DLA - Delta Apparel: A High-Risk-High-Reward Turnaround Play I Would Avoid

2023-06-01 05:58:34 ET

Summary

- Delta Apparel faces a delicate situation with declining sales, high customer inventory, and weakened consumer purchasing power due to inflationary pressures.

- The company urgently needs to generate enough cash from operations to cover interest expenses and pay down some debt.

- The company plans to reduce its workforce and production capacity to address depressed profit margins and rising interest expenses.

- Investors with a high-risk appetite may consider Delta Apparel stock as a high-risk/high-reward turnaround play, but uncertainties in the macroeconomic landscape and potential recession pose significant risks.

Investment thesis

Delta Apparel ( DLA ) is currently in a very delicate situation, and this is reflected in the currently depressed share price. It seemed that sales were starting to recover in fiscal 2021 and 2022 after a few years of deterioration, and the share price reached a new all-time high as a consequence, but high customer inventory and weakened consumer purchasing power due to inflationary pressures are deteriorating sales again. In addition to declining volumes, higher production costs stemming from high inflation rates are producing a strong negative impact on profit margins, and to this must be added rising interest expenses and the growing concerns about a potential recession due to recent interest rate hikes.

As a consequence, the share price has plummeted by 72% from all-time highs reached in 2021, which reflects catastrophic expectations on the part of investors. Still, these headwinds, and even a potential recession, are directly linked to the current macroeconomic landscape, so, in my opinion, these are headwinds of a temporary nature. Furthermore, the company holds very high inventories, which the management intends to make use of by reducing production capacity. So I believe that even though this is a high-risk/high-reward turnaround play and the company has a balance sheet that should allow it to navigate the current complex macroeconomic landscape for quite some time, investors should avoid this company as interest expenses will certainly represent a serious problem in the future. Still, I will try to be as neutral as possible.

A brief overview of the company

Delta Apparel is a vertically-integrated apparel company that designs, manufactures, sources, and markets a wide portfolio of core activewear and lifestyle apparel products under the brands Salt Life, Soffe, and Delta. The company was founded in 1999 and its market cap currently stands at ~$68 million, employing around 8,600 workers worldwide. The company's products are sold through outdoor and sporting goods retailers, independent and specialty stores, better department stores and mid-tier retailers, mass merchants, eRetailers, the U.S. military, and through the company's digital platform. The company also owns branded retail stores across the United States.

Delta Apparel logo (Deltaapparel.com/Brand/Delta)

Insiders own 16.25% of the company's shares outstanding, which means they are the main beneficiaries of the good performance of the share price. The company does not pay dividends although it has historically rewarded shareholders through share buybacks, and the share price has shown strong volatility over the years, so I believe it is important to take advantage of economic cycles to buy low and sell high and thus get returns in the form of capital appreciation.

Currently, shares are trading at $9.71, which represents a 72.46% decline from all-time highs of $35.26 on May 18, 2021. This is a sharp drop caused by the fall in demand due to customer destocking and consumers' weakened purchasing power due to high inflation rates, although the increase in costs and interest expenses also play a fundamental role in the current situation of the company.

Net sales are weakening as demand is low

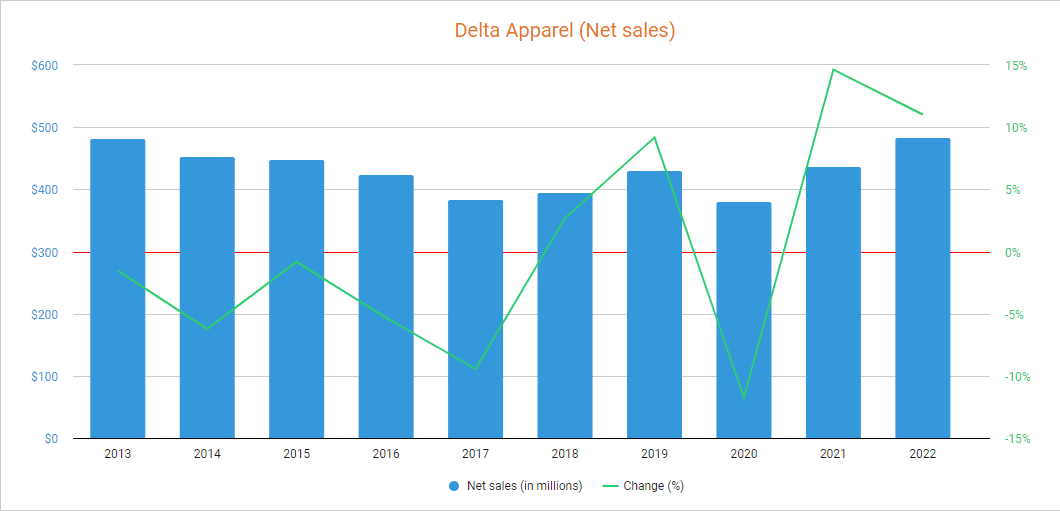

Before the coronavirus pandemic that took place in 2020, the company had been suffering a continuous deterioration in its sales, and although these began to improve in fiscal 2019 as they increased by 9.17% compared to 2018, net sales declined again by 11.74% in fiscal 2020 as a consequence of restrictions derived from the coronavirus pandemic crisis. Still, net sales have recently been recovering at a fast pace as they increased by 14.62% in fiscal 2021, and by a further 11.02% in fiscal 2022.

Delta Apparel net sales (Seeking Alpha)

{kind=link}

Now, high inventories within the mass and other retail supply chains and weakened purchasing power among consumers due to high inflation rates, as well as growing concerns about a potential recession, caused a net sales decline of 3.12% year over year during the first quarter of fiscal 2023 and a decline of 16.22% (also year over year) during the second quarter.

The company is currently opening new branded retail stores for its Salt Life brand, which is delivering very acceptable growth rates and profit margins, and plans to expand in the Northeast market later this year, specifically in New York and Virginia, with a total of 26 Salt Live retail stores in operation by the end of fiscal 2023. Furthermore, in March 2023, the company announced its expansion into the home furnishing market by launching a new home furnishings collection in its Salt Life brand.

The recent decline in the share price along with a much lighter drop in sales has caused a sharp drop in the P/S ratio to 0.148, which means the company currently generates $6.76 for each dollar held in shares by investors, annually.

This ratio declined by 75.97% from the 10-year high of 0.616 and is 55.56% lower than the average of the past 10 years, which shows the great pessimism among investors as they are placing much less value on the company's sales because for the company's situation to improve, profit margins have to improve significantly in the coming quarters, which will depend not only on the macroeconomic landscape but also on the management's ability to reduce the workforce sufficiently in order to profitably use its inventories.

Margins remain depressed and the company will likely need to take more debt

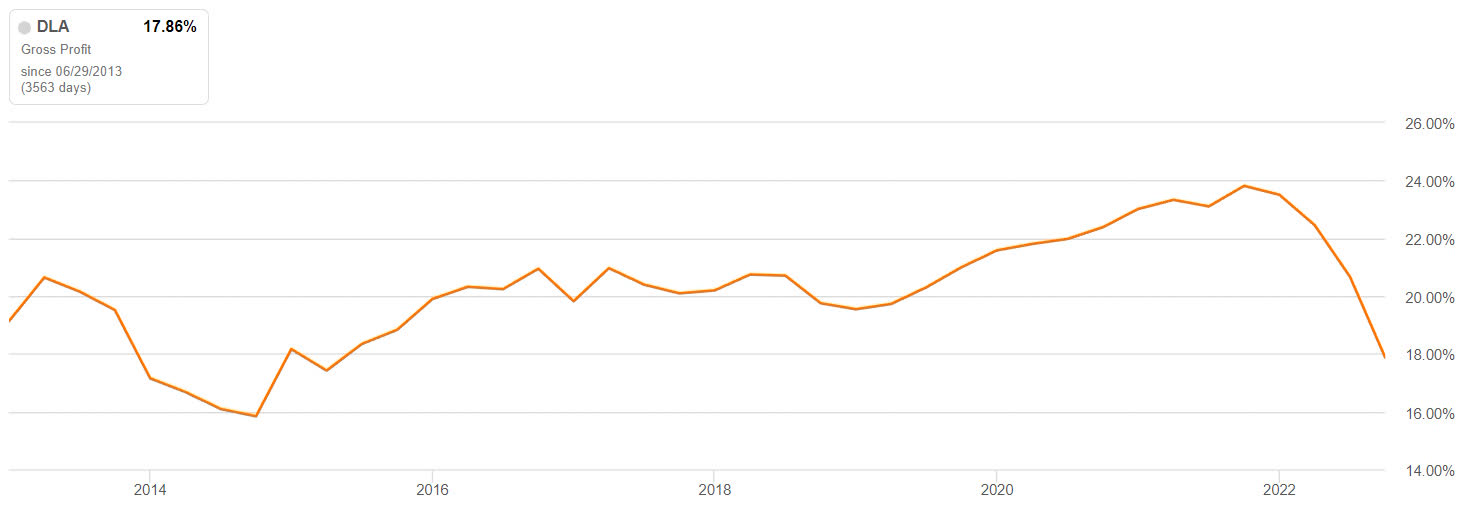

Overall, the company has remained profitable over the years thanks to positive gross profit and EBITDA margins, but the coronavirus pandemic crisis and the subsequent supply chain issues and inflationary pressures have caused disruptions in the company's operations in recent years. The company acquired Autoscale.ai in 2021 to provide automated solutions for design creation, art and licensing management, marketing spending, and seamless connectivity with various online marketplaces. The acquisition should drive some profitability in the long term, but ongoing inflationary pressures and declining volumes caused a significant decline in gross profit margins to 14.69% during the second quarter of fiscal 2023 while EBITDA entered again in negative territory at -1.41%, both far below current trailing twelve months' margins.

Delta Apparel gross profit margin (Seeking Alpha)

{kind=link}

In this regard, higher cotton prices and manufacturing facilities operating below full capacity and shutting down for longer times are the main causes of this recent margin contraction due to higher production costs and unabsorbed labor. This plunge in profit margins has caused a lot of pessimism among investors, and the management is reducing the workforce in order to reduce the cost structure of the company amidst weaker demand, which should help stabilize profit margins and get positive cash from operations by partially depleting inventories in the medium term. Furthermore, the Salt Life Group segment grew by 16% year over year during the second quarter of fiscal 2023 quarter and enjoyed very high gross margins of 59%.

Still, the good performance of the company will also depend on the improvement of the macroeconomic context, which makes this turnaround play a high-risk/high-reward one in my opinion, especially if we consider the company's debt pile is starting to become a serious problem. Fortunately, the company has ample inventories that it can draw on to try to generate positive cash from operations in the future, although it will most likely need to take some more debt as cash and equivalents is currently very low.

The balance sheet is weak, but high inventories should enable positive cash from operations soon

Due to increasing production costs and declining volumes, the company has had to borrow to continue producing, which has brought the long-term debt to $169 million. This poses a significant risk to the company as cash and equivalents is very low at $0.63 million, whereby the company will likely keep borrowing as long as margins remain depressed.

In addition to this, one of the aspects that investors should currently be most concerned about is the recent increase in interest expenses, which reached $3.72 million during the second quarter of fiscal 2023. This means that time is working against the company as the deterioration of the balance sheet as a result of depressed profit margins could continue causing further increases in interest expenses as the company may need to continue borrowing more cash.

The problem is that interest expenses of $14.88 million are very high if we take into account the cash that the company was able to generate before the current contraction in margins, and therefore, the company is currently in a very delicate situation from which it can only get out if it manages to drastically reduce the workforce and quickly empty its inventories to reduce its debt before interest expenses further deteriorate the balance sheet, and although it is true that this is a very plausible possibility, demand remains weak and a potential recession as a result of interest rates could cause another demand headwind for the company in the medium term.

But as a consequence of weak demand, inventories have increased significantly to $243 million as the company did not react in time to a weaker demand environment. Still, the management already reduced inventory levels by 6% since December 2022 thanks to operating manufacturing facilities below their full capacity while performing longer shutdown times, albeit at the expense of lower profit margins due to high unabsorbed labor. In this regard, the expected workforce reduction should allow the company to profitably empty its inventories and generate positive cash from operations in the medium term and maybe weather current headwinds and a potential recession, although the problem is in the speed at which it can do it and with what profit margins as demand is low while production costs are high, and the company needs to continue covering interest expenses.

Actually, it is normal for companies to be slow to react in times of sudden increases in production costs and lower demand, and a mismatch between production capacity and demand can happen and produce temporary negative cash from operations due to a rise in inventories. In fact, what makes this a risky investment is, in my opinion, the high level of debt of the company and the uncertainty of when the current macroeconomic situation will be reversed as time plays against the company due to interest expenses.

Share buybacks should not return in the foreseeable future

As the company does not pay dividends to its shareholders, it carries out share buybacks in order to reduce the total number of shares outstanding when operations allow it. This is a way of returning cash to shareholders as their positions passively grow over the years, and the company successfully reduced the number of shares outstanding by 11.63% in the past 10 years.

Still, the pace of share buybacks has come to a standstill since the outbreak of the coronavirus and is expected to continue like this for quite some time as operations are currently very weak amidst current inflationary and demand headwinds and growing concerns about the company's debt position and a potential recession.

Risks worth mentioning

Indeed, Delta Apparel is a company for investors with an appetite for risk as this represents a high-risk/high-reward investment, although I would like to highlight below those risks that I consider the most important to take into account.

- The company's greatest risk is in its debt position as interest expenses, which have reached $3.72 million during the past quarter, will be hard to cover once the company's operations improve.

- The company might have trouble reducing its inventories on time as customers also have high inventories. In order to produce cash from operations high enough to cover interest expenses and partially pay down the debt, production capacity would have to be drastically reduced, but inventories should also be quickly converted into cash, which is easier said than done.

- If inflation rates remain elevated, profit margins could remain depressed despite ongoing workforce reductions.

- Recent interest rate hikes to alleviate high inflation rates around the world could cause a global recession, which could have a further impact on demand. This would not only negatively impact sales, but also profit margins due to more unabsorbed labor.

Conclusion

Certainly, the situation is very delicate in Delta Apparel and only those investors with sufficient risk appetite should invest in this turnaround play. Time is currently playing against the company as interest expenses are skyrocketing and very low cash and equivalents suggest the company may soon need to borrow more cash in order to keep operating as profit margins are depressed due to high customer inventories (declining volumes) and rising production costs.

To address depressed profit margins and rising interest expenses, the management currently plans to reduce its workforce and continue to operate fewer hours per day in order to reduce its production capacity, and thus reduce its inventories, although this will not be an easy task as customers are also currently destocking its inventories. In this regard, I believe that although the management has a plan and ample potential to successfully navigate current and potential headwinds, high inflation rates and weaker demand (especially if a recession finally materializes), are largely out of its control and no one knows how long will they last.

For further details see:

Delta Apparel: A High-Risk-High-Reward Turnaround Play I Would Avoid