CCHWF - Curaleaf Is Too Expensive Relative To Other Cannabis Stocks

Summary

- I have followed Curaleaf closely since it went public in 2018.

- The company is the biggest American cannabis operator, but its market share isn't dominant.

- The stock is cheap outright, but there are better options for investors.

Curaleaf ( CURLF ) is the largest publicly-traded American cannabis company by sales or by market cap, but it isn't necessarily the best company. Its growth isn't the highest among its peers, and its margins are good but not great. In this piece, I discuss its operations, its valuation and its chart, and I explain why I have no position currently in my model portfolios.

Operations

Curaleaf calls itself the "world's leading cannabis company" in its investor presentation , which does a pretty good job of describing the company's operations.

The company operates in 21 states, with 26 cultivation sites and 146 stores. It is in six western states, Arizona, California, Colorado, Nevada, Oregon and Utah, and the rest of the operations are in more recently legalized states to the east. Florida, where it has 56 stores now (after opening its 56th after the deck), is a big part of the company.

One big difference between Curaleaf and its peers is that the company is actively pursuing Europe through an acquisition that closed in April 2021 and is known now as Curaleaf International. The company owns 68.5% of this division after selling a stake for $130.8 million in April 2021. As of 9/30/22, the company's stake in Curaleaf International is carried at $184.35 million.

The management team hasn't been stable. Executive Chairman Boris Jordan has been running the company, but the CEO has changed a few times. When the company went public, Joe Lusardi, now Executive Vice Chairman of the Board, was CEO. Now, Matt Darin, one of the founders of Grassroots Cannabis, which Curaleaf acquired, is the CEO. He replaced Joseph Bayern, formerly of Lowell Farms ( LOWLF ), who served briefly. The CFO position has had a lot of turnover too.

Analysts expect Curaleaf's revenue to increase by 15% to $1.54 billion in 2023 from the projected $1.35 billion in 2022. In the first three quarters of 2022, the company generated $990.4 million of revenue, up 11%. In Q3, sales rose 7% from a year ago to $339.7 million. The closest operator, Trulieve, was 11.5% lower than this, which you can see at the New Cannabis Ventures ranking page . Adjusted EBITDA is expected to grow by 26% to $416 million in 2023, an expansion in the margin from 24.6% to 26.9%. The company generated operating cash flow of $71.5 million in the first three quarters of 2022, and it spent $99.2 million on capital investment.

The Valuation

Curaleaf had cash of nearly $200 million and debt outstanding at nearly $600 million as of 9/30/22. Most of this debt is due in 2026. The tangible book value was $433 million. The company's inventory was a bit high relative to peers at $438 million, but the 12% increase from 12/31/21 was not too different from its revenue improvement. Note that the company completed the Tryke acquisition during Q4. This deal used $10 million of cash and resulted in the issuance of 2.7 million shares initially, with a projected additional $75 million and 16.5 million shares over time and up to 1 million contingent shares based on exceeding certain EBITDA targets in 2022.

At $4, the market cap of Curaleaf is $2.87 billion, which is 6.6X tangible book value. Cannabis investors can find Canadian LPs and ancillary companies that trade at much lower multiples, and Including the net debt of about $400 million boosts the enterprise value to $3.27 billion, which is 7.9X projected EBITDA for 2023 and just 2.1X projected 2023 revenue.

I hold positions in one or more of my model portfolios in all of the Tier 1 names except for Curaleaf. My smallest long position is in Green Thumb Industries ( GTBIF ), which I discussed recently as a good company with a cheap stock but not the cheapest . The other Tier 1 names include Cresco Labs ( CRLBF ), Trulieve ( TCNNF ) and Verano Holdings ( VRNOF ). Cresco Labs is buying Columbia Care ( CCHWF ), which is trading at a massive discount to the agreed-upon share exchange ratio, which reflects a potential change in that deal. Here are the projections and valuations for these six MSOs:

{kind=link}

Curaleaf trades at a large premium to the peers. The projected growth is the group's average, and its balance sheet looks in line with the peers.

My target for year-end 2023, based upon the 2024 projections, is for Curaleaf to rally to 3X projected revenue of $1.65 billion. This results in a market cap of approximately $4.55 billion, or $6.34, up 59%. The target valuation is also 11.9X projected adjusted EBITDA. This projected gain is good, but, in my view, low compared to some other MSOs or other cannabis companies.

The Chart

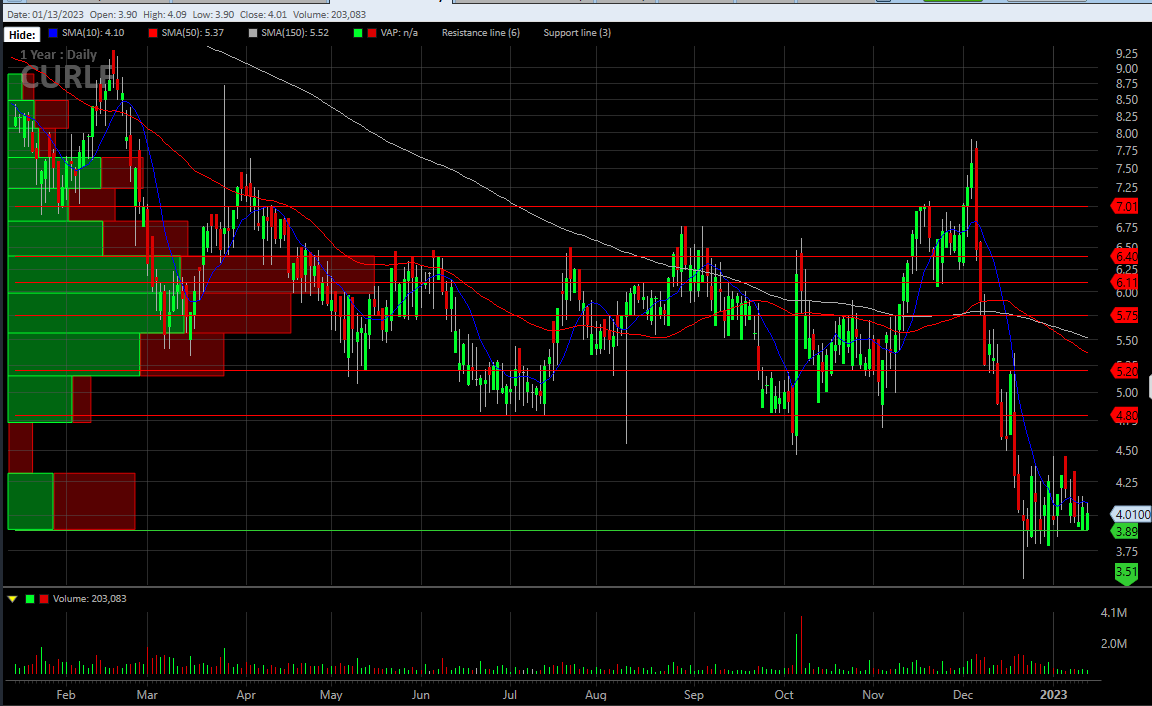

My projected year-end price of $6.34 is up a lot, but it is a big discount to where the stock traded recently:

{kind=link}

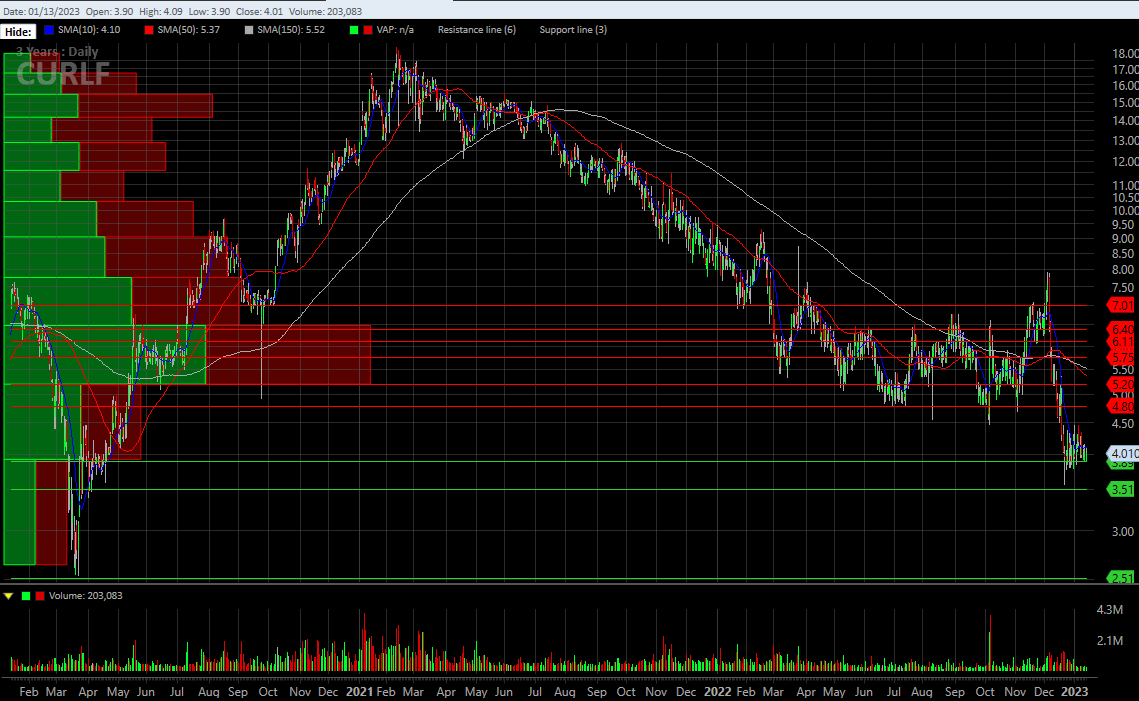

Curaleaf is down a lot over the last year, but it is up a lot from the early 2020 lows (when the pandemic hit):

{kind=link}

My target, of course, may be too low, but I think that its peers would do better too under any conditions that would allow for even higher valuations. Some of the factors that could help American cannabis operators would be either the elimination of the onerous tax, 280E, or the ability to begin trading on the NASDAQ. I am not predicting full legalization in the near-term, and this could actually be a negative if the FDA were to take charge of regulation of the industry.

Conclusion

Curaleaf is 20% of AdvisorShares Pure US Cannabis ETF ( MSOS ), but it is not in either of my model portfolios, Beat the Global Cannabis Stock Index or Beat the American Cannabis Operators Index. MSOS is experiencing share redemptions and continuing to trade at a discount to its NAV, and continued pressure could lead the ETF to reduce its Curaleaf position, which is its second largest.

In my view, the premium to peers that Curaleaf trades at is not justified. Investors who want to own MSOs can select other Tier 1 names or perhaps smaller. I wrote about Planet 13 Holdings ( PLNHF ) in mid-December, and it is still more attractive than Curaleaf in my view. The price is lower today than when I wrote it up, explaining how I was prepared to buy the dip (which I did in both of my model portfolios). Investors can also pursue stocks in other sub-sectors. I am very overweight ancillary companies in my model portfolio Beat the Global Cannabis Stock Index, and, while I am underweight Canadian LPs, I shared my favorite Canadian LPs in the New Cannabis Ventures newsletter this week.

I think Curaleaf can rally, but investors can pick up greater potential gains without taking additional risk in other names.

For further details see:

Curaleaf Is Too Expensive Relative To Other Cannabis Stocks