get the incremental resources to the market in order to sell them. As the cash flows of midstream companies directly correlate with the volume of resources transported, this should result in growing cash flows. However, as I have mentioned in various previous articles, many American energy producers have been opting to either keep their production steady or limit their growth in order to avoid oversupplying the market and crashing energy prices. In fact, American crude oil production is currently lower than it was throughout much of 2019 and 2020 so that is clear evidence of this. As such, we might not see an enormous amount of growth from the companies in this fund even if the efforts by the Saudi Arabians bear fruit and cause energy prices to increase on a sustainable basis.

As my long-time readers on the topic of closed-end funds are no doubt well aware, I do not generally like to see any single asset in a fund account for more than 5% of the fund's total assets. This is because that is approximately the level at which an asset begins to expose the portfolio to idiosyncratic risk. Idiosyncratic, or company-specific, risk is that risk that any asset possesses that is independent of the market as a whole. This is the risk that we aim to eliminate through diversification, but if the asset accounts for too much of the portfolio then it will not be completely eliminated. Thus, the concern is that some event may occur that causes the price of a given asset to decline when the market does not, and if that asset accounts for too much of the portfolio then it may end up dragging the fund down with it. As we can clearly see above, there are six companies in the portfolio that currently exceed this 5% threshold. In addition, the two Plains All American companies combined exceed the threshold so in reality we have seven companies that are exposing the fund to idiosyncratic risk. Anyone should be willing to be exposed to the risks of holding these companies individually before taking a position in the fund.

Leverage

In the introduction to this article, I stated that closed-end funds such as the ClearBridge MLP and Midstream Total Return Fund have the ability to employ certain strategies that have the effect of boosting their yields beyond that of most of the things in the market as well as the underlying assets. One of these strategies is the use of leverage. In short, the fund borrows money and then uses that borrowed money to purchase the common equity of midstream corporations and partnerships. As long as the interest rate that the fund pays on the borrowed money is lower than the yield of the purchased assets, this strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing at institutional rates, which are considerably lower than retail rates, this will usually be the case. With that said, this strategy is not as effective today as it was when interest rates were at 0% but most midstream companies still have high enough yields for this strategy to work.

However, the use of debt in this fashion is a double-edged sword. This is because leverage increases both gains and losses. As such, we want to ensure that the fund is not using too much leverage because that would expose us to too much risk. I do not typically like to see a fund's leverage exceed a third as a percentage of its assets for this reason. As of the time of writing, the ClearBridge MLP and Midstream Total Return Fund has levered assets comprising 28.61% of its portfolio so it appears to be meeting this requirement. Thus, it appears that this fund is striking a reasonable balance between risk and reward.

Distribution Analysis

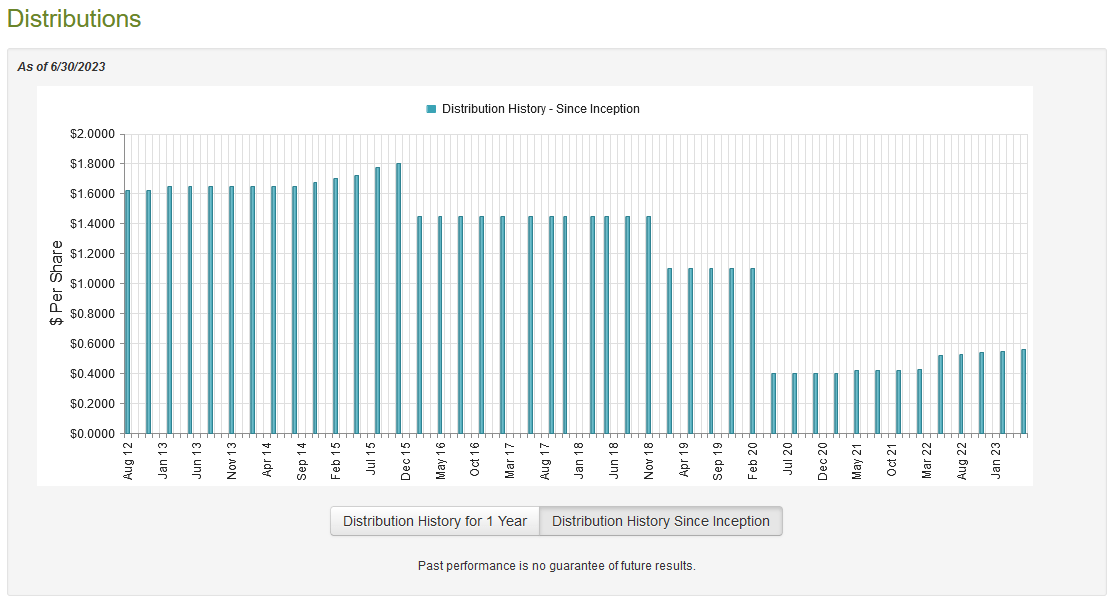

As mentioned throughout this article, one of the biggest reasons why people invest in midstream master limited partnerships and corporations is because of the high yields that these entities normally possess. This comes from the fact that these companies tend to possess relatively low growth rates, so they pay out a high proportion of their cash flows as distributions to the investors. In addition, the market does not normally assign high multiples to these companies so the distribution ends up being a high percentage of the market price. The ClearBridge MLP and Midstream Total Return Fund assembles a portfolio of these entities and then applies a layer of leverage to boost their yields beyond that of the underlying assets. As such, we can assume that this fund would have a high yield itself. This is indeed the case as it currently pays a quarterly distribution of $0.56 per share ($2.24 per share annually), which gives it a 7.06% yield at the current share price. The fund has unfortunately not been especially consistent with its distribution over the years, as can be clearly seen here:

{kind=link}

This history is quite likely to be a turn-off to those shareholders that are seeking a safe and secure source of income to use to cover their bills and finance their lifestyles. It is not unexpected however, as many midstream funds have a similar distribution history. This is particularly true with the distribution cuts in 2015 and in 2020. As some of you may recall, these were both extremely challenging periods of time for the midstream sector that led to a number of lasting changes in the sector. In particular, we saw some midstream companies convert to corporations and others cut their distributions in order to pay down debt and reduce their dependence on the market. In both cases, the lesson that these companies learned is that the market can be quite hostile to fossil fuel companies at times, so it is important that they do not rely on it as a source of capital. As these events caused the fund to take some capital losses and reduced the money that comes in, it was forced to reduce its distributions to avoid paying out too much and destroying its asset base.

With that said, any investor that is purchasing the fund today will not be affected by the fund's past history. This is because anyone buying the fund today will receive the current distribution at the current yield. As such, the important thing for anyone buying today is the fund's ability to maintain its current payout.

Unfortunately, we do not have an especially recent document that we can consult for the purposes of our analysis. The fund's most recent financial report corresponds to the full-year period that ended on November 30, 2022. As such, it will not include any information about the fund's performance over the past seven months. This is unfortunate because the energy sector in general has been somewhat weaker over the first six months of this year than it was throughout most of 2022. With that said, we should still get a good idea of how well the fund managed to take advantage of the improvements in the sector last year as well as how well it handled the general decline in energy prices that started last summer. During the full-year period, the Clearbridge MLP and Midstream Total Return Fund received $22,349,956 in dividends and distributions along with $65,461 in money market fund distributions. However, a large percentage of this was paid to the fund by the master limited partnerships in the portfolio. This money is not considered investment income for accounting purposes, so the fund only reported a total investment income of $5,256,493 during the period. It paid its expenses out of this amount, which left it with a $6,094,349 net investment loss. This was obviously not enough for any distributions, but the fund did pay out $14,182,061 to the shareholders over the period. At first glance, this might be concerning because the fund clearly did not have sufficient net investment income to cover its distributions.

However, this fund does have other ways to obtain money besides just net investment income. As already mentioned, the fund received $16,963,024 in distributions from the master limited partnerships in its portfolio. That money is not considered to be investment income, but it was enough to completely offset the net investment loss and most of the distributions. In addition to this, the fund was able to generate capital gains during the period. It reported net realized gains of $11,943,682 and had another $74,041,607 in net unrealized gains. That all was clearly more than enough to cover the distributions that it paid out over the same period with a substantial amount of money left over. In fact, the fund was able to pay its distributions, do a share buyback, and still had its assets increase by $63,592,954 over the period. As that alone is enough to cover a few years of distributions, it appears as though this fund should have no trouble maintaining the distribution. We have nothing to worry about here.

Valuation

It is always critical that we do not overpay for any assets in our portfolio. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a closed-end fund like the ClearBridge MLP and Midstream Total Return Fund, the usual way to value it is by looking at the fund's net asset value. The net asset value of a fund is the total current market value of all of the fund's assets minus any outstanding debt. This is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can obtain them at a price that is less than the net asset value. This is because such a scenario implies that we are purchasing the fund's assets for less than they are actually worth. This is, fortunately, the case with this fund today. As of June 30, 2023 (the most recent date for which data is currently available), the ClearBridge MLP and Midstream Total Return Fund has a net asset value of $36.93 per share but the shares only trade for $32.00 per share. That gives the fund's shares a 13.35% discount on net asset value at the current price.

This is a very large discount, but it is not as good as the 19.30% discount that the shares had on average over the past month. While it is possible that a better price can be obtained by waiting, frankly a double-digit discount is good enough for me to consider purchasing a closed-end fund. This price is more than acceptable.

Conclusion

In conclusion, the ClearBridge MLP and Midstream Total Return Fund looks like a pretty good way to add some exposure to this high-yielding asset class to your portfolio. There could be some reasons to buy these companies today as Saudi Arabia and Russia are apparently attempting to push up energy prices, and while this does not directly benefit the companies in the fund, it could have some beneficial impact if high prices stimulate production. However, the biggest reason to have exposure to the sector is the high yields that these companies possess. This fund has a reasonable portfolio of most of the best companies in the sector and earned enough money last year to maintain its 7.06% yield for quite a long time. When we combine this with a very attractive discount to the intrinsic value today, ClearBridge MLP and Midstream TR Fund Inc. looks like a winner.

For further details see:

CTR: An Enormous 7.06% Yield At A Cheap Price