DDOG - Datadog: Soaring Like A Meme Stock But The Juice Will Run Out

2024-01-10 10:29:02 ET

Summary

- Datadog's stock has surged 50% in the last two months alone, perhaps due to the generative AI potential.

- The company maintains a net cash balance sheet and generated a GAAP profit in the latest quarter.

- I explain why growth rates are unlikely to accelerate meaningfully in the near term based on analysis of cRPO.

- Consensus estimates for the company's growth rates look aggressive, and its valuation is rich against those expectations.

It can be uncomfortable to watch high-flying growth stocks continue to soar and soar, but valuation will always matter at some point. Case in point: Datadog ( DDOG ) is a name which feels like it should get a generative AI boost even if growth rates continue to decelerate at an alarming pace. The stock’s upward surge over the last two months alone may be indicating that Wall Street expects an inflection in revenue growth at some point, with investors perhaps hoping for an aggressive “Nvidia moment” in capitulation. I argue to the contrary - consensus estimates look aggressive, and DDOG’s valuation looks rich against those aggressive expectations. Wall Street appears to be making similar mistakes as they did heading into the 2022 tech stock crash not too long ago. While the quality is undeniably high here, investors must not ignore the importance of minding valuation. I reiterate my neutral rating for the stock.

DDOG Stock Price

DDOG is a profitable tech stock, but that hasn’t stopped it from showing strong gains amidst a tech melt-up. The stock is up 50% in the last two months alone.

I last covered DDOG in September where I recommended avoiding the stock due to the overvaluation. The stock has jumped another 25% since then, but I caution against extrapolating the strong stock returns with continued future outperformance. While it may very well be possible that DDOG sees an acceleration in top-line growth at some point, I'm of the view that the optimism is more or less priced in at this point.

DDOG Stock Key Metrics

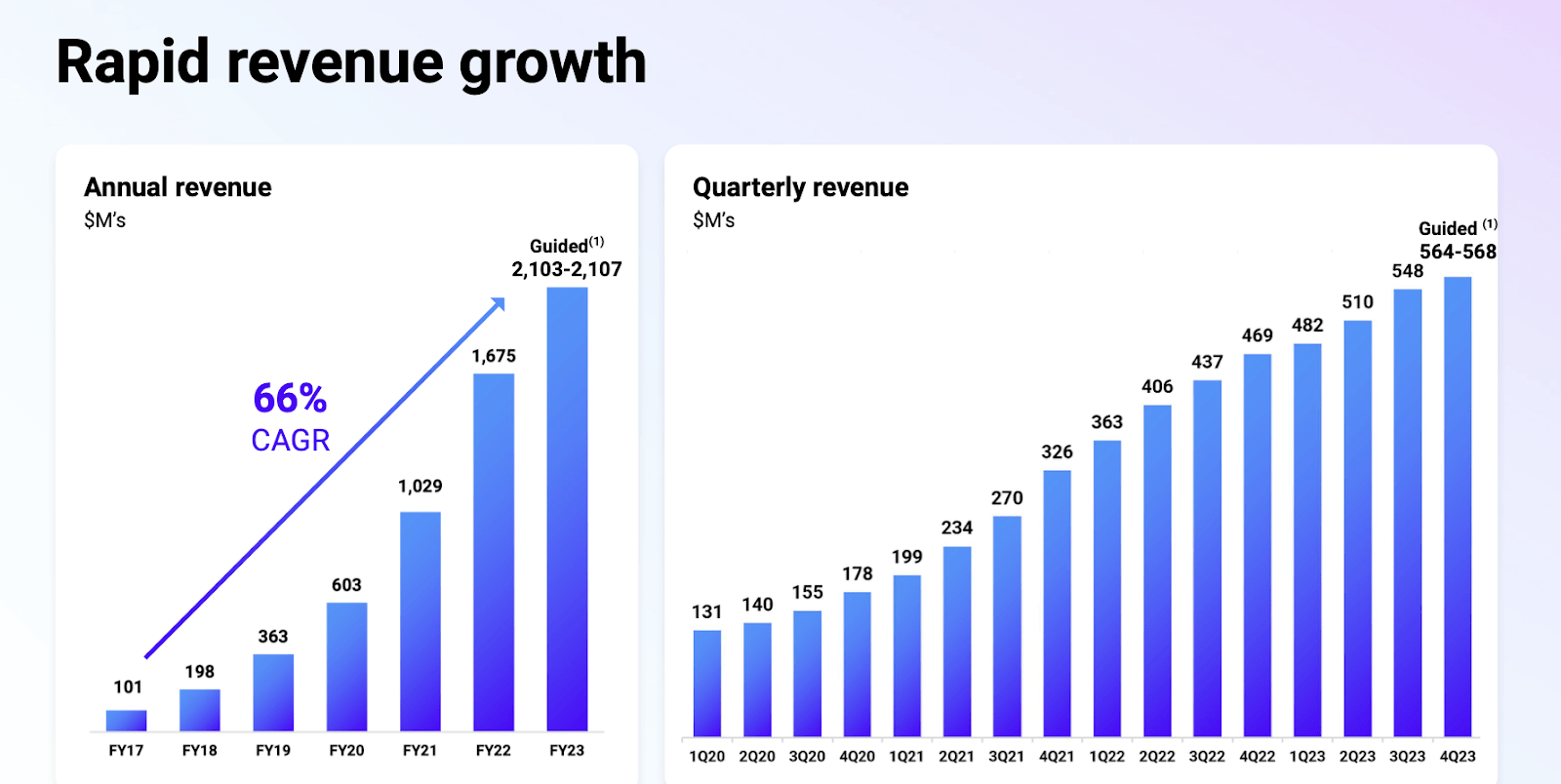

In its most recent quarter, DDOG delivered 25.4% YoY revenue growth to $548 million, surpassing guidance of $525 million.

{kind=link}

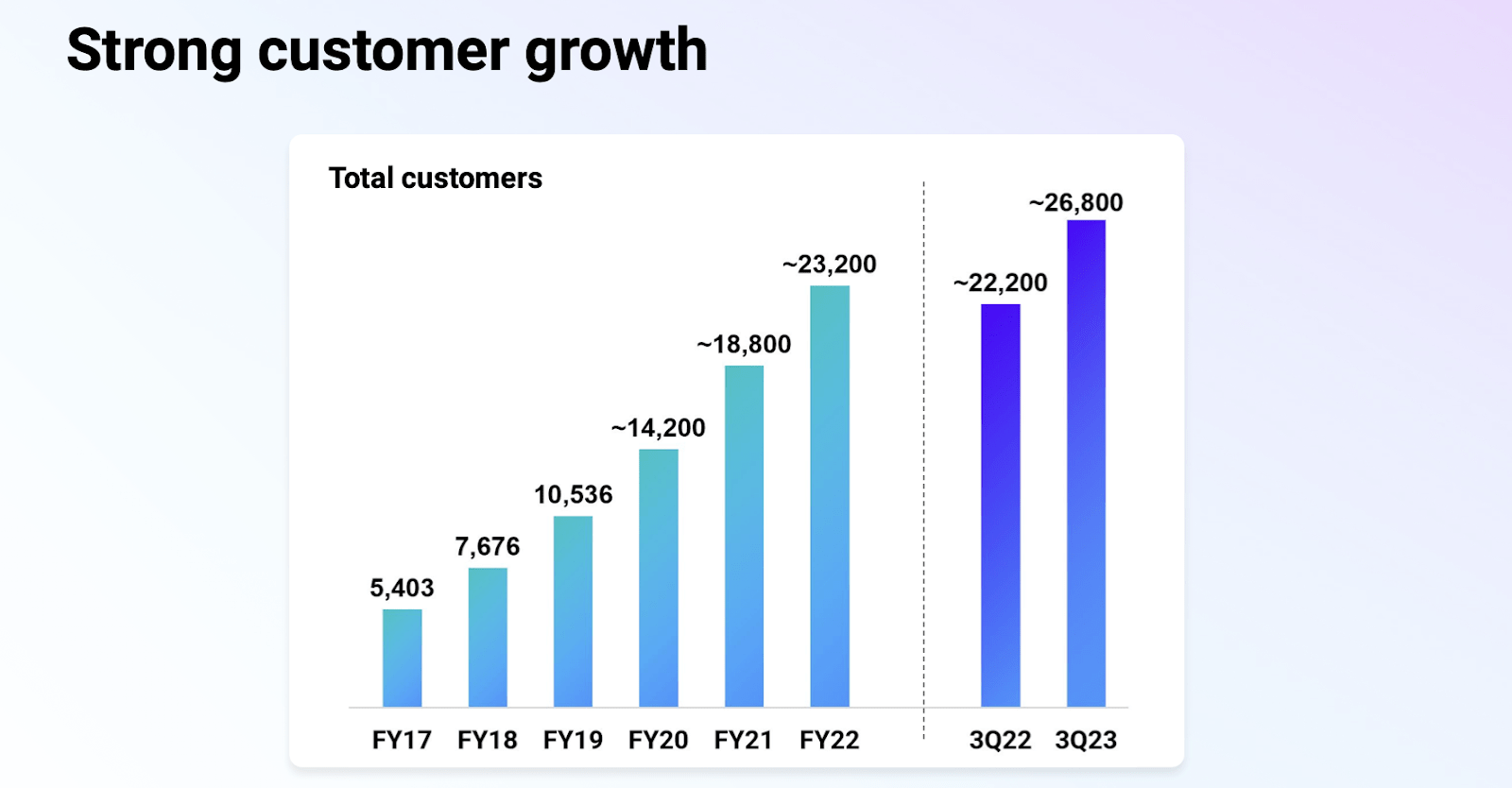

DDOG entered 2023 with a deeper product portfolio than many tech peers, which has enabled it to sustain stronger growth rates than smaller peers (albeit inclusive of meaningful deceleration in growth). DDOG was able to grow its customer count at an impressive 2.7% QoQ clip (though this should accelerate as the macro environment improves).

{kind=link}

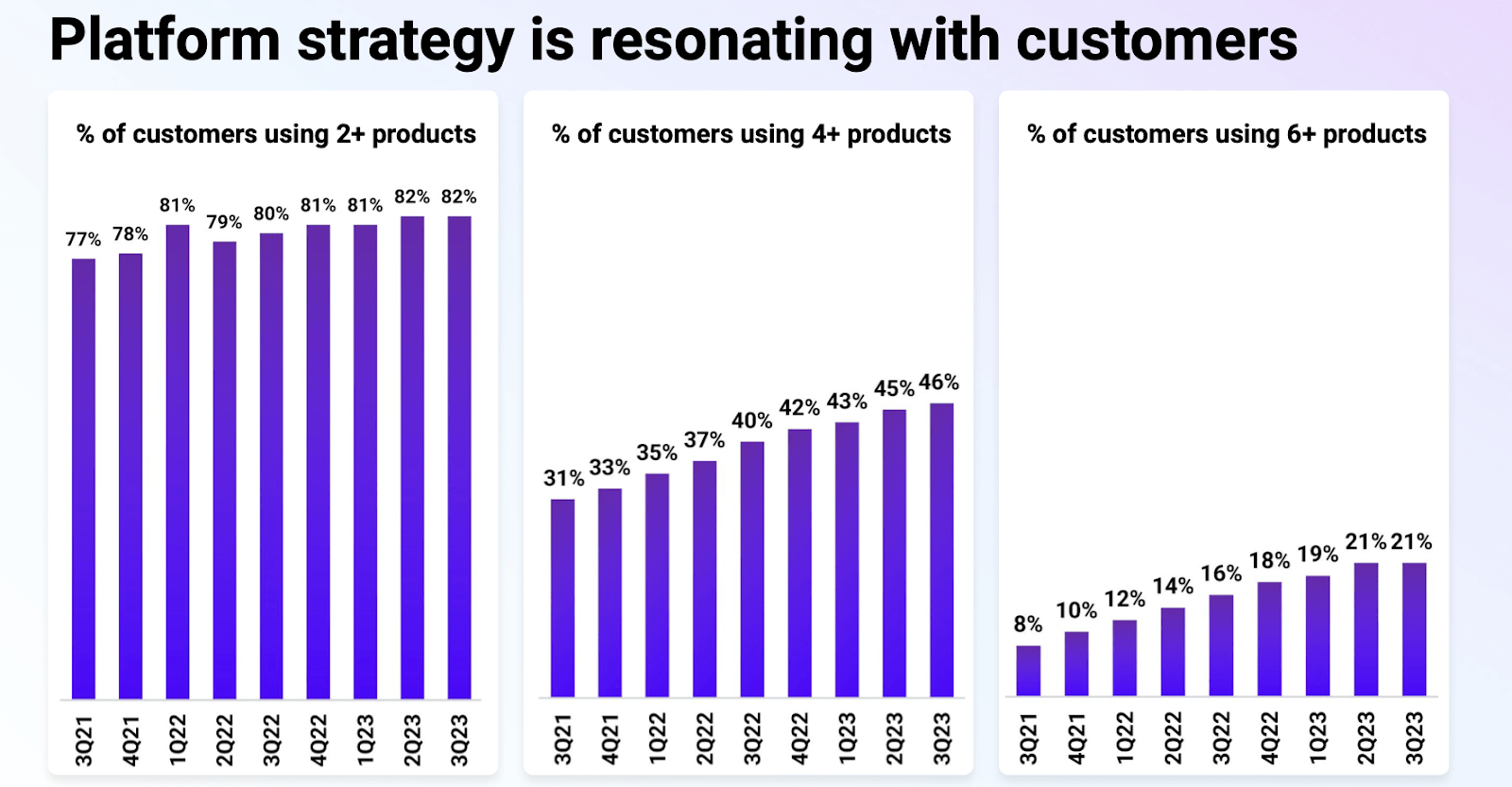

DDOG saw its dollar-based net retention rate dip to “slightly below 120%,” which is still an impressive rate that has undoubtedly contributed to the top-line growth. DDOG has a strong track record of cross-selling new products to existing customers.

{kind=link}

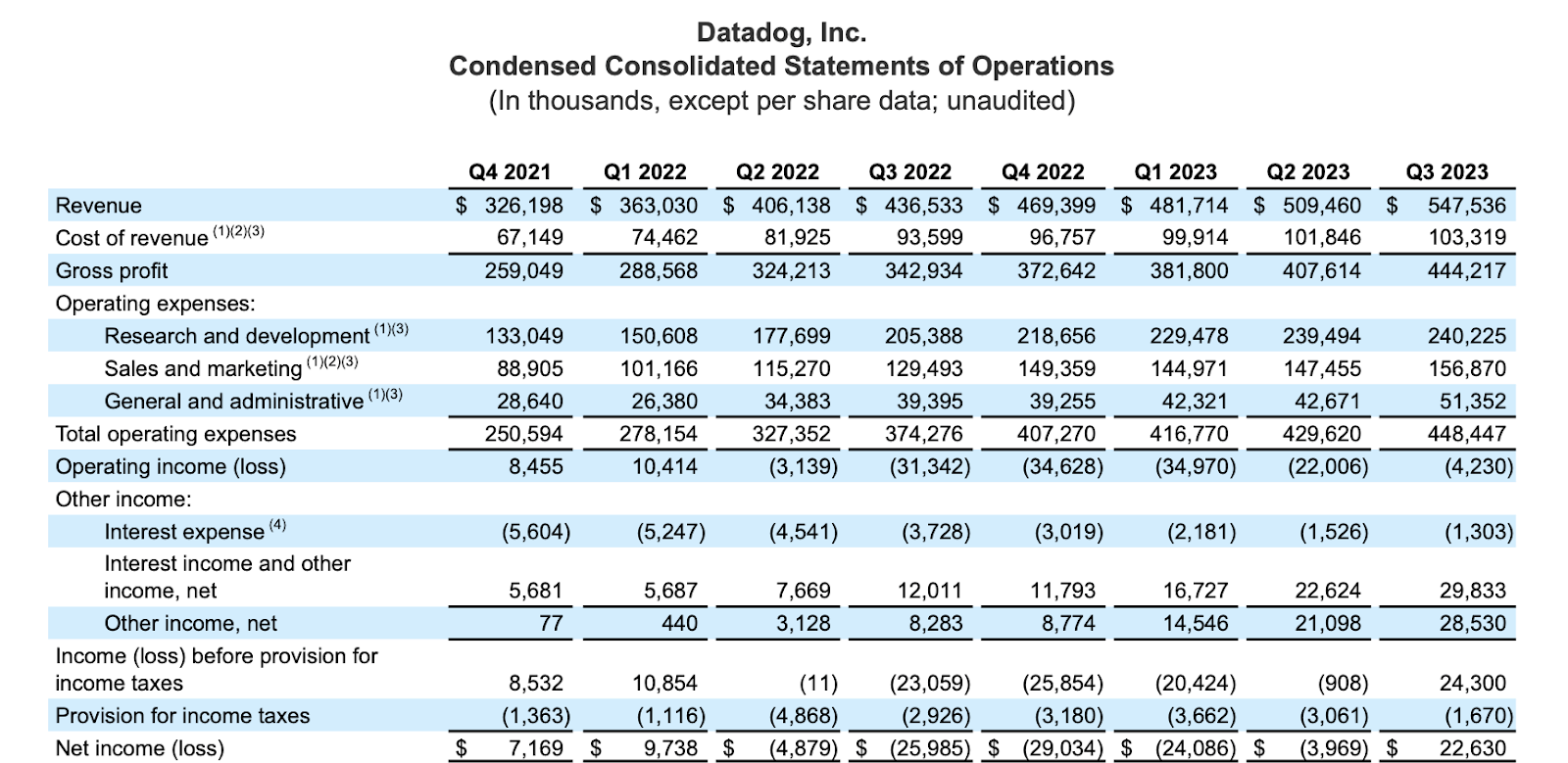

DDOG generated $130.8 million in non-GAAP operating income, surpassing guidance of $102 million. DDOG was able to even post positive GAAP net income for the first time since 2022. The company was actually generating positive GAAP operating income heading into early 2022 before it decided to invest aggressively in headcount. The company generated an operating loss in the latest quarter but the interest income earned from its cash balance helped swing the bottom-line positive.

{kind=link}

DDOG ended the quarter with $2.3 billion of cash vs. $741 million of convertible notes. Together with the GAAP profitability, this represents a bulletproof balance sheet position.

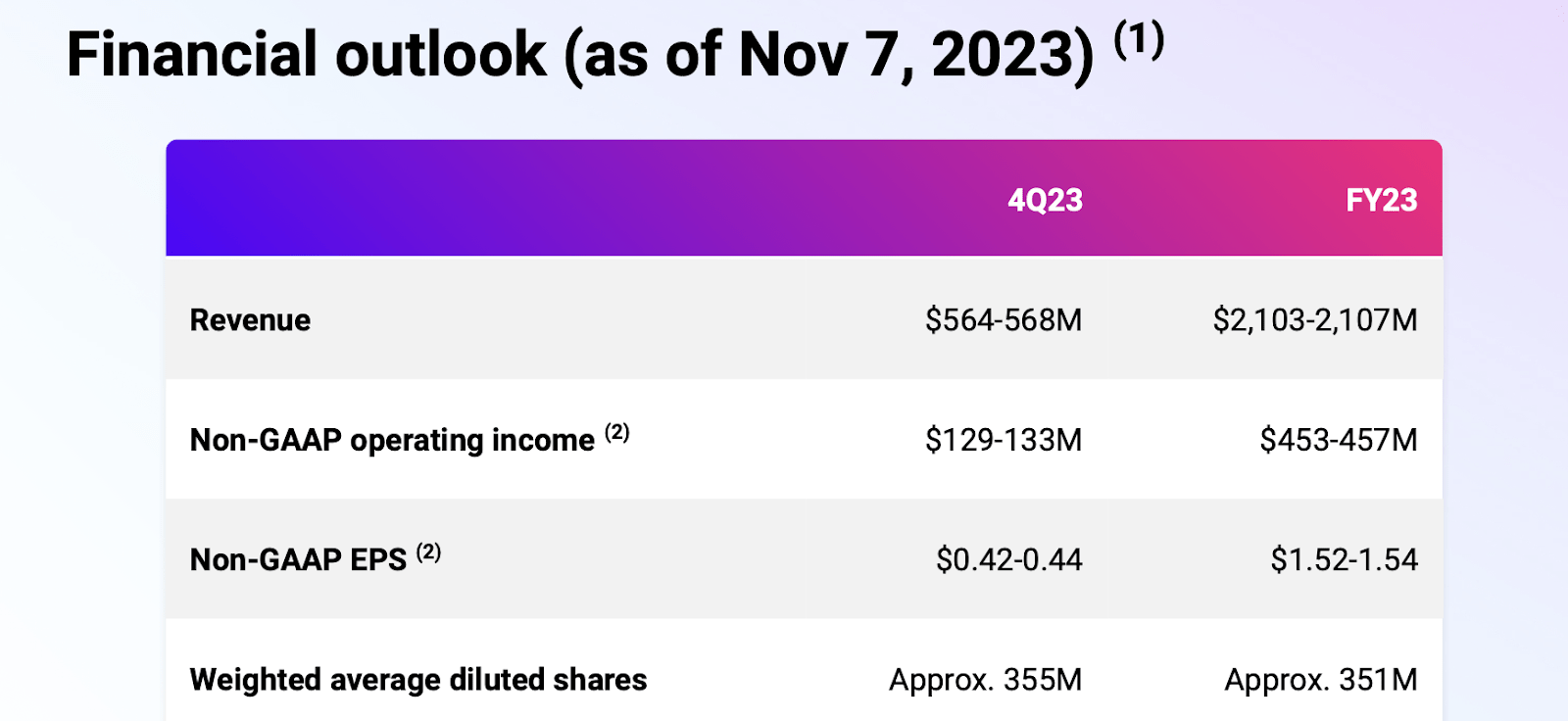

Looking ahead, management has guided for the fourth quarter to see revenue growth further decelerate to 21% at the high end. Management has typically beat guidance, but it isn’t clear if the company can sustain the 25% growth rate just posted in this past quarter.

{kind=link}

On the conference call , management noted that “cloud optimization activity from some of our customers may be moderating.” That may help to explain the strong showing on remaining performance obligations, which grew 54% YoY with cRPOs growing 30% YoY. RPOs can be a leading indicator for future revenue growth - between the cRPO 30% growth rate and the rising stock price, it appears all but certain that revenue growth should accelerate at some point. I found it unusual that management noted that customers are still seeking to sign multi-year deals, leading to an increase in the weighted average booking duration. This is in contrast with most tech peers which have seen customers seek lower contract sizes due to the higher cost of capital. Investors who may be hoping for further improvements in GAAP profitability may be disappointed as management stated that they have “no shortage of investments to make and are confident in our ability to execute to strong ROI on those investments,” leading them to refrain from providing 2024 margin guidance. That verbiage appears to indicate that DDOG may seek to reinvest more growth dollars back into the business, not too dissimilar with what it did in early 2022 as noted earlier.

Is DDOG Stock A Buy, Sell, or Hold?

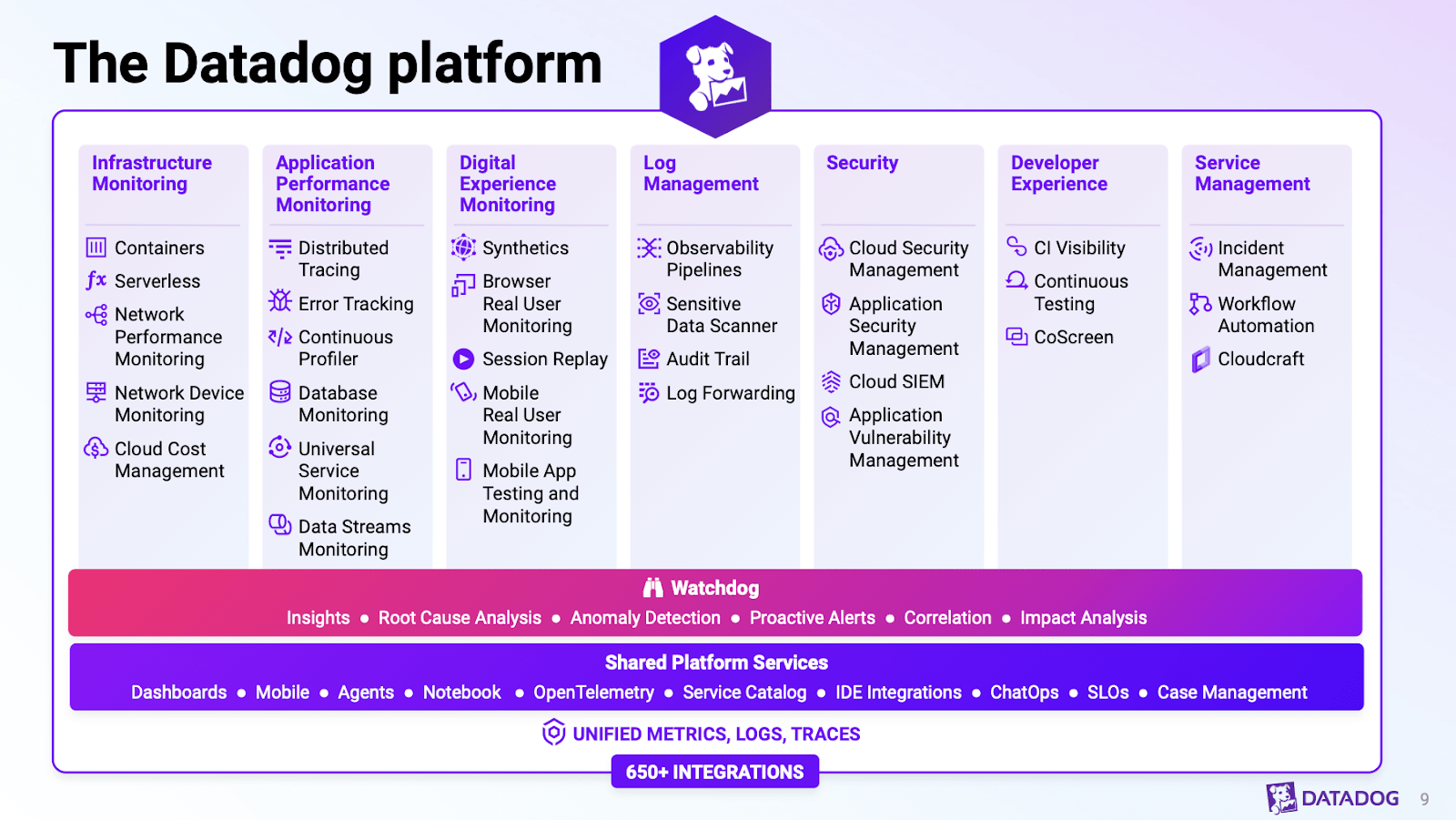

DDOG is a leading observability company which helps customers to monitor their data.

{kind=link}

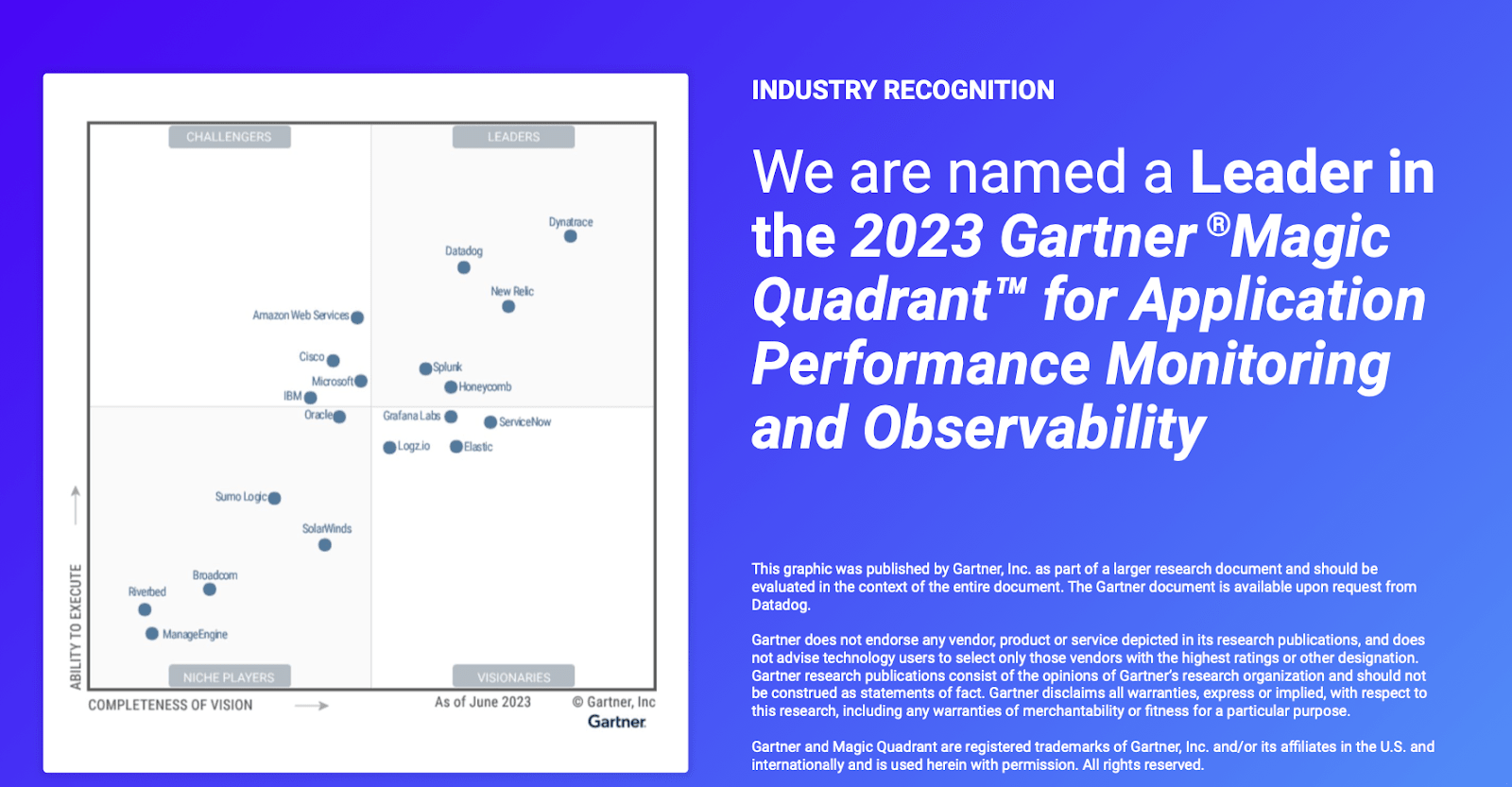

DDOG competes in a highly-competitive market against well-known names like Dynatrace ( DT ) and ServiceNow ( NOW ).

{kind=link}

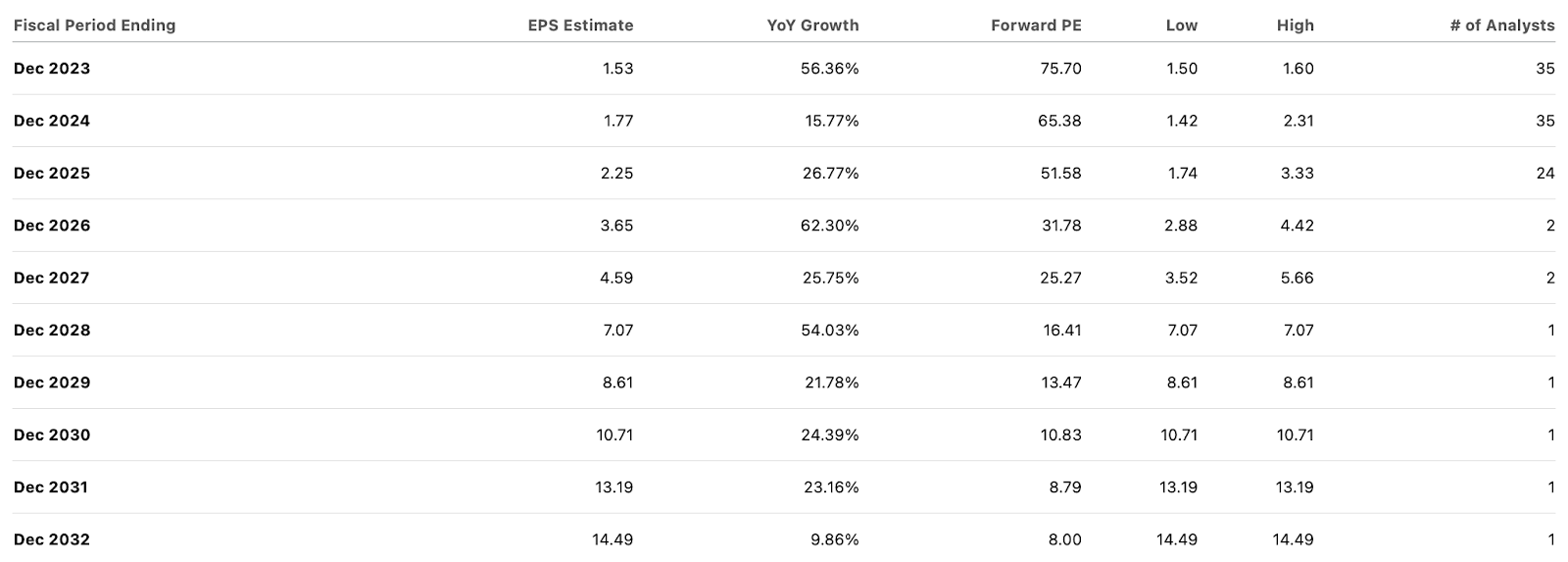

The stock recently traded hands at a lofty valuation of 76x earnings, but earnings are expected to grow rapidly due to operating leverage.

{kind=link}

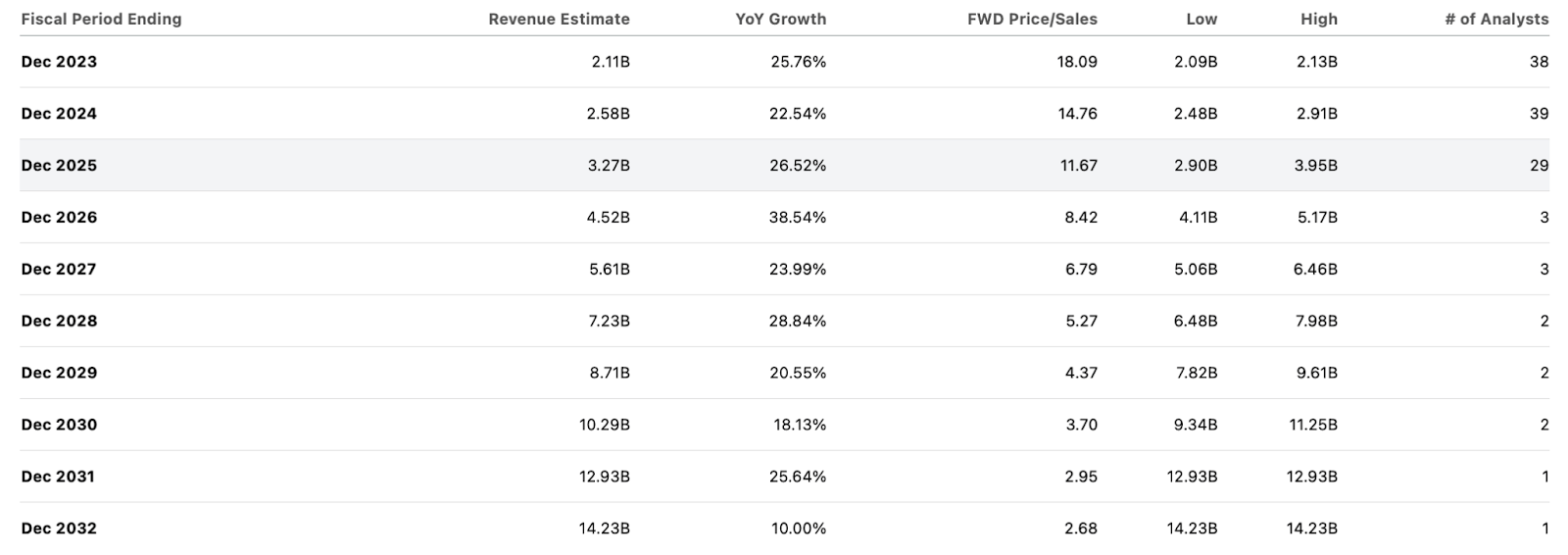

Consensus estimates call for an eventual return to 39% top-line growth, with the company expected to sustain 20-plus growth rates for many years.

{kind=link}

I am of the view that consensus estimates look quite aggressive - the company was growing at a 66% rate in 2020, followed by 71% and 63% growth rates in 2021 and 2022. While it may seem reasonable to assume revenue growth to accelerate from the 25% current level to somewhere closer to the 63% rate shown in 2022, I find it more reasonable to assume that the company saw an aggressive pull-forward in growth rates that is unlikely to repeat again. It's worth noting that the closest competitor DT is expected to post materially slower growth rates in spite of a lower revenue base.

{kind=link}

Yes, it's quite possible if not likely that DDOG can see an acceleration in top-line growth due to both an improving macro environment as well as increased interest in generative AI, which may help to increase demand for data observability products. However, I find the consensus estimate for 38.5% growth to be full, if not outright aggressive. For starters, the 30% cRPO growth posted in the quarter implies some acceleration, but there isn't clear reasons why one should expect it to lead to 38.5% growth next year. DDOG generated "high 30's" cRPO growth in the fourth quarter of 2022 , ahead of the 25.8% growth projected this year. DDOG had generated 80% cRPO growth in the fourth quarter of 2021 ahead of the 63% growth shown in 2022. DDOG may need to show cRPO growth in excess of 38.5% before investors should begin expecting an acceleration to that level.

Based on consensus estimates, DDOG is trading at around 3x 2031 sales. That would be after eight years of roughly 25% annual top-line growth which in itself looks hard to believe, given that deceleration is typically a mathematical reality. Yet even based on that estimate, DDOG does not look obviously cheap. If we assume 15% revenue growth exiting 2031 (higher than the 10% consensus estimate), 40% long term net margins, and a 1.5x price to earnings growth ratio (PEG ratio), then DDOG might trade at 9x sales by then, implying 14.7% annual upside potential over the next eight years. Those kinds of returns may be more than enough to outperform the broader market, but I find the assumptions too aggressive. It's important to note that unlike NVDA, which inherently has a greater cyclical component and has seen revenue growth surge due to many customers having to re-design data centers with their technology , DDOG is a software company which does not typically lend itself to such volatility in growth rates. As stated multiple times, I view a surge to 38.5% growth to be too optimistic but directionally is the ballpark level of acceleration in growth that investors should be expecting (as opposed to for example 60% growth). Another issue is that I expect DDOG to see growth rates decelerate more meaningfully than consensus, meaning that forward returns might be more in the 10% to 12% level over the next many years, at best. I'm wary of investing in stocks that trade at rich valuations based on high expectations, given that a shift in sentiment can lead to disastrous results under such scenarios. I reiterate my neutral rating on the stock as investors should look harder for bargains in the tech sector.

For further details see:

Datadog: Soaring Like A Meme Stock, But The Juice Will Run Out