DLA - Delta Apparel: Affected By Demand Slowdown And Inflation

2023-03-27 05:28:53 ET

Summary

- Delta Apparel's stock price might have risen year to date, but its P/E ratio is still far lower than that for the consumer discretionary sector.

- Weak performance in the latest quarter, with shrinking sales and losses, indicates challenges for the company in this tough year for the economy, including in the stock market.

- However, its past performance is good, and its cost reduction initiatives can bode well for it in better times.

If there is any company that has been impacted by current macroeconomic conditions, the US based casual and athletic wear manufacturer Delta Apparel ( DLA ) would be it. In its recent results for the first quarter of the financial year 2023 (Q1 FY23) ending December 31, 2022, the company mentioned both rising costs, associated with persistently high inflation numbers and weakness in demand, which is also seen in subdued economic growth as an explanation for why its numbers have suffered.

What the stock movements say

However, that does not mean that the US-based company which manufactures blank apparel under the Delta Group and branded lifestyle apparel under the name Salt Life is an immediate no-go. A look at its trailing twelve months GAAP price to earnings (P/E) ratio shows that the number stands at 6.4x which is significantly lower than the 14.5x for the consumer discretionary sector as a whole.

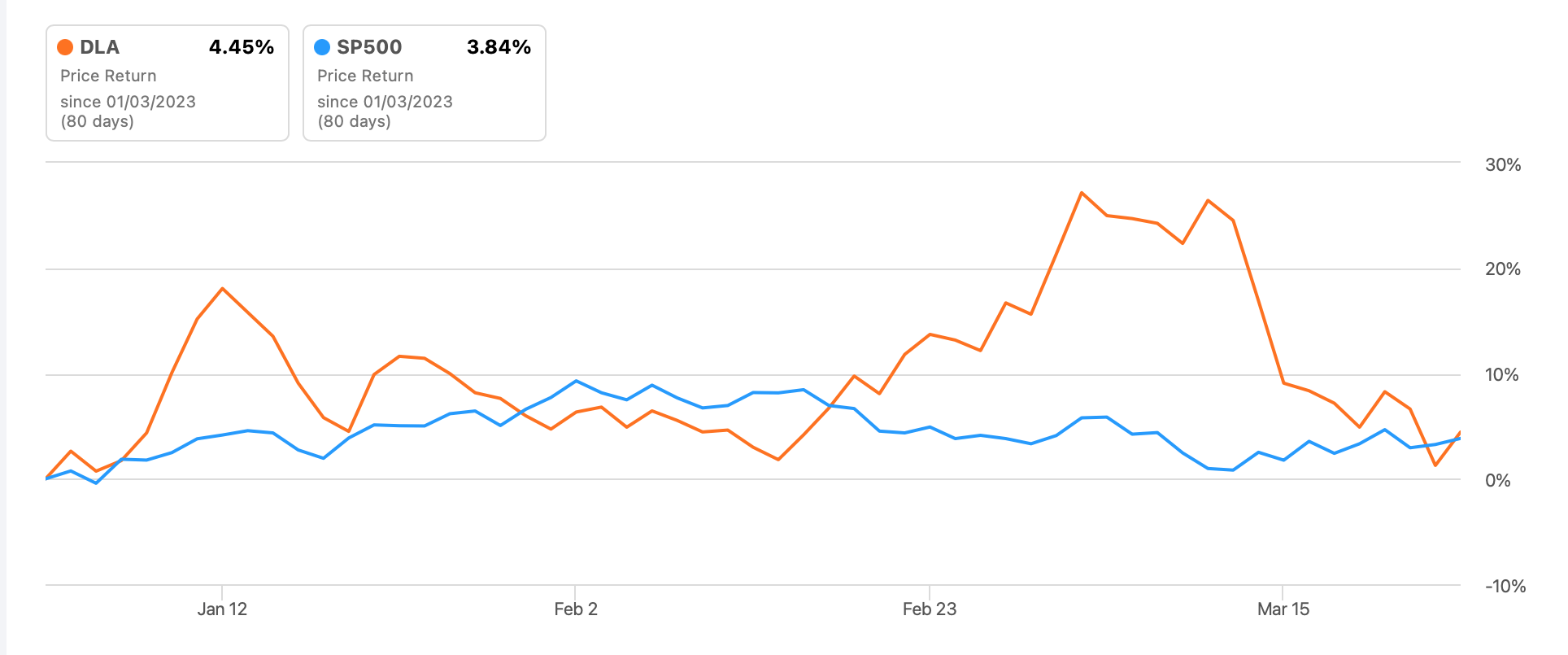

This indicates that there is a possibility that its stock price might have overcorrected despite the fact that it has actually risen year-to-date, by 4.5%, and by more than the S&P 500 ( SP500 ) (see chart below). But its performance is still underwhelming compared to the 9.65% increase in the S&P 500 consumer discretionary index. In fact, even over the past year, the stock has fallen far more dramatically by over 61% compared to the 24% drop in the sector index.

Price trends (Source: Seeking Alpha)

{kind=link}

Here I take a closer look at the company's financials to assess if there is a case for its stock price to rise in the future, considering its recent stock performance and low market valuation.

The company

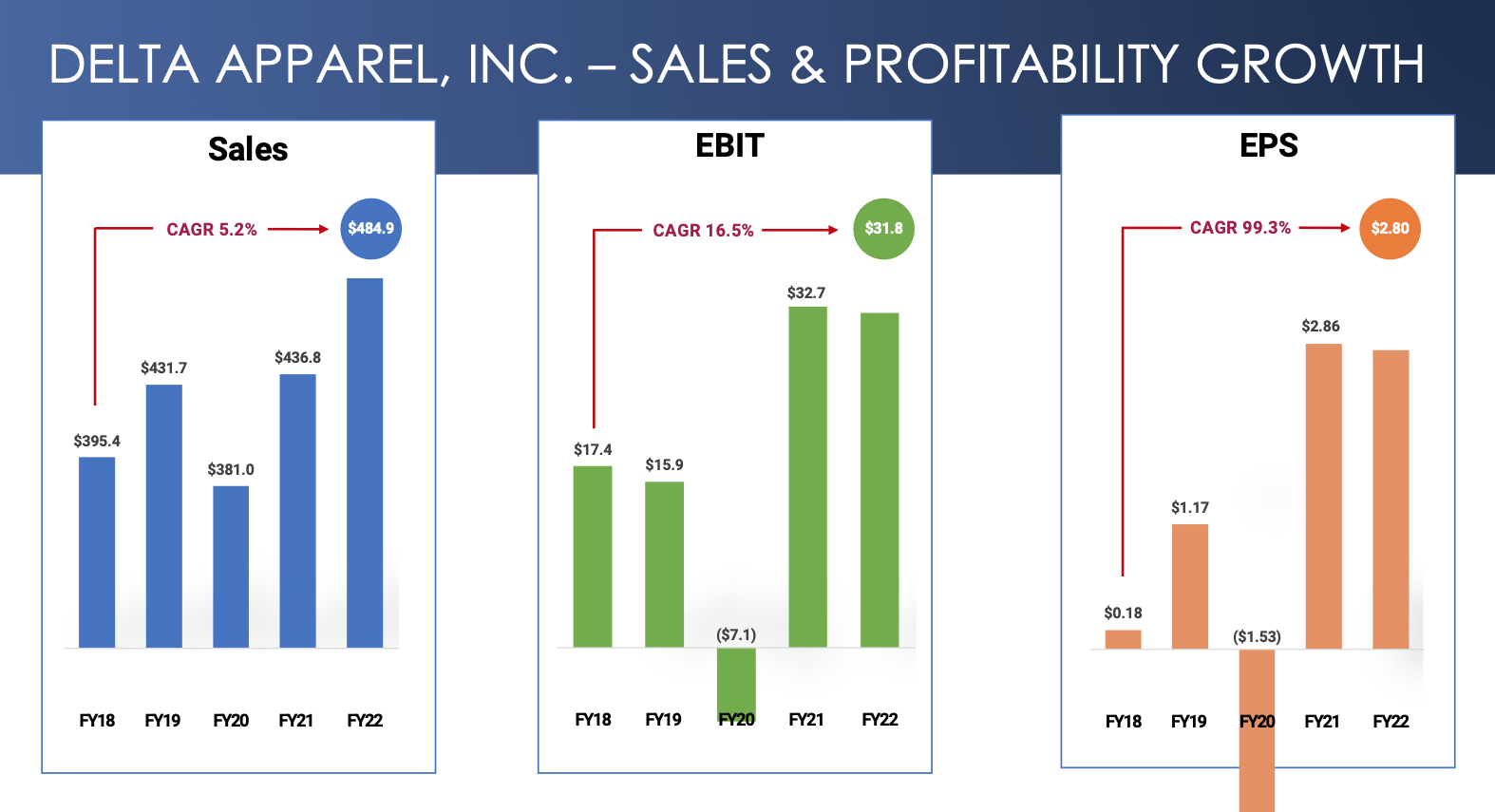

Delta Apparel functions in a growing market. The athletic wear market alone is estimated to be at USD 8 to 10 billion in the US and is expected to see 6% to 7% growth globally in the next decade. With an 11% growth in revenues for FY22, the company was clearly doing alright sales wise and was also profitable until recently. But clearly, this is not the whole story going by its recent stock price movements.

{kind=link}

Weak latest performance

A look at its latest earnings release gives some clues as to why that might be the case. In Q1 FY23, the company's sales declined by 3% year-on-year as demand fell for the mass retail supply chain. For context, 87.6% of the company's revenues came from its segment called the Delta Group, much of whose sales are derived from the wholesale business, with the remaining from its retail and e-commerce operations (see table below).

{kind=link}

By contrast, however, its direct-to-garment printing business DTG2go and Salt Life brand saw good growth during the quarter, increasing by 20% and 17% respectively. Growth in Salt Life is particularly encouraging. While it is still a small part of the company's overall revenue, with a 12.4% share, it is not trivial either. The positive impetus provided by these segments, however, was clearly not enough to result in growth in overall sales.

At the same time, a rise in costs was driven partly because of new store openings but also because the increased cost of labour and raw materials like cotton shrank its profits. Its gross margin fell sharply to 12.7% from 20.8% at the same time last year. It also fell into an operating loss.

Potential positive developments

Going forward, however, there could be some turnaround in the company. For one, as inflation comes off as widely expected, through the course of 2023, its cost numbers could look better, which could help its profitability. Also, the company has planned a series of initiatives that could also improve its financials, both by reducing costs and increasing revenues.

In terms of cost reduction, Delta Apparel plans to reduce its dependence on externally sourced textile fabrics and scale existing facilities. It also plans to shift part of the production from Mexico to Central America. Improved labour efficiency is also on the cards, which can lead to increased production at little extra cost. These are expected to result in savings of up to USD 6 million a year, which is about 7.4% of its operating costs as of FY22.

Increasing pricing for print services and blank garments, another of its initiatives, can help in both passing on costs to customers and increasing revenues. Delta Apparel's objective to reduce inventory is also notable, considering the 41.4% increase in inventory levels seen in Q1 FY23 from the same quarter last year. This is particularly important as its quick ratio looks stretched at 1.9x. It was already high, to be sure, in Q1 FY22, but less so at 1.4x.

Stock assessment

These figures indicate why Delta Apparel is not exactly a favourite among investors right now. Falling sales, losses and rising inventories make it look risky at this time. Even then, its 6.4x P/E ratio, despite its reporting losses for two quarters running now, looks quite low. Its price-to-sales (P/S) at 0.2x compared to the sector's P/S at 0.8x is also competitive. But then again, for all the wrong reasons.

What next?

I do believe that there is potential for the company to perform better during improved macroeconomic conditions. Its last year's results indicate as much. Further, despite increased debt, its balance sheet looks alright, too. In fact, if there was another stock market upswing on improved inflation or growth numbers, I would not be surprised if the stock ran up based on expectations. But 2023 is hardly the year when we can depend on sustained improvement in the economy. If anything, it is shaping up to be quite the opposite. Risks of recession are rising and while inflation is coming off, it remains to be seen when the interest rate hikes will cease.

For now, I would hold off from buying the stock. But it is not a sell either; in other words, it is not a lost cause, just a company going through a hard time as of now. It is a wait-and-watch.

For further details see:

Delta Apparel: Affected By Demand Slowdown And Inflation