PLAY - Dave & Buster's: An Intriguing Turnaround Opportunity

2023-12-02 06:36:34 ET

Summary

- Dave & Buster's is a chain of entertainment and dining venues that combines a restaurant and sports bar with an arcade.

- The company acquired its competitor 'Main Event' and decided to maintain its management to begin a strategic review.

- This strategic review aims to increase growth and improve operational efficiency through well-marked key points that seem highly achievable.

- Although the business was already good in itself, this strategic change could give 'boost' to the company's performance, which together with the current valuation makes it a compelling turnaround.

Investment Thesis

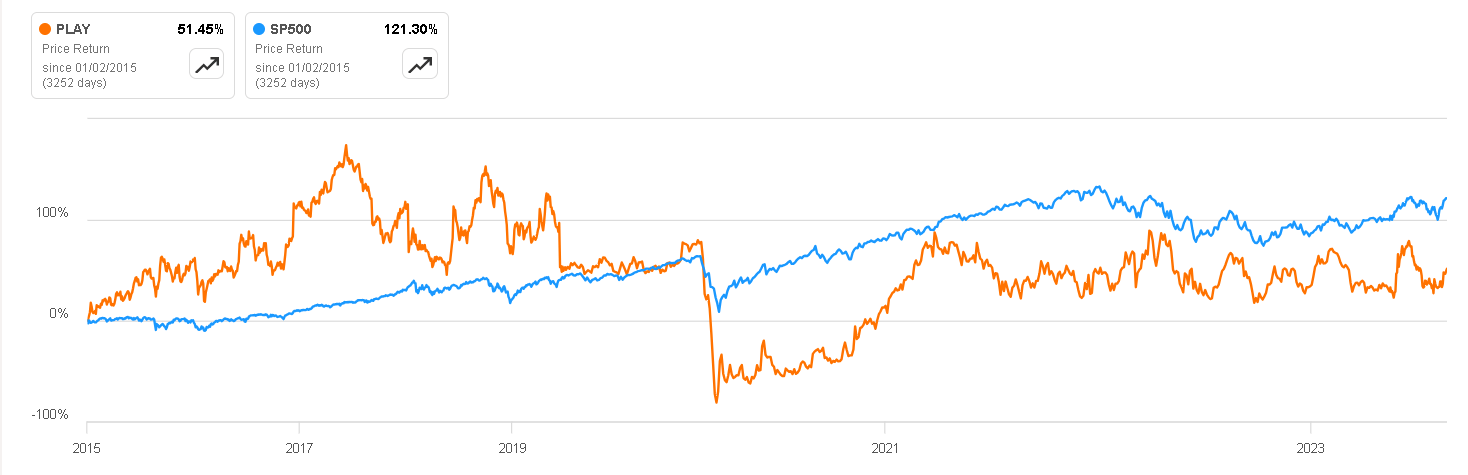

Dave & Buster's ( PLAY ) is a company that, in the past, consistently outperformed the index, demonstrating year-over-year profit growth. Contrary to initial perceptions, its business model proves to be more stable and resilient than it might appear. However, the onset of Covid-19 caused a temporary setback, and since then, significant developments have unfolded. These include a substantial acquisition, the involvement of an activist investor, a change in management, and other noteworthy events, collectively shaping the company into what I consider a turnaround situation .

In this article, I will delve into the details of the aforementioned changes and events. Additionally, I will explore what one might anticipate from the business in a hypothetical crisis and conduct a valuation to justify why I believe the company is a ' strong buy ' and could offer attractive returns in both the short and long term.

{kind=link}

Business Overview

Dave & Buster's is a chain of entertainment and dining venues that combines a restaurant and sports bar with an arcade. The establishments typically feature a full-service restaurant offering a menu of American cuisine, as well as a wide variety of arcade games and attractions. Customers can play games and earn tickets that can be redeemed for prizes.

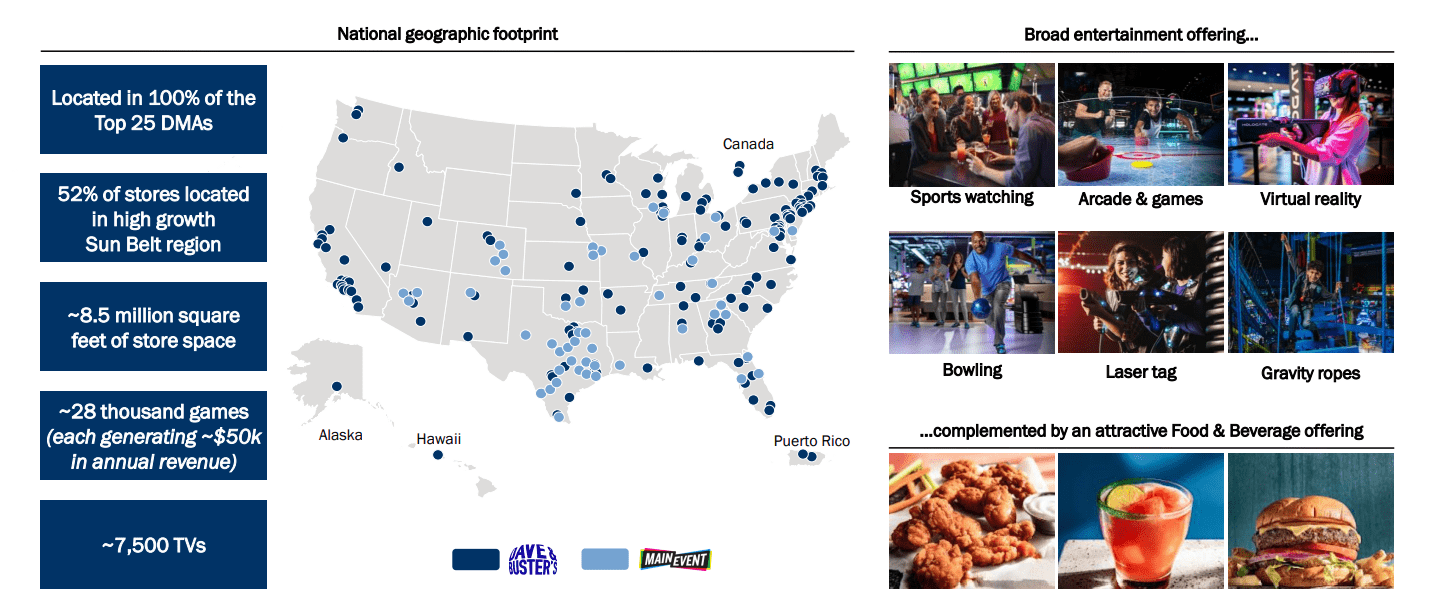

The concept is popular for its combination of food, drinks, and interactive entertainment, making it a destination for individuals and groups looking for a fun and social experience. Currently the company has more than 200 locations throughout the United States and I believe that there are numerous states in the country where it could continue its geographic expansion .

Dave & Buster's Investor Presentation

{kind=link}

Despite initial impressions, the company's revenue appears to be considerably more stable than one might expect from a purely entertainment-oriented business. This stability stems from the discretionary nature of customer spending at Dave & Buster's. When compared to other attractions like Six Flags, Disney parks, or Sea World, the expenditure per person at Dave & Buster's is significantly lower.

In the most recent quarterly report, Six Flags reported a total per capita spending of $60 USD for the first nine months, Sea World reported $80 USD spent per person, and Disney or Universal Studios costs could be even higher. In contrast, at Dave & Buster's, the average cost for a meal usually hovers around $15 USD . Additionally, patrons often receive a complimentary $10 to $20 Power Card with their meal, and for $20 USD, one can acquire 100 chips to play . Consequently, the average cost per person may range from $20 to $30 USD. This makes Dave & Buster's an attractive option for families seeking weekend outings but facing budget constraints that limit visits to theme parks.

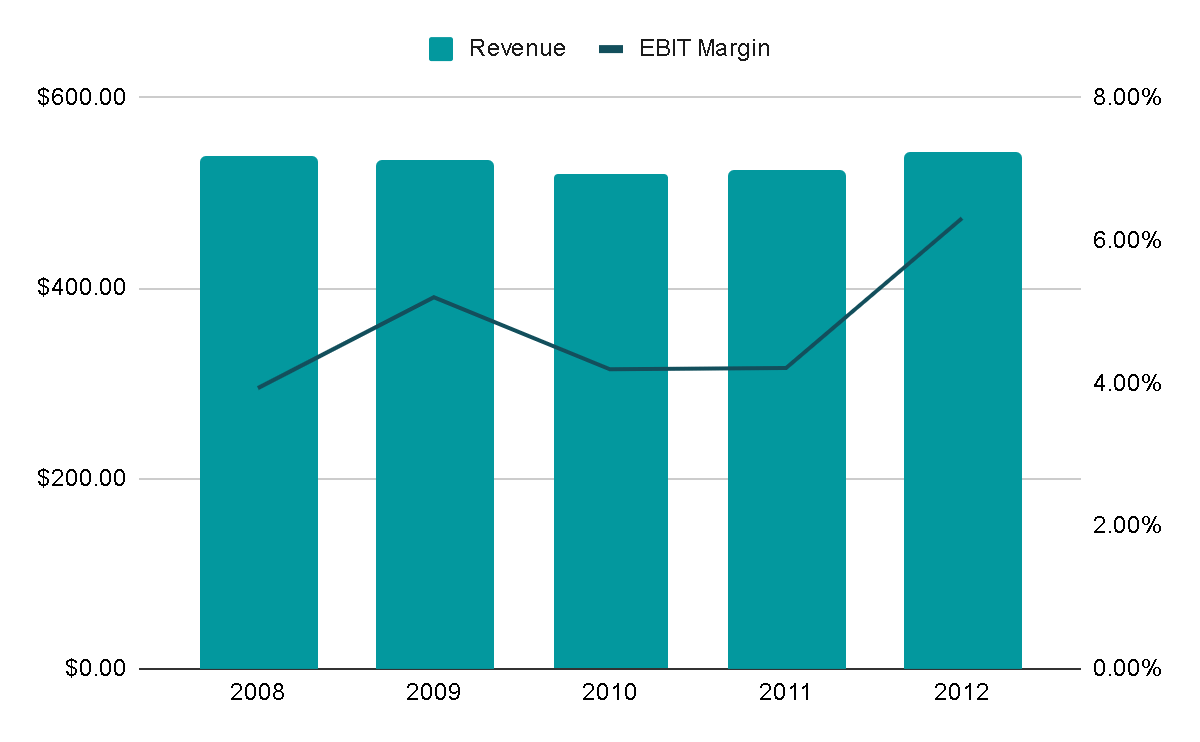

This affordability is evident in the company's performance during the economic crisis of 2008. Between 2008 and 2010, the company experienced only a 2.8% decrease in total revenue, not annually, but cumulatively. Moreover, the EBIT margin did not suffer significantly, underscoring the company's relative resilience in adverse macroeconomic conditions.

{kind=link}

Acquisition of Main Event and Strategic Review

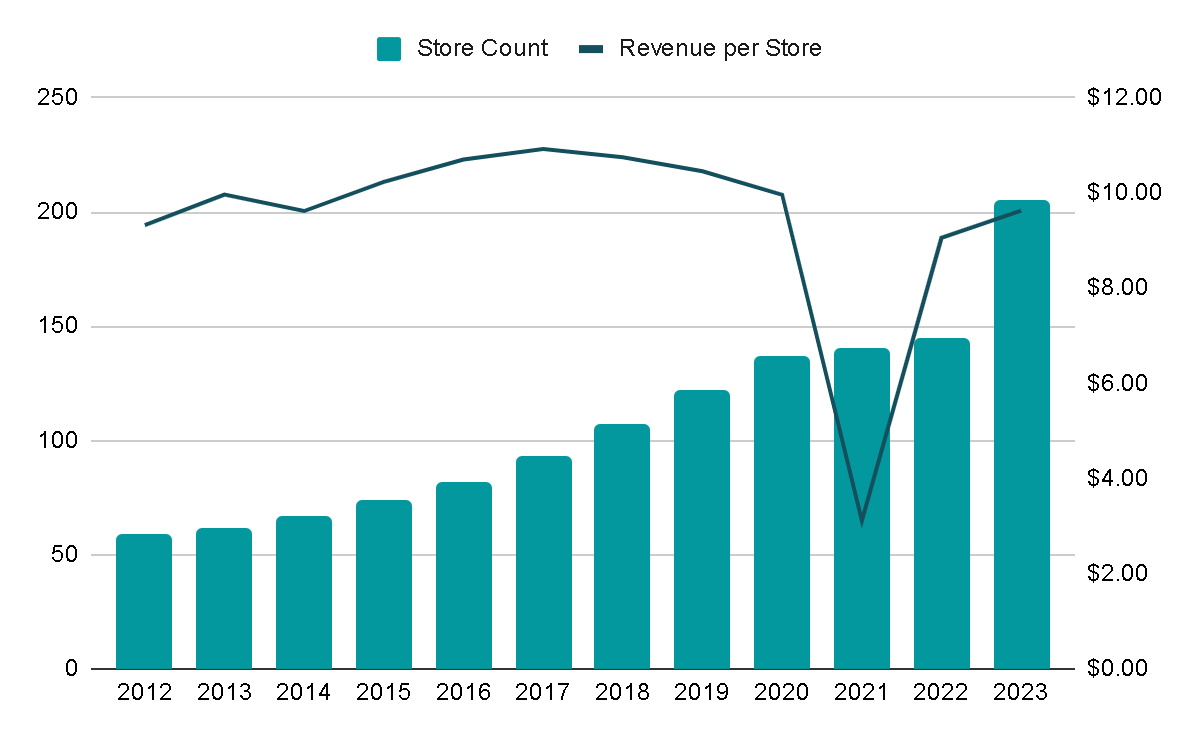

The company had been opening stores at an annual rate of 9% since 2012. However, in June 2022, they made a significant move by acquiring Main Event from the Australian group Ardent Leisure. Main Event operated 50 locations in the United States and 3 branded stores under The Summit. The noteworthy aspect of this acquisition goes beyond the numerical expansion. It involves the integration of Chris Morris , the former CEO of Main Event, who will now assume leadership at Dave & Buster's. Alongside the activist fund Hill Path Capital , they brought forward strategies to orchestrate a turnaround in the company's performance . The goal is not only to expand through the acquisition but also to leverage the new scale and broader services, such as the addition of bowling, to optimize costs and facilitate further growth.

Examining the growth per store since 2012, it has been a modest 0.3% throughout this period, even when excluding the impact of the events in 2020/2021 due to COVID-19. In other words, the company did not achieve organic growth, not even at inflation rates. This deficiency in organic growth is poised to be one of the key focal points for the new management as they strive to implement strategies for sustained and meaningful expansion.

{kind=link}

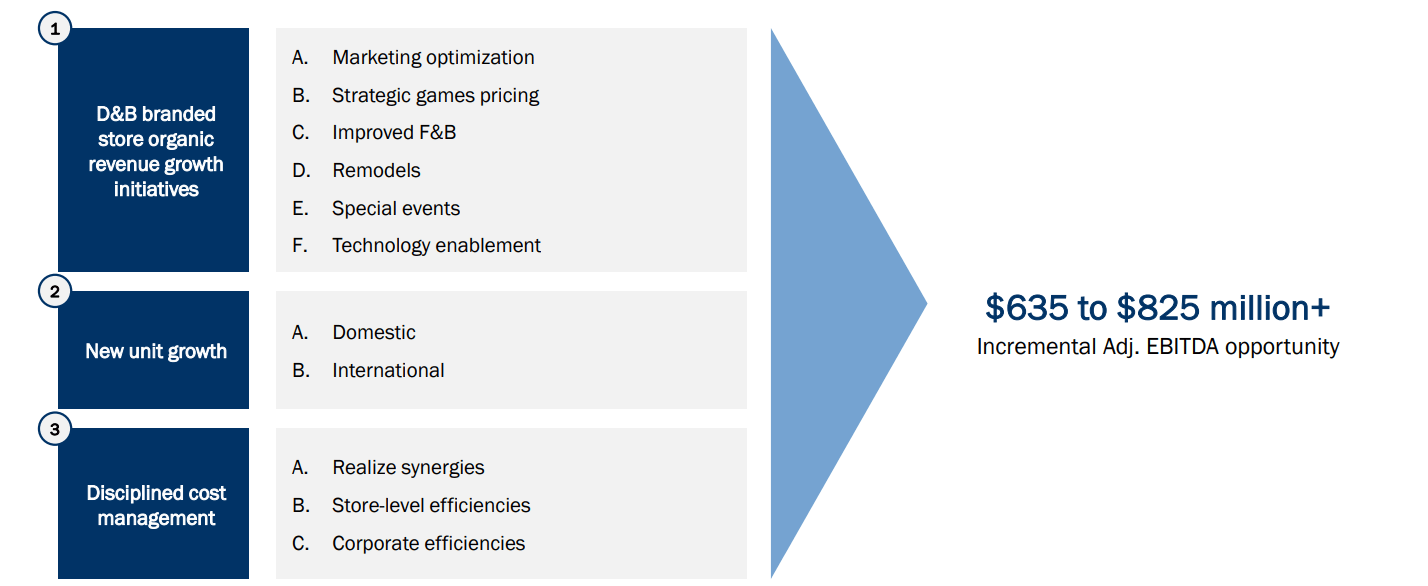

The board has pinpointed specific areas for optimization, aiming to generate incremental growth ranging from $700 to $975 million in revenue and $430 to $600 million in EBITDA. These optimization strategies revolve around the following key points :

1. Marketing Optimization:

- Although the Dave & Buster's brand enjoys significant recognition and consideration, the conversion from interested parties to customers stands at 50%, with an average annual visit frequency of 1.4x.

- The board anticipates that by enhancing customer engagement through innovative entertainment offerings and overall marketing improvements, the average annual visit frequency can be slightly increased, leading to a corresponding rise in income.

- Utilizing major sporting events such as the Super Bowl or the NBA Finals to boost traffic and customer spending is identified as an effective strategy to enhance visit frequency.

2. Strategic Games Pricing:

- The new management has observed that game prices at Dave & Buster's are notably lower than those of its peers, with discounts ranging from 40% to 80%.

- Power Card prices have remained unchanged for over 20 years , as reflected in the Revenue per Store graph. A price adjustment is seen as a direct contributor to net profit, offering a significant lever for future profit growth without requiring additional investment.

3. Improved Food and Beverage (F&B):

- The company aims to enhance menus, adjust prices, and streamline the ordering process to encourage higher consumer spending. We will go into a little more detail about this later.

These three identified aspects provide valuable insights into the strategic direction of the management and underscore the substantial opportunity for improvement within the company.

Dave & Buster's Investor Presentation

{kind=link}

Revenue Distribution and Margins

If we look at the company's performance, it seems to me that it fits perfectly with the phrase that Warren Buffett once said:

“I try to invest in businesses that are so wonderful that an idiot can run them. Because sooner or later, one will.”

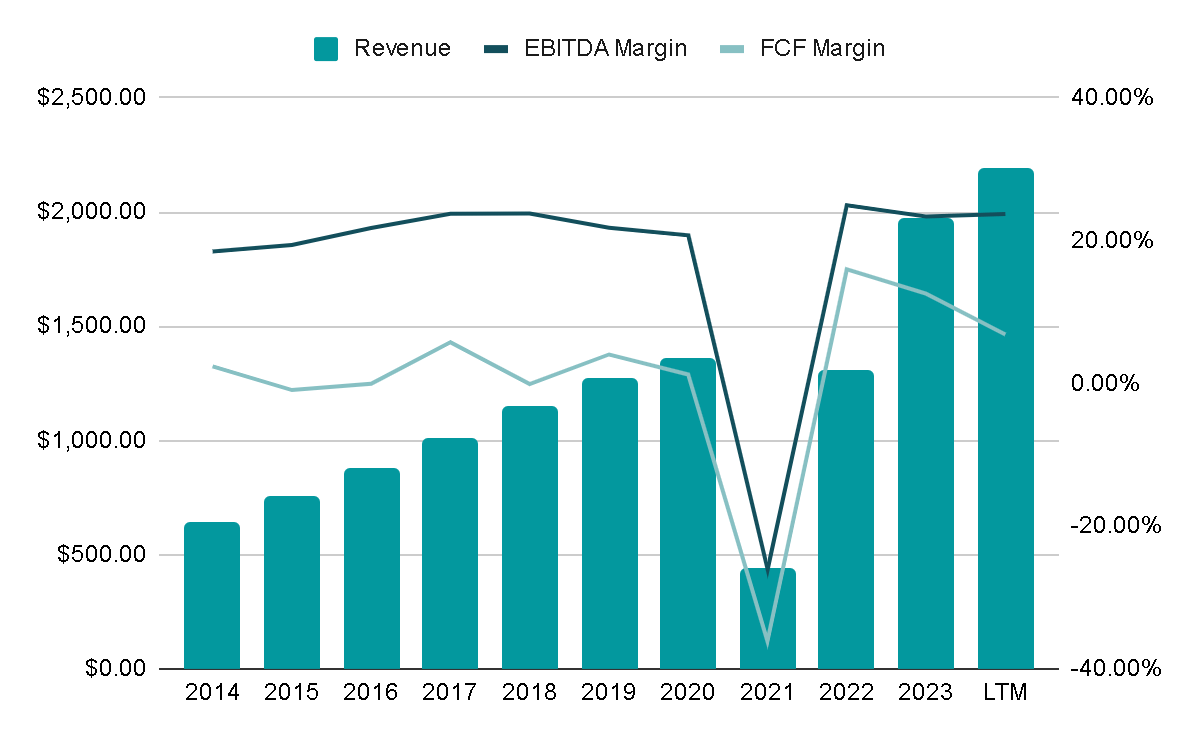

While I do not think that the former D&B management is incompetent, there is recognition of operational underperformance relative to the company's potential. Despite this, the company exhibited impressive figures, with annual revenue growing by 9.5% prior to the Main Event acquisition, even accounting for the challenges posed by COVID-19. The EBITDA margins remained solid at around 22%, indicating a company with strong fundamentals . The prospect of further improvement on top of this already excellent performance is quite promising.

{kind=link}

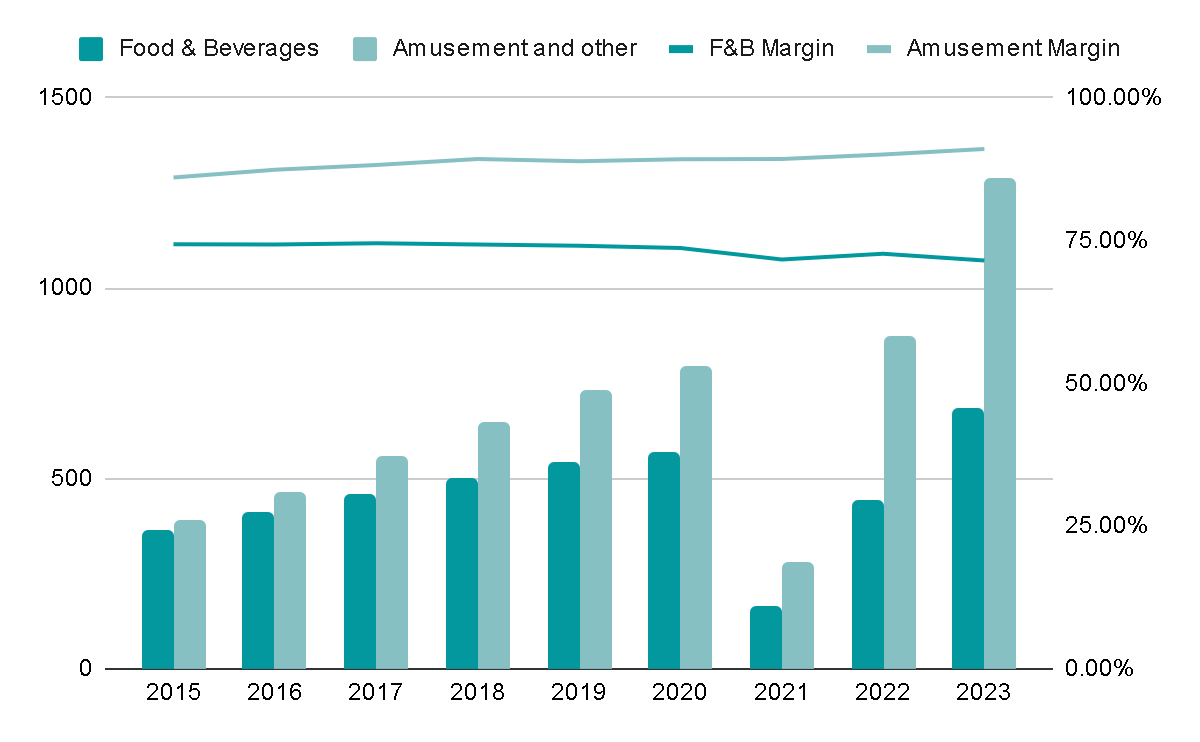

Delving into the company's two segments, it's notable that 65% of the revenue comes from the 'Amusement and Other' category, primarily comprised of games, while the remaining portion is represented by 'Food & Beverages'. Although both segments boast high gross margins, the annual report indicates a significant discrepancy in growth rates since 2015. The 'Amusement and Other' segment has experienced a growth rate twice that of the 'Food & Beverages' segment, which has grown by approximately 8%. This observation suggests a strategic imperative for management to focus on enhancing the growth of the 'Food & Beverages' segment. As evident, there is substantial room for improvement in this area as well.

{kind=link}

Valuation

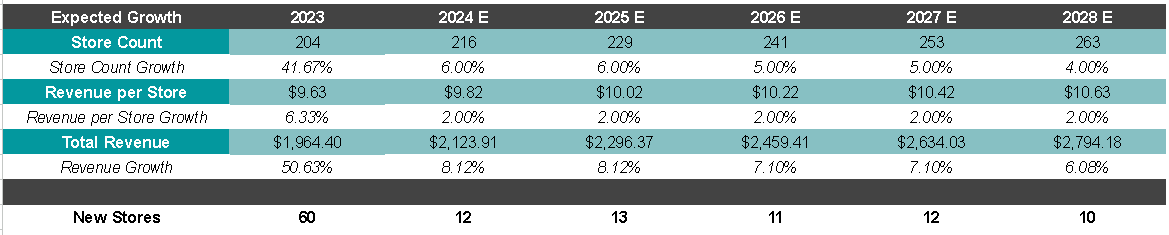

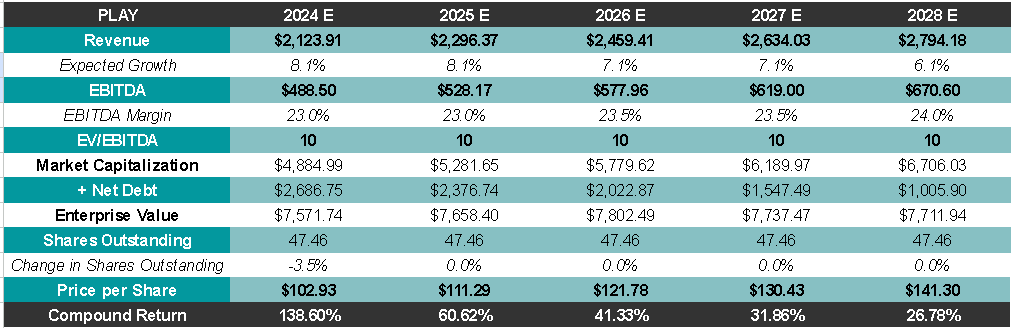

To estimate the intrinsic value of the company and potential returns over the next five years, I will conduct a valuation considering key performance indicators such as the number of stores and revenue per store.

I'm assuming a more conservative annual increase of 12 stores compared to the board's expectation of 16 stores per year for the next three years, also I project a modest 2% growth in revenue per store. This conservative estimate, below inflation, aims to underscore the attractiveness of the valuation even with cautious assumptions.

{kind=link}

Additionally, I assume a slight expansion in the EBITDA margin, increasing from the current 23.7% to 24%, reflecting a conservative outlook . Applying a 10x EV/EBITDA exit multiple to this EBITDA, we could expect a Market Cap of $6.7 billion within five years. With an expected 47.5 million outstanding shares, this would result in a per-share value of $140 USD. Compared to the current price, this represents an annual return of almost 27% , and the intrinsic value could potentially be double the current share price.

{kind=link}

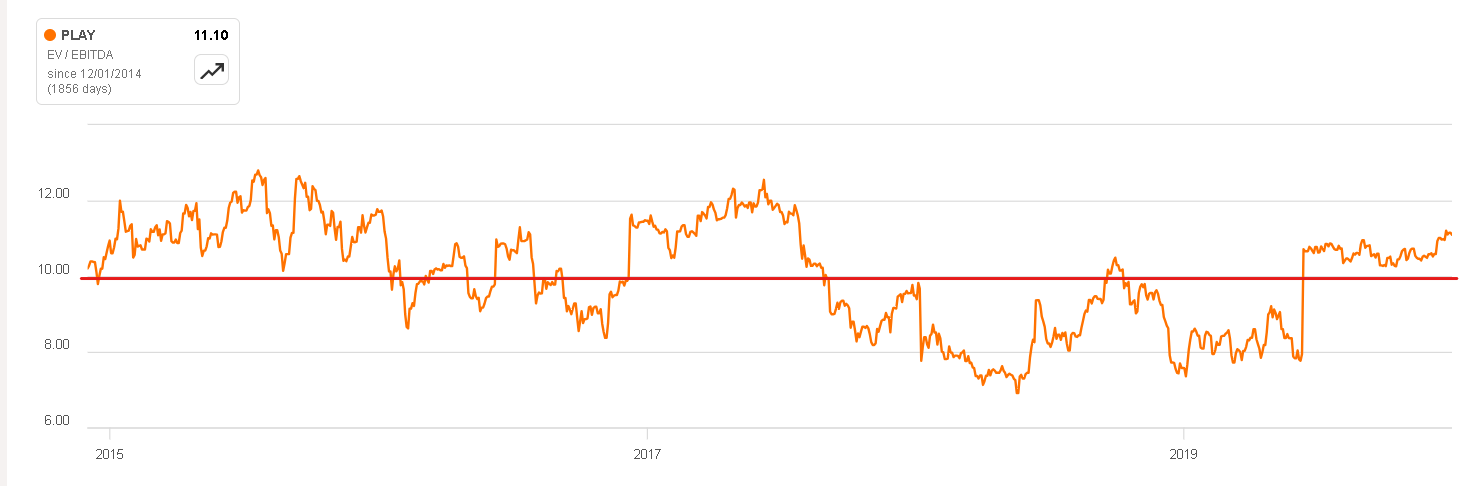

A significant contributor to this potential performance is the current trading multiple of 8x EV/EBITDA, notably lower than the historical average of around 10x. This discrepancy seems reasonable considering the capital-intensive nature of the business and a modest Return on Capital Employed of approximately 10-11%. The valuation indicates a compelling opportunity for future growth and a potential increase in market multiples to historical levels.

{kind=link}

Risks

There are inherent risks to the business model and the company's strategy, including factors like an economic slowdown, competition from other entertainment centers, potential damage to reputation, and the integration of Main Event not going as planned. However, one particularly noteworthy concern revolves around the issue of debt .

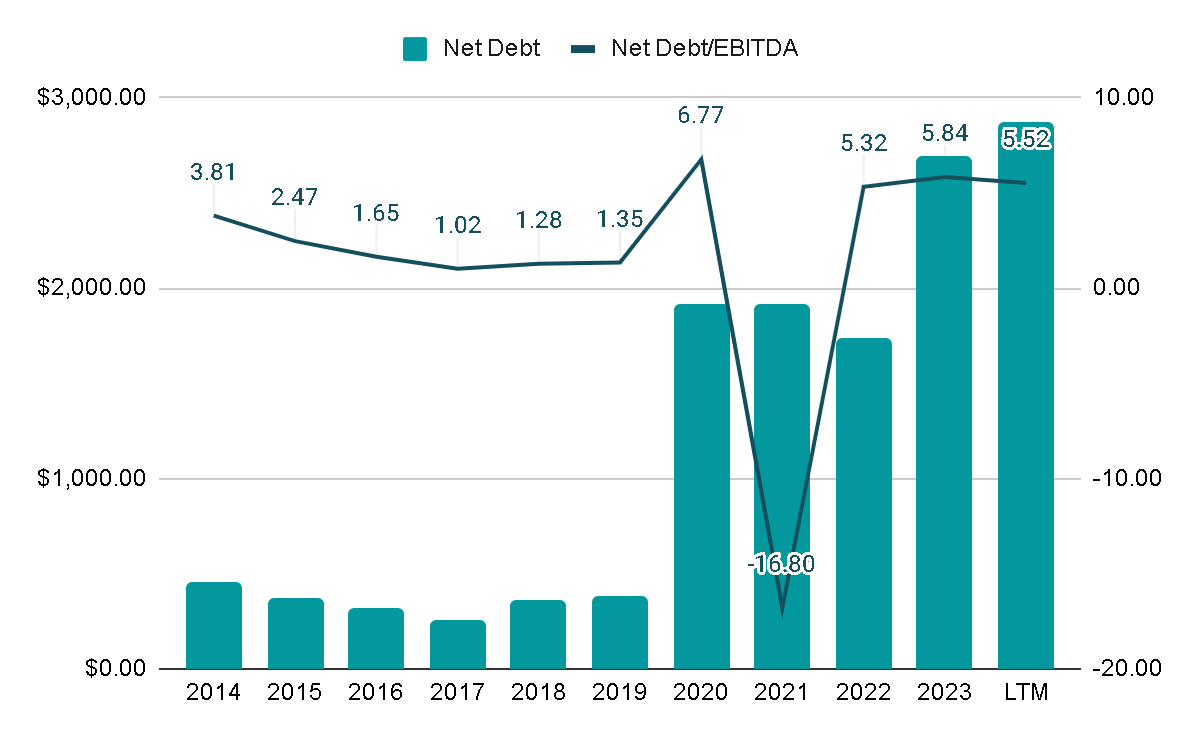

To facilitate the acquisition of Main Event, the company had to incur additional debt, refinancing a $500,000 revolving credit line and introducing a new term loan facility of $850,000. This debt comes with a maturity date set for June 2029. In total, the company now carries $1.28 billion in debt, as reported in the previous fiscal year, with an average interest rate of 9.6%. This debt burden is compounded by substantial lease obligations, amounting to approximately $1.59 billion. Given the need for physical space to operate, the company relies on leased properties for its stores, support centers, and warehouses.

The current Net Debt/EBITDA ratio stands at around 5.5x, a level considered quite high. Excluding leases, this ratio remains elevated at 2.5x when compared to the EBITDA of the last twelve months. While the risk of imminent bankruptcy may not be imminent, it's essential to acknowledge and address these high debt levels, particularly due to the elevated interest rates. Reducing debt should be a priority, especially as the company integrates the acquisition of Main Event, to enhance financial flexibility and mitigate potential challenges associated with servicing high-interest debt.

{kind=link}

Final Thoughts

I believe there are compelling reasons to anticipate that Dave & Buster's will perform well in the coming years. The arrival of a board that has demonstrated past success, particularly with Main Event, signifies a positive change. They have chosen to address key aspects that were previously neglected, and achieving these improvements does not seem unrealistic or overly complicated. The business, despite operating below optimal levels, was already performing well, and the current valuation provides a sufficient safety margin to offset the risks discussed in the article.

Considering these factors, it appears to me that D&B is a clear ' strong buy ,' and, from my perspective, it stands out as one of the most intriguing turnaround opportunities currently available in the market.

Editor's Note: This article was submitted as part of Seeking Alpha's Top 2024 Long/Short competition, which runs through December 31 . With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Dave & Buster's: An Intriguing Turnaround Opportunity