DDOG - Datadog: History Tells Us To Exercise Caution

2024-01-09 08:01:02 ET

Summary

- Datadog has a compelling revenue growth story as its growth maintains pace with cloud hyper-scalers.

- Throughout history, many observability companies have failed to achieve significant scale after similar early prospects as Datadog.

- For Datadog to create significant value, it needs the market structure of observability to have changed, and for cloud spending projections to reach upper bounds.

- Datadog is a gamble on this happening, and a poor gamble at a $38B valuation, it is completely un-investable from a value perspective.

For the short history of Datadog (DDOG) as a public company, its stock has come with a big story and even bigger valuation.

Cloud computing has transformed software development over the past decade and a half. Instead of businesses investing in costly hardware, they can spin up an instance on Amazon's AWS ( AMZN ), Microsoft Azure ( MSFT ), or Google Cloud ( GOOGL ). This allows businesses to grow without investing in CapEx and further complicating their operations.

Entire startups have been built in the cloud. Cloud has greatly expanded the number of applications, which has made monitoring these applications a job for software developers rather than observability teams. This is where Datadog has pitched itself as the superior observability tool for development teams.

This is just the beginning of the story. Datadog has had significant growth, even after a rough patch for cloud spending, Datadog is still growing by 25% while posting positive free cash flow margins. History might classify the cloud hyper-scalers as some of the defining businesses of this era, much like the railroads in the late nineteenth century.

Datadog's thesis is simple, as more applications are built, more applications need monitoring. Cloud native Airbnb ( ABNB ) generated $63.2B of gross booking volume in 2022, which averaged out equates to about $48,100 of bookings per minute. Any significant downtime can cost large enterprises millions of dollars in revenue.

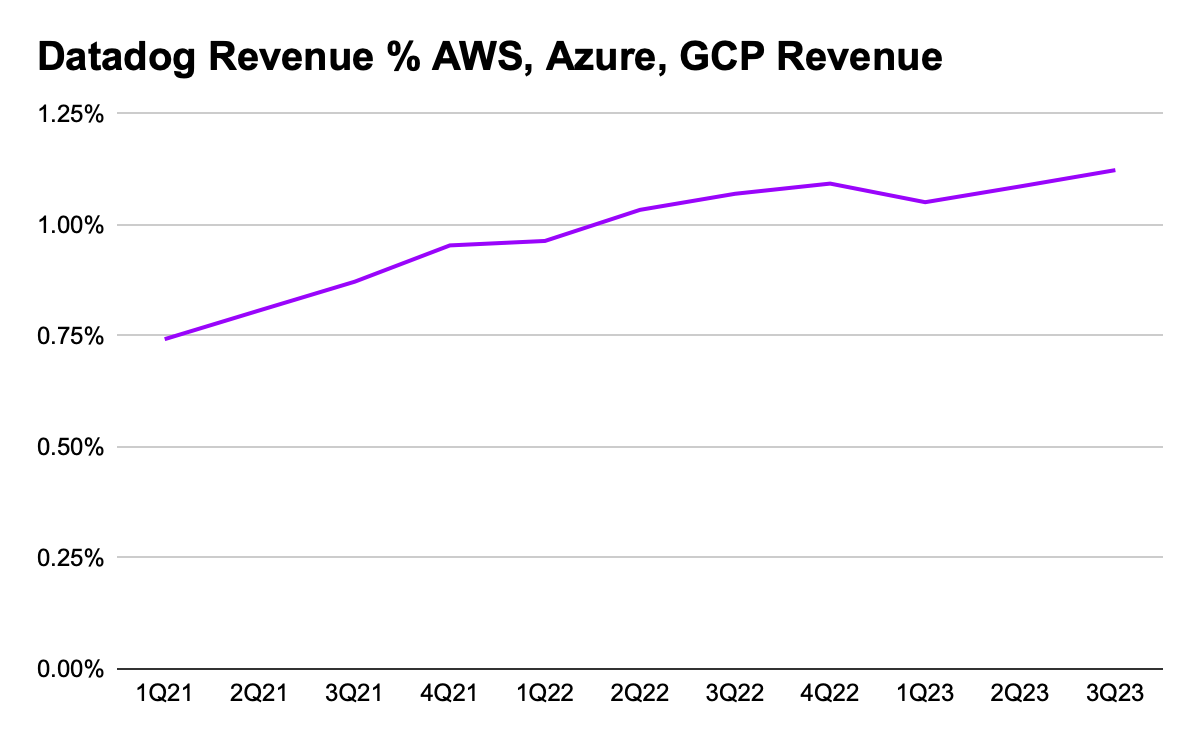

Because cloud computing is providing software and hardware, they are able to charge based on consumption, unlike traditional SaaS providers. This has created even more excitement around these businesses as revenue growth appears boundlessly tied to growth in new applications. Likewise, observability companies have matched this pricing strategy, Datadog had been gaining share on the hyper-scalers, but that has stalled over the past several quarters. Datadog's revenue has sat at just a tad over 1% of hyper-scaler revenue:

{kind=link}

With just knowing Datadog's revenue trajectory, this would appear like a slam dunk, can't miss investment. But investors should always be extremely cautious when dealing with emerging high-growth businesses. Datadog is currently valued at $38B, the history of observability companies that showed similar early promise as Datadog is robust. None were able to break through to the scale necessary that could give investors any confidence Datadog could too.

Competitive Landscape:

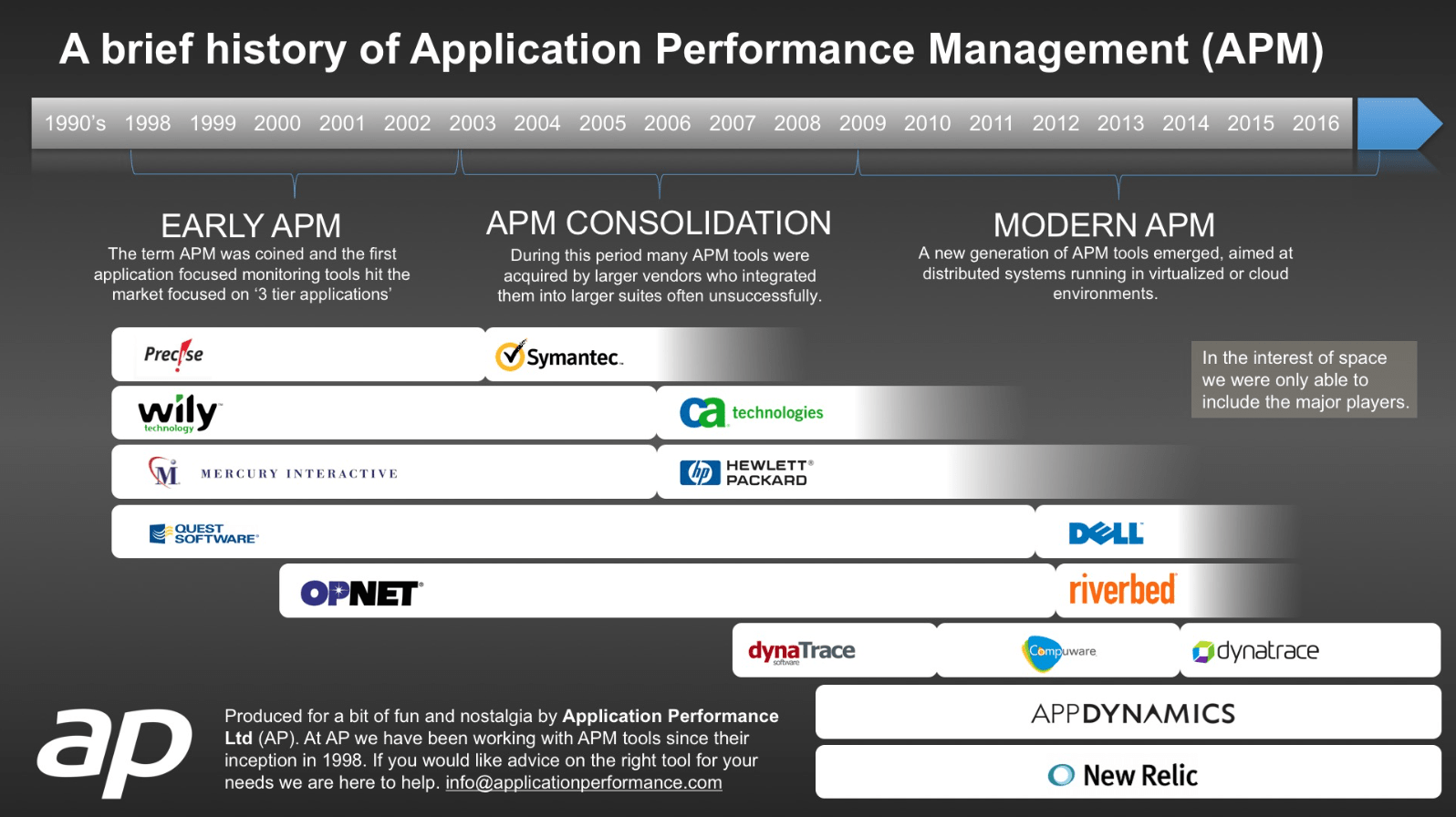

The observability market is littered with the hopes and dreams of numerous companies. Below is a historical timeline of some of Datadog's predecessors:

{kind=link}

This timeline doesn't included Splunk ( SPLK ), which was recently acquired by Cisco ( CSCO ) for $28B. Cisco reportedly tried to acquire Datadog for $7B just before its IPO. New Relic ( NEWR ) was also acquired by private equity for $6.5B.

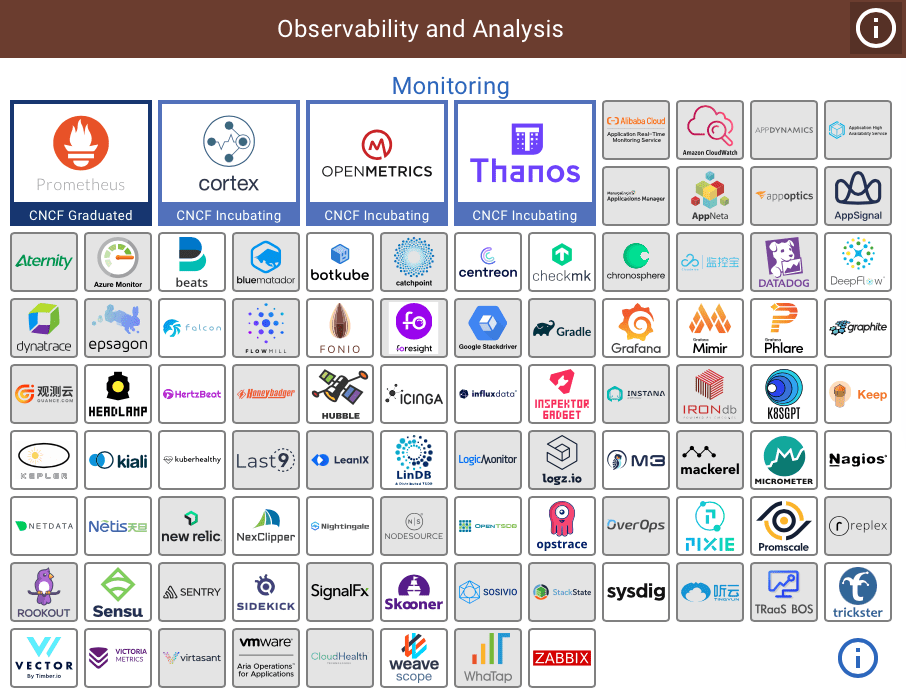

Below is a chart of the numerous existing and emerging Datadog competitors :

{kind=link}

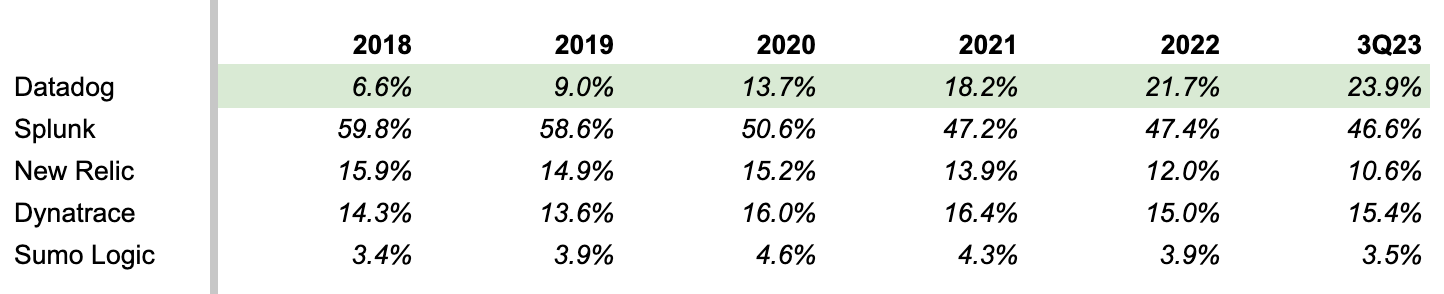

Despite this, Datadog is clearly leading the pack in observability. Its growth trajectory has vastly outpaced its publicly traded peers:

{kind=link}

Datadog's advantage can primarily be attributed to its go-to-market motion. Datadog's sales team targets cloud developers, getting in the door by selling cloud infrastructure monitoring and expanding from there. Competitors have largely pitched their products by focusing on critical applications in the enterprise that need monitoring, a more complicated sales process.

It's also possible cloud has fundamentally changed the observability market. Splunk created a product called Storm , which was built for developers, much like Datadog. It abandoned the service because its customers at the time preferred one-on-one hosted services. New Relic was mentioning Datadog on earnings calls before it went public, believing it would coexist with Datadog, but recognizing its tools were more modern.

What happens moving forward remains to be seen. Investors must balance the two entirely plausible, but opposite ends of the spectrum for possible outcomes. On one hand, the market structure may have changed, and Datadog is well positioned to continue to win share and consolidate market share. On the other hand, the observability space has historically been extremely competitive, and tools have not remained relevant for long periods of time.

Valuation:

Given these parameters, investors can derive a framework to think about the stock. In the near term, growth will likely be tied to hyper-scaler spending. The first risk is that forecasting hyper-scaler growth is difficult. The current run-rate is $184B for the 3 major players. Some scenarios believe $2T is a reasonable base case scenario . This seems fairly aggressive, a 20x or so from here.

Along with the systemic risk of how large the cloud industry will be, Datadog faces a competitive threat that is significant. While there doesn't appear to be any obvious challenger today, throughout history competition has always seemed to emerge when a company has taken a significant lead.

In the first 9 months of 2023, Datadog has generated $70M of free cash flow in excess of stock-based compensation. The stock is simply un-investable from a value investor perspective. Datadog generates insignificant earnings and has very real terminal value concerns given its industry.

Datadog is purely a gamble that the industry structure has changed, giving Datadog a significant lead over competitors, and also that cloud spending reaches the upper bounds of projections. Based on the past, the most likely outcome is that Datadog's growth eventually fizzles out and the business is acquired. It's very difficult to see Datadog earning enough for investors to make any money at a $38B valuation. As always, the market is a weighing machine in the short term. Datadog has a great story, and when interest rates are low, investors seek high risk business models in search of returns.

For further details see:

Datadog: History Tells Us To Exercise Caution