DDOG - Datadog Earnings Surprise: The Peter Lynch Hypothesis In Action

2023-08-08 09:41:49 ET

Summary

- Datadog, Inc.'s Q2 results surprised me with a slowdown in revenue growth rates.

- Despite the growth slowdown, Datadog's underlying profitability is set to improve.

- I am cautious about Datadog's valuation and its ability to regain growth momentum in 2024.

- The company's downward revision of revenue projections raises questions about its future performance.

- What's the Peter Lynch Hypothesis? How this can be used on the long or short side.

Investment Thesis

Datadog, Inc. ( DDOG ) reported Q2 results that took investors by surprise. The biggest takeaway from this earnings result is the most obvious, that Datadog is no longer a growth company.

That being said, this earnings report wasn't all bad news, and in actuality, Datadog's underlying profitability is set to improve further.

However, given its valuation, I remain on the sidelines. Here's what you need to know.

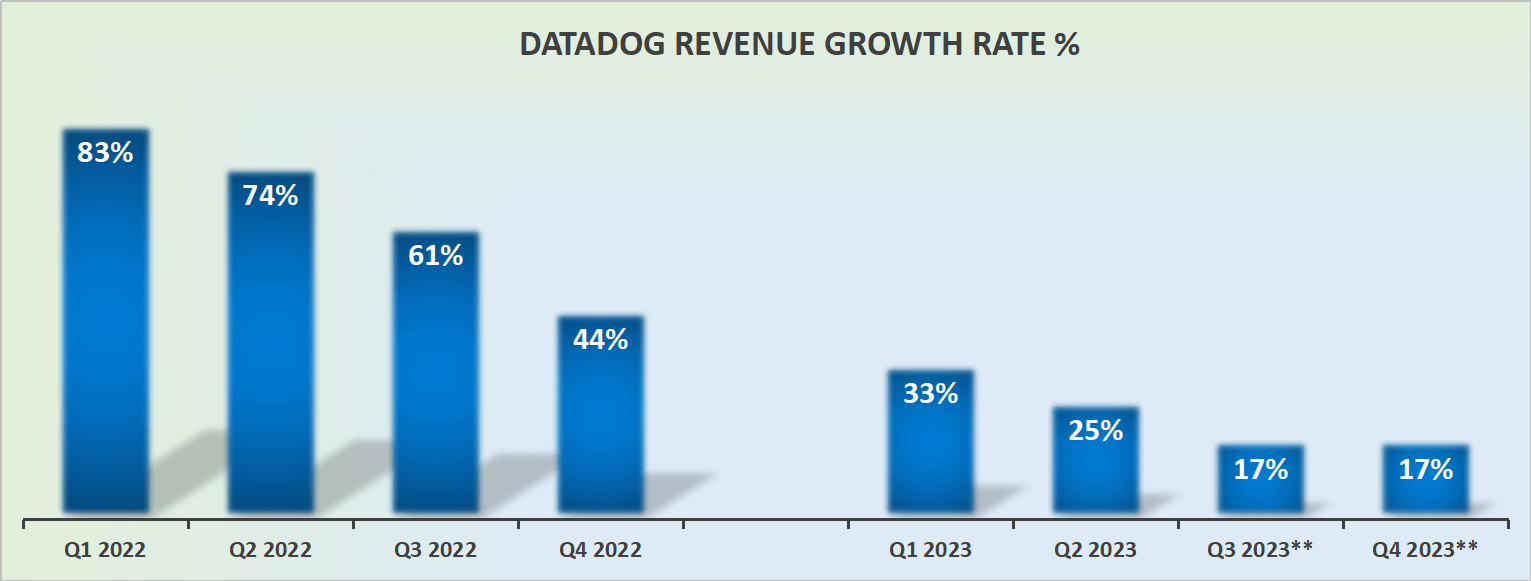

Revenue Growth Rates Hit the Breaks

Datadog provides monitoring, security, and analytics for cloud-scale applications and infrastructure.

This set of results not only took many investors by surprise, but it will also have ramifications for other IT and data analytics companies. The most obvious here is Snowflake ( SNOW ). But the impact will be felt over the whole sector, even with indirect peers such as Cloudflare ( NET ) and MongoDB ( MDB ) being impacted.

{kind=link}

Datadog is guiding for a slowdown for the remainder of 2023. Datadog was a company that investors could count on to deliver rapidly growing revenues together with an attractive bottom line. Even though its bottom line continues to be attractive, investors were not attracted to Datadog for its profitability , which we'll soon discuss further.

Datadog was meant to be a growth stock. It was given a growth multiple on this contention. However, it turns out that Datadog's product suit was less in demand than many investors were led to believe.

Perhaps, what's even more challenging to grasp is that H1 2023 was the fastest half of the year. For me, this was the most surprising aspect.

Many investors have heard discussions throughout this earning season about how the back half of 2023 was ready for a reuptake in software demand after enterprises took a pause in their software infrastructure spend. You can read more on this from Microsoft ( MSFT ) or Amazon ( AMZN ) or Alphabet ( GOOG , GOOGL ) -- yes, I've provided analysis on all these names.

The Peter Lynch Hypothesis

I've termed the Peter Lynch hypothesis as being when a stock is changing its narrative, but the fundamentals haven't fully caught up the narrative . I've described to my followers how this can work on the long or the short side.

Allow me to explain. For Datadog, the big question is if 2023 will see Datadog exit with around 20% CAGR, what sort of growth rates can Datadog be expected to see in 2024?

Simply put, can we count on Datadog to accelerate its growth rates so that beyond H2 2023, it could re-accelerate back to an approximate 25% CAGR?

Here's the fact of the matter: growth companies don't downwards revise their growth rates in practically any condition. They can miss on the bottom line. They can become less profitable. But what they can not do is downwards revise their revenues. And yet, albeit by a small margin, that's exactly what Datadog did.

This forces us to consider the following:

SA Premium

What you see above is that as we headed into the earnings results, analysts following Datadog had their consensus estimates for the company at around mid-20s% CAGR. But it now seems that analysts were too bullish. By extension, this means that in the coming days and weeks, we'll see analysts downwards revising their financial targets.

And that's how the Peter Lynch hypothesis starts to play out. When the fundamentals are starting to change and expectations start to move towards and align with the fundamentals.

Since the start of 2023, Datadog's multiple has expanded from around 8x forward sales to 16x forward sales. A jump of 100% in multiple expansion in around half a year.

Accordingly, we can conclude that investor expectations were incredibly high. Even though Datadog was able to note that it was increasing its profitability by more than 10% to $400 million since its Q1 guidance was provided, investors were not willing to pay more than a $30 billion market cap for a $400 million adjusted operating profits. Investors were excited and hopeful to see Datadog delivering very rapid topline growth. And on this front, Datadog didn't live up to investors' expectations.

The Bottom Line

In this quarter's earnings report, I was taken by surprise as Datadog showed a slowdown in its revenue growth rates, indicating that it might no longer be a high-growth company.

While its underlying profitability is improving, the demand for Datadog's product suite seems to be weaker than I previously thought.

Now I wonder if Datadog can regain its growth momentum in 2024 after a slower H1 2023?

The fact that the company downwardly revised its revenue projections raises questions about its future performance.

As an investor, I'm cautious about Datadog, Inc.'s valuation and its ability to meet growth expectations. I'll stick to the sidelines.

For further details see:

Datadog Earnings Surprise: The Peter Lynch Hypothesis In Action