CULP - Culp's Fiscal Health: The Rising Net Loss Concern

2023-06-30 13:17:42 ET

Summary

- Culp has shown signs of improvement in its Q4 2023 earnings, with net sales increasing by 7.9% compared to the previous year.

- However, the absence of key profitability indicators and dividends, along with a high Dividend Payout Ratio, suggest that Culp, Inc. is in a precarious financial situation.

- The company faces potential risks including operational losses, lackluster demand in the Residential Home Furnishings industry, and a heavy dependence on macroeconomic recovery.

- The company's current health and bleak performance outlook warrant me to give a sell recommendation on the stock.

Thesis

As the dust settles on Culp, Inc.'s (CULP) latest earnings report , the tenuous state of the company's performance becomes apparent. Reporting an EPS of -$0.37, beating expectations by $0.10, and revenue of $61.43M, surpassing by $5.91M, Culp, an international operator in the manufacturing and marketing of materials for mattresses and upholstered furniture, has shown resilience amidst the financial tumult. Despite challenging industry demands and a bleak sales outlook, Culp's financials paint a picture of potential turnaround anchored on prudent cost management, strategic restructuring, and operational efficiency. However, my deeper dive into its performance reveals a more disquieting reality, warranting a "sell" rating for its stock.

Company Overview

Culp, Inc., headquartered in High Point, North Carolina, operates internationally and is renowned for crafting and marketing materials for mattresses, stitched covers, and assembly kits. Their operations are primarily divided into two sections: the Mattress Fabrics division, dedicated to the creation of fabrics for bedding elements such as mattresses and box springs, and the Upholstery Fabrics division, delivering an array of fabric choices for both residential and commercial upholstered furniture. Additionally, they provide services encompassing window dressing installation and office seating solutions, primarily serving the hospitality and commercial sectors

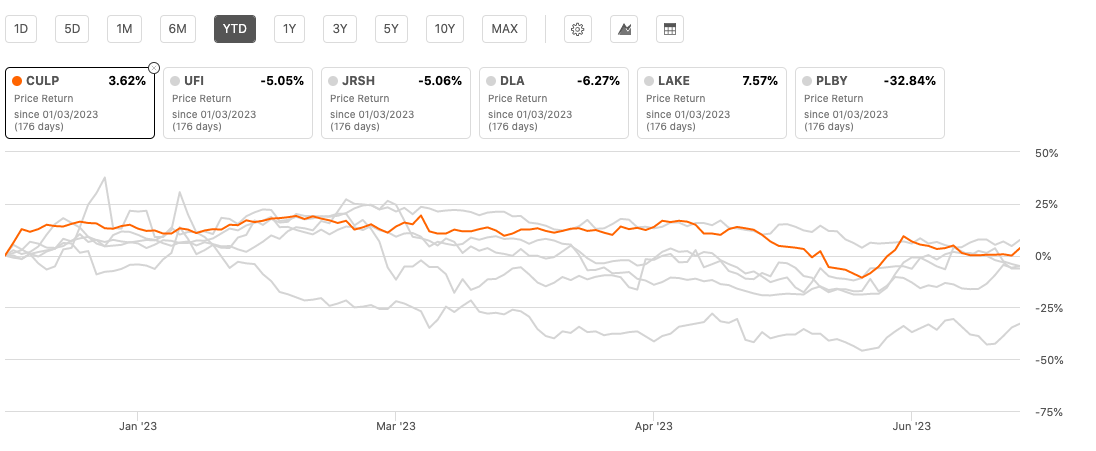

Performance

Relative to its peers in the Consumer Discretionary (Textiles) sector, Culp, Inc. has managed to keep its head above water YTD with a very modest return.

{kind=link}

Seeking Alpha

Culp's Bullish Q4 2023 Earnings Takeaways

Culp, Inc.'s financial results for the fourth quarter exhibit encouraging signs of improvement. Net sales demonstrated resilience, climbing by 7.9% compared to the prior year period. The positive trajectory was primarily driven by higher sales in both the Mattress Fabrics and Upholstery Fabrics segments, as well as enhanced margins on new products and operational efficiencies. Notably, the Mattress Fabrics segment saw a commendable sales increase of 3.1% year-on-year and a remarkable 24.3% sequentially, bolstered by the introduction of new customer programs.

Despite a challenging industry demand environmen t, the company's focus on cost management paid off, resulting in lower overhead costs. This favorable development can be attributed to the strategic restructuring and rationalization initiatives implemented in these areas. Moreover, the Upholstery Fabrics segment received a non-recurring customer payment and witnessed solid demand in its hospitality contract business, accounting for approximately 32% of total sales in the segment.

While net sales for the full fiscal year experienced a decline of 20.3% compared to the previous year, this decline was overshadowed by the company's notable achievements in enhancing operational performance. Despite reporting a loss from operations for the year, Culp showcased progress in driving positive outcomes. By effectively managing working capital and decreasing inventory levels, the company generated cash flow from operations and free cash flow of $7.8 million and $6.9 million respectively, an incredible turnaround from negative figures seen during previous fiscal years.

Furthermore, capital spending was tightly controlled, with a focus on essential projects, resulting in reduced capital expenditures compared to the previous year. Looking ahead, the company anticipates capital spending for fiscal 2024 to range between $4 million and $6 million, concentrating on maintenance projects and initiatives to enhance quality and efficiency within the Mattress Fabrics business.

Finally, Culp Corporation concluded the fiscal year with $47.8 million, combining cash reserves of $21 million and borrowing availability of $26.8 million under the asset-based domestic credit facility.

Valuation

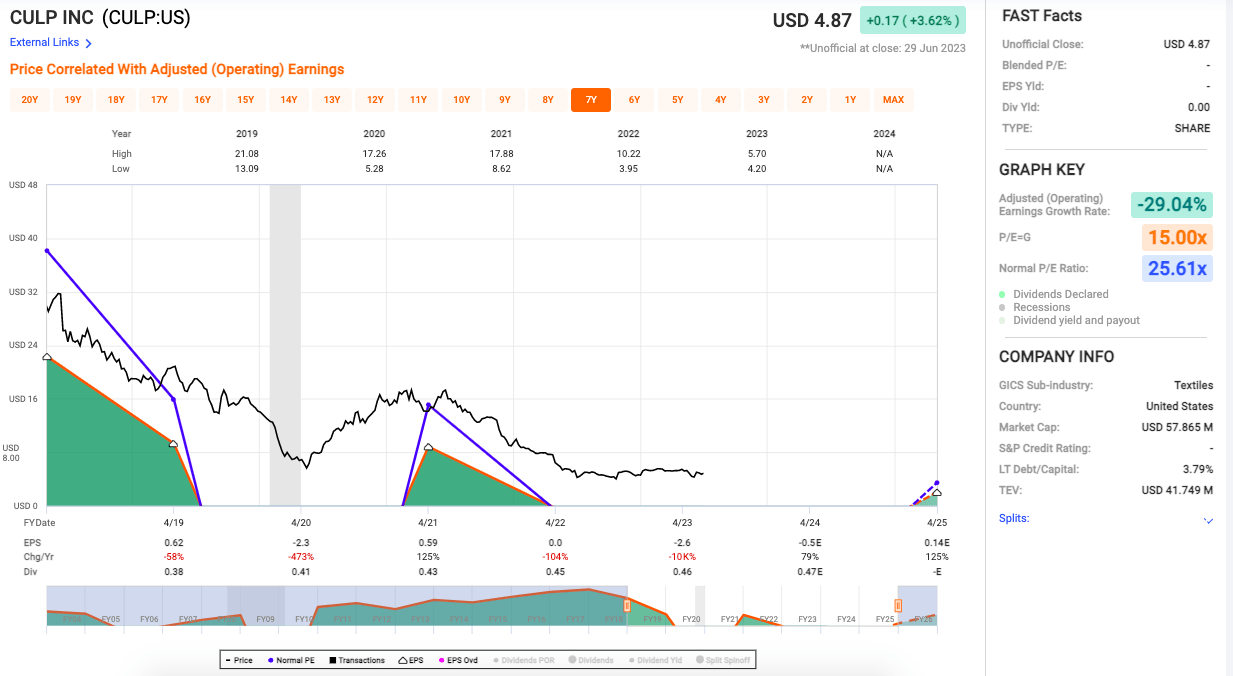

However, the data presented below paints a worrisome picture for CULP.

{kind=link}

Fast Graphs/Author Snapshot

The key statistic here, one that leaves me considerably bearish on this stock, is the Adjusted (Operating) Earnings Growth Rate of -29.04%. This downward trend shows that the firm is struggling to generate profits, a cardinal red flag for any investor.

Now, let's talk about the elephant in the room: the lack of a Blended P/E and an EPS Yield. To put it bluntly, the metrics suggest that Culp, Inc. is in a precarious financial situation. The dramatic decline in operating earnings, coupled with the absence of key profitability indicators and dividends, signals trouble.

{kind=link}

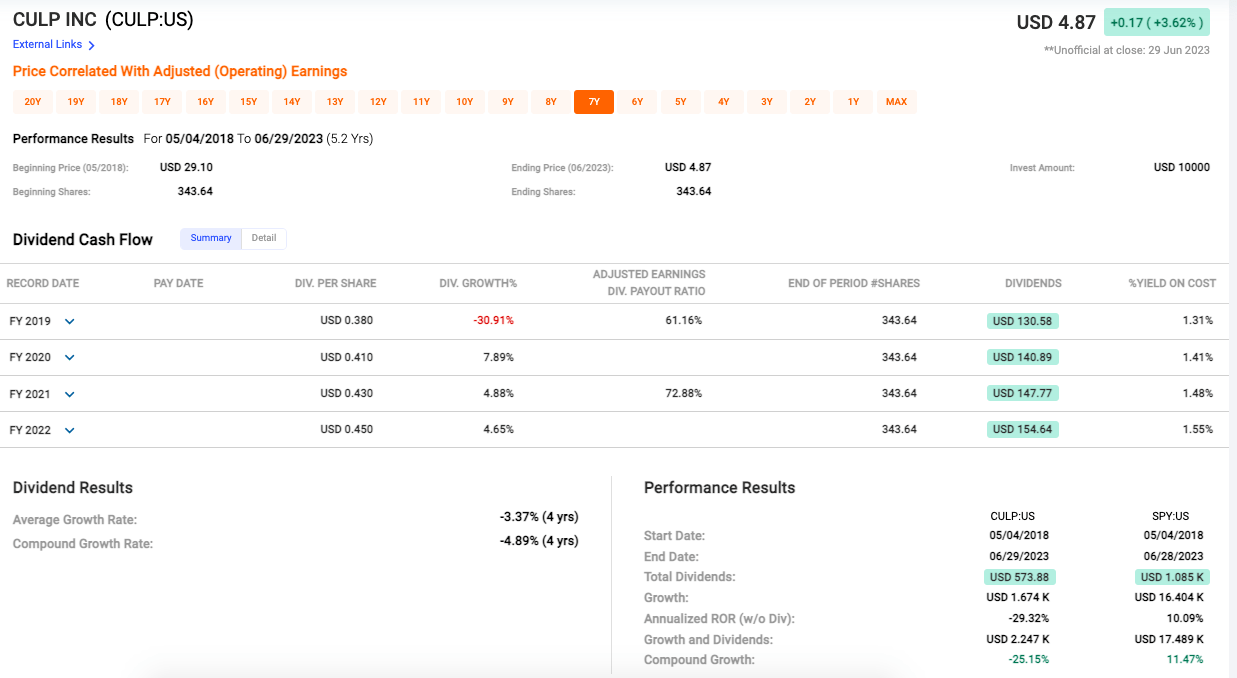

Fast Graphs: 7 YR Performance/ Author Snapshot

Another statistic (see above) that immediately stands out is the dramatic fall in the company's share price over a 5.2-year period from USD 29.10 to USD 4.87. This sharp decline indicates the stock has been underperforming and shows the company's diminishing value over time.

The Dividend Cash Flow section provides additional insight, showing a sporadic dividend growth rate over the years. Even though dividends have slightly increased from USD 0.38 per share in 2019 to USD 0.45 per share in 2022, the growth has been inconsistent and negligible. The average dividend growth rate over four years stands at a concerning -3.37%, indicating an overall decrease, not growth.

Moreover, the comparison to the SPDR S&P 500 ETF Trust (SPY) paints a stark picture. While Culp managed to generate a total dividend payout of USD 573.88 over the same period, SPY provided nearly double that amount. Additionally, the growth of SPY eclipses Culp showcasing a compound growth of 11.47% against Culp's -25.15%. The comparative performance makes it clear that an investment in CULP could've been better placed elsewhere.

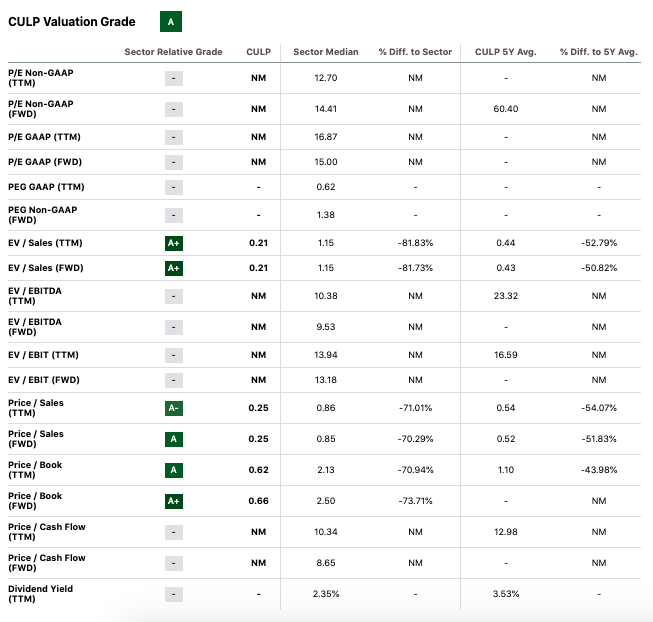

Sector Valuation

Conversely, Culp, Inc.'s Enterprise Value (EV) to Sales ratios , both trailing twelve months ((TTM)) and forward, are highly favorable. They've received an A+ valuation grade, which is impressive. It's trading at a significant discount to the sector median—over 80% cheaper on an EV/Sales basis. That's an encouraging sign and tells me the market might be underestimating the company's revenue generation potential.

{kind=link}

Seeking Alpha

The Price to Sales (P/S) ratios also signal a similar story. Culp, Inc. is considerably cheaper than the sector median, and also less expensive compared to its five-year average. This low valuation based on sales could indicate a potentially undervalued stock, assuming the company can maintain or grow its sales figures.

According to Price to Book (P/B) ratios, the outlook appears positive. The company trades at a significant discount from both sector median and five-year average values indicating that market price does not accurately represent net asset value.

Risks & Headwinds

Despite an encouraging uptick in sales during the fourth quarter, the company's net sales have contracted by a substantial 20.3% in contrast to the preceding year. This discrepancy points towards possible underlying difficulties, ones that might leave a lasting imprint on the company's performance in forthcoming fiscal periods.

Moreover, a closer examination of CULP's operational performance paints a somewhat bleak picture. The company has disclosed operational losses for not only the final quarter but also the entire fiscal year. Although there are hints of this negative trajectory tapering off with losses incrementally shrinking, the question remains—when will the company break free from the shackles of these operational setbacks and resurface into the realm of consistent profitability? The answer to this is as yet unclear.

According to management, unfavorable trends in the Residential Home Furnishings industry, where CULP maintains a significant foothold, appear to be a pressing issue. The current lackluster demand could potentially cast a pall over CULP's future sales and growth trajectories.

Adding to the company's woes is the halt in dividends and the absence of any share buybacks during the fiscal year, which raises red flags about the management's ability to navigate liquidity challenges.

Turning our attention to the Upholstery Fabrics segment, there's a noticeable uptick in SG&A expenses that could potentially weigh on future profitability.

Finally, an examination of the net losses underlines the stark reality of CULP's fiscal health, that is, the net loss for the fiscal year stands at an alarming $31.5 million, a substantial escalation from the previous year's $3.2 million. This signifies an intensified financial strain that could hinder the company's ability to rebound in the near term.

Final Takeaway

Despite Culp, Inc.'s commendable efforts to streamline operations, enhance product margins, and manage costs, the overarching issues cannot be overlooked. Its net sales continue to contract, operational losses persist, dividends have been halted, and the firm faces challenges within its key industry. Most concerning is the drastic -29.04% Adjusted Earnings Growth Rate, which, coupled with the alarming increase in net loss from $3.2 million to $31.5 million, indicates substantial financial strain. Although some valuation ratios suggest undervaluation, the company's current health and bleak performance outlook warrant me to give a sell recommendation on the stock.

For further details see:

Culp's Fiscal Health: The Rising Net Loss Concern