DDOG - Datadog's Surprising Turnaround: A Profitability Revelation (Upgrade)

2023-12-11 09:10:28 ET

Summary

- Datadog surprises with substantial profitability improvements in Q3 2023.

- Concerns arise as revenue growth rates decelerate, with expectations hovering around the mid-20s% for Q4.

- Revised stock rating to a slightly bullish stance reflects the company's impressive progress in profitability.

Investment Thesis

Datadog (DDOG) is a monitoring and analytics platform that provides organizations with real-time insights into the performance of their applications, infrastructure, and logs. It enables DevOps and IT teams to monitor, troubleshoot, and optimize the health and efficiency of their technology stack.

As you'll soon read, I made a bad call on this stock by being neutral on this name as it headed into its Q3 2023 results.

While I categorically maintain that Datadog still has a lot of work to prove that it can sustain its 60x forward operating profit valuation, I admit that the business has made a lot of progress in its underlying profitability.

Therefore, I'm inclined to revise this stock to an ever-so-slightly bullish rating, as I stand by my assertion that this stock is pricing in a lot of upside and will need to prove itself.

Rapid Recap,

Back in October, in my previous neutral analysis , I said,

When growth companies start to slow down, there's a period of shareholder rotation. Where the growth investors sell and move on to the next fastest-growing business, but where value investors are still not interested as they only focus on the company's bottom line, and they steadfastly refuse to pay up for growth. No matter how alluring the story.

And that's where Datadog finds itself, in no man's land. Here I'll describe some positive and negative aspects to help readers think through this investment.

With the benefit of hindsight, I made a bad call on this stock. As you can see below, the stock has sizzled since my last analysis.

Author's work on DDOG

At the time, I didn't expect Datadog to make such strong progress on its underlying profitability. Therefore, I now upgrade this stock to a very tepid buy rating.

Datadog's Near-Term Prospects

Datadog's near-term prospects are marked by its sustained commitment to innovation and strategic market positioning. The company's Q3 performance reflects not only robust financial growth, but also a testament to its ability to adapt to the evolving dynamics of the cloud computing landscape.

One key indicator of Datadog's near-term strength lies in its successful execution of a multi-product platform strategy. The increasing adoption rates illustrate that 82% of customers are using two or more products, showcasing the depth of Datadog's offerings. This broad platform adoption indicates a growing recognition and trust among customers in Datadog's ability to provide comprehensive solutions for their cloud-based infrastructure and observability needs.

Furthermore, Datadog's focus on customer-centric innovation is evident in its expansion into the DevSecOps space. The introduction of packages like Infrastructure DevSecOps and APM DevSecOps simplifies the integration of monitoring and security across the entire cloud environment and application landscape. This not only aligns with industry trends emphasizing the convergence of development, operations, and security teams but also positions Datadog as a holistic solution provider in the fast-evolving DevSecOps landscape.

{kind=link}

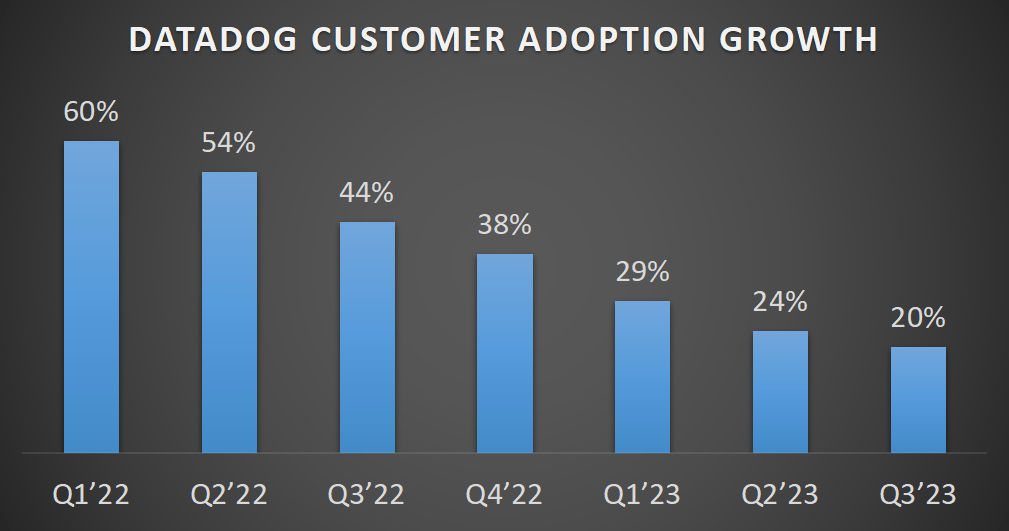

Datadog clearly has a very compelling narrative. But now, I ask that you look at the graphic above and see if you see a general trend. Followers of my work will know that I put a lot of emphasis on a solid customer adoption curve.

And for businesses with a declining customer adoption curve, I am very strict when it comes to its valuation, as I know that it might all look attractive right now, but this time next year its customer adoption rate may be around the high teens, at which point the bears will be out and all over this name, once again.

Revenue Growth Rates Should Stabilize

{kind=link}

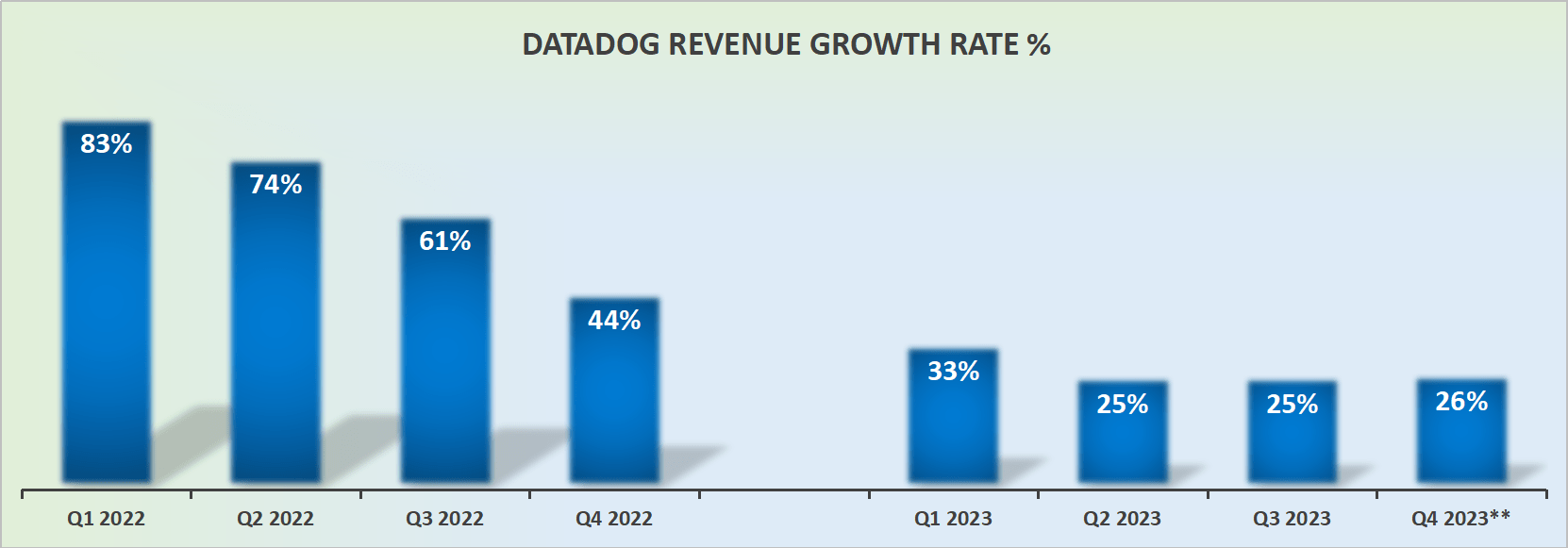

Datadog is no longer delivering those juicy growth rates of last year. In fact, for its guidance for Q4, I've largely assumed that management is lowballing its estimates and I've added 5% to the high end of its guidance.

And even in that case, Datadog is going to be growing at 26% y/y. Furthermore, keep in mind that from Q3 into Q4 of last year, Datadog's growth rates meaningfully decelerated.

Therefore, the comparables with the prior year substantially eased up and yet, for Q4 of this year its growth rates are still only expected to come in around the mid-20s%.

One way or another, I contend that the days when Datadog could be counted on for hyper-growth rates are now in the rearview mirror.

And now, let's discuss its growth in profitability, the crown jewel of the bull case that I failed to fully appreciate.

DDOG Stock Valuation -- 60x Forward non-GAAP Operating Profits

Consider this, 2022 non-GAAP operating income reached $326 million. And in 2023 is expected to grow by 43% y/y to around $465 million. That's an impressive growth rate, undoubtedly.

But now keep this in mind, Datadog spent the majority of the past 12 months working very hard to improve its profitability. After all, prior to these Q3 results, the stock had gone nowhere. In fact, for the most part, it had generally traded down.

My point? Datadog was determined to improve its cost structure so that the low-hanging fruit that could be taken out of the cost structure was addressed first.

Therefore, as a corollary to this thought process, I do not believe investors should expect 2024 to see the same level of bottom-line appreciation to its underlying profitability.

Hence, I've assumed a fast growth in profitability in 2024, but more measured than in 2023.

This means that in 2024 its non-GAAP operating profits might increase to around $630 million, for a 35% y/y increase. A figure that appears to be achievable.

This leaves Datadog priced at 60x forward non-GAAP operating profits. And that's a rich-priced tag for mid-20s% topline growth.

The Bottom Line

In conclusion, the journey of Datadog has taken an unexpected turn, leaving me astounded by the substantial improvements in its underlying profitability. While my initial assessment maintained a cautious stance, the company's Q3 2023 results unveiled a remarkable transformation.

The strategic focus on a multi-product platform, coupled with innovations in the DevSecOps space, showcases Datadog's adaptability and comprehensive solution offerings.

Despite concerns about decelerating revenue growth rates, the astonishing surge in non-GAAP operating income, reaching $465 million in 2023, marks a significant achievement. The diligent efforts to enhance cost structures and achieve profitability growth signal a new chapter for Datadog.

Although the valuation at 60x forward non-GAAP operating profits appears steep, the demonstrated progress commands attention, prompting a revised, albeit cautious, shift to a slightly bullish rating. Datadog's narrative unfolds with unexpected vigor, leaving observers intrigued by the potential yet to be fully realized.

For further details see:

Datadog's Surprising Turnaround: A Profitability Revelation (Upgrade)