DDOG - Datadog: Enterprises Cloud Optimization Starts To Moderate Impressive AI Contribution

2023-12-08 08:29:00 ET

Summary

- Datadog's stock price has surged by 30% since the publication of the article.

- The company achieved impressive Q3 FY23 results, with a 25% increase in revenue and significant growth in non-GAAP operating profits.

- The early signs of cloud optimization stabilization and the contribution of AI providers are positive indicators for Datadog's future growth.

Since I published my introductory article in August, Datadog ( DDOG ) stock price has surged by 30%. Following their impressive Q3 FY23 results, I maintain a 'Strong Buy' rating with a fair value of $120 per share.

Quarterly Results and Outlook

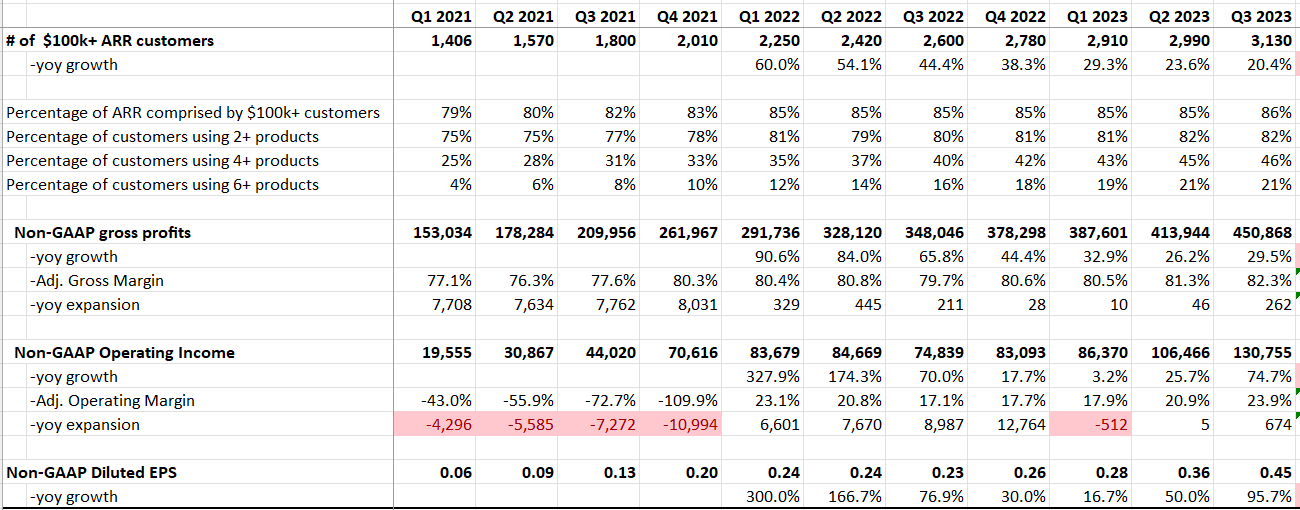

During Q3 FY23 , their revenue increased by 25% year over year, and non-GAAP operating profits grew by 74.7% year over year. More importantly, they achieved a milestone of 3,130 customers with ARR of $100,000 or more, reflecting a substantial 20% year-over-year growth.

{kind=link}

In terms of cash flow, they generated $138 million in free cash flow, representing a notable 25% free cash flow margin. This marks a significant leap from their FY22 margin level of 21.1%. For the full year, they anticipate revenue to fall between $2.103 billion and $2.107 billion, with Non-GAAP operating income projected to be in the range of $453 million to $457 million. This outlook is particularly robust, reflecting over 25% year-over-year growth in full-year revenue, a noteworthy achievement amid a challenging economic macroenvironment. In summary, my key takeaway from their earnings calls can be summarized as follows.

Enterprise Cloud Optimization Starts to Moderate

During their Q3 earnings call , the management indicated that they observed early signs of certain enterprise customers beginning to moderate their cloud optimization. These optimizations seemed to stabilize towards the end of Q2, and there are indications of improvement in Q3.

As I highlighted in my introductory article, numerous enterprises overspent on their cloud consumption during the pandemic period. Starting last year, these customers initiated efforts to optimize their cloud usage on major platforms such as Azure and AWS, posing some growth headwinds for Datadog.

I believe the early signs of cloud optimization stabilization are quite positive for Datadog. On one hand, they can potentially boost consumption-related growth in the coming quarters. On the other hand, as businesses begin migrating their workloads to cloud platforms, Datadog can attract more new customers. For example, they successfully closed a record number of new deals, each with commitments exceeding $100,000 in annual value during the quarter.

2.5% of ARR Driven by Native AI Providers

For some contexts, ARR is the annualized revenue run-rate of subscription agreements from all customers at a point in time for Datadog. During their Q3 earnings call, they disclosed that 2.5% of their ARR was attributed to AI providers.

These customers, predominantly model providers, have been associated with Datadog for over a year, and notably, they are currently experiencing faster growth compared to the rest of Datadog's customer base. While 2.5% may seem like a modest percentage, I believe it holds significant meaning for Datadog's future growth.

It is evident that AI and machine learning are experiencing rapid growth in today's landscape. Datadog's log management and infrastructure monitoring platforms encompass vast datasets that serve as mission-critical inputs for machine learning. It is logical for AI providers to leverage Datadog's technology and platforms.

I anticipate that AI customers will contribute significantly to Datadog's growth in the near future. More importantly, enterprises are likely to increase their consumption of Datadog's platforms for their proprietary machine learning and AI initiatives.

Valuation Update

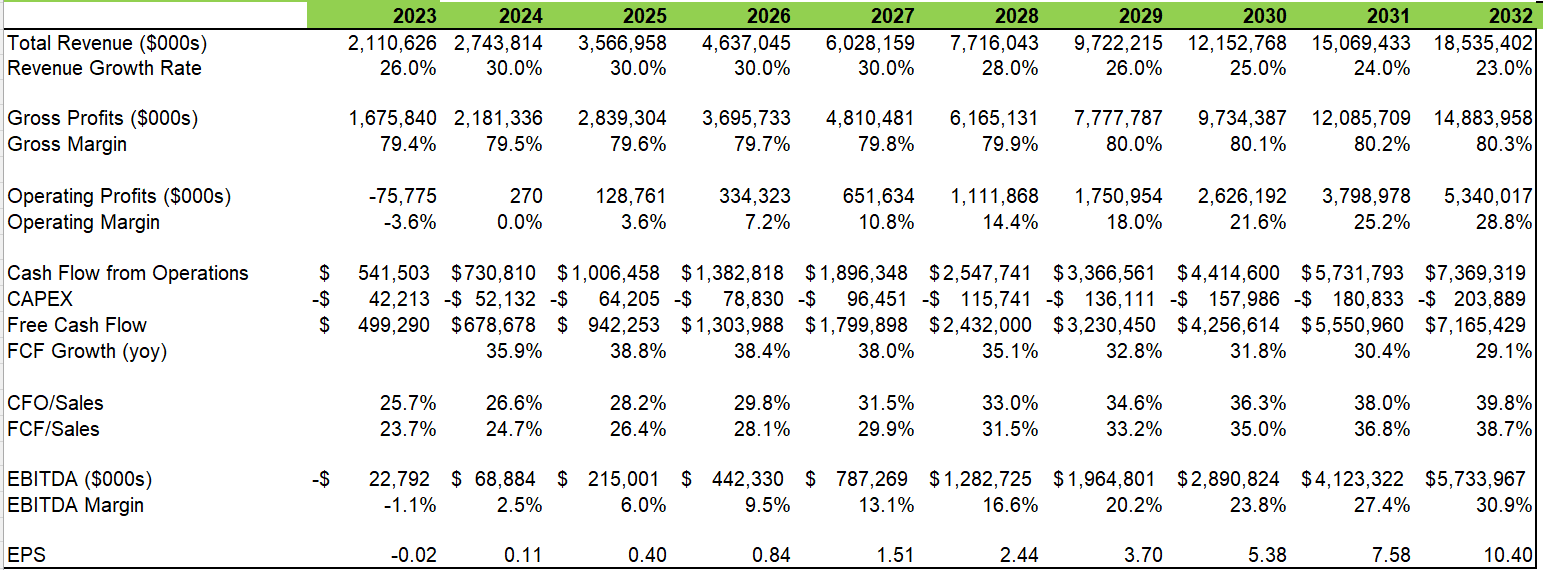

The model's assumptions for FY23 align with the company's guidance, signaling a robust growth year despite the impact of enterprise cloud optimization. I anticipate that AI providers will continue to be a significant driver of growth for Datadog. As cloud optimization trends are expected to taper off in FY24, I foresee Datadog's growth rate strengthening, reaching an impressive 30% annual growth rate from FY24.

{kind=link}

I have maintained the margin assumptions in the model, utilizing a 10% discount rate, 4% terminal growth, and a 25% tax rate. The estimated fair value remains at $120 per share.

Conclusion

Datadog had a robust quarter, firing on all growth cylinders. The long-term thesis of structural growth remains intact, and I am maintaining a 'Strong Buy' rating with a fair value of $120 per share.

For further details see:

Datadog: Enterprises Cloud Optimization Starts To Moderate, Impressive AI Contribution