OSH - CVS And Oak Street: The Pros And Cons Of A Deal That Felt Inevitable

2023-03-31 13:56:57 ET

Summary

- CVS announced its $10.6bn acquisition of Oak Street when announcing broadly positive Q422 earnings. The deal is expected to complete in 2H23.

- The objective is to position CVS as a patient-centric healthcare provider and ensure no patient of health plan member is left behind.

- There are sound reasons for adopting such an approach. But is Oak Street the answer?

- The company is relatively small, heavily loss making, and worth less than half what CVS ultimately paid to acquire it based on market cap valuation.

- CVS could have built a business like this in-house. The promise that Oak Street can drive EBITDA of >$2bn by 2026 seems unrealistic. The deal is by no means disastrous but the deal feel symbolic rather than financially astute.

Investment Overview - If It Ain't Broke...

Back in February, when cover ing CVS' (CVS) FY22 earnings a nd discussing the likely performance in 2023 - I took a bearish view, putting me in a minority of ~1 amongst fellow contributors. I spent some time discussing the company's decision to acquire the value-based primary care provider Oak Street Health ( OSH ) in a deal worth $10.6bn, or $39 per share.

I also gave CVS a bearish rating in June 2021 and June 2022 , and the company's shares have underperformed - down 27% across the past 12 months, and down 19% so far this year. The five-year performance is positive however at +21%.

As a long-term investment proposition I'm not necessarily against CVS - a sprawling healthcare giant whose three divisions - HealthCare Benefits, Pharmacy Services and Retail / Long Term Care - drove $322.5bn of revenues last year - up 10.4% year-on-year, and generated cash flow from operations of >$16bn. The company also pays an attractive dividend currently yielding 3.24%.

CVS has driven strong revenue growth in every year since 2013, and net income has increased in every year since 2013, so why complain? The company also has developed from a drugstore chain into a major provider of healthcare insurance thanks to its $78bn takeover of Aetna, giving it access to one of the most lucrative areas within health insurance - Medicare Advantage.

At the end of 2021, CVS' CEO Karen Lynch - who was formerly president of Aetna (AET) - outlined plans for " Revolutionizing the Consumer Health Experience While Driving Profitable Growth," commenting in a press release :

Now is the time to undertake our next major evolution and capitalize on our role as the leading health solutions company in America. By leaning into our high-growth foundational businesses and expanding our reach in areas like health services and primary care, we have an opportunity to shift care to be more centered around the consumer while capturing a meaningfully greater portion of health care spend.

Nine months later, CVS announced the acquisition of home-based care specialist Signify Health - a deal which completed this week - for ~$8bn, or $30.5 per share. In February this year, Lynch announced the $10.6bn acquisition of Chicago headquartered Oak Street Health ( OSH ) and its 169 primary care clinics.

No one can argue that Lynch has not been as good as her word - nearly $20bn has now been spent on value based care and primary care initiatives - and these acquisitions certainly seem to fit the narrative of what the modern healthcare industry should be - but with that acknowledged, has CVS made the right moves, at the right time, and with a clear plan in mind, or are these purchases too opportunistic, not based on demonstrable performance, and perhaps not large enough?

Let's begin our analysis by asking a simple enough question.

Is Oak Street's Business Worth $10.6bn?

Prior to CVS' acquisition of Oak Street the market certainly did not seem to believe that Oak Street was a >$10bn valuation company. At the beginning of 2023, Oak Street's shares traded at ~$20, valuing the company at ~$4.8bn.

Granted, to complete a buyout, companies - especially those as large as CVS - usually have to pay a premium, and additionally, companies as large as CVS could write-down a $10bn loss without even causing too much of a stir ($5.8bn of opioid litigation charges and a write-down of $2.8bn related to its Omnicare business was written down in CVS' 2022 earnings reporting) - but even so, the figure feels high.

In Oak Street, CVS is buying a company that drove $2.1bn of revenues in 2022, up from $1.4bn revenues in 2021. If that feels like a positive, the negative is that Oak Street made a net loss of >$(500m) in 2022, and a net loss of >$(400m) in 2021. Despite the losses, CVS says that Oak Street CEO Mike Pykosz will stay on to lead the company after it's acquired, with the company becoming a "payor-agnostic business within CVS Health," according to a CVS presentation .

{kind=link}

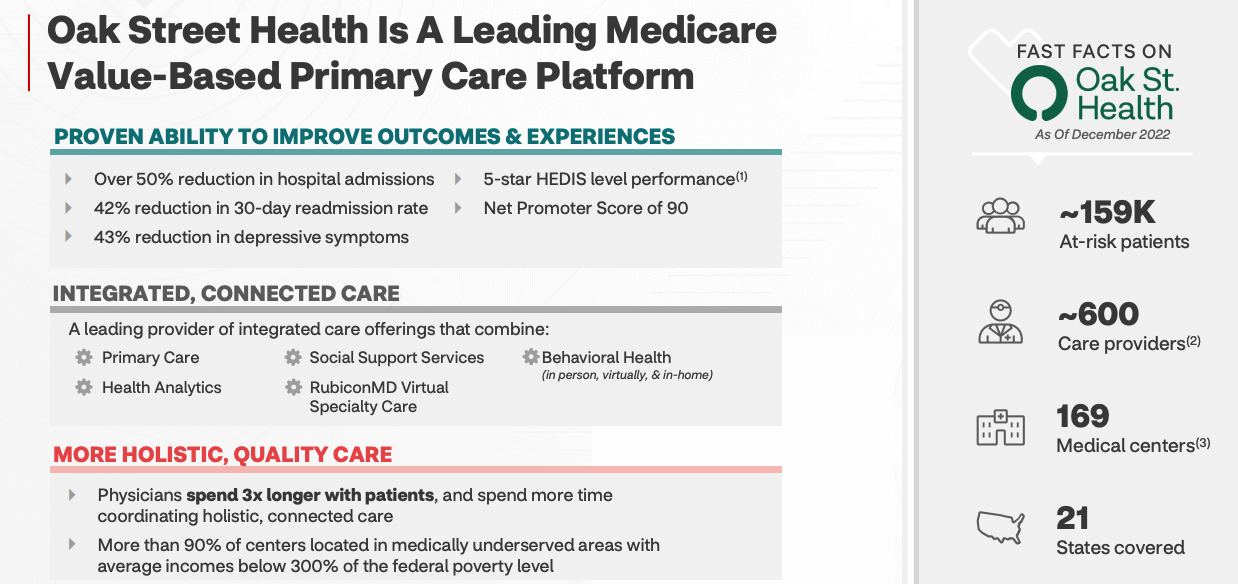

As shown above, Oak Street has a strong reputation in healthcare. It reduces expensive hospital admissions. It provides holistic patient care, which includes reducing depressive symptoms. Physicians spend more time with patients, and centers are located in medically underserved areas. Within the health insurance business, the ability to keep an eye on your members is extremely important.

{kind=link}

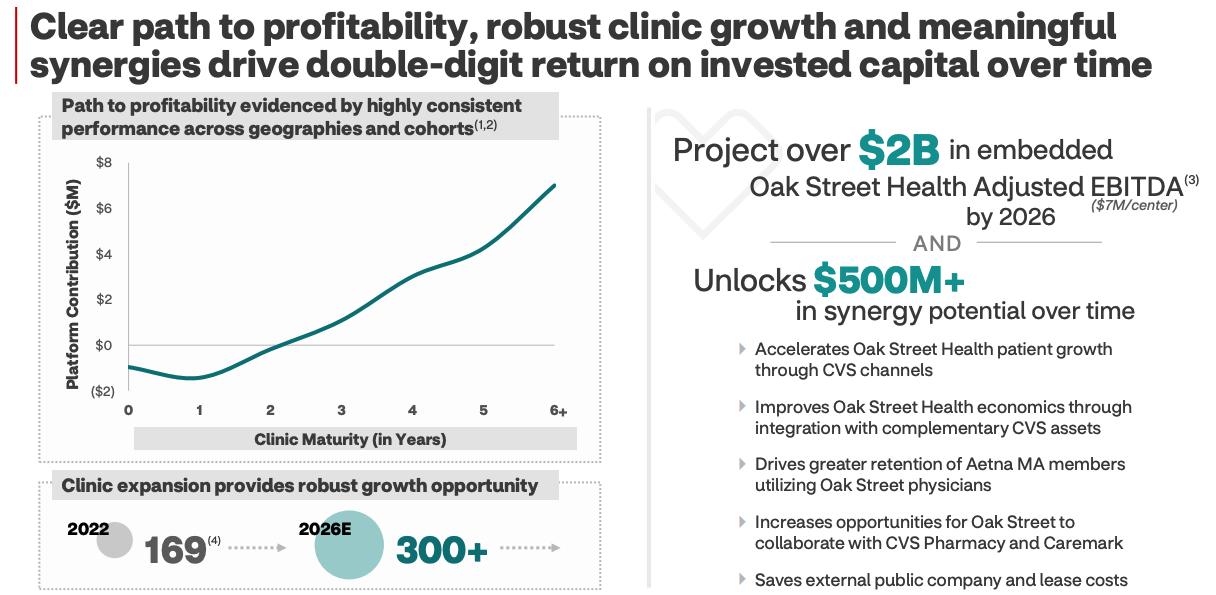

CVS also believes that there is a "clear path to profitability" - despite the fact Oak Street's business model has lost >$1bn across the past three years.

The path is based on rapid growth of clinics - from 169 to >300 by 2026, with each clinic generating ~$7m of EBITDA (analysts were told on CVS' Q422 earnings call ), which adds up to >$2bn of EBITDA contribution by 2026, and unlocks ~$500m of cost synergies, CVS says, which will allow it (CVS) to drive overall earnings per share >$10 by 2025.

That math is quite intriguing when we consider that Oak Street's clinics must have lost an average of nearly $3m each in 2022, taking the businesses net losses into account. It would be intriguing to know which element of Oak Street's nascent business is going to be responsible for swapping losses with profits, as it seems far from clear. Primary care is an expensive business.

What strikes as more surprising about CVS' acquisition of Oak Street however is the scale.

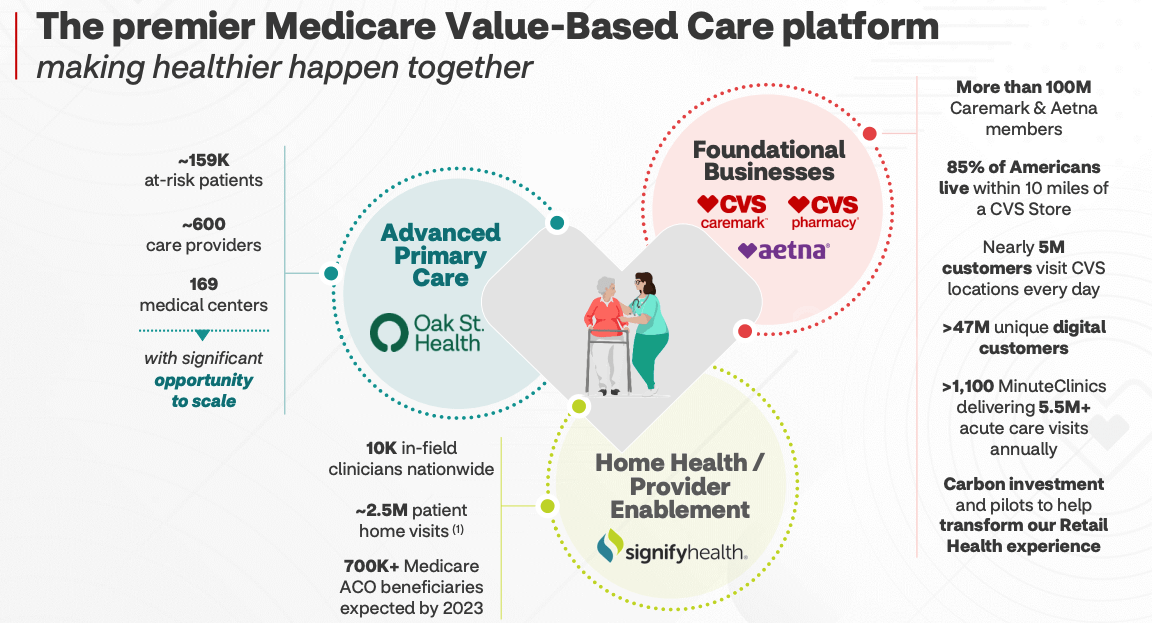

CVS plans to dominate healthcare landscape (CVS presentation)

{kind=link}

When I look at the slide above I can see that CVS is a bona fide healthcare giant, with 5m visitors to its clinics each day, and 100m Caremark (Caremark is the Pharmacy Benefit Manager company acquired for ~$24bn in 2007) and Aetna members, and 1,100 Minute Clinics.

These are big numbers, and looking at Signify's portion of this diagram, I can see they have 10k in-field clinicians, completing 2.5m patient home visits, and covering 700k Medicare beneficiaries. Again, these are big numbers, quite possibly worth paying $8bn to gain access to.

Looking at the Oak Street figures however I'm less impressed. 159k patients, 600 care providers, and 169 medical centers. If CVS expects to extract $2bn EBITDA from less than double the number of clinics by 2026, then each patients' contribution would need to be close to $7k, by my calculation.

Put another way, if 159k patients generated just over $2bn of revenue in 2022, how do ~300k patients generate >$2bn of EBITDA less than five years later? And bear in mind, there are only 600 care providers able to treat these patients - perhaps >1k by 2026, but even so, I find the economics of turning a heavily loss making company into a high margin success in just a few years quite confusing.

Presumably CVS will be providing most of the impetus. That being the case, why spend $10bn to acquire a business losing >$500m per annum when you can likely build a better version of Oak Street internally? In summary, from some perspectives at least, it's a little difficult to understand how Oak Street is worth >$10bn.

Is This The Right Time For CVS To Buy Oak Street?

After my February note on CVS and discussion of it, several commenters pointed out numerous positives about the Oak Street deal that struck me as valid. Wall Street analysts also have broadly supported the deal.

The main argument runs that the deal is more about the big picture than the current profitability (or otherwise) of Oak Street. CVS wants to have insight into every aspect of the healthcare business, so it can highlight areas of waste and drive operational efficiencies, and Oak Street can help it to achieve its goal.

In the current environment, it's generally accepted that there's "downward pressure" on Medicare Advantage rates, and as I noted in February, CVS's plan star ratings are falling - by 2024, it's predicted only 30% of its members will be in 4+ star plans, vs. 78% this year. Oak Street is expected to be able to help improve these ratings, and higher rated plans receive greater bonus payments.

Oak Street can help those patients most at risk of falling through gaps in the healthcare system find the care that they need, therefore even if Oak Street looks after just a couple of hundred of thousand patients, the savings created are disproportionately large.

In time, Oak Street could provide CVS with a powerful lobbying tool as it defends some of the most vulnerable patient populations - that also comprise one of the most significant drain on a health insurers' resources.

When we consider these arguments, in my view it reflects a shift in the healthcare landscape towards a more holistic, value-based care model, and an ambition to make sure patients are properly looked after.

It's an argument that clearly has merit, and staff as experienced as CVS senior management clearly have excellent visibility into the market. In their opinion, then, this is exactly the right time to be investing money into value-based primary care. But does that make Oak Street the right choice?

Final Thoughts - Did CVS Invest >$10bn In An Idea Instead Of A Business The Implications Of That Could Be Troubling

CVS had made it known all the way back in December 2021 that it would like to centre care around the consumer, which as a strategy seems reasonable and sensible, although trumpeting that you intend to move in such a direction may not have been so wise.

With that said, paying more attention to your health plan members and making sure they can access healthcare does not necessarily mean they will not fall ill. CVS may be in danger of drawing the conclusion that keeping patients out of hospital equates to success, and is a good reason to spend >$10bn on Oak Street - plus, Oak Street can provide outreach to more vulnerable populations.

I accept the latter point but not necessarily the former. Hospitals are a tried and tested way to access primary care and sometime patients need to visit them - fighting against that tide seems flawed.

Most of all, however, in relation to Oak Street - an early stage, loss-making business, my question would be why CVS did not simply develop its own version of such a business? CVS has 10x more Minute clinics than Oak Street has clinics. Oak Street isn't profitable, and it only has 600 primary care providers on its books.

Buying Oak Street is not like buying Caremark or Aetna - or even Signify, in my view. These were highly evolved business models in profitable markets with high barriers to entry. There are fewer barriers to entry in Oak Street's market, and the business model remains unproven - or even disproved, if you take the bottom line into account.

Ultimately, CVS's long-term share price performance does not depend on the success or otherwise of Oak Street - although the deliberate shift in direction management is taking - embracing a vision of healthcare that may be neither profitable nor shared by the public - is potentially more troubling.

Oak Street may only be a small step in the direction of "holistic care" but management clearly wishes to take many more steps in that direction and I wonder if it's investing too many of its tangible assets such as operational cash flow into an intangible and unproven business model?

Such an approach could damage the company and its share price long term.

For further details see:

CVS And Oak Street: The Pros And Cons Of A Deal That Felt Inevitable