MSOS - Curaleaf Is A Bad Cannabis Investment

2024-01-07 04:02:19 ET

Summary

- Curaleaf's Q3 financials were disappointing, with revenue below expectations and a decline in adjusted EBITDA.

- The company's balance sheet remains a major risk, with high debt and negative tangible equity.

- Curaleaf's valuation is high compared to its peers, and its projected growth has declined over the past year. Investors should consider other options.

I warned about Curaleaf ( OTCPK:CURLF ) in October, explaining how it has more risk than its peers . The stock has rallied since then, but so have its peers and the overall market. I still am very negative on the stock, and I discuss here the Q3 financials, the updated outlook, the chart, and the valuation.

Q3 Was Disappointing

Curaleaf shared its Q3 financials in early November. Analysts had expected the company to generate $340 million in revenue with adjusted EBITDA of $75 million. It reported revenue that was below expectations at $333 million, up just 2% from a year earlier and down 2% sequentially. Adjusted EBITDA was $75.3 million, which was up 4% sequentially but down 13% from a year earlier.

Cash flow from operations for Q3 improved from $13.5 million in Q2 to $57.3 million. For the first three quarters of 2023, the company generated $73.0 million from its operations while spending $49.4 million on the purchases of property, plant and equipment, so the free cash flow was less than $25 million. Cash flow from operations has improved due to lower inventory and higher income tax payable.

The balance sheet remained a major risk, with a current ratio (current assets divided by current liabilities) of just 0.87X. Cash did increase a little to $118.1 million, but the debt outstanding is $584.6 million. Net debt of $466.5 million at the end of Q3 was down from $529 million, but it excludes taxes owed. Curaleaf owed income tax payable of $237.3 million as a current liability, up 45% since Q4 of 2022. It also carried an "uncertain tax provision" of $109.5 million, a long-term liability. These tax obligations aren't included in the total debt. These liabilities could become a major challenge, as the company doesn't yet generate substantial net cash. The tangible book value at the end of Q3 was very negative at -$751.5 million.

The Fundamental Outlook Has Not Improved

Since the last financial update, the analysts have cut their forward estimates. I use Sentieo to track this, and the outlook for 2024 is now for revenue to increase 5% to $1.42 billion. Adjusted EBITDA is now forecast to increase 18% to $352 million as gross margin expands from 45.8% to 49.2%. Ahead of the Q3 report, their estimates were revenue of $1.44 billion and adjusted EBITDA of $361 million, so the year-ahead outlook is slightly worse now.

I pay attention to the outlook for 2025, as a year from now, it will be the one-year forward outlook. Four analysts expect that revenue will increase 16% to $1.64 billion. They project that adjusted EBITDA will grow 31% to $462 million. They were expecting revenue of $1.74 billion and adjusted EBITDA of $522 million ahead of the Q3 report.

The Chart Has Not Changed

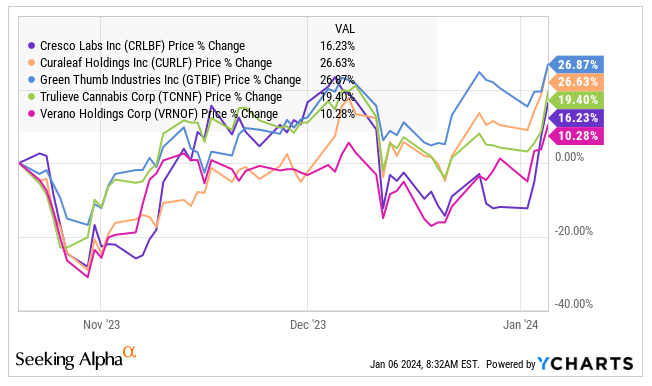

Since the last article was published on 10/22, Curaleaf has rallied by 26.6%. The New Cannabis Ventures Global Cannabis Stock Index has rallied by less, gaining 9.1%, but Curaleaf has moved a bit higher than most of its Tier 1 MSO peers:

{kind=link}

The two leaders, which include Curaleaf and Green Thumb Industries ( OTCQX:GTBIF ) are the largest holdings of AdvisorShares Pure US Cannabis ETF ( MSOS ), which has seen an inflow over this time frame, with shares outstanding increasing by 7.8% since then. GTI is currently 26.3% of MSOS, while Curaleaf is 21.4%. The ETF has purchased 1.02 million shares of GTI and 2.81 million shares of Curaleaf since then.

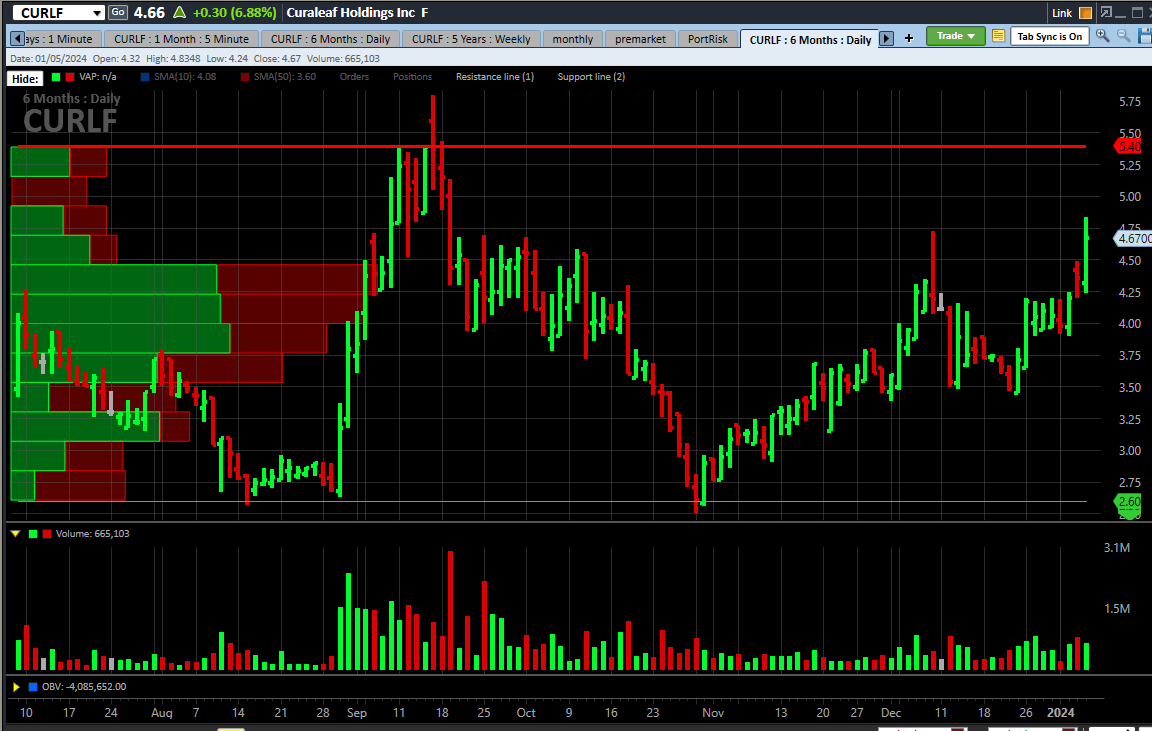

Looking at the chart for the past six months, Curaleaf is still below the peak in September. Its low in late October was below the low from August, which was prior to the news that the Department of Health & Human Services had recommended that the DEA reschedule cannabis from Schedule 1 to Schedule 3, which has not yet happened but could be a great thing in that it would wipe out 280E taxation on the industry.

{kind=link}

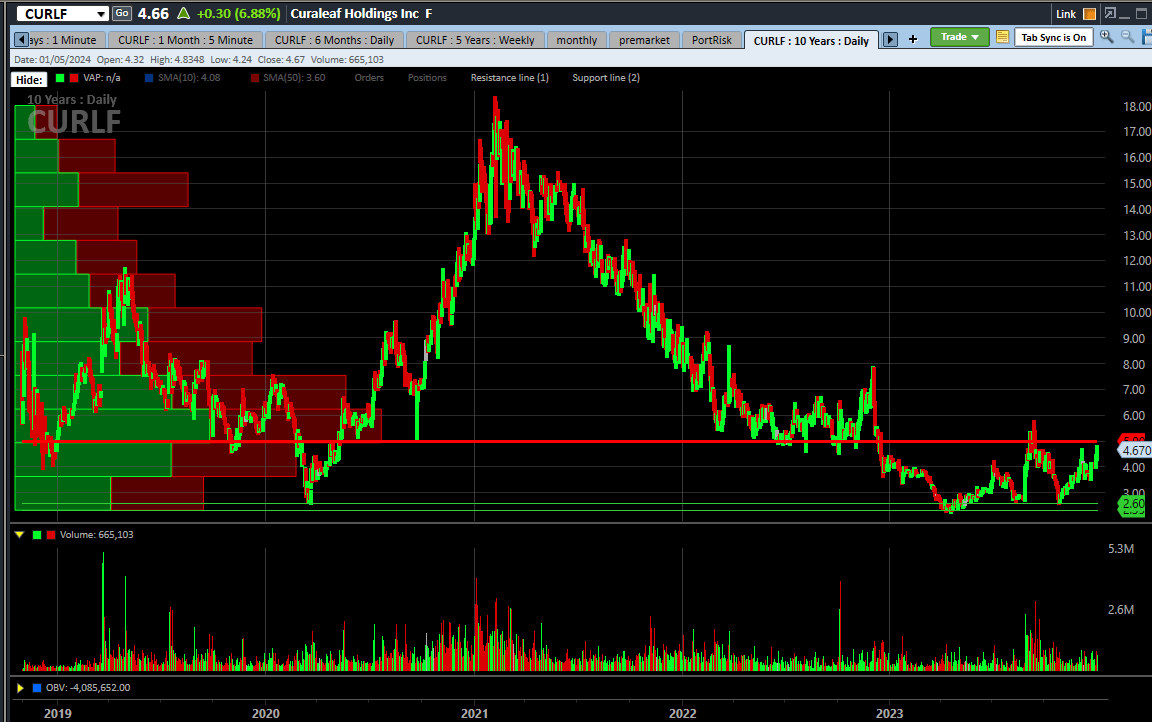

The entire trading history of Curaleaf shows that it made an all-time low during 2023 and is down a lot from the peak in early 2021:

{kind=link}

There appears to be resistance at $5 in my view. The trading volume spiked in late August and into September, and it seems higher than a year ago but substantially less than during the summer spike. The stock made that new recent low in late October, but the chart is essentially the same.

The Valuation Is Quite High Relative to Peers

Curaleaf seems extremely expensive relative to its peers. Its balance sheet is the worst among them, and the projected growth, while higher, isn't that different. The only big difference is that Curaleaf has international operations, but they remain a small portion of their overall business. The 2023 projected revenue has declined by 13% over the past year, and the projected adjusted EBITDA has dropped by 29%.

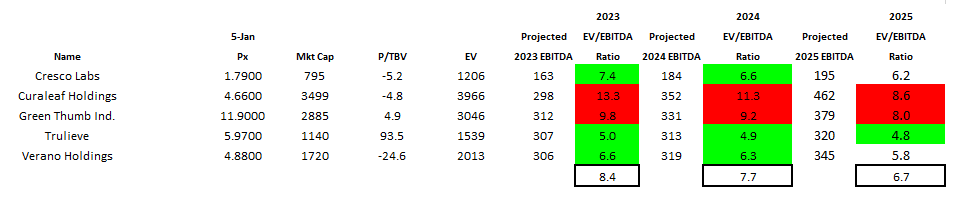

Here is the Tier 1 MSO group, which also includes Cresco Labs ( OTCQX:CRLBF ), Green Thumb Industries, Trulieve ( OTCQX:TCNNF ), and Verano Holdings ( OTCQX:VRNOF ) valuations of enterprise value relative to projected adjusted EBITDA for 2023, 2024 and 2025:

{kind=link}

Curaleaf, which has a lot of debt and very negative tangible equity, trades the highest relative to projected adjusted EBITDA.

Ahead of the Q3 report, I shared an outlook on the price of Curaleaf with the subscribers of my investing group. If 280E goes away, I thought that the stock could reach $4.95 by year-end 2024, but it could fall to $1.44 if 280E remains. These estimates were based on achieving an 8X enterprise value to projected adjusted EBITDA for 2025 in the optimistic scenario and just 3X in the pessimistic scenario. These were lower than the targets I shared in that article during October due to lower multiples.

Updating my outlook for lower projections and the current cash level and share count, I am raising those multiples of 10X and 4X. For the targets, I am assuming that 8.3 million options are exercised, giving them a share count of 751 million on a fully-diluted in-the-money basis and boosting cash by $24.4 million. The optimistic scenario yields a target of $5.56, up just 19%. Of course, it could go higher than a valuation of just 10X, but this would help other stocks too. The pessimistic scenario yields a target of $1.86, which would be 60% lower and a new all-time low.

Conclusion

Two weeks ago, I published an article on Green Thumb Industries, writing that it isn't the best way to invest in cannabis. Well, it's a lot better than Curaleaf! I would suggest replacing Curaleaf with GTI, but there are better choices.

For investors who want to own a large MSO, I own only one in my model portfolio designed to beat the NCV American Cannabis Operator Index, and that is Trulieve. It's up since I last wrote about it in mid-November, discussing why I like it , and I did recently reduce it in that model portfolio. I have almost 20% cash in the model portfolio currently.

I believe that investors should sell Curaleaf. For those that like large MSOs, I have shared two ideas in the prior paragraph, and I think that there are some Tier 2 MSOs that make sense over it as well. I continue to believe that there are better investments in certain Canadian LPs, and some ancillary stocks make more sense for those that want to capitalize on rescheduling potentially. In my Beat the Global Cannabis Stock Index model portfolio, I own just two cannabis companies that total just 14% of the portfolio. This is well below the current weight in the index of 37%. I have a cash position of 13% and am overweight Canadian LPs and ancillary companies.

Curaleaf should keep rallying if 280E goes away, but it will likely underperform its peers. If 280E remains, the company could drop a lot. Investors should wait until the valuation relative to peers looks more attractive.

For further details see:

Curaleaf Is A Bad Cannabis Investment