OSH - CVS Health: This Cash-Rich Predictable Business Should Fare Well Even In A Potential Recession

2023-04-26 12:54:41 ET

Summary

- CVS shares have underperformed the broad market in recent months due to investor concerns over high spending on M&A activities and expected pressure on Medicare reimbursement rates.

- Management is not nearly as pessimistic and continues to see growth ahead. The past acquisition's track record speaks in the executives' favor.

- The business produces steady cash flows and trades at a bargain base price of 6x Cash Flow and 8x Earnings, which appears too cheap when compared to its peers.

- My price target for CVS is $125, and I expect a potential annualized investment return of about 20% over the next 5 years when factoring in the 3.3% dividend.

Is a recession coming?

In recent weeks, almost no day seems to go by without a new "doom and gloom" note coming out. The strategists employed by the Street to read the tea leaves are seeing a crash ahead, and CNBC loves to make new headline s about the expected bloodbath. Yet, the indexes show a positive YTD return. Even if my educated guess would be that a downturn is indeed approaching, I prefer my investment decisions not to be overly dictated by what is going to happen in the next 10 months. If anything, I would rather focus on the next decade. As I keep building wealth for my retirement, I am a believer that buying quality companies will offer, in due time, an adequate return no matter where we stand in the economic cycle.

That is not to say I buy quality at any price. As a value investor, I always try to make the best use of capital, not swing at every pitch, and look for mispriced opportunities. But what if a strong, recession-resistant business was on sale today? I would see no reason not to pull the trigger, even with a recession possibly ahead. Let me explain why, at the current levels, I am a buyer of CVS Health Corporation ( CVS ) shares and think that the stock offers a great risk-reward adjusted opportunity.

Business overview

With a market cap of almost $100 billion, CVS Health Corporation is one of the largest healthcare companies in the US and the world. As of 2023, the company operates approximately 9,600 retail pharmacies and approximately 1,200 family health care clinics. However, CVS is much more than that. With its acquisition of Caremark in 2007, CVS also became the largest pharmacy benefit manager ((PBM)) in the US processing over two billion adjusted claims annually. The $24 billion deal was the first defining step of CVS’s strategic vision to become “a leading health solutions company” and create a vertically integrated player active throughout the entire value chain of the complex American healthcare system.

Fast forward ten years, and CVS’s vision came to full fruition through two other acquisitions. In 2018, CVS Health completed a transformative merger with Aetna, a major health insurance provider. And in 2022, after a pause of three years to pay down debt and reduce leverage, it was the time of home-healthcare provider Signify Health. The $8 billion all-cash transaction recently closed after a bidding war . While arguably never fully understood by the market, these two mergers enabled CVS to create a totally integrated healthcare model, with the ability to offer a complete range of healthcare services. With the combined capabilities of Caremark, Aetna and Signify Health, CVS can offer everything from prescription drugs and basic medical care to complex medical management and insurance services. The mergers position CVS Health as a leading healthcare service provider, with a focus on consumer-centric solutions that prioritize affordability, accessibility, and convenience.

The outlook

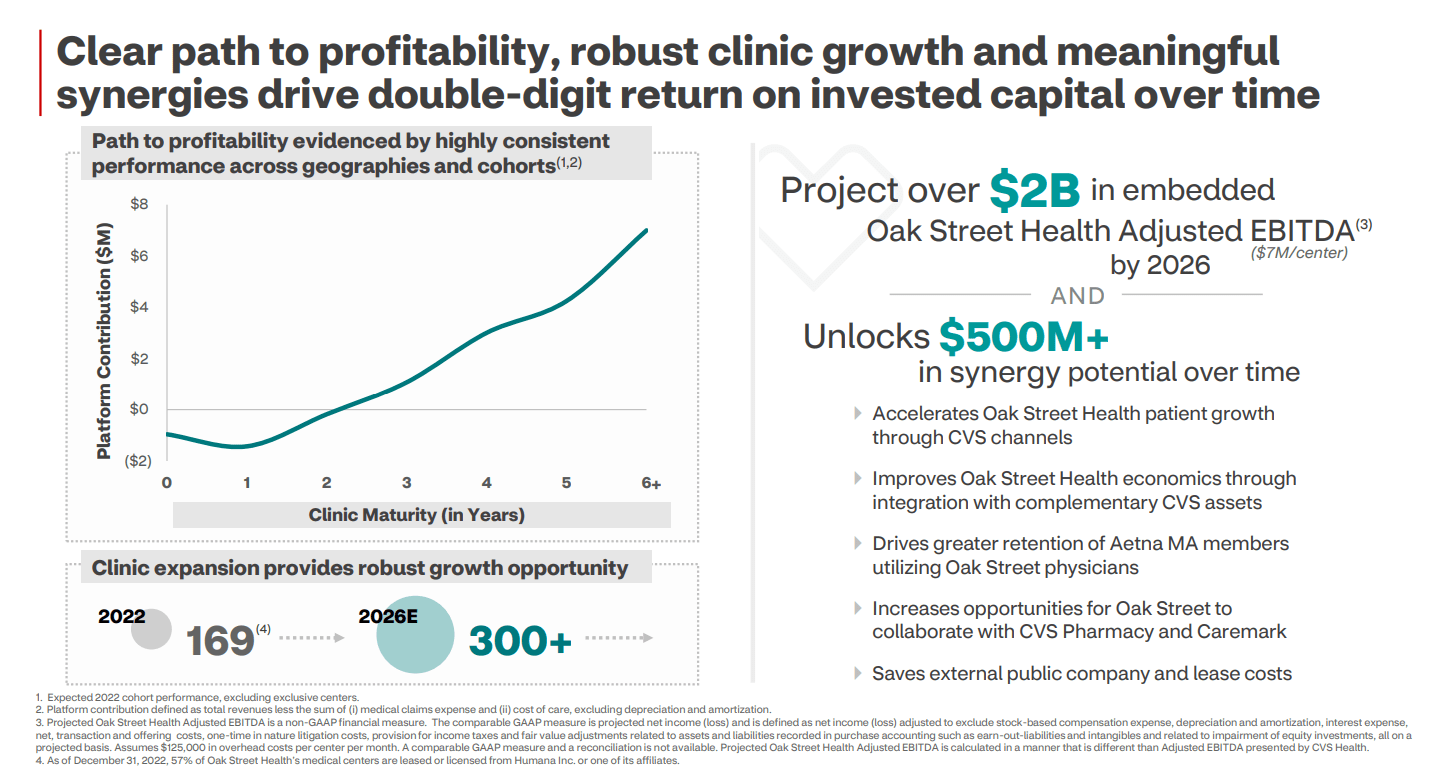

Investors are now rightfully expecting CVS to focus on execution, but the company decided instead to commit even more money to foster its vision and recently announced the acquisition of Oak Street Health ( OSH ) in February. The new, all-cash, deal is valuing OSH at $10.6 billion. Management expects to rapidly scale the primary care clinics operated under the Oak Street banner from 169 to over 300 by 2026. The price tag paid for OSH (approx. $60 million per clinic) seems rich, and the market reception was cold. However, CVS seems to think that these centers can contribute an average of $7 million EBITDA each, once they reach maturity stage. If so, the math behind the transaction would stand at approximately 8.5x adjusted EBITDA per clinic, an OK price tag. In addition, there could be upside potential as Oak Street integrates into the established CVS platform and creates further opportunities for the various business units of CVS. The company has projected such an upside value to be worth $500 million, and I like the fact that most of the highlighted synergies are top-line growth enhancers.

Nevertheless, I find it quite difficult to understand how a company that was worth less than $5B at the end of 2022, making $2.1 billion in revenues and -$0.4 billion EBITDA can turn into a business generating $2 billion EBITDA with less than double the number of clinics within four years. While the math to get there is intriguing, I also find it unrealistic. Perhaps a more realistic rationale for this deal is, however, not to be searched within the numbers of OSH clinics. Taking a “holistic approach” in line with the company’s vision of healthcare, one must look at the bigger picture of CVS and the company’s standings on its Medicare Advantage plans. There is a lot of downward pressure going on throughout the industry and CVS has been hit harder than competitors. Aetna MA PPO plan rating of 3.5 stars means that in 2024 the company will be ineligible for bonus payments. The OSH acquisition is expected to help mitigate the downfall, potentially reverse it and provide CVS with a tool to create savings, offset the pressure on rates looking after a disadvantaged segment of the population.

{kind=link}

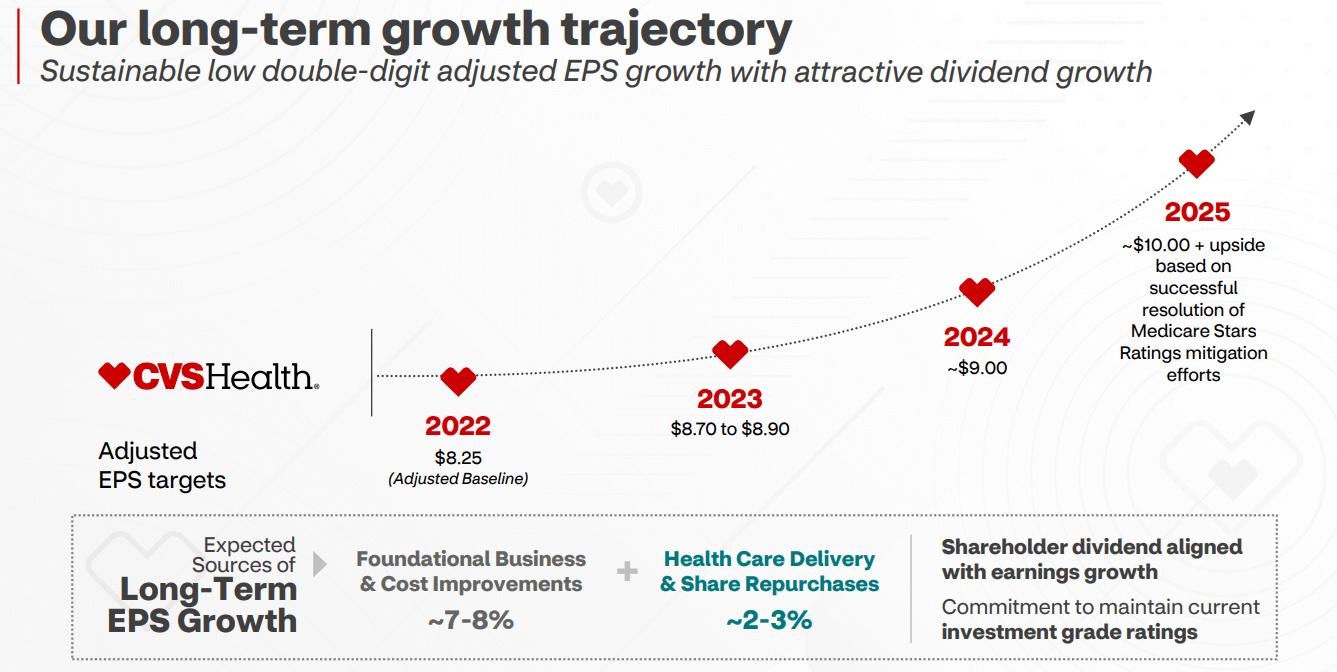

Since there are no expected challenges to the deal, the closing of the merger could come even earlier in the year than factored in by management’s guidance, with a slight negative impact on CVS’s FY23 earnings. A moderate guidance cut could come with Q1 2023 results in May, and I believe such uncertainty has also weighed on the stock’s recent performance. However, such short-term headwinds should not, in my opinion, spook investors. I believe CVS execution of the Aetna merger has been a success, and because the company has broad shoulders to take on the costs associated with the Signify and Oak Street mergers without any meaningful increase in leverage, I am willing to give some leeway to CVS management with regards to these deals. CVS earned $8.7 per share last year and, despite expecting a pause in the current year (with results expected to be roughly flat, and not negative, vs. last year) growth is set to resume as soon as 2024.

According to the latest investor presentation, the company expects to earn approximately $9 per share in 2024 and $10 in 2025. At the current share price of $73, CVS is trading at just 8x next year’s earnings and 7x the two-year figure. These are typically P/E values that are assigned by the market to cyclical, no-growth, or low-growth businesses, not to a steady business that is set to generate bottom-line growth in the high single digits. The misalignment begs a question: are the expectations too rosy? A quick cross-check of CVS and industry results should help clarify that.

{kind=link}

CVS (and competitors) growth

CVS has relied heavily on M&A to transform and grow its business, and the activities come with higher execution risks than those of companies who typically achieve growth organically. With reference to the healthcare space, recent history is full of problematic M&A stories: Valeant – now Bausch Health Companies ( BHC ), Teva Pharmaceutical ( TEVA ), or Mylan – now Viatris ( VTRS ). However, several years have now passed since the Caremark and Aetna deals. CVS has demonstrated to have skillfully integrated the PBM and insurance divisions and future growth of these units can now be seen as organic.

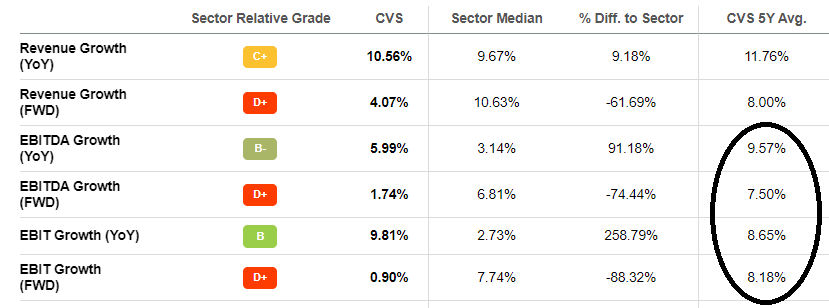

Post-Aetna-merger, CVS Health EBIT and EBITDA growth averaged in the 8%-9% range. EBITDA increased from $12.8 billion in 2018 to almost $20 billion in 2022. EBIT increased from $10 billion in 2018 to $15.4 billion in 2022. EPS growth was slower and affected by one-offs, but based on these figures, I can see that potential for future acceleration of EPS growth towards management’s goal of 9%-11% is there.

{kind=link}

Morningstar’s analyst following the stock is a bit more skeptical, and because management has pushed back on the starting date of double-digit growth multiple times, “only incorporate high-single-digit earnings growth in our model for the long run”. I think the critique is fair, and I agree that based on CVS' recent history, conservatively modeling 8%-9% growth is not a bad idea. Yet, the market seems to be underestimating the strength of CVS’s integrated model, and hence prices CVS like a no-growth business, which is only what its legacy retail pharmacy business is.

The image of CVS seems painfully that of a Walgreens Boots ( WBA ) full-flagged competitor, rather than a player active across other segments of the healthcare value chain such as UnitedHealth Group ( UNH ) or Elevance Health ( ELV ). Taking for example ELV, the stock currently trades at almost 14x forward earnings (and I think ELV shares are on the cheap side as well). Elevance Health five-years EBITDA/EBIT growth is higher than CVS, with approximately 12% CAGR, so a slightly higher multiple seems appropriate. Still, even assuming that ELV is fairly valued at 14x-15x earnings per share, it would not be unreasonable to pay at least 11x-12x earnings per share for the kind of growth CVS has shown.

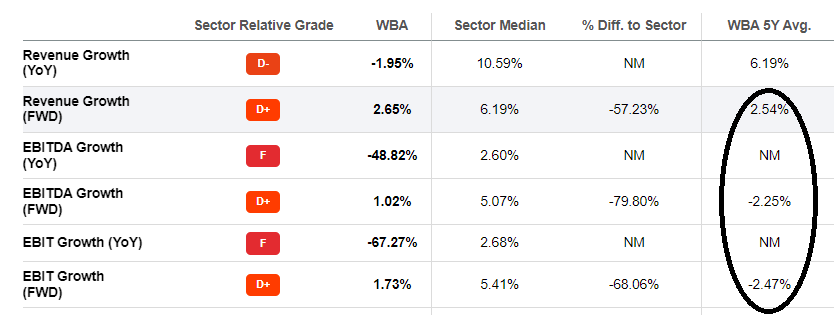

On the opposite side of the value chain there are retailers such as WBA and, as I said, CVS historically started out as a retailer as well. The market seems likely stuck with that association. The proof is WBA trading at 8x expected forward earnings, just like CVS. But now look at WBA's last five years of growth or lack thereof:

{kind=link}

Both WBA and CVS trade at 8x earnings. Both are reporting solid cash flow generation. The difference is, I expect only one of these two companies to substantially increase the amount of cash flow generated in five to ten years from now. I vote with my money, and that is on CVS.

Recession-resistant revenues

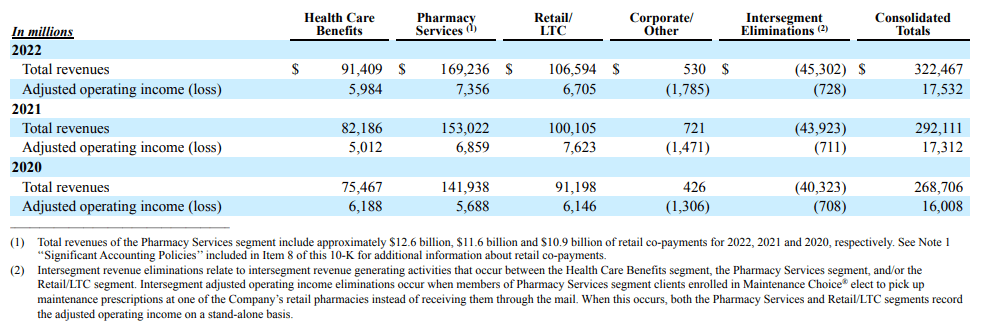

Breaking down CVS' revenues, the company reports three main operating segments: healthcare benefits, pharmacy services, and retail/LTC. The healthcare benefits segment is CVS' insurance business (Aetna), the pharmacy services segment is chiefly its PBM business, while in retail/LTC, CVS reports results of the drug stores and clinics.

In 2022, insurance revenue was $91.4 billion, pharmacy services revenue was $169.2 billion, and retail was $106.6 billion. The exact weight for each segment cannot be calculated precisely as reported values are gross of intersegment eliminations, but it is enough to have a sense of things. Approximate weights are 50% for pharmacy services, 30% for retail/LTC, and 20% for insurance.

{kind=link}

I do not think that it is plausible to expect that even in a recession, the insurance and PBM segment revenues would take a serious hit. CVS's "recession-sensitive" revenue is limited to its 30% retail segment exposure. But because clinic revenue is bundled within this segment and should also be stable, the real segment exposure is less than that. Even then, prescription drugs are not likely to be affected either; only ancillary revenues would be hit. Is that enough for drug stores to really feel recession pain? The evidence is mixed: while drug stores haven’t been immune to the Great Recession, the general data shows little correlation between drug store sales and the broader economy's direction. All in all, because its retail exposure is low and healthcare has been a great sector to hide in periods of recession, I expect CVS to perform well from here, regardless of a downturn in the next few months.

Valuation

I already briefly made a case of CVS being a potentially undervalued pick based on relative valuation. The company trades at a low P/E multiple of 8x, which is in line with that of WBA, despite having better historical performance as well as prospects, being exposed throughout the entire healthcare value chain and not only cyclical retail. At the same time, a lower P/E compared to Elevance Health or UnitedHealth may be warranted, but the gap with these companies seems to be too wide.

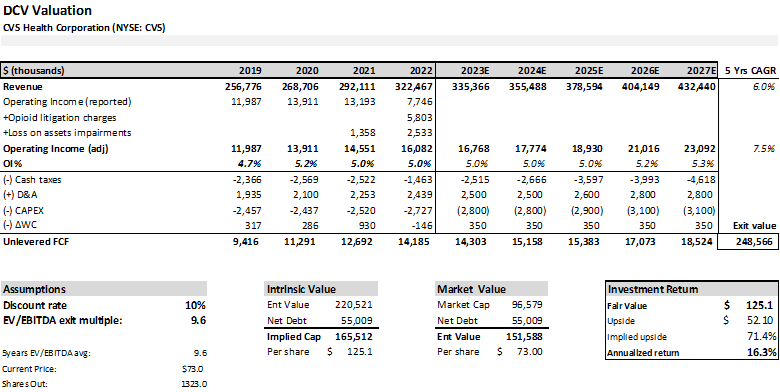

I am assigning CVS an intrinsic value of $125 by 2027 (5-year holding period) based on my DCF model. I think the model represents a good base case valuation as it uses relatively conservative assumptions. In my model, I used a 5-year revenue CAGR of 6% and EBIT CAGR of 7.5% with an acceleration to hit this target through a marginal profitability improvement from 5.0% to 5.3% towards the end of the forecast period. These growth targets are in line with the performance of the firm post-Aetna acquisition. The company’s core profitability level of approximately 5% is also left roughly unchanged compared to current levels and implies minimum synergies realized from improved scale and the integration of Signify and Oak Street Health.

For the end of the forecast, I used an EV/EBITDA exit multiple of 9.6 which is also in-line with CVS 5-year average and appears relatively undemanding when cross-checked with the averages of CVS peers within the healthcare sector.

{kind=link}

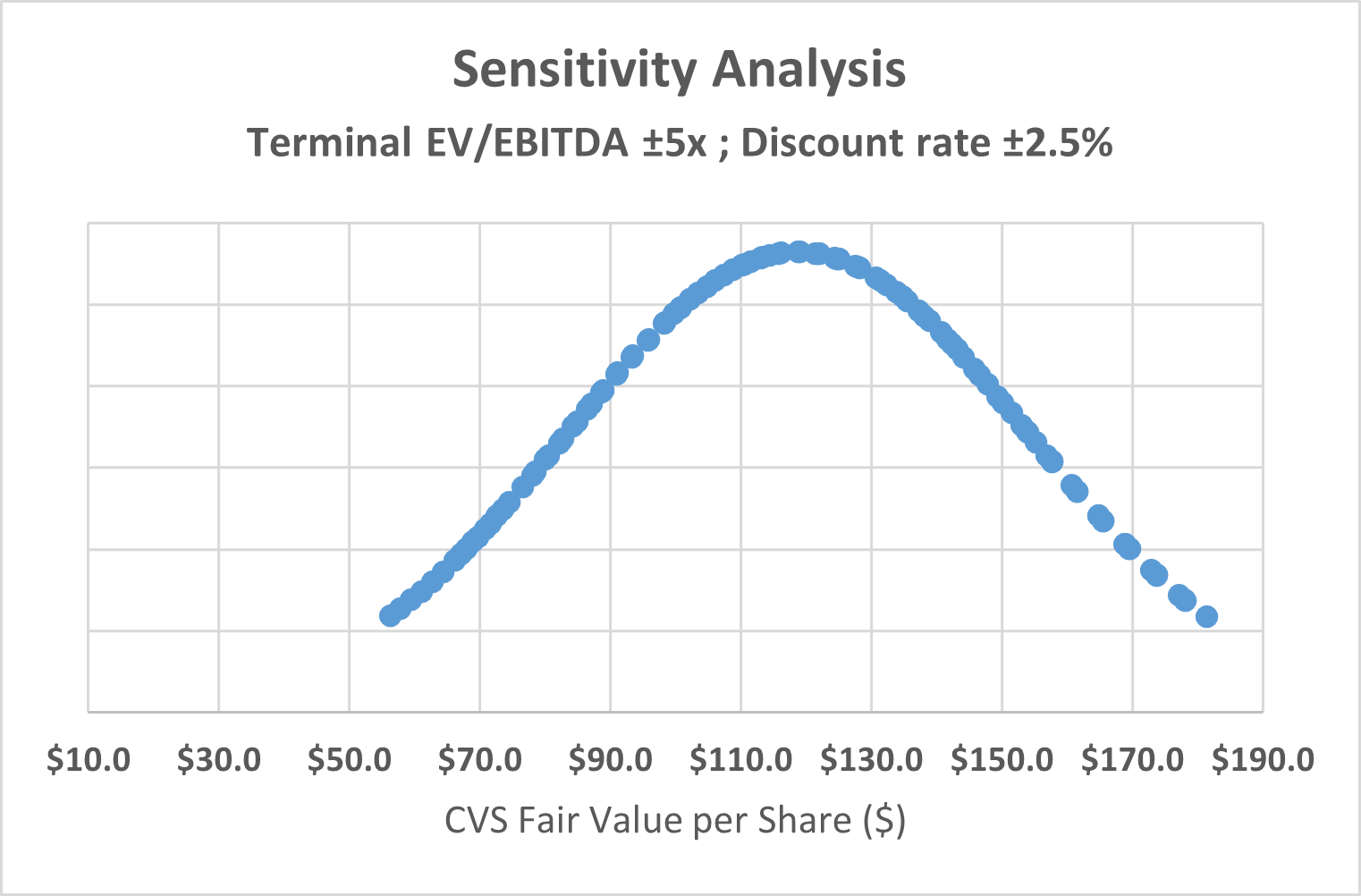

For the model, I used a 10% discount rate assumption. I then carried out a sensitivity analysis with regards to both the EV/EBITDA terminal multiple and discount rate.

{kind=link}

For the target price to fall slightly below $60, an EV/EBITDA of 5x and discount rate of 12.5% were required. The most likely range of values fell between $90 and $150.

Investment case

Arguably, CVS shares have been trading on the cheap side for a while. But with the market spooked by yet another large acquisition and worries of an economic downturn, CVS Health fell approximately another 20% and now trades around 52-week lows.

Despite acquisition woes, CVS core business is solid and cash-generating. Even better, its business is inflation and recession resistant. Healthcare is not discretionary spending, and even in a severe economic downturn, people are unlikely to cut down substantially on their wellbeing. While health spending is as essential as food, I would argue that there are some simple ways to reduce spending on food, but not on health.

Buying CVS today offers a trifecta of 1) a bargain base valuation, with shares trading at less than 6x TTM cash flow, 8x P/E; 2) interesting growth prospects, that the company’s management estimates can accelerate and reach “sustainable low double-digit adjusted EPS growth.” Even if I find such a view optimistic, EBIT growth of 7% - 8% looks achievable based on historical and industry results. 3) A recession-resistant business, that can weather the economic uncertainty ahead.

Furthermore, the company offers a decent dividend yield now exceeding 3%. Because of the Aetna merger, the dividend has been kept steady between 2017 and 2021, but it has been growing again at a healthy clip since then. Management seems committed to raising the dividend over time, and the company could become increasingly interesting for DGI investors as the 5-year average growth rate accelerates again.

Based on the $125 target I assign to CVS, there is an implied upside of approximately 70% or a 5-year annualized return of 16.3%. When also considering the dividends, the potential total return could reach up to 20% annualized. I rate shares a BUY.

Risks to the thesis

The main threat I see to my thesis is the high execution risk management faces. M&A activity tends to be hit or miss most of the time, with odds often skewed against the buyer. While prospects always look rosy on paper, the actual level of synergies and savings can rarely reach management’s optimistic forecasts. CVS made major gambles with Caremark and Aetna, but fortunately, they have worked out. While these were transformative deals, it is harder to argue that CVS really needed Signify Health or Oak Street Health to advance its growth plans. Skepticism is warranted, but on the flip side, because the recent transactions are relatively small compared to the overall company size, failure to deliver the expected results from the integration is unlikely to jeopardize the entire operation.

I have followed CVS for years after it purchased Aetna, but I never felt comfortable pulling the trigger because of the high debt load that came in connection with this merger, preferring to watch from the sidelines and monitor the combined entity's cash flow volumes. At the end of 2019, CVS's net indebtedness stood at almost $81 billion. Fast forward three years, and that figure stood at $55 billion, an impressive reduction of $26 billion. While the absolute debt load is still not small, it falls within 3x of CVS's EBITDA, supporting an investment-grade credit rating.

A second set of risks is related to regulatory changes in the US healthcare industry. US healthcare has been notoriously known internationally for its high costs, and unsurprisingly, it has often been at the center of political debate. During the pandemic, the Democratic party at some point called for a potential "Medicare for All" scenario, which would have abolished private insurance coverage. It goes without saying that this change would have been disastrous for the insurance benefit division of the company. A more moderate approach has since emerged, and I believe it is unlikely that disruptive reforms will pose an existential threat to CVS' business. On the other hand, it also seems clear that the industry is exposed to mild headwinds in the near to medium-term, like the pressure on Medicare Advantage rates that has forced management to seek mitigatory actions such as the OSH acquisition.

Conclusion

With a looming recession ahead, investors usually seek refuge in stable cash flows and recession-resistant revenues. The healthcare industry is one of the best sectors to hide during a recession, and it is therefore unsurprising to see healthcare as the second best performing sector in the US (after industrials) over the last twelve-month period. While I try to be agnostic to short-term market movements when I choose my long-term investments, I also recognize the importance of balancing long-term investments with capital preservation and timing decisions to maximize returns.

Healthcare industry-wide valuations are not cheap now, with Morningstar only identifying a handful of 5-star rated stocks. Most of these companies are within the cannabis industry. While I do think opportunities exist in cannabis, companies in this space are typically small caps with weaker financial positions and due to the illegal status of cannabis at the US federal level, investment risks are high. Among the very few non-cannabis undervalued stocks identified by Morningstar, CVS Health is an investment-grade, large cap company.

In my opinion, CVS offers one of the best risk-adjusted returns available on the market today. The company operates a cash-rich, predictable business with steady margins and recession-resilient revenues. With shares trading at a bargain price near 52-week lows, I anticipate an annualized return of approximately 20% over the next five years for investors, based on a 70% upside to my fair value estimate of $125 and a current dividend yield of 3.3%.

Editor's Note : This article was submitted as part of Seeking Alpha’s Best Investment Idea For A Potential Recession competition, which runs through April 28. This competition is open to all users and contributors; click here to find out more and submit your article today!

For further details see:

CVS Health: This Cash-Rich, Predictable Business Should Fare Well Even In A Potential Recession