CBAY - CymaBay: Long Term Is Constructive With Potential Seladelpar Conversion

Summary

- CymaBay caught a strong bid in early FY23 after advising its collaboration with Kaken Pharma in Japan.

- Its seladelpar compound has potential to create a medical breakthrough in primary biliary cholangitis.

- This could disrupt the current treatment paradigm and enable CBAY to capture market share rapidly.

- Net-net, rate buy.

Investment Summary

In FY23, we continue building out exposure to underappreciated names within the healthcare spectrum that are working toward a medical breakthrough in complex disease segments. Immediately we turn readers' attention to CymaBay Therapeutics, Inc ( CBAY ), noting its stock caught a tremendous bid off its FY22 lows and has re-rated at a factor of 1.7x since December. Underscoring the extensive repricing was the firm's announcement it will team up with Kaken Pharmaceutical in Japan, to develop its investigational seladelpar compound. Seladelpar is indicated in the treatment of primary biliary cholangitis, and has gained additional traction in other potential indications, with CBAY building its pipeline around these [see: Figure 3]. However, it is the company's biliary cholangitis hypothesis with seladelpar that has us most interested in accumulating a position in its stock,. This is due to 1) the complexities of the condition; 2) the lack of positive long-term treatment outcomes; and 3) the unmet clinical need within this disease segment. In this deep dive I'll run through all of the moving parts in the investment debate for seladelpar, looking specifically at primary biliary cholangitis, to guide the most informed investment reasoning possible. Net-net, we rate CBAY stock a long-term buy, searching for initial potential targets in the $13 range.

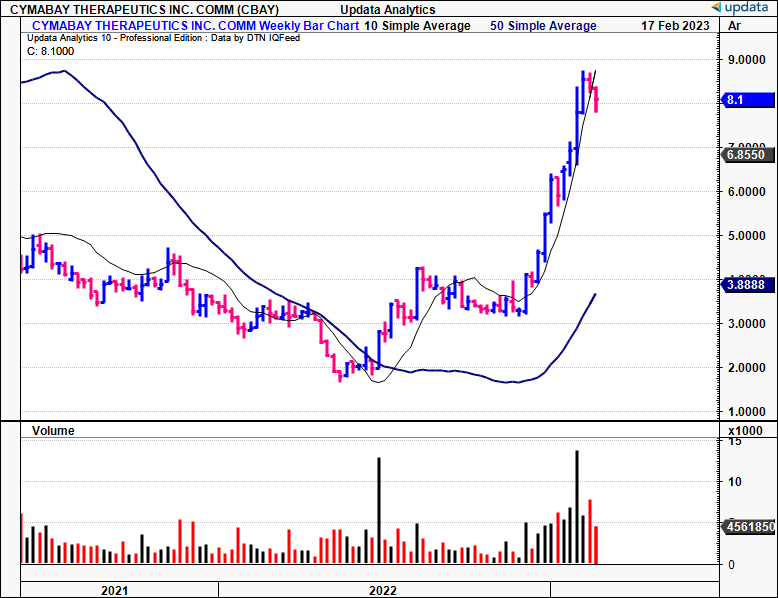

Fig. (1) CBAY Weekly price evolution, FY21–date

{kind=link}

Key catalysts to drive CBAY shares higher

The major development in CBAY's growth route is the collaboration with Kaken Pharma to develop its seladelpar compound in Japan, mentioned above. As also mentioned, seladelpar's indication in the treatment of primary biliary cholangitis ("PBC") has the potential to disrupt the current standard of care, closing an unmet gap within the treatment domain. It is therefore important to have a fundamental understanding of the condition in order to understand the investment opportunity here:

1). PBC is classified as an autoimmune disorder of the small intra-hepatic bile ducts

It is characterized by the progressive destruction of said ducts, with subsequent breakdown of biliary epithelial cells, and eventual replacement by fibrotic [scar] tissue. The buildup of this scar tissue eventually leads to biliary obstruction. The aetiology of PBC is still largely unknown, but genetic factors are thought to responsible for its pathogenesis. In particular, there is an increased risk of PBC in individuals with certain human leukocyte antigen ("HLA") haplotypes, such as HLA-DR3 and HLA-DR4. For reference, both of these serotypes are frequently associated with autoimmune diseases. Additionally, genetic variants in the CD4, CD8, and TCR genes have been associated with PBC. There's also an environmental component of PBC, thought to be related to infection, such as Helicobacter pylori bacteria, that may trigger an aberrant immune response. Clin ically , P BC presents with elevated levels of serum enzymes such as alk aline phosph at ase , am in ot rans fer ase , and gamma - gl ut am yl transfer ase. Physical signs include pr ur itus , fatigue and j aund ice , but diagnosis requires bloodwork and additional imaging to rule out to exclude other liver/bile duct complications.

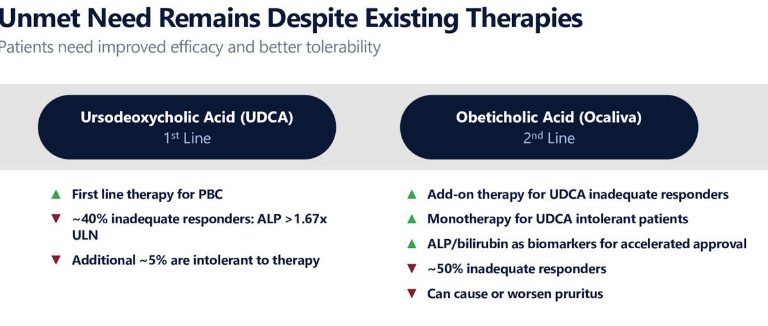

2). The current standard of treatment for PBC is the administration of ursodeoxycholic acid ("UDCA" )

It has been the treatment standard since the 1980's. UD CA has been shown to be effective in improving biochemical parameters and slowing the progression of hist ological damage with PBC , also providing sympt omatic relief . However, efficacy response is illustrated at ~50–70%, and there's a raft of side effects associated with long-term usage. The remainder of treatment is made up with obeticholic acid, again with questionable response efficacy [Figure 2]. Consequently, CBAY's seladelpar compound has emerged as a potential alternative to UDCA. Looking at its pharmacology, seladelpar is a potent and selective agonist of peroxisome proliferator-activated receptor delta ("PPARD"). This is a nuclear receptor expressed in the liver, that plays a role in regulating lipid and bile acid metabolism. This is actually quite an interesting hypothesis. By binding to PPARD, seladelpar activates pathways that lead to reduced cholestasis, improved bile acid synthesis, and decreased production of pro-inflammatory cytokines. Subsequently it directly addresses the underlying mechanics that result in PBC in the first place.

Fig. (2)

Image retrieved from CBAY investor presentation, August 2022, pp. 8

{kind=link}

3). The economics of the PBC treatment market are an attractive feature in the CBAY investment debate

It is estimated to reach $ 1 .75 Bn by FY 28' , growing at CAGR 10.5 % into that period. Further research points to a 10.5% geometric growth over the same period . Earlier research from FY18' projected a CAGR 36% into FY26'. Market research also suggests the growth is set to be driven in part by the introduction of new treatments . Hence, this provides a good springboard for uptake of seladelpar if it reaches commercial status. Moreover, UD CA currently accounts for > 80 % of the market. It is also expensive, and this has been labelled as a potential inhibitor of its growth looking ahead. In that vein, there's concentration risk in the treatment market, meaning that CBAY's alternative has potential to rapidly steal market share in our opinion.

4). Still, PBC treatment is dominated by exceptionally large players like AbbVie, Merck, Pfizer, Sanofi, and Gilead

The majority of these companies focus on the UD CA route. CBAY would therefore be competing against these names – yet, there's no saying further collaborations will be off the table. In fact, the presence of these large names within the space illustrates to us a high probability of collaboration by the best estimation. For CBAY, this would markedly reduce its execution risk in commercialization, and for the large players, it would reduce their pipeline risk, enabling both parties to retain a higher EBIT margin.

5). Looking at its deal with Kaken, we see evidence of this kind of benefit for CBAY already in situ

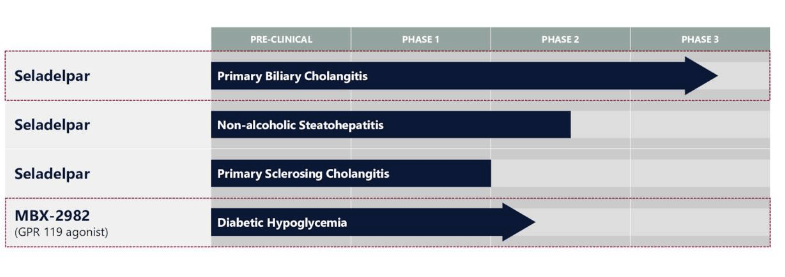

The terms dictate that Kaken has exclusive licensing to develop and then commercialize seladelpar in Japan. It will assume this responsibility for the Japanese market if the compound successfully advances through all late-stage processes to development. Subsequently, CBAY will receive an upfront payment of ~$34mm, and is entitled to additional milestone payments up to $128mm. CBAY will also receive a 20% royalty of net sales. Consequently, this reduces the execution risk for CBAY, whilst mitigating the pipeline risk for Kaken, as mentioned earlier. This is also a particularly strong deal for CBAY, seeing as there are currently no approved treatments for PBC in Japan – UDCA included. Hence, if successful, the CBAY/Kaken duo will have the entire share of the Japanese PBC market. Research Outreach (2020) explained that >37,000 people are likely to have PBC in Japan. Lemos (2013) illustrated that UDCA costs ranges from US$2,240–$4,100, depending on dosage per kilogram – however, that was back in FY13'. Whilst we don't make any assumption seladelpar will cost the same as UDCA, if we presume at least a 50% weighted acquisition cost ("WAC"), and a 70% penetration of the Japanese PBC market, this is a $53mm per year opportunity for the compound in Japan [note: these are very basic assumptions to provide context]. CBAY's seladelpar full pipeline is observed below.

Fig. (3)

Image retrieved from CBAY investor presentation, August 2022, pp. 3

{kind=link}

Financials

CBAY is pre-revenue, given its pre-clinical status. It recorded $30mm in cash on the balance sheet last report , with an additional $122mm in marketable securities. Subsequently, it had $150mm in immediate liquidity by Q3 FY22'. In addition to these numbers, it also raised an additional ~$85mm via secondary public offering in January, selling 10mm shares and pre-funded warrants at $7/share. Proceeds will be used to advance developments of seladelpar. Given the company's confidence in raising at this market cap, along with the Kaken collaboration investors were quick to jump in, rallying the stock to 52-week highs with authority. Henceforth, it is well capitalized to continue pushing for seladelpar's approval status. Its current ratio is at 12x and the capital structure includes $86mm in long-term debt, whereas equity holders sit at $60mm in book value. Hence, the debt ratio is 62%, leading to $0.70 in book value per share. Looking at a TTM basis, the company burnt through $38mm in cash from Q1–Q3' last year, on a net debt issue a ~$50mm in debt in Q3. We expect that CBAY will require further external financing before it reaches commercial stage, a potential risk factor that is discussed later.

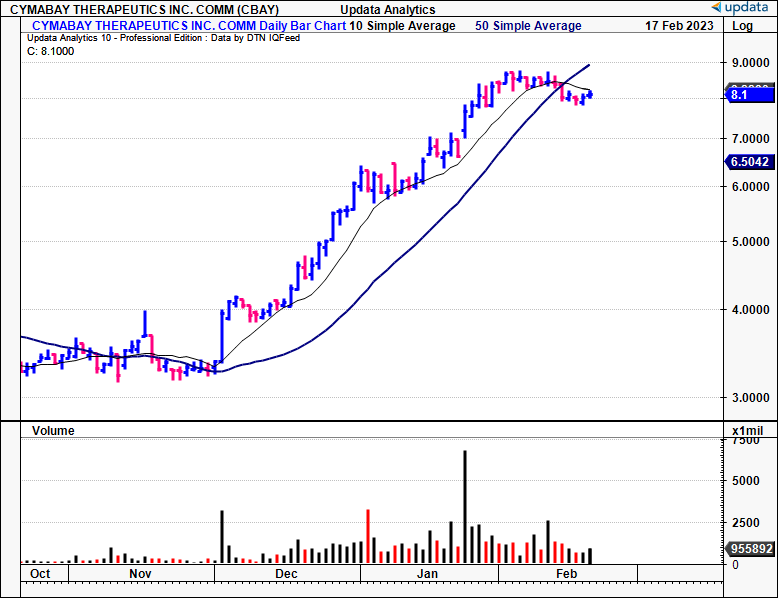

CBAY technical picture

Looking to the charts, the stock has crossed back beneath the 250DMA this month, after a strong rally off its December lows. The 50DMA had acted as strong support as it ran up the page, but CBAY has crossed this level as well. Volume trends have been declining as well. The question from here will be, if it can reverse course and again rally back to the upside. The 50DMA/250DMA cross is a potential risk factor, and we'd like to see these cross back to the upside to support the immediate upside case.

Fig. (4)

{kind=link}

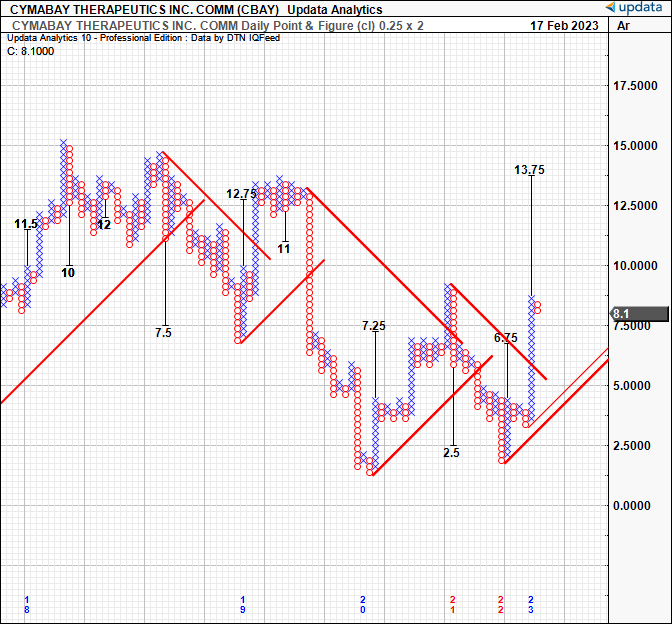

Looking to the point and figure studies, that measure price action without the noise of time or short-term machinations of the market, we have an upside target to $13.75. This is something to factor into the investment debate, as it exhibits that the price upside could lead to a further re-rating higher. You'll see the $6.75 target that was thrown off in June was met with conviction. Hence, this provides a good range for investors to look toward into the coming periods.

Fig. (5)

{kind=link}

Risks

There are several risks that must be considered into the CBAY buy thesis. Chief among these is the r egulatory risk. Being an early stage biotech, its success is dependent on seladelpar moving through late-stage clinical trials and obtaining FDA approval in the U.S., Japanese government approval in Japan, CE Mark in the EU, ATAGI approval in Australia, and others in various jurisdictions. In that vein, i f it doesn' t receive regulatory approval , or if the clinical trials are delayed or terminated , its likely investors will punish the stock. We also mentioned above the stiff competition for PBC treatments from the various global pharma elites. This is a key risk that must be considered as well. If any of these competitors build on innovations made by CBAY, or develop more cost - effective substitutes, this will likely limit the upside potential in terms of sales growth. Finally, we'd also highlight that CBAY will likely have to continue raising external financing until it is able to achieve commercial success with seladelpar [or any of its pipeline]. This must be factored in as well, because it may dilute current shareholders, or, equity offerings may only be made to certain investors. Collectively, investors should recognize these risks in their entirety before making any investment decisions.

In short

CBAY presents as a differentiated offering for investors speculating on clinical-stage assets. Its seladelpar segment is gaining momentum with the Kaken collaboration, adding further credence to its propensity for regulatory approval. We are bullish on CBAY for the long-term and believe it has potential to create a remedial breakthrough in PBC, with a large chance to steal market share from the current standard of care in UDCA. The economics of the PBC market are equally as interesting, with potential for high-growth over the coming years, based on market research. Seeking Alpha's quant system has it rated as a 'strong buy' and this adds further weight to our buy call. Investors must recognize the risks discussed before any investment decisions. Net-net, rate buy.

Fig. (6)

{kind=link}

For further details see:

CymaBay: Long Term Is Constructive With Potential Seladelpar Conversion