EADSY - Delta Air Lines Stock: Strong Buy On Historic Earnings And Supercycle Growth

2023-07-14 07:51:22 ET

Summary

- Delta Air Lines reported Q2 earnings of $2.68 per share, beating analyst consensus by $0.29 and exceeding the high end of its guided range by $0.18.

- Despite record-high earnings and reinstated dividends, the stock has lost altitude due to flat guidance on total revenues and expected decline in unit revenues.

- Delta is proactively working on longer-term savings and fleet efficiency, expecting earnings of $6 to $7 per share for the year, up from the $6 guided during the Investor Day.

Delta Air Lines (DAL) reported its second quarter earnings before the opening bell on the 13th of July. At the time of writing, the stock is trading roughly flat after an initial spike. I don't want to be overly focused on any lack of price action, but I want to have a look at the results and the guidance as well as a price target for the stock.

Delta Beats Expectations

{kind=link}

Delta Air Lines has an excellent track record when it comes to beating revenue estimates. In the second quarter, it booked $15.58 billion in revenues beating estimates by 0.77%. On earnings levels it beat expectations 5 out of the last 8 quarterly earnings and in the second quarter its $2.68 in earnings per share beat the analyst consensus by $0.29 and beat the high bound of the $2.20 to $2.50 guided range by $0.18 cents. So, without doubt Delta Air Lines had a strong quarter.

A Dive Into The Delta Air Lines Results

{kind=link}

When analyzing companies, I don't just pay attention to the results and management comments, but also how the results are presented and Delta Air Lines does a terrific job putting revenues from various end markets next to unit revenues, yield and capacity.

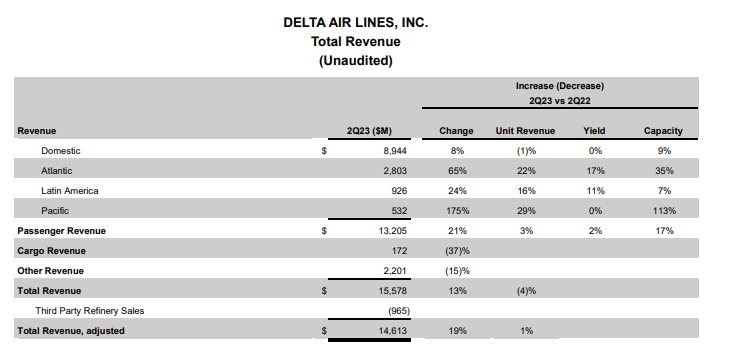

Overall, passenger revenues grew by 21% and that was driven by a combination of 17% capacity growth and 3% expansion in unit revenues and a 1 point expansion in load factors. Between the end markets, we see quite some variability in revenue growth, unit revenue changes, yield changes and capacity expansions.

On domestic, we see that capacity increased by 9% and revenue grew by 8% as unit revenues softened a bit. So, on the domestic market it seems that growth on revenues is more in line with capacity expansion and we might be hitting a limit on the revenue potential there. On Atlantic and Pacific we still see unit growth in the 20 to 30 percent region with capacity expansion in the Pacific more than doubling as the network and frequencies are being restored. In the Latin American market we also see a strong uptick in unit revenues against a lower capacity expansion. This suggests that the growth in revenues primarily comes from long-haul transatlantic and pacific followed by Latin America and after that the domestic market which could start turning into a headwind if unit revenues head go to more normalized levels.

Overall, the revenues still improved by 21% with revenue growth in all passenger end markets and I still see growth ahead as international corporate travel also mixes more into the recovery story. Cargo revenues declined by 37%, which is not odd given that unit rates are softening. Other revenues declined by 15% driven by lower revenues on refinery sales offset by higher loyalty program and ancillary revenues for a total decline in unit revenues of 4% and a 1% unit revenue growth when excluding refinery sales.

In total, operating income was nearly $2.5 billion. With 6% cost growth and 13% growth in revenues there was an appreciable expansion on the operating margin to 16% or 17.1% on adjusted basis.

{kind=link}

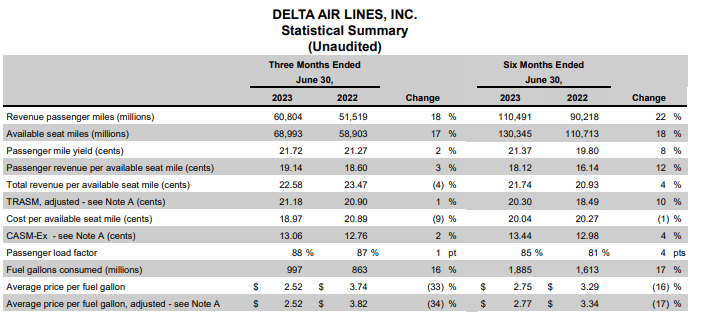

The unit figures might give a better picture, showing that adjusted TRASM was up 1% with cargo revenues pressuring the overall unit revenues. Passenger unit revenues were up 3%. In prior quarters, we had double-digit growth in unit revenues. That is obviously tapering now as the comp is changing to strong unit revenues this year being measured against strong unit revenues last year and growth in revenues is coming from continued growth in unit revenues in some markets but more so from capacity expansion in the markets were Delta still needs to recover capacity. Overall, unit costs declined by 9% helped by 33% lower fuel prices but ex-fuel unit costs were up 2% showing that adding capacity has not yet pushed down the unit costs which makes sense given increased labor and inflationary costs. Important, however, is that Delta pointed out that they are at an inflection point here.

So, overall, Delta booked strong earnings that exceeded expectations and show that the company is on the right trajectory.

Delta Air Lines Stock Loses Altitude

{kind=link}

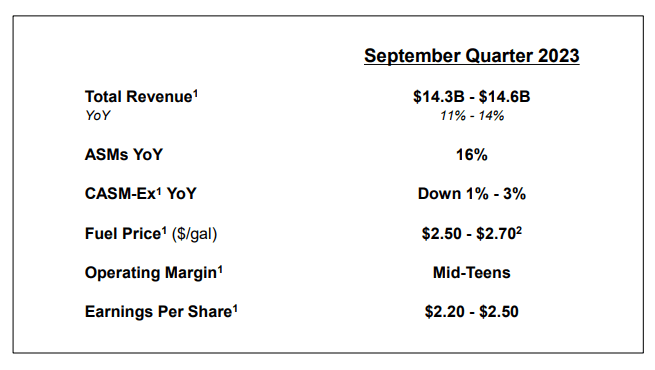

While Delta booked record high earnings per share and it has reinstated its dividend as announced previously, the stock has lost altitude. So, the big question is why that is and as is often the case the guidance seems to be the culprit. The guidance is honestly not awful at all. The company, however, has guided flat sequentially on total revenues which I think is not something that the markets want to see. Additionally, capacity growth will fall behind of total revenues and unit revenues are expected to decline 2 to 4 percent sequentially. While that is not awful, I'd think the market would have liked to see more reassurance that the revenue environment remains strong and in the guidance investors likely couldn't find any sign of that as the earnings per share also have been guided in the $2.20 to $2.50 range while Delta posting earnings of $2.68 in Q2 and unit costs are expected to taper year-over-year this quarter. We should, however, keep in mind that cargo revenues are expected to decline and overall there are better comparable year-over-year quarters that don't result in double-digit unit revenues for most end-markets going forward and primarily in the domestic market the recovery of capacity and industry constraints also is going to result in lower growth and perhaps even decline that will be offset in the long-haul segments. So, while unit revenues remain elevated, this is not necessarily a story any longer of throwing in capacity and raking in the extra revenues. Those familiar with the airline industry have likely also seen that pre-pandemic airlines would throw capacity on the market to compete thereby eroding unit revenues, and I think that is a fear that might now be affecting investors again even though unit revenues are still strong. While I still see strong growth on international and corporate travel with premium cabin product revenue growth exceeding main cabin and total passenger revenue growth, the question is also becoming whether the airline industry will be able to significantly reduce unit costs before unit revenues start to decline significantly.

Nevertheless, the company is also proactively working on longer-term savings and some immediate items. For instance, the recent undisclosed order for 12 Airbus (EADSF) A220-300s was disclosed as being a Delta order and that fits in the longer-term objective of making the fleet more efficient. Delta has already achieved a 6% reduction in its fuel efficiency and, as the company grows its next generation fleet, that number will obviously increase. That is already benefiting the company now, and those relative benefits will only grow. Furthermore, the company is swapping some Boeing ( BA ) 757 flights by Airbus A321neo flights which on the longer flights increase savings while the Boeing 757s will be used on the domestic network where revenues are becoming more challenging.

Furthermore, the company now expects earnings of $6 to $7 per share for this year up from the $6 guided during the Investor Day and the $5 to $6 per share guided earlier. That is also might be what kept the stock prices down as a guidance for $7 per share and $2.50 per share for the third quarter would suggest that the fourth quarter might be somewhat soft. So investors have to balance a strong second and third quarter with unit revenue headwinds and the implication of the current guidance for the fourth quarter, and they have done so with a flat performance for the stock following its earnings.

What Is Delta Air Lines Stock Worth?

{kind=link}

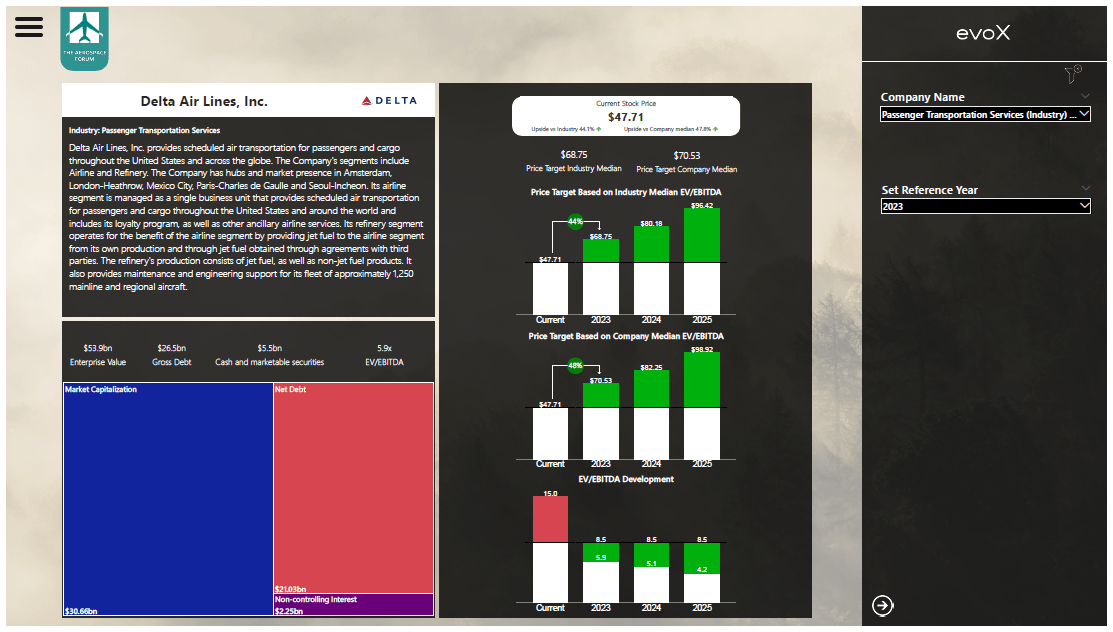

After going through the results and guidance, the big question of course is what Delta Air Lines stock is worth. Wall Street has a $58.58 median price target representing almost 23% upside. I ran the numbers using The Aerospace Forum's evoX Financial Analytics tools and our modeling shows that if Delta is able to perform as expected the company should be worth $68.75 to $70.50 per share, representing 44 to 48 percent upside coinciding with the high end of the range of expected by Wall Street analysts.

What Are The Risks For Delta Air Lines?

{kind=link}

Wall Street analysts see roughly half of the upside compared to what our model shows, so there could be some higher estimates on our side on the financial performance compared to the consensus. Therefore, it is also important to discuss the risks, and there certainly are risks ahead. While the company has been pointing at a supercycle for airlines as another $300 billion in airline revenues is still missing from the topline of airlines and air travel spendings as a percentage of GDP has yet to capture historic levels, there are also some potential weaknesses. Right now, I don't have any concern about demand. Demand is expected to remain high. My bigger concern is whether airlines will reach the desired capacity growth to meaningfully reduce unit costs excluding fuel before the unit revenues start to drop and significantly harm revenues. It is not something I expect any time soon as the industry remains constrained from the supply side, but it is a risk airline investors should keep in mind and it possibly warrants lower price targets than what I have modeled.

Conclusion: Delta Air Lines Stock Is At The Start Of A Growth Story

The Q2 results were good and enabled Delta to book the highest earnings per share, but we also see some market concerns in the unit revenue decline guided and the overall guidance as strong H1 results and a strong Q3 outlook make Q4 look somewhat soft. It is very well possible that the guidance will be hiked further, but at this point, unit revenues can make investors nervous. That is definitely a watch item, but the bigger picture shows Delta deleveraging, diversifying its revenue streams and building an even more fuel efficient fleet, and the results we saw in the second quarter and this year are actually just the start of Delta's growth story after the pandemic eroded earnings.

For further details see:

Delta Air Lines Stock: Strong Buy On Historic Earnings And Supercycle Growth