DASH - Delivery Hero: Beaten Down Enough And Worth Buying

2023-04-04 13:05:34 ET

Summary

- Delivery Hero is currently trading at -78% from its all-time high.

- Delivery Hero posted 9.26% YoY gross merchandise value growth in 4Q which is very strong compared to other major services.

- The food delivery industry is forced to focus on profitability. More reasonable competition and market consolidation is a catalyst.

- Adjusted EBITDA as a % of GMV improved significantly from -3.3% in 4Q 2021 to -0.3% in 4Q 2022.

- In my view, Delivery Hero has significant potential upside and I assign a target price of €44.5.

Editor's note: Seeking Alpha is proud to welcome Borut Markelj as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Delivery Hero's (DLVHF) 4Q 2022 results came a bit lower than expected but the company's stock has been hit harder than anticipated. Investors may be overreacting to short-term results and I believe there is a clear future for food delivery services. The global food delivery sector is projected to grow at a CAGR of 12.33% between 2023 and 2027, and it appears that younger generations have no inclination to revert back to self-cooking. Delivery Hero is actively shifting its focus from growth to profitability, as evidenced by several financial indicators. I think the investors who will be patient enough for this restructuring to unfold will get rewarded.

Many people used online food delivery ordering prior to the COVID-19 pandemic, and many more are using it now. In this article, I will explain why a recent sell-off in food delivery stocks represents a good investment. We have seen big declines in stock values ranging from 50% to 82% from their all-time highs where Delivery Hero is currently trading at -80% from its all-time high.

| All-time high |

| All-time low |

| Today's value |

| Change from All-time high |

| Year-to-Date return |

| JTKWY |

| 19.84 |

| 2.33 |

| 3.77$ |

| -81.00% |

| -15.47% |

| DASH |

| 257.25 |

| 41.37 |

| 63.56$ |

| -75.29% |

| 31.43% |

| DROOF |

| 6.00 |

| 0.84 |

| 1.04$ |

| -82.67% |

| 2.62% |

| DLVHF |

| 171.95 |

| 25.99 |

| 34.13$ |

| -80.15% |

| -29.53% |

| UBER |

| 64.05 |

| 19.90 |

| 31.7$ |

| -50.51% |

| 25.00% |

Created by Author, using data from 03 April 2023.

Growth and Profitability?

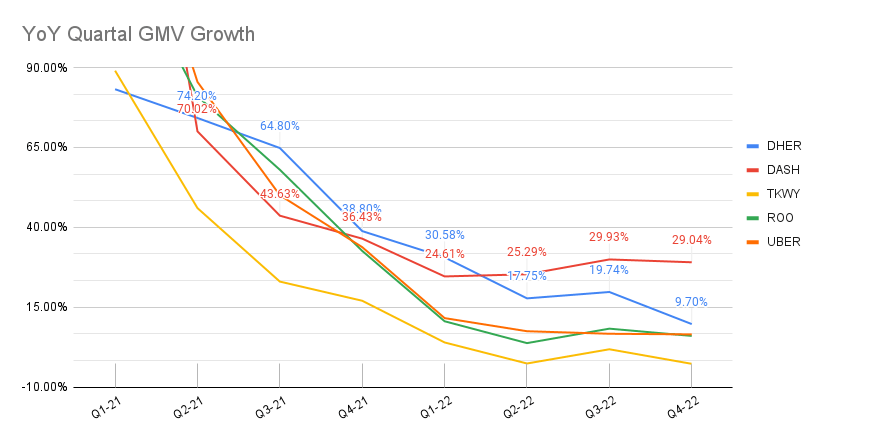

I will focus on GMV (gross merchandise value or total transaction value), as this is one of the most relevant metrics and all companies report it on a quarterly basis. GMV growth for the last 6 quarters is obviously slowing down and the effect of the pandemic is easing out. The graph below illustrates YoY quarterly growth development, illustrating a drastic slowdown in 2022 with some services already experiencing negative growth rates.

YoY quarterly GMV growth (Created by Author, using data from Q4-22 reports)

{kind=link}

Delivery Hero reported 9.7% GMV growth for 4Q 2022 which is the second-highest growth after DoorDash (DASH). Just Eat Takeaway performed poorly and actually reported a -2.74% decline in 4Q 2022 GMV on a YoY basis. For Uber Eats (UBER), data I only took growth on their delivery segment.

For Delivery Hero, concerning data came from the Asian market which represented 58.7% of the total GMV in 4Q 2022 and the growth in this area stagnated on a year-to-year basis. Management explained that the weak YoY growth was mainly due to lockdowns that were enforced in South Korea last year and were lifted later in April 2022. Therefore, I also expect the same weak or negative growth for 1Q 2023 from this market.

Delivery Hero GMV growth in the Asian market (public)

{kind=link}

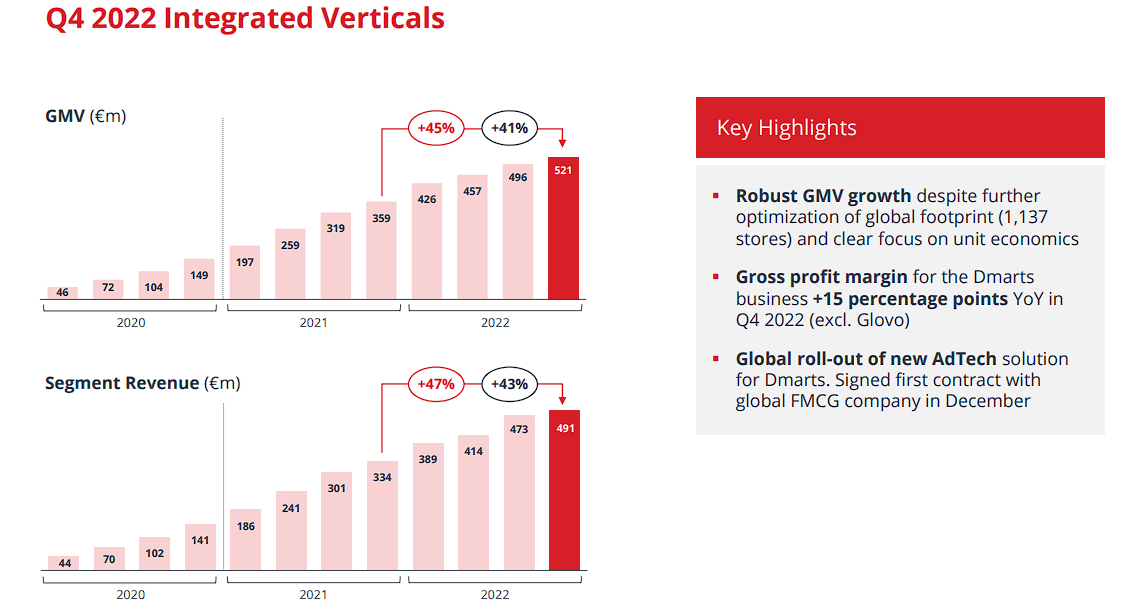

The biggest GMV growth was recorded in the Integrated vertical where the concept of cloud kitchen and micro fulfillment centers (MFCs) is reported. The number of MFCs established is currently at 1137 worldwide and remained mainly flat from 1Q 2022 when Delivery Hero was operating 1122 MFCs. Even with the same number of stores, revenue jumped more than 45% YoY and I am looking forward to the yearly report to examine unit economics improvements. I definitely see a big potential in MFCs going forward as real estate infrastructure with Delivery Hero's own fleet is capable of delivering any goods within 30 minutes within the cities.

Q4 2022 Integrated Verticals (IR Q4 presentation)

{kind=link}

On the investor's call, Delivery Hero management was not able to provide GMV and Revenue guidance for 2023, which will be provided later on 27th April together with 1Q 2023 and the yearly report.

None of the food delivery companies reported profits in the latest quarters and investors probably began to question when, if not now, this business model will turn profitable. The pandemic gave the segment a large boost, in terms of free advertisement in mainstream media (the online food ordering platforms were often mentioned as a good solution to all food-related problems during lockdowns), and of course by heavily increasing the user bases and their order frequencies. During the pandemic, the world simply changed in favor of these services.

V aluation and target price

Delivery Hero reached €9.5 billion in revenue and €44.6 billion in GMV through 2022, making it currently trading at a 0.8x price-to-sales ratio. The company improved adjusted EBITDA as a percentage of GMV significantly from -3.3% in 4Q 2021 to -0.3% in 4Q 2022 and is promising further improvements in 2023. The adjusted EBITDA management target for 2023 is 0.5% as a percentage of GMV and free cash flow breakeven in H2 2023.

Based on available reports I made a DCF analysis and set my target price at €44.5 per share . I believe my estimation is conservative as I took into consideration a modest yearly growth rate and used a lower EBITDA/GMV margin target than what management has set.

I've worked in the food delivery sector for a long time and also had the privilege to run a local food delivery platform that was later acquired. From my experience, the EBITDA/REVENUE margin between 14% and 18% is easily possible to achieve with this business model. I actually achieved this with my own company on a smaller scale, where we faced higher transaction costs, higher development costs per order and higher equipment costs. Delivery Hero's long-term EBITDA/GMV margin target is 5-8%. However, for my DCF analysis, I have predicted that the company will only achieve a margin of 4.5% in the terminal year.

I also used a more modest GMV yearly growth of 12% compared to management guidance of 20% yearly growth.

Assumptions taken into consideration:

- Risk-free rate: 2.47% (10y German bond)

- For the terminal growth rate, I took the 10y German bond (the same I used for the risk-free rate)

- Equity risk premium 6.95%

- Beta on food delivery 1.57

- Tax rate 30.18%

- Cost of equity 13.3%

- Cost of capital 14.1%

- Nr. shares outstanding 265,730,000

- The conversion used USD/EUR = 0.93

| 2022 |

| 2023 |

| 2024 |

| 2025 |

| 2026 |

| Terminal value |

| 1 |

| 2 |

| 3 |

| 4 |

| 5 |

| GMV [billion] |

| €44,700 |

| €49,170 |

| €55,316 |

| €62,231 |

| €70,010 |

| €71,739 |

| Growth GMV YoY |

| 17% |

| 10.00% |

| 12.50% |

| 12.50% |

| 12.50% |

| 2.47% |

| Operating Margin (GMV -> RVN) |

| 21.92% |

| 22.00% |

| 22.55% |

| 22.99% |

| 23.45% |

| 24.05% |

| Revenue [billion] |

| €9,800 |

| €10,817 |

| €12,476 |

| €14,310 |

| €16,420 |

| €17,256 |

| Revenue growth rate |

| 10.38% |

| 15.34% |

| 14.69% |

| 14.75% |

| 5.09% |

| EBITDA (% GMV) |

| -1.50% |

| 0.50% |

| 1.25% |

| 2.55% |

| 3.55% |

| 4.50% |

| EBITDA [million] |

| -€671 |

| €246 |

| €691 |

| €1,587 |

| €2,485 |

| €3,228 |

| FCFF [million] |

| -€468 |

| €172 |

| €483 |

| €1,108 |

| €1,735 |

| €2,254 |

| Risk-free rate |

| 2.47% |

| 2.47% |

| 2.47% |

| 2.47% |

| 2.47% |

| 2.47% |

| Equity risk premium |

| 6.95% |

| 6.95% |

| 6.95% |

| 6.95% |

| 6.95% |

| 6.95% |

| Cost of equity |

| 13.39% |

| 13.39% |

| 13.39% |

| 13.39% |

| 13.39% |

| 13.39% |

| Cost of debt |

| 15.59% |

| 15.59% |

| 15.59% |

| 15.59% |

| 15.59% |

| 15.59% |

| Cost of capital |

| 14.12% |

| 14.12% |

| 14.12% |

| 14.12% |

| 14.12% |

| 14.12% |

| DFCF [million] |

| -€410 |

| €132 |

| €325 |

| €653 |

| €896 |

| €10,232 |

| Valuation [billion] |

| €11,828 |

| Valuation per share |

| €44.5 |

Author's DCF Calculations

If you are not comfortable going long with Delivery Hero at current prices, you could also sell some put options. Due to the high implied volatility, the premiums are really high. For example, selling a Dec15'23 22 Put will pay approximately €220 per option.

Risks to my investment thesis

The primary risk I see is associated with the macroeconomic environment, particularly in case of a severe recession, which would result in customer purchasing power deterioration. In such case, customers would shift from ordering in high-end restaurants towards food delivery chains with lower average order values. Users may also reduce their frequency of orders and opt to cook more at home.

Another risk is the impact of increased interest rates on Delivery Hero's ability to access capital as favorably as before. For instance, on 13.02.2023, Delivery Hero placed 1000 million convertible bonds due in 2030 with an interest rate of 3.25%, which is considerably higher than previous rates. The proceeds from the newly issued bonds will be utilized to repurchase existing convertible bonds that are set to mature in 2024 and 2025. Delivery Hero reinforced its financial position by improving its debt maturity profile and boosting its balance sheet.

Convertible bonds currently outstanding:

| Maturity date |

| Coupon |

| Value outstanding in million (€) |

| Initial Conversion Price (€) |

| 1/23/2024 |

| 0.25% |

| 287 |

| 98 |

| 7/15/2025 |

| 0.88% |

| 750 |

| 143.9 |

| 4/30/2026 |

| 1.00% |

| 750 |

| 183.1 |

| 1/23/2027 |

| 1.00% |

| 875 |

| 98 |

| 1/15/2028 |

| 1.50% |

| 750 |

| 148.9 |

| 3/10/2029 |

| 2.13% |

| 500 |

| 183.1 |

| 2/21/2030 |

| 3.25% |

| 1000 |

| 57.75 |

Author's table based on businessinsider data

The third risk is major shifts in rider law. Delivery Hero currently treats the majority of couriers as sub-contractors, and in some countries, this classification is still in development. While there have been some positive court decisions in the US regarding the topic, regulations and legal decisions in the MENA, Asian, and European regions where Delivery Hero operates are still evolving. Delivery Hero brand Glovo was recently fined € 56.7 million over hiring.

Market consolidation and who wins?

The bigger you get, the more optimization is possible. As companies consolidate operations, they can optimize various areas such as HR, equipment, and online payment transaction costs, leading to lower costs per order. The biggest cost food delivery services currently have is paying a courier to deliver a meal. The total delivery distance per order is measured by current location -> pickup, and pickup -> delivery location. By increasing a courier density, the distance between the current location and the pickup location can be reduced, and with bigger fleets, the routing and scheduling algorithms gain more possibilities to optimize the total distance traveled.

However, whenever one market matures and one player establishes high commissions and delivery fees, it creates an opportunity for new services to emerge and challenge them. With the current environment being less friendly to new smaller players entering markets and raising new capital, consolidation is likely to occur faster, resulting in fewer players competing in each market.

We should also expect companies to focus more on the markets they are winning and sell or exchange operations in those where they are losing money. For example, last year Just Eat Takeaway left Romania and Deliveroo left the Netherlands , such processes already happened before, but supposedly it will be more definitive this time.

We have already seen M&A transactions of DoorDash acquiring Wolt and Delivery Hero taking over Glovo . Just Eat Takeaway is also searching for a possible buyer for Grubhub. Personally, I would also not be surprised if Deliveroo (DROOF) merged with one of the bigger players.

Conclusion

I believe that the food delivery industry, particularly when combined with ultra-fast delivery from micro fulfillment centers, has a promising future. Everyone has to eat at least once per day and the Delivery Hero is in a great position to remain one of the biggest food delivery companies and a market leader in many markets.

Nevertheless, I believe that the current valuation, in light of the potential market opportunity, justifies the identified risks, and I mark Delivery Hero stock as a buy.

For further details see:

Delivery Hero: Beaten Down Enough And Worth Buying