INVE - Daktronics: Still Not The Sign To Unload Stock

2023-03-22 10:51:54 ET

Summary

- Daktronics continues to post strong sales, profit, and cash flow results, and backlog is up year-over-year.

- DAKT stock looks affordable on an absolute basis and it's cheap relative to other firms.

- The business also has attractive growth potential from here that management can capitalize on and it has the footprint necessary to pursue it.

While I do not believe for one second that markets are efficient or close to it, I also don't believe that they are so inefficient that they would often provide an opportunity to generate significant returns relative to the market, and still have additional significant upside than investors can capture after the initial move higher. But one of the opportunities where this does appear to be the case is with Daktronics ( DAKT ), an enterprise that designs and produces electronic scoreboards, programmable display systems, and large video screen displays for a variety of venues. Recently, financial performance achieved by the business has been robust. Add on top of that the fact that shares look cheap, and it's hard not to like the business. But what's really exciting is that shares are cheap even after the stock has skyrocketed in recent months during a time that the broader market has declined. And to make matters even better, growing backlog and a large global market opportunity make the business a compelling prospect for long-oriented investors.

A sign of great things to come

In early December of last year, I found myself revisiting my prior investment thesis regarding Daktronics. In that article , I found myself impressed by the continued sales growth that the company had seen, but I also acknowledged that some of its bottom line results had worsened. That worsening, combined with broader economic concerns, caused me to be less optimistic about the company's prospects than I was previously. Even so, I still maintained the company as a ‘buy’ candidate. Since then, things have gone remarkably well. Even though the S&P 500 has declined by 2.5%, shares of Daktronics have generated upside of 41.9%. And since initially rating the company a ‘buy’ in August of last year, shares are up 27.9% compared to the 4% drop the broader market has experienced.

{kind=link}

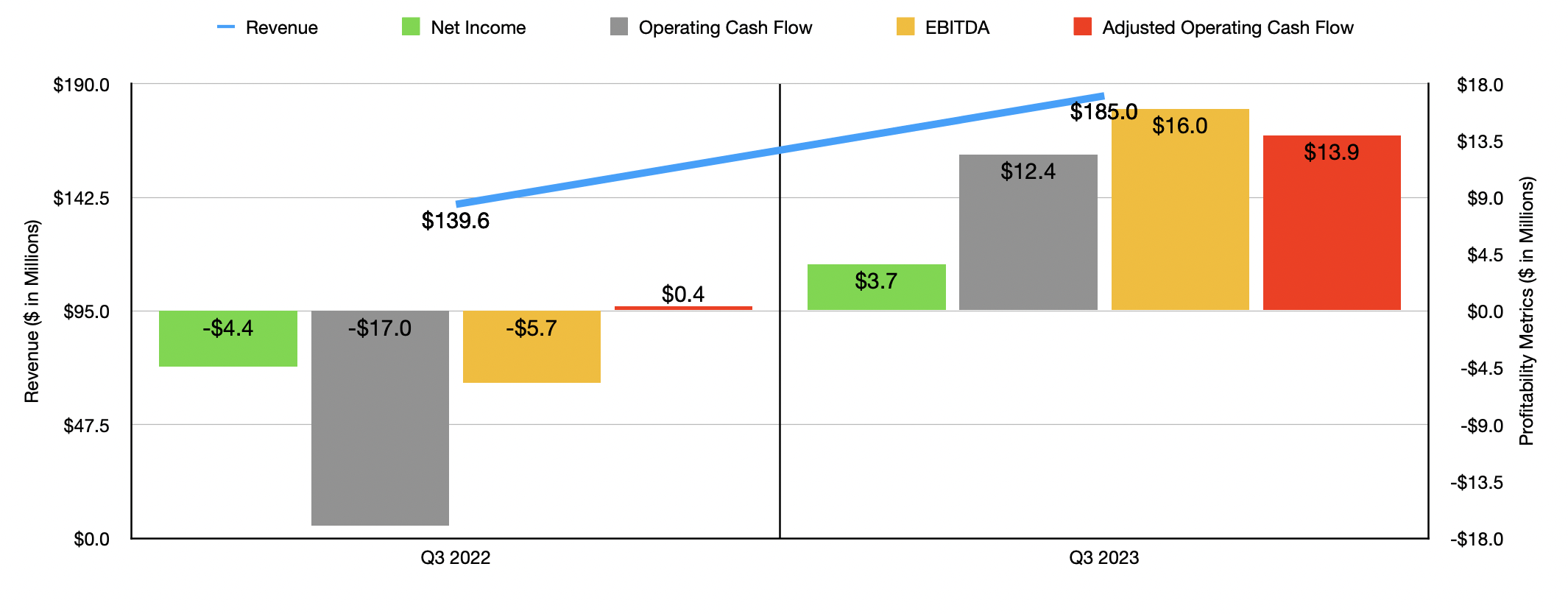

Although I had my moments of doubt back in early December, my thoughts on the company and its prospects have definitely evolved over the past few months. Before we get into exactly what the firm's opportunities are moving forward, we should touch on some of its recent financial performance. In the latest quarter for which data is available, the third quarter of the 2023 fiscal year, the company reported revenue of $185 million. That represents an increase of 32.5% over the $139.6 million in sales reported one year earlier. This growth was driven by strength across the board. Although international revenue for the company grew only 2.4%, other portions performed very strongly. The most significant upside came from the live events category. Sales here spiked 73.5% from $39.1 million to $67.7 million. That increase, management said, was driven by strong market demand, greater production capacity, and higher prices that the company implemented later in the 2022 fiscal year and early in 2023. Over that same window of time, commercial revenue grew 24.6% from $40.1 million to roughly $50 million. This is not to say that everything was great. Order volumes did decrease year over year. But that's to be expected in an inflationary environment.

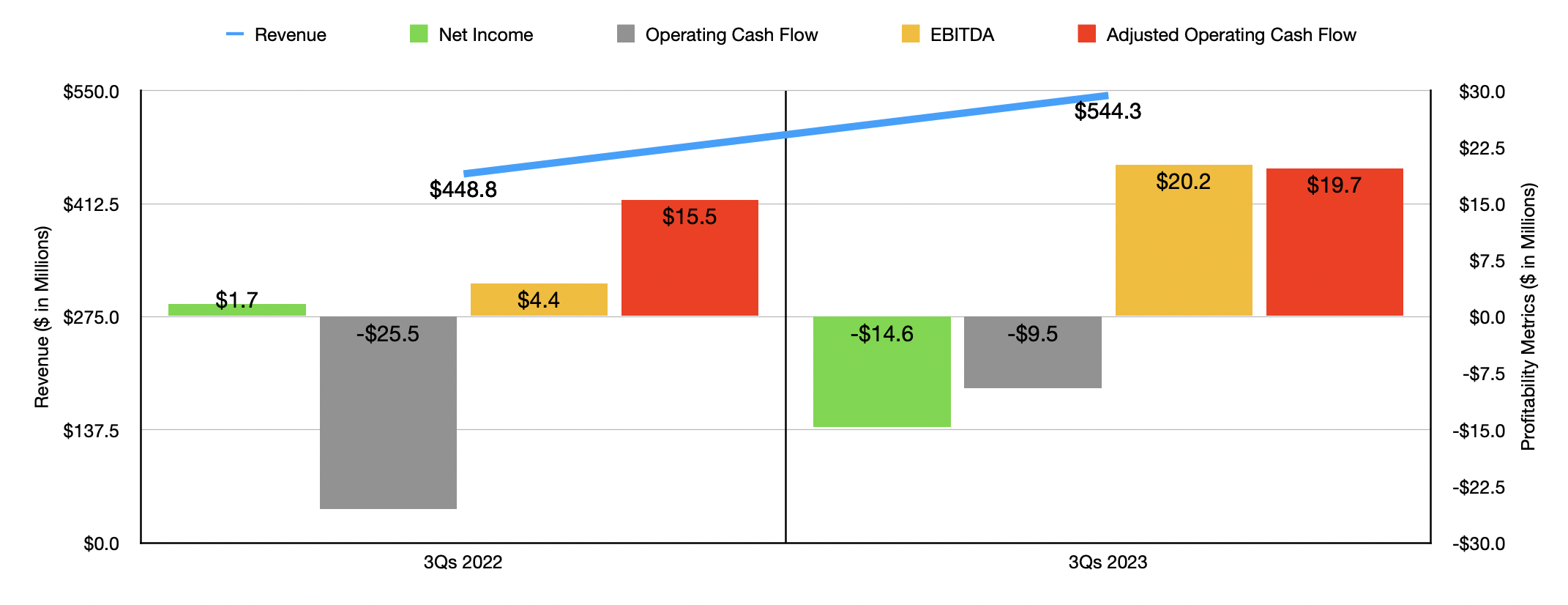

The price increases that the company was able to push through, combined with the other aforementioned factors, helped push the firm's bottom line up as well. The business went from generating a net loss of $4.4 million in the third quarter of the 2022 fiscal year to generating a profit of $3.7 million in the third quarter of the 2023 fiscal year. Other profitability metrics followed a similar trajectory. Operating cash flow, for instance, went from negative $17 million to positive $12.4 million. If we adjust for changes in working capital, it would have gone from $0.4 million to $13.9 million. Meanwhile, EBITDA turned from negative $5.7 million to $16 million. As you can see in the chart below, results for the first nine months of the 2023 fiscal year were definitely more mixed relative to the same time one year earlier compared to what was seen in the third quarter. But on the whole, the company benefited from rising sales and mixed but generally growing cash flows.

{kind=link}

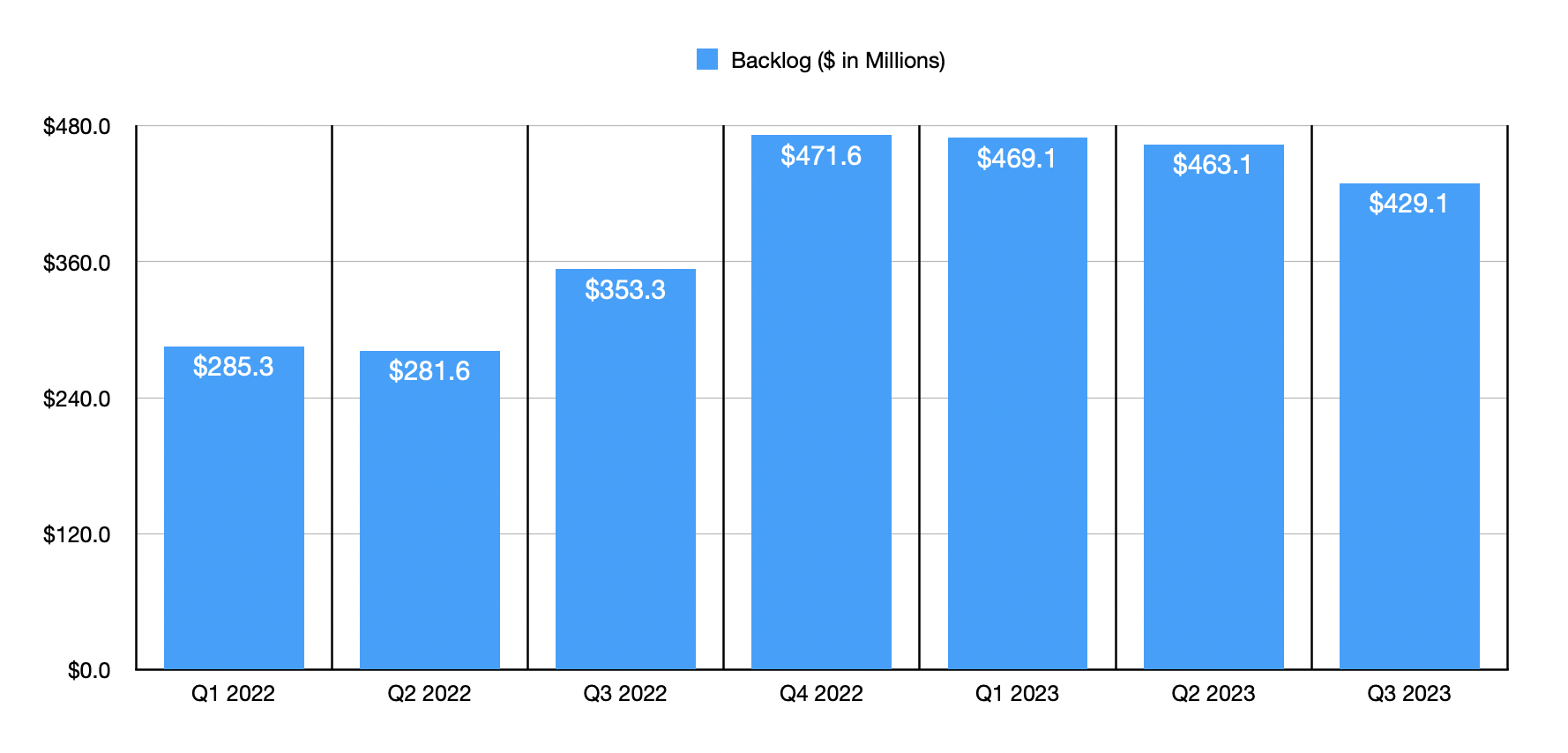

Outside of the most recent data provided by management, there's also the fact that the company has some great opportunities in the long run. The first sign of this emerged in the firm's backlog. As of the end of the latest quarter, backlog for the business totaled $429.1 million. That's up meaningfully compared to the $353.3 million reported one year earlier, though it is down from what it was in the prior few quarters. While I would not be surprised to eventually see some pullback because of broader economic concerns, the data that's available today suggests that, in the long run, backlog for the business is set to continue growing. I say this because of what the broader market opportunity is for the LED display space.

{kind=link}

At this moment, the vast majority of the company's revenue comes from the US. For the first three quarters of the 2023 fiscal year, for instance, 87.1% of sales came from here at home. No other country accounted for such a large portion of sales that management was forced to report data for. But we do know that the company has sales offices throughout parts of Europe such as Spain, France, Germany, the UK, and elsewhere. It also has a presence in Canada, the Middle East, China and Southeast Asia, Australia, and Japan. Clearly, management has been laying the groundwork to make this into a global enterprise.

{kind=link}

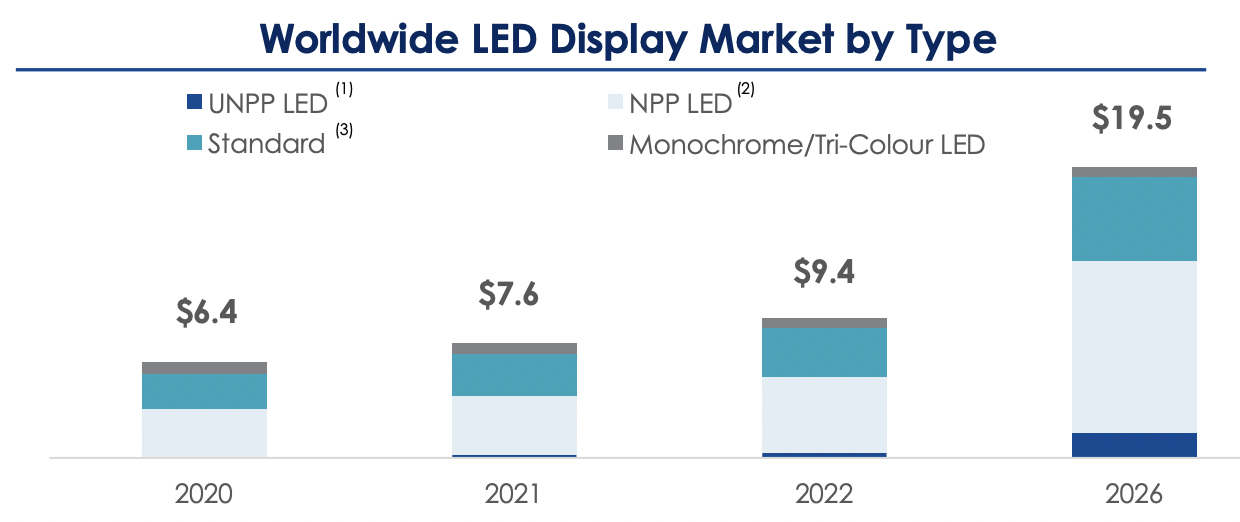

This is a great thing, because the global opportunity for the LED display market is fantastic. In 2022, the market opportunity was worth around $9.4 billion. By 2026, it's estimated to grow to about $19.5 billion. That translates to a roughly 20% annualized growth rate for the business. Most of that growth should take place in the areas in which the company has a presence. Today, the market in those regions totals about $8.7 billion. But by 2026, it should expand to $18.8 billion. In North America alone, the overall market opportunity for the company using data from 2021 was $1.2 billion, with Daktronics boasting a 45.1% market share. Excluding China, the international market in that year was worth about $1.7 billion. And at that time, Daktronics controls only about 4.9% of that market. This leaves open the opportunity for significant growth overseas.

{kind=link}

This is not to say that the company's prospects are only good overseas. There is still a sizable market opportunity for them to capture here at home. And based on recent data revealed by management, the company seems to be doing a good job there. In early February, for instance, management announced that the company had been selected to install one of the largest video displays in baseball at Citizens Bank Park in Philadelphia. And in Minnesota, at Target Field, the company was chosen to upgrade visitor experience by installing an HDR-capable main video display that is roughly 75% larger than what was there previously. This will include more than 13.1 million LEDs and 23,000 square feet of LED displays across the 22 different displays that the company has been awarded at that park for the 2023 season.

{kind=link}

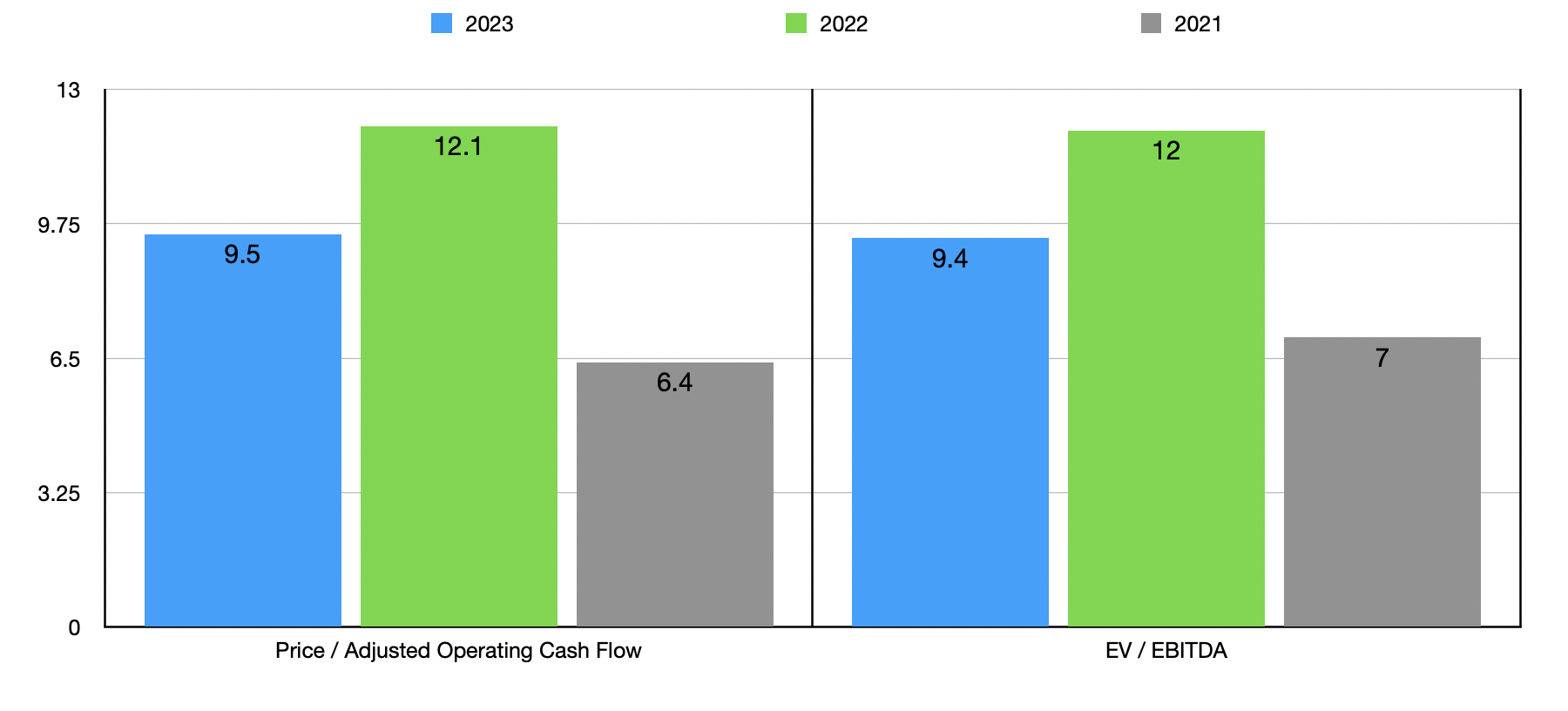

Even if the company does not grow from here, shares would look attractive in my view. If we annualize results experienced for the 2023 fiscal year so far, we would get adjusted operating cash flow of $23.3 million. Meanwhile, EBITDA for the company would be $24.7 million. Using this data, I was able to value the company. This can be seen in the chart above, along with valuations using data from 2021 and 2022. Though far from being a perfect match, I did compare the company to five businesses that I felt were the closest from an operational perspective. As you can see below, using the price to operating cash flow approach, these firms ranged from a low of 24.9 to a high of 506.9. Meanwhile, using the EV to EBITDA approach, we get a range of between 10.5 and 63. Compared to the 2023 estimates, Daktronics is cheaper than any of its peers.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Daktronics |

| 9.5 |

| 9.4 |

| Luna Innovations ( LUNA ) |

| 506.9 |

| 63.0 |

| Iteris ( ITI ) |

| 48.2 |

| N/A |

| Identiv ( INVE ) |

| 97.5 |

| 57.1 |

| National Instruments Corp. ( NATI ) |

| 156.2 |

| 25.3 |

| OSI Systems ( OSIS ) |

| 24.9 |

| 10.5 |

Takeaway

From what I can see today, Daktronics is a solid business that is doing a remarkably good job at this point in time. The company is performing well and its backlog has done nicely on a year-over-year basis. Add on top of this the fact that shares look cheap and that the firm has an attractive catalyst for growth from here, and I do think that it makes for a reasonable prospect even after seeing its stock price rise so much. So because of this, I've decided to keep the ‘buy’ rating I had on the company previously.

For further details see:

Daktronics: Still Not The Sign To Unload Stock