FSLR - Daqo: Trifecta Of Glut Volatile Spot Prices And Geopolitical Discounts

2023-09-03 12:00:00 ET

Summary

- DQ's higher sales volume is not able to counter the falling ASPs, as witnessed in the drastic decline of its annualized FQ2'23 EPS and gross margins.

- The embedded geopolitical discount in its stock valuation of NTM P/E of 4.30x is highly apparent, compared to the sector median P/E of 8.00x and FSLR NTM P/E of 17.28x.

- This is despite the DQ stock's undervaluation, compared to its FQ2'23 book value of $63.40 and cash horde of $3.17B.

- It remains to be seen if its bullish support may sustain at these levels, as the DQ stock retests the critical support level at the $35s, potentially triggering more near-term volatility.

- Due to the potential commoditization of polysilicon panels, the correction in its valuations, and the volatility in the polysilicon ASPs, we prefer to observe the developing situation for a little longer.

The DQ Investment Thesis Has Been Destabilized By Volatile Spot Prices

We previously covered Daqo New Energy ( DQ ) in June 2023, discussing the IRA domestic content tailwinds, with solar developers allowed to claim up to 40% in tax credits with only 40% in solar components to be made within the US.

We had bullishly projected that its Mongolia plant might potentially side-step the Xinjiang trade ban due to the tax credit clarity, triggering the expansion of its top and bottom lines from FQ2'23 onwards.

On the one hand, DQ has reported an exemplary sales volume of 51.55K MT in FQ2'23 (+103.9% QoQ/ +37.3% YoY ), demonstrating the robust demand for polysilicon. Its production volume has also drastically expanded to 45.3K MT (+33.8% QoQ/ +28.2% YoY), thanks to its production ramp in Mongolia.

On the other hand, due to the polysilicon supply glut, the average selling prices have also plunged to $12.33 per kg in the latest quarter (-55.6% QoQ/ -62.7% YoY), naturally impacting its gross margins to 40.7% (-30.7 points QoQ/ -35.4 YoY).

While DQ remains profitable, we are not surprised by the stock's underperformance over the past few months indeed. It is apparent that the higher sales volumes are not able to counter the falling ASPs, as witnessed in the drastic decline in its annualized FQ2'23 EPS of $5.40 (-61.4% QoQ/ -83.5% YoY).

Moving forward, its fully ramped up production in Inner Mongolia may potentially further optimize its production costs, with the management already reporting a notable moderation to $6.92 per kg (-8.3% QoQ/ -4.6% YoY) in the latest quarter.

The DQ management has also raised its FY2023 polysilicon volume to 195.5K MT at the midpoint ( +46.1% YoY ), compared to the previous FQ4'22 guidance of 192.5K MT (+43.8% YoY). This is on top of the pilot production of its higher margin semiconductor-grade project with 1K MT annual capacity from September 2023 onwards, potentially balancing its impacted ASP headwinds.

So, Is DQ Stock A Buy , Sell, or Hold?

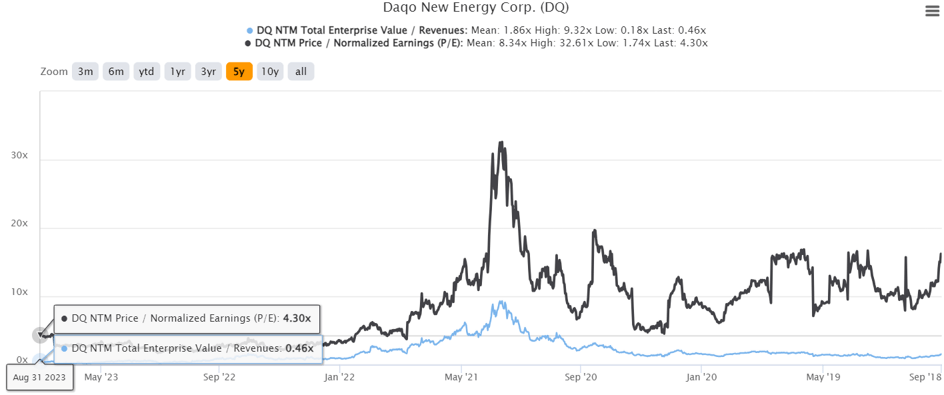

DQ 5Y EV/Revenue and P/E Valuations

{kind=link}

For now, DQ trades at NTM EV/ Revenues of 0.46x and NTM P/E of 4.30x, improved compared to its 1Y mean of 0.44x/ 2.66x, though drastically moderated from its 3Y pre-pandemic mean of 1.69x/ 9.01x.

The embedded pessimism is even more notable, compared to the sector median P/E of 8.00x and First Solar's ( FSLR ) NTM P/E of 17.28x, suggesting the impact of the Chinese ADR geopolitical discount and polysilicon supply glut.

Despite this, the DQ stock is also inherently undervalued, compared to its FQ2'23 book value of $63.40 (-1.9% QoQ/ +17.5% YoY), which is largely attributed to its cash horde of $3.17B (-23.2% QoQ/ -3.6% YoY).

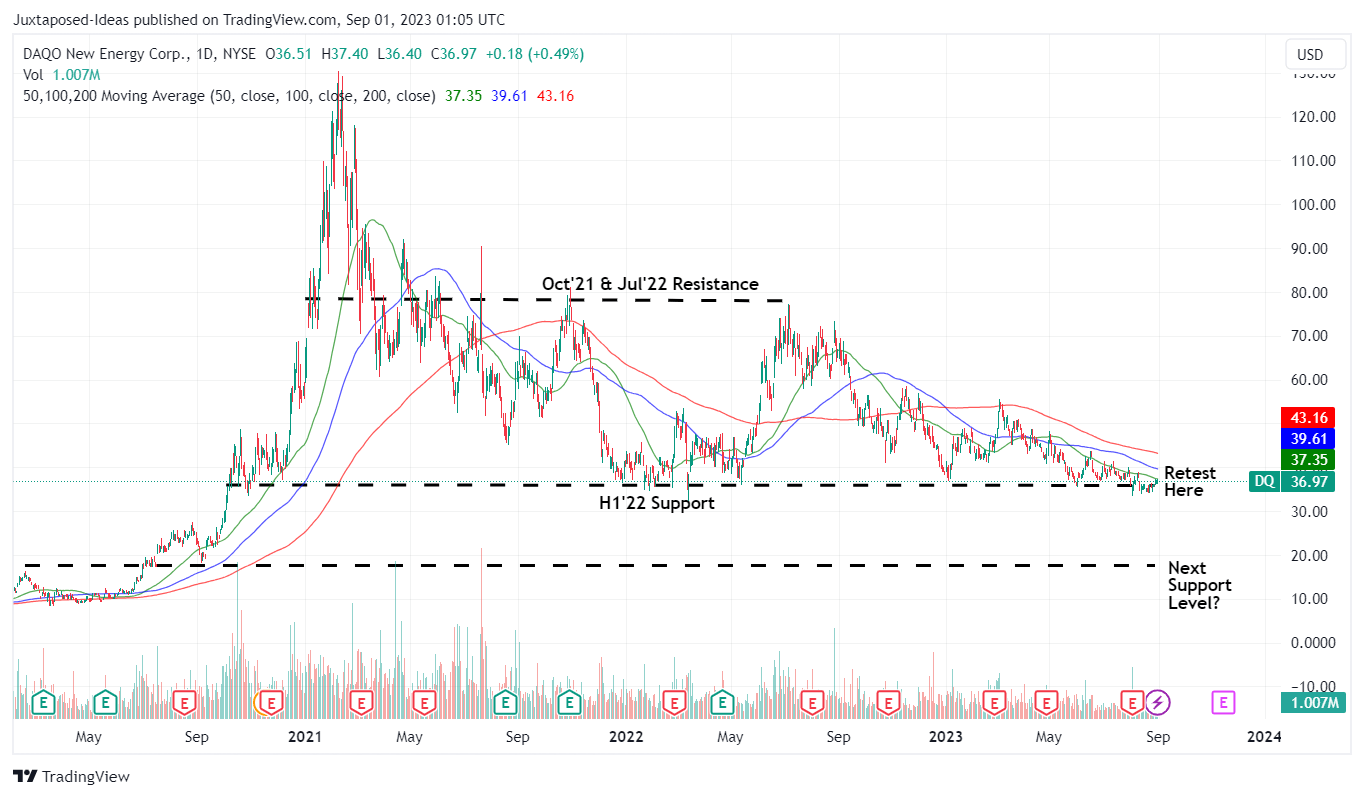

DQ 5Y Stock Price

{kind=link}

For now, it remains to be seen if its bullish support may sustain at these levels, as the DQ stock retests the critical support level in the $35s, potentially triggering more near-term volatility.

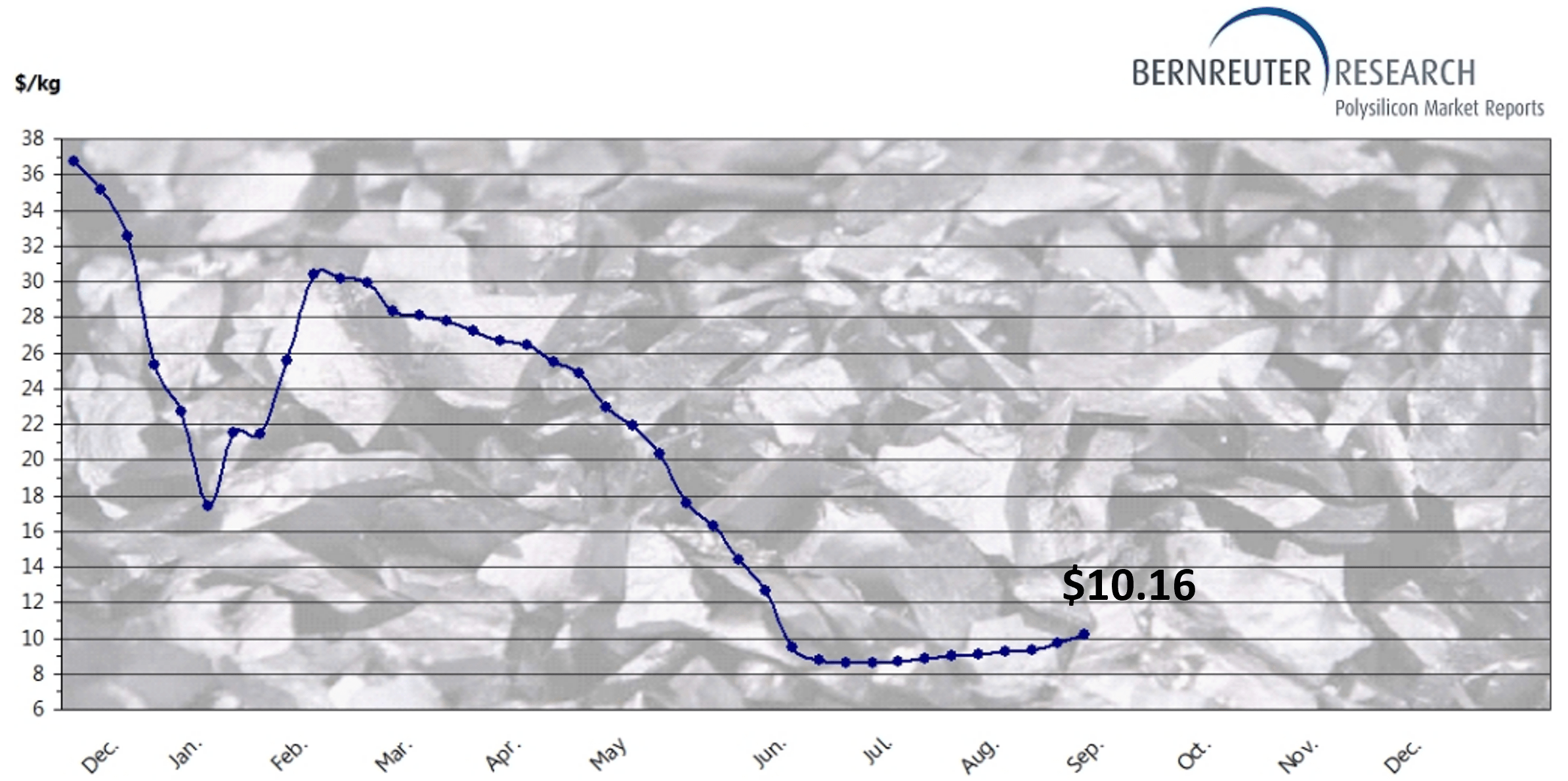

Global Polysilicon Spot Prices

EnergyTrend, Bernreuter Research

{kind=link}

Combined with the decline of polysilicon spot prices to $9s per kg in Q3'23, we may see DQ's financial performance further disappoint in the upcoming quarter, naturally impacting its stock prices.

However, we may see things improve by Q4'23, with the management already reporting a bottoming of price volatility as prices recover to $10.16 per kg by August 30, 2023, attributed to the easing of the domestic price war and inventory clearance in Q2'23:

By mid-July, we saw an approximately 15%-20% price recovery compared to the bottom reached in June. Recently, we have also seen an increase in the ASP premium for N-type polysilicon with a meaningful increase in demand volume. We expect that this trend will further benefit us as the industry transitions to next-generation N-type technology. ( Seeking Alpha )

While DQ reported elevated inventory levels of $159.49M by the end of June 2023 (-16.8% QoQ/ +205.1% YoY), most of these are attributed to the slower than expected "customer qualification process" from the Inner Mongolia facility.

With this process already cleared by end of July 2022, the management has already reduced its inventory levels to "approximately one week of production across our two facilities" by the time of the conference call in early August 2023.

Here comes the biggest question indeed. Is it wise to buy DQ here?

We have previously projected a long-term price target of $59.70, based on its historical P/E of 8x and the consensus FY2024 EPS estimates of $7.48. However, we are no longer certain if it is wise to formulate another buy investment thesis based on a rearview mirror P/E outlook.

This is especially due to the potential commoditization of polysilicon panels, as the global manufacturing capacity of solar PVs expand drastically to 1K GW by 2024 , more than double of the 450 GW reported in 2022.

As a result of the potential correction in its valuations and volatility in the polysilicon ASPs, we prefer to rate the DQ stock as a Hold (Neutral) here, while observing the situation for a little longer.

For further details see:

Daqo: Trifecta Of Glut, Volatile Spot Prices, And Geopolitical Discounts