PLAY - Dave & Buster's: Time To Play The Growth

2023-06-27 06:11:47 ET

Summary

- Dave & Buster's Entertainment offers growth opportunities through store expansion, increased traffic, and potential price increases on games.

- The company plans to add 48 stores in the next three years, remodel existing locations, and expand overseas with franchises.

- PLAY faces risks such as economic downturns, competition, and concept staleness, but is attractively priced compared to peers.

With several growth opportunities in front of it, Dave & Buster's Entertainment ( PLAY ) looks attractively price at current levels.

Company Profile

PLAY owns and operates entertainment and dining establishments in the U.S., Puerto Rico, and Canada. The company currently has two concepts, its namesake Dave & Buster's stores as well as Main Event, which it acquired last year.

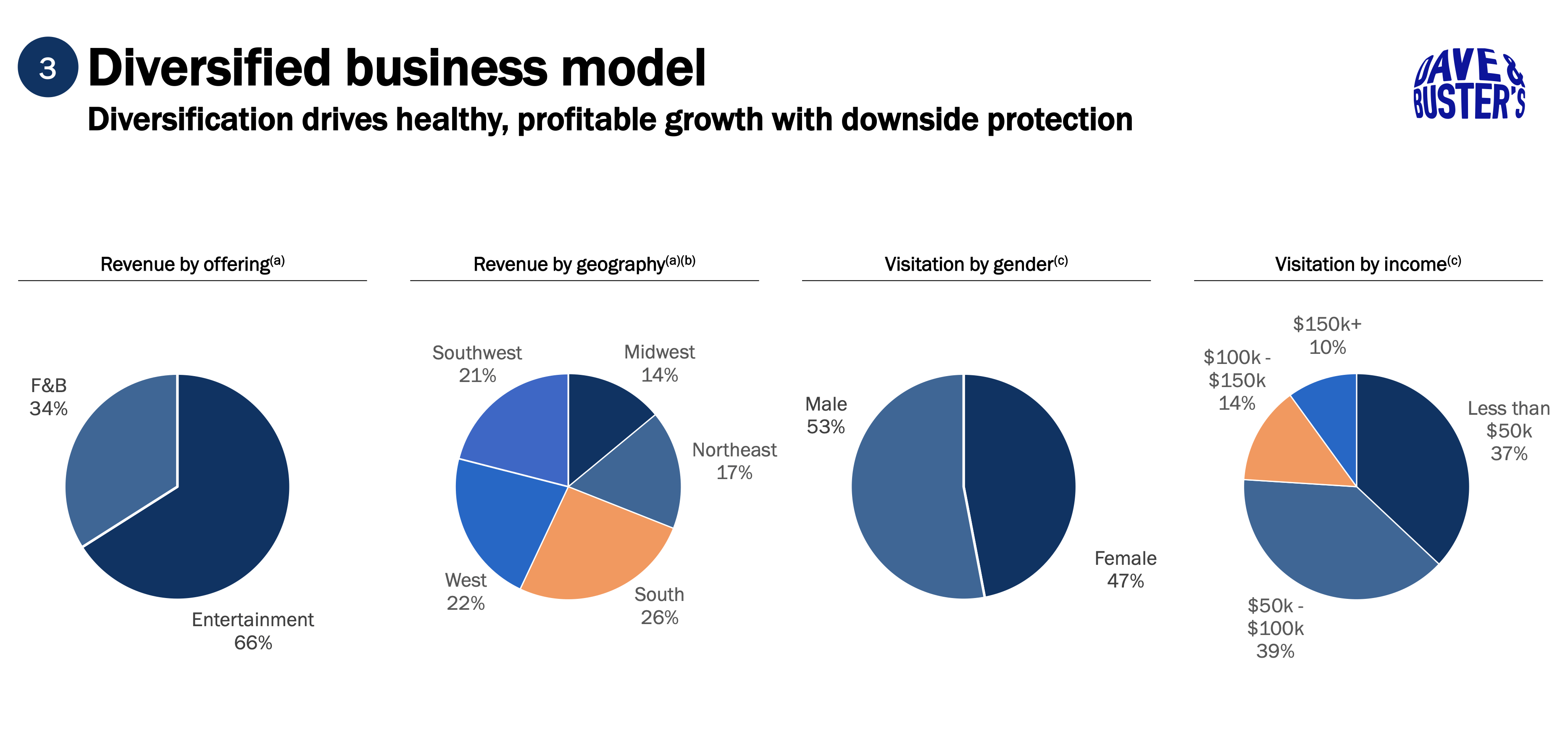

Both concept focus on game play and entertainment at their location, with amusement revenue counting for approximately 65% of its revenue in fiscal 2022. The company offers redemption games, where customers can win tickets to exchange for prizes, as well as non-redemption games, such as virtual reality, video, and simulation games. Its Main Event concept also includes bowling, laser tag, and billiards, as well as some locations with gravity ropes, mini golf, and mini escape rooms.

Food and beverage, meanwhile, represented about 23% of its total revenue in fiscal 2022. Each location also has a full bar, with alcohol beverages representing about a third of its food and beverage revenue and 11% of total revenue.

{kind=link}

Opportunities and Risks

PLAY has a number of opportunities to drive growth. With just over 200 units, including just over 50 Main Event units, store expansion is one such attractive prospect.

For its part, PLAY believes it has the opportunity to support over 550 stores across the U.S. It plans to add about 48 stores in the next three year, which is about a 24% increase in its number of units.

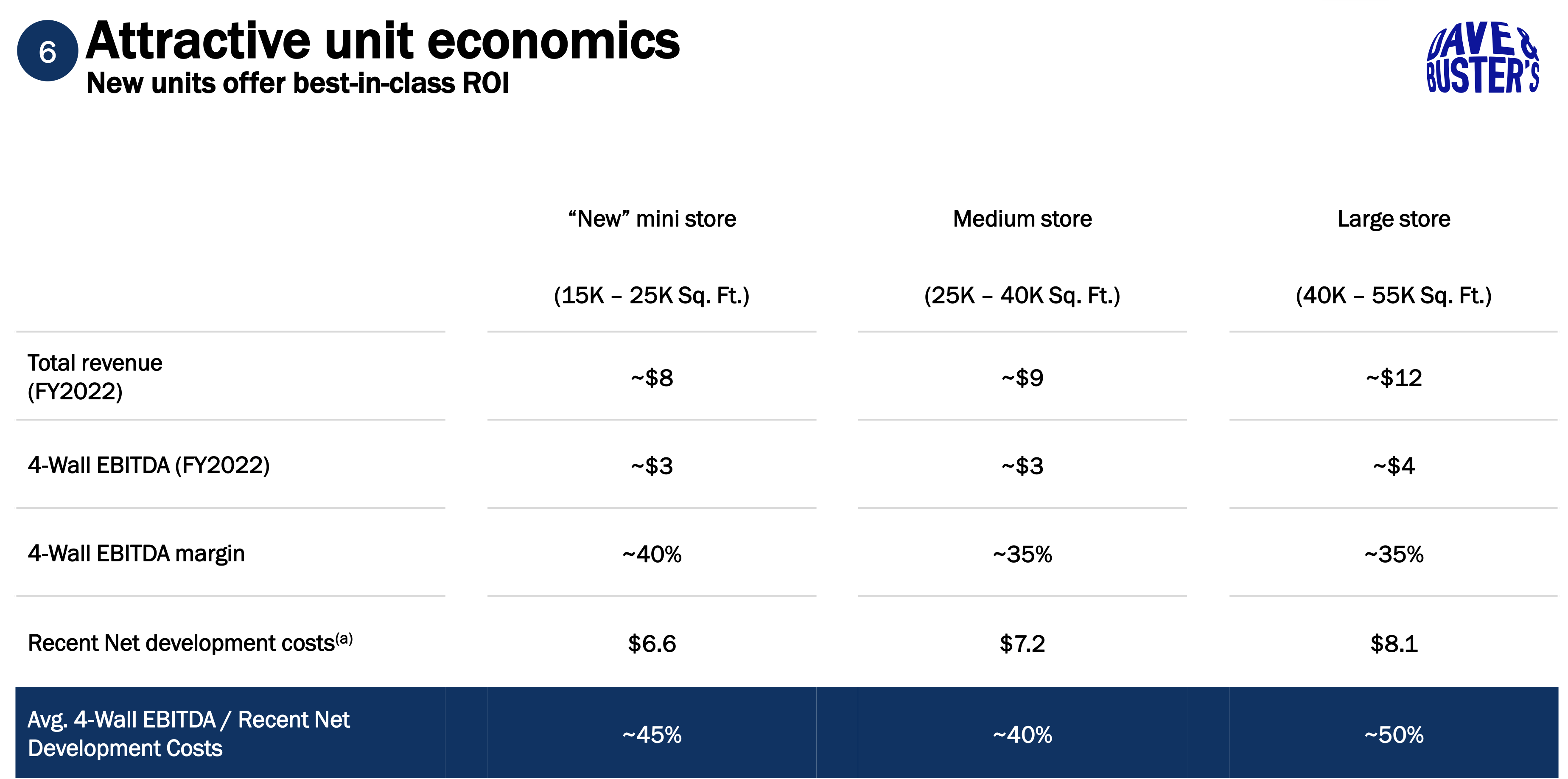

Many of these new units will be mini stores, which are about 19,000 square feet, compared to about 44,000 square feet for traditional stores. Each mini store can generate about $3 million in 4-wall EBITDA, representing an approximate $144 million opportunity. These smaller stores cost about $6.6 million to develop, so the payback period is just over 2 years.

{kind=link}

In addition, the company also has the opportunity to expand overseas, which it will do with franchises. It thinks it can support 200+ international locations, with each store contributing about $300,000-400,000 in EBITDA.

Driving more traffic to its existing locations is another opportunity for PLAY. In recent years, the company has leaned into being a place to watch sports outside of the home, and it will continue to push that narrative to drive guest visitations during various sporting events. D&B has between 20-35 screens per location and a large sports viewing area, so the plan is to optimize marketing around big events to watch these events. Improving its menu, upgrading its restaurant tech, and remodeling stores will also be done to help improve traffic and keep guests coming back.

On the remodel front, the company estimates that it will cost between $1-4 million, with a target ROI of 20-25%. It said its last remodel cycle was between 2011-2017 and that its stores saw an average 12%+ sale uplift and a 33% 4-wall EBITDA uplift.

PLAY also believes it has an opportunity to increase the prices on its games. The company said the prices for competitors' games were 40% and 80% higher than those of D&B. However, it doesn't plan to increase prices across the board. Instead it will look to raise prices on lower chip tiers, as well as implement different prices by geography and introduce dynamic pricing during peak periods. At the same time, it will look to raise prices in line with inflation.

Given that PLAY's games have about 90% gross margins, even a small price increase can have a pretty large impact on its bottom line. The company estimates that for every 1% increase in price that it would increase EBITDA by $10 million.

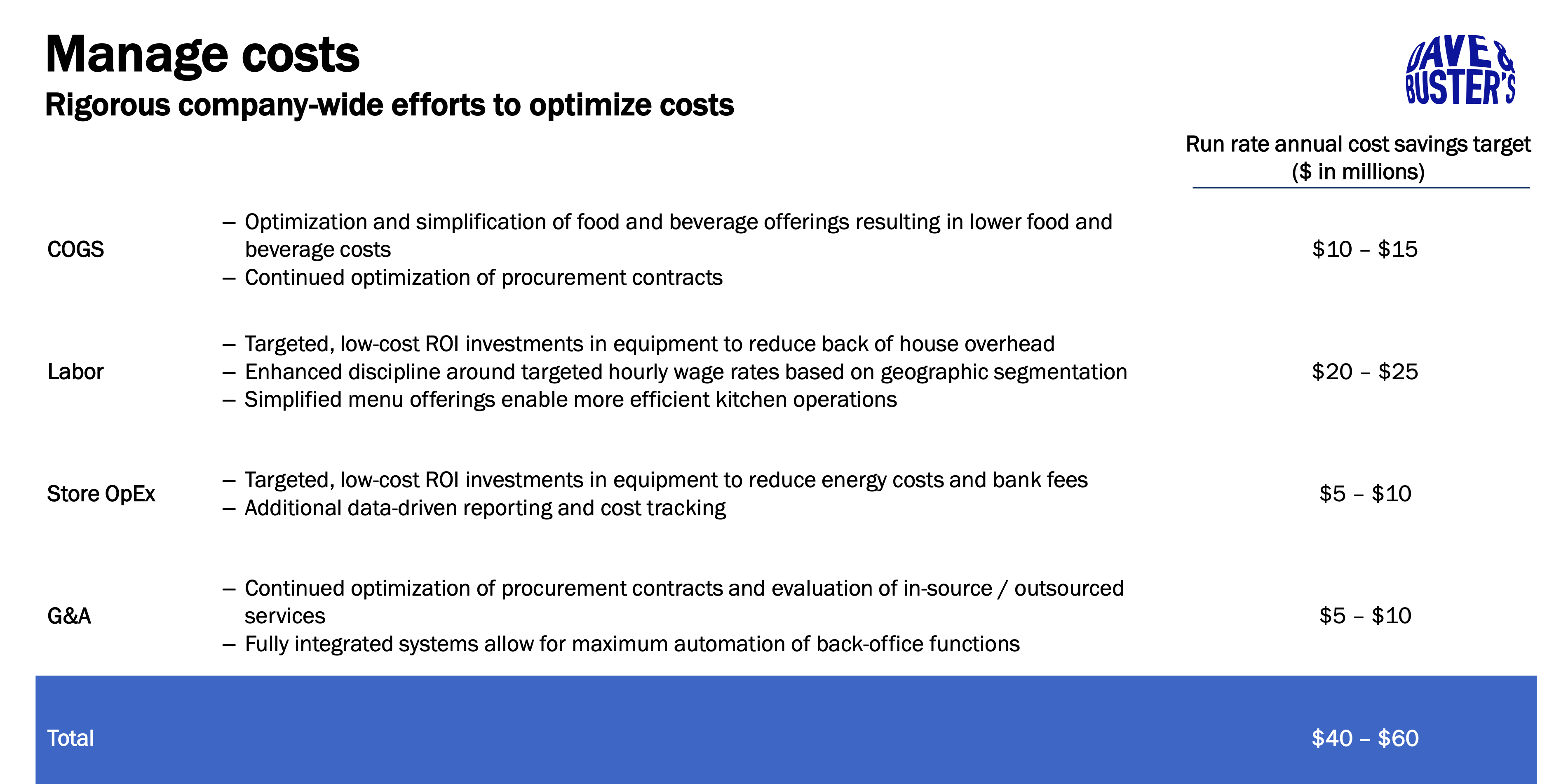

In addition to driving revenue growth, with its recent merger with Main Event, PLAY also has opportunities on the costs side as well. The company recently raised its synergy target for $20 million to $25 million, with about $17 million still to be realized. It also thinks it has the ability to reduce costs through investments in technology, as well as through things like menu simplification and optimizing procurement contracts. It sees another $40-60 million in cost saving potential in addition to its Main Event synergies.

{kind=link}

On the risk side, the economy is a big one. Going to a D&B or Main Event isn't cheap, so less frequents visits from customers when they are pinching pennies is a possibility. Inflation has driven up costs, so a night out at D&B or a day spent at Main Event could be something that people pullback from if the economy continues to weakens.

In a similar vein, the company has a nice corporate event business as well. When companies pull back on spending, events and holiday parties can be some of the first perks to get cut. For its part, PLAY notes that the business is still below pre-Covid levels and that Main Event has done a good job growing this business though compensating managers, which D&B can replicate.

Competition and staleness are two other risks. The next new hot concept might just be around the corner like TopGolf when it came onto the seen in force. Meanwhile, throughout its history, PLAY has gone through some periods where the concept has gone out of favor. In addition, its virtual reality platform never really lived up to expectations given the time and labor involved with it.

Valuation

PLAY stock currently trades at 8.4x the FY2024 (ending January) consensus EBITDA of $550 million and 7.8x the FY2025 consensus of $590 million.

It trades at a forward P/E of 11.8x the FY24 consensus of $3.62 and 9.6x the FY25 consensus of $4.47.

Revenue growth is expected to grow 16.5% this year given the Main Event acquisition, and then grow over 7% the year after.

The company has over $1.1 billion in debt, and is about 2x leveraged.

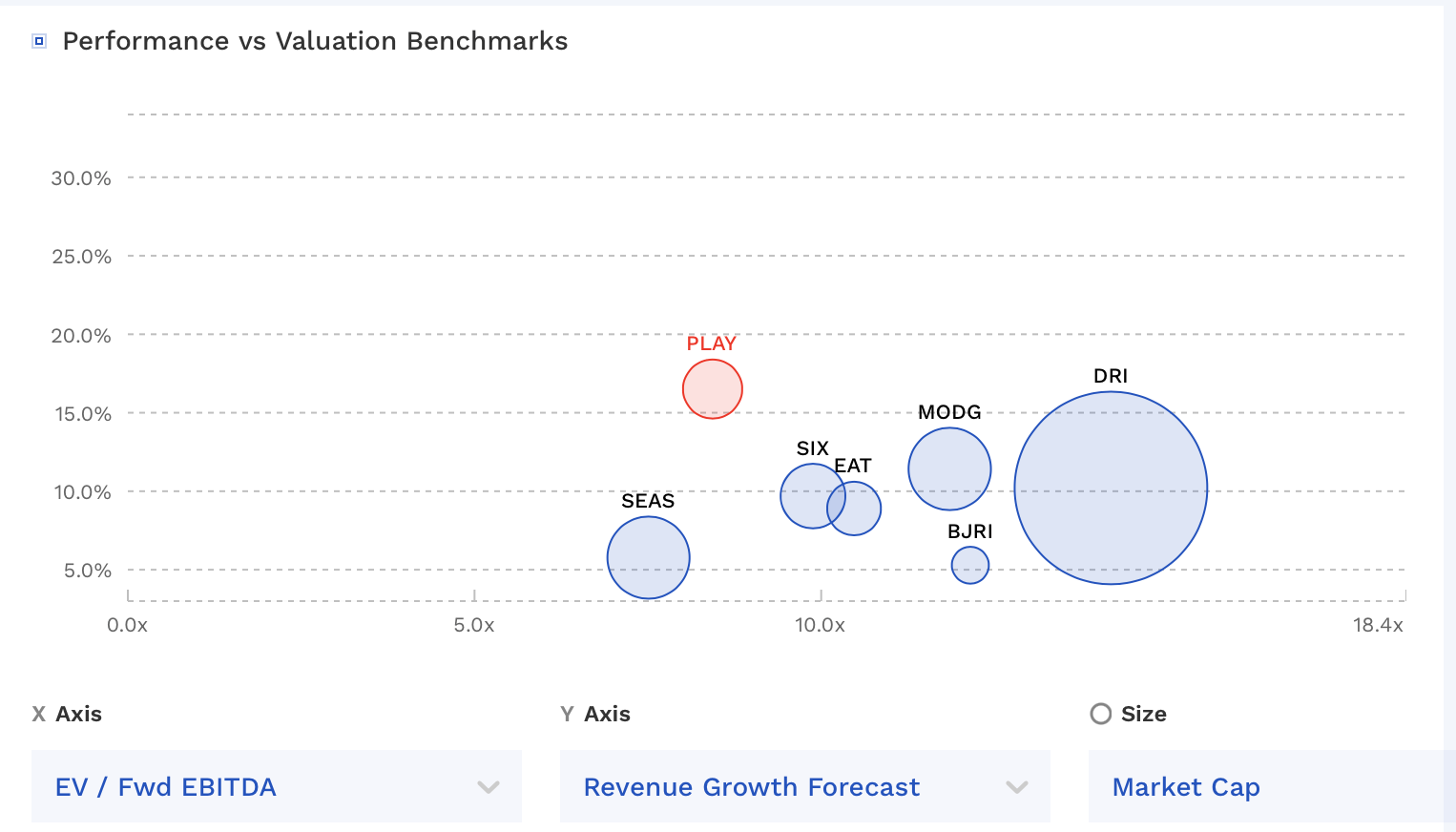

PLAY trades towards the lower end of its entertainment and restaurant peers.

{kind=link}

Conclusion

PLAY is an interesting name in the restaurant and entertainment space, as its focus on games gives it a superior margin profile to its restaurant peers. At the same time, it can be a bit more vulnerable to consumer trends and the economy.

The Main Event acquisition looks like a good one, and with it comes a largely new management team. The company has some nice growth opportunities ahead with expansion growth and remodeling, while at the same time it can take out costs as well. In addition, the ability to raise some game pricing could be a powerful growth driver as well.

Compared to other "peer" companies, I think PLAY looks attractively priced for the growth potential in front it. I see upside to $60+, which would be about a 9x multiple on FY25 estimates. Note however given its economically sensitivity, it does certainly carry some risk.

For further details see:

Dave & Buster's: Time To Play The Growth