DMTK - DermTech: Intriguing Product Tough Market. Pivotal Year Ahead!

2023-04-14 15:21:48 ET

Summary

- DermTech has designed a non-invasive sticky patch to test for melanoma.

- The product is potentially cheaper than current standards of care and more accurate.

- DermTech sees its patch as targeting a ~$2.5bn market and is targeting an annual revenue opportunity of >$300m.

- In reality, revenues last year were just $14m, and billable sample volume and ordering clinician growth has slowed.

- Despite an apparently strong product, losses of >$100m in 2022 are unsustainable - the company needs to quickly find a new CEO, and a commercial partner if it is going to succeed.

Investment Overview - DermTech's Low Key Listing

DermTech (DMTX) is - at the time of writing - a $131m market cap medical technology company that describes itself as follows in its 2022 10-K Submission (annual report).

We are a molecular diagnostic company developing and marketing novel non-invasive genomics tests that seek to transform the practice of dermatology. Our platform may change the diagnostic paradigm in dermatology from one that is subjective, invasive, less accurate and higher-cost, to one that is objective, non-invasive, more accurate and lower-cost.

DermTech joined the Nasdaq in September 2019 via a business combination with Constellation Alpha Capital Corp. ("Constellation"), a publicly traded special purpose acquisition company ("SPAC"). The company had planned an IPO as far back as 2014, but ultimately withdrew citing "poor market conditions".

Being a small company, a SPAC listing was likely the only way DermTech could gain access to the public markets. SPAC's are set up to have no underlying business model but sufficient funds to complete a listing, after which their stock price is set at $10 and they have up to 2 years to find a suitable company to merge with or acquire.

A popular and light touch (from a regulatory perspective) way for smaller companies to access the markets, SPAC's however have generally delivered very poor returns for investors. In February, I assessed the performance of 28 SPAC listed biotech companies and found the average return on investment across the prior 12-month period was -51%, with 24 of 28 companies experiencing losses, 15 of which experienced losses >80%.

DermTech stock is down >75% since its 2019 listing, trading at $4.3 per share at the time of writing (the company completed a 2-1 reverse stock split immediately after the merger concluded). The company only raised $29m through the SPAC merger, although according to a press release:

Participating investors included experienced life sciences investors such as RTW Investments, HLM Venture Partners, Irwin and Gary Jacobs, the founding family of Qualcomm, Inc., and two institutional investors each with over $10 billion in assets under management.

The Elevator Pitch - Disrupting the Melanoma Testing Industry

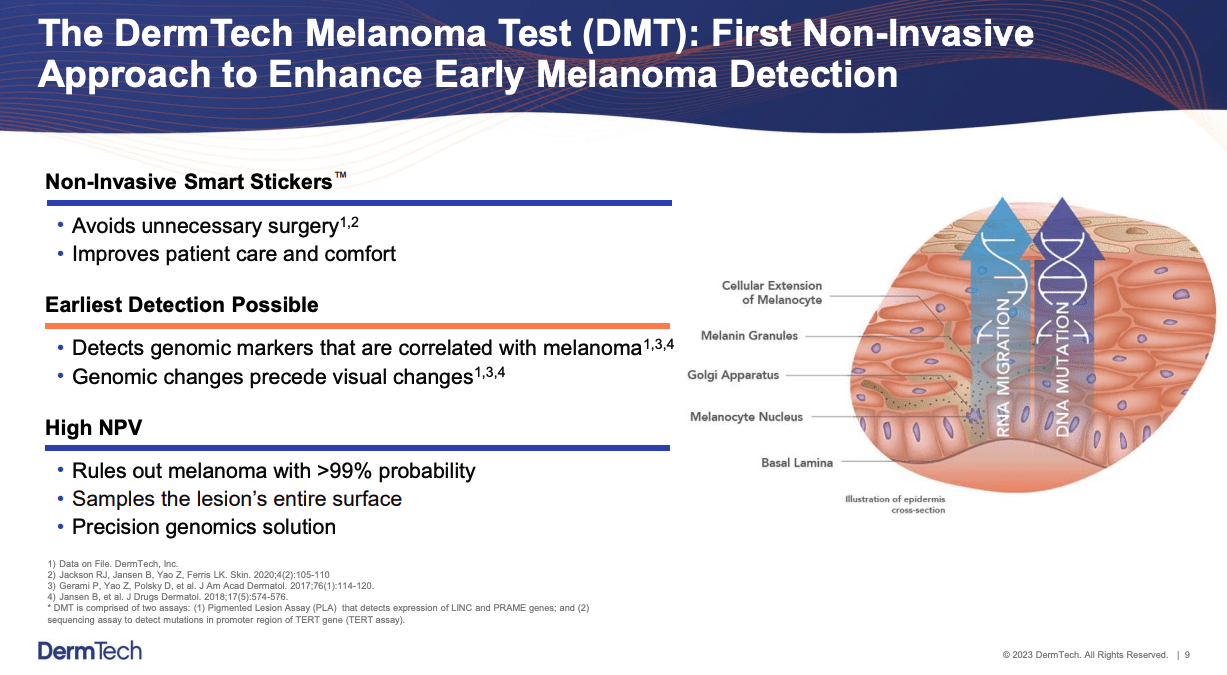

DermTech may be small however the company has some big ambitions for its practically unique, non-invasive smart stickers designed to enhance early melanoma detection.

DermTech Melanoma Test Overview (DermTech presentation)

{kind=link}

As we can see above, DermTech says that its stickers have "greater than 99 percent negative predictive value" adding that they represent:

an easily and non-invasively way to collect skin samples, in contrast to the existing standard of care of using a scalpel to biopsy suspicious lesions.

The company's 2022 10-K goes on to elaborate:

Current dermatologic diagnosis is primarily based on subjective visual assessments and subsequent surgical diagnostic procedures. This legacy paradigm is prone to error and results in a substantial number of unnecessary and invasive surgical procedures.

Our platform provides a non-invasive alternative that minimizes patient discomfort, scarring, and risk of infection. Further, because our testing results utilize genomic analysis, we provide more accurate, objective diagnostic information than the currently prevailing diagnostic procedures.

It sounds like an attractive option for a patient, who can briefly apply the sticker which "gently lifts skin cells off the surface of your mole" (source: website) and is then analysed at DermTech's CLIA-licensed, 9k square foot laboratory in the State of California, which has capacity to carry out 150k tests per annum, according to an investor presentation . Test results arrive within 5 business days, DermTech says.

Less invasive and inconvenient than using a scalpel, DermTech's stickers - which are called DermTech Melanoma Tests ("DMTs") - may be significantly more accurate, and cheaper than current methods, according to a study published in Journal of the American Medical Association ("JAMA"), which concluded:

In this cost-savings analysis of the pigmented lesion assay using model inputs for patients with pigmented lesions suggestive of melanoma, a $447 (47%) cost reduction per assessed pigmented lesion vs the current histopathologic standard of care was achievable if the assay was priced at $500. Savings were driven by reduction in initial biopsies and excisions and reduced stage-related treatment costs from missing fewer melanomas.

Pigmented Lesion Assay ("PLA") was the original name of DermTech's product before a second generation product was released in 2021. The original was designed to detect expression of the LINC00518 ("LINC") and preferentially expressed antigen in melanoma ("PRAME") genes using a nucleic acid amplification process called reverse transcription-polymerase chain reaction ("RT-PCR"). The newer version is additionally designed to identify the presence of mutations in the TERT gene promoter region using DNA sequencing.

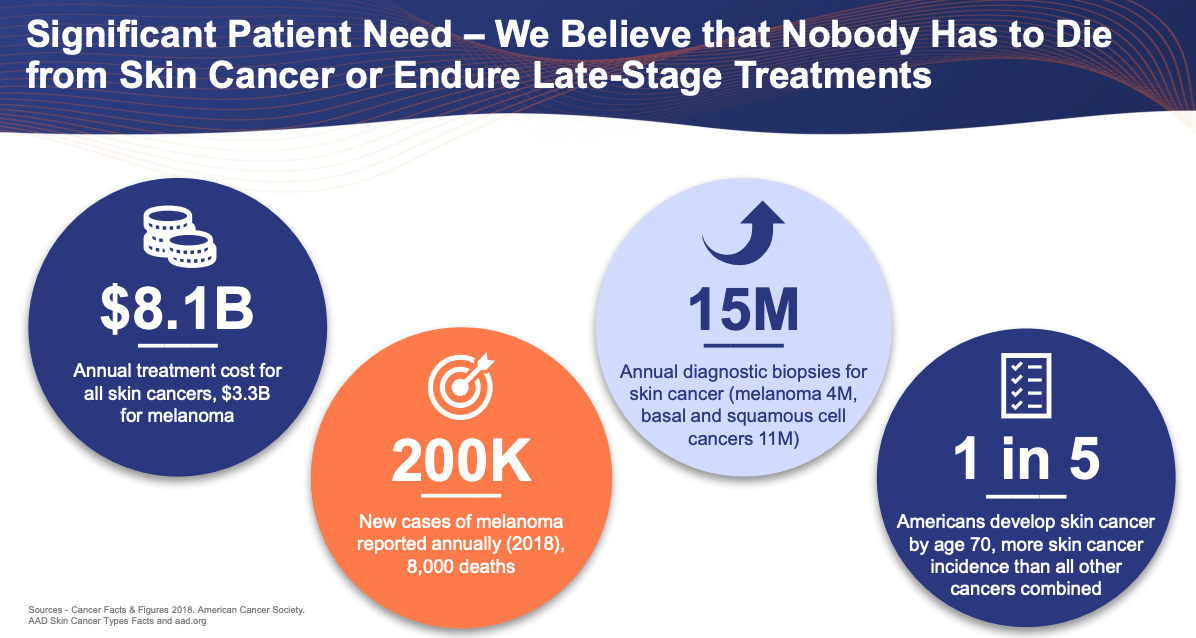

Melanoma detection overview (DermTech presentation)

{kind=link}

As we can see above, melanoma is a serious problem in the US, with ~200k cases reported annually, and 8k mortalities, with treatment costs rising >$8bn per annum.

DermTech maintains that its technology reduces the probability of missing melanoma to <1%, versus current standards of care which have a probability of missing a diagnosis of 11-17%, studies show, and reduces the number of surgical biopsies required for a diagnosis by 5 - 10x, whilst it also:

improves the positive predictive value ("PPV") approximately five-fold (from 3-4% with the current surgical techniques to 18.7% with DMT without TERT assay)

Theoretically, then, we could speculate that at full capacity and at $500 per DMT, DermTech has an earning potential of ~$75m per annum, but actually DermTech management is thinking of much bigger numbers.

The Market Opportunity - Theoretical versus Reality

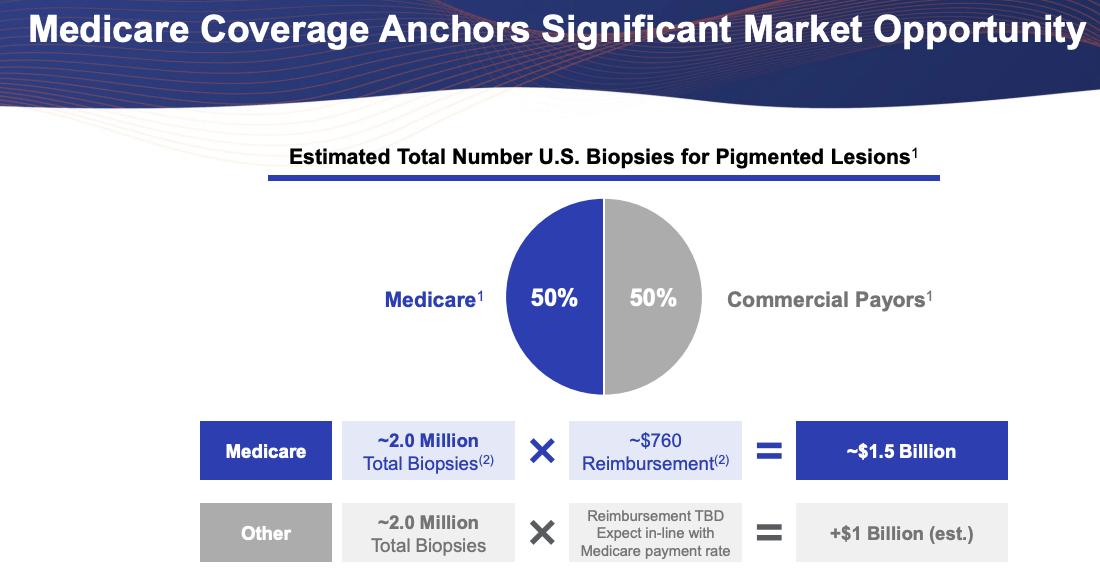

First of all, it is absolutely key that DermTech can secure reimbursement from health insurers for its testing.

market opportunity Medicare + Other (DermTech presentation)

{kind=link}

As we can see above Medicare alone offers a market of ~2m biopsies per annum that DermTech believes, based on ~$760 of reimbursement, is worth as much as $1.5bn per annum, whilst dealing directly with commercial payors could offer another blockbuster (>$1bn per annum) opportunity.

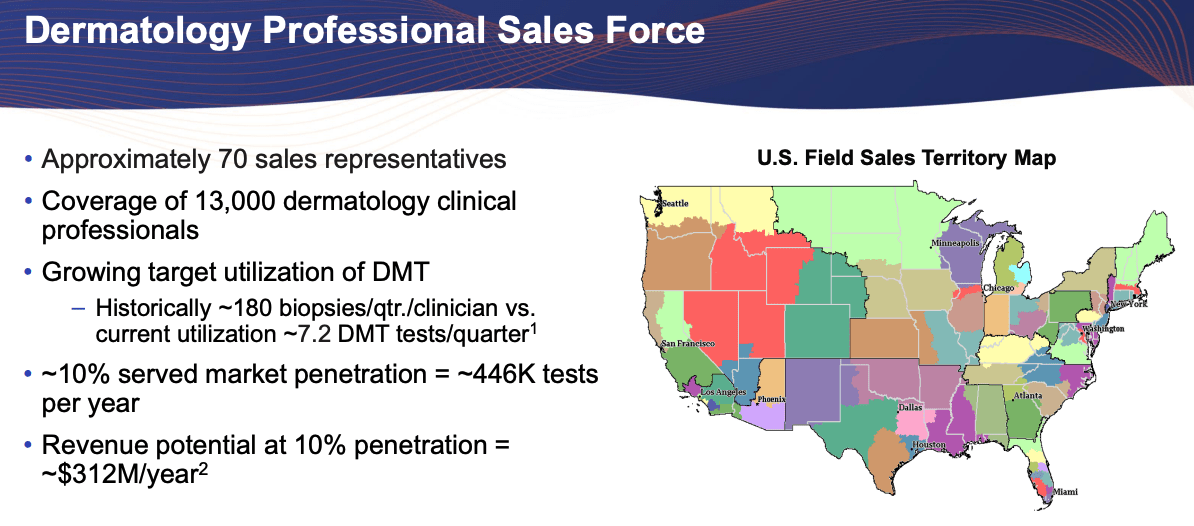

DermTech current revenue opportunity (DermTech presentation)

{kind=link}

DermTech has already built a sales force of ~70, which, as shown above, management believes can generate revenues of ~$312m per annum based on 10% market penetration, and a price of $700 per test. $312m is more than 2.5x current market cap valuation, so clearly, if management hits these kinds of numbers, provided bottom line losses are either narrowing significantly or non-existent, you would expect DermTech's valuation to soar.

Now let's consider FY22 earnings released on March 2nd:

DermTech FY22 earnings (Seeking Alpha)

We can see that management has a long way to go to achieve some of its goals. First of all the average selling price is presently ~$202, which is some considerable way below the $700 per assay figure management is chasing. This figure also declined in 2022, which is a concern.

According to a DermTech statement in its 2022 10-K submission:

In late October 2019, the American Medical Association provided us with a PLA Code. Pricing of $760 for the PLA Code was published on December 24, 2019 as part of the Clinical Laboratory Fee Schedule for 2020.

DermTech therefore concludes that:

With Medicare coverage granted, we have the opportunity to approach commercial payors, and as a result, we believe that the DMT may generate significant revenues in the future.

This might suggest that a >$700 dollar reimbursement fee for each assay is possible, but DermTech states just a couple of paragraphs later that:

Because each payor generally determines for its own enrollees or insured patients whether to cover or otherwise establish a policy to reimburse our tests, seeking payor approvals is a time-consuming and costly process.

We cannot be certain that coverage for our current tests and our planned future tests will be provided in the future by additional commercial payors or that existing policy decisions or reimbursement levels will remain in place or be fulfilled under existing terms and provisions.

DermTech says that presently it collects the vast majority of its revenues - £13.79m in FY22 out of total revenue of $14.5m in 2022 - via assay revenues, which it defines as follows:

The Company generates assay revenue from its DermTech Melanoma Test it provides to healthcare clinicians. The transaction price is the amount of consideration that the Company expects to collect in exchange for transferring promised goods or services to a customer, excluding amounts collected on behalf of third parties.

In other words, DermTech drives revenues via direct sales contracts, as opposed to reimbursement deals, and not seem to have its reimbursement business up and running yet. Although the latter route to market offers a potential reimbursement per test of >$700, at present, there appear to be no - or very few - organisations willing to accept this contract.

Secondly, revenue of $13.7m from assays in 2022 represents ~4.3x less than the sales and marketing spend. Granted, the market opportunity is large enough that investors would expect losses to be heavy in the early years as the company ramps up marketing and production, but it should also be noted that DermTech reported a net loss of $111.7m in FY22, and in its investor presentation, the company reports a year-end cash position of $130m.

In other words, if 2023 performance is anything like 2022, then DermTech will need to raise significant funds - probably diluting shareholders in the process - just to avoid going bankrupt.

2023 and Beyond - Can DermTech Achieve Its Goals In Dermatological Testing

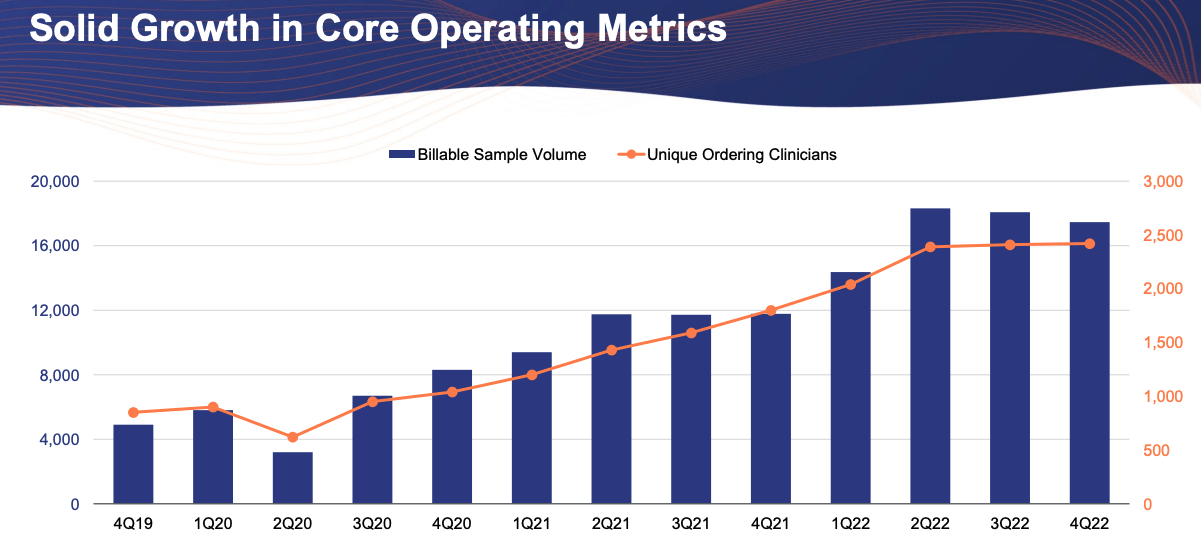

It seems as though growth has been slowing at DermTech, with billable sample volume and unique ordering clinician numbers falling and stagnant respectively across the past few quarters, and the reimbursement aspect of the business failing to take off so far.

performance in core operating markets (investor presentation)

{kind=link}

Despite the apparently obvious benefits of DermTech's lead product, there are clearly some tricky obstacles to growth in DermTech's markets, or management has simply not been executing well, which may explain why the company announced - alongside its FY22 earnings - that company President, CEO and Director Dr. John Dobak will step down from his role as CEO, with no successor having yet been appointed.

DermTech is apparently struggling to convince insurers to reimburse for its products - the company admits as much when stating in its 10-K that:

We believe we will achieve successful coverage outcomes from these efforts over the next 12 to 24 months, although no assurances can be given that any reimbursement coverage approvals will be obtained.

This could be either because payors are not yet aware of the product, or because they continue to favour standards of care (or cannot get out of contracts signed with existing standards of care). At the same time, DermTech may be struggling to market its products to direct buyers - telemedicine channels have proven to be neither popular or lucrative, despite attracting a great deal of hype, especially around the pandemic.

These 2 issues are hard to solve without plenty of funding being available - a luxury that DermTech does not have at present - to spend on sales staff and marketing. An optimal scenario would be for DermTech for find a commercial partner with deep pockets that can help push DMTs towards the mainstream. The question may be why this has not already happened, given DermTech has been around for over a decade.

It could be that DermTech's product is not quite as unique or effective as the company makes out, although from a layman's perspective it appears to be an improvement on current standards of care.

This point is also reflected by the fact that, back in late 2020, DermTech stock surged as high as $80 per share, apparently on positive news flow such as the positive medical benefit verdict reached by Geisinger Health in relation to the PLA system, an agreement reached with Blue Cross Shield for its Commercial and Medicare Advantage membership, and the fact that the National Comprehensive Cancer Network (NCCN) had recommended DermTech's patch for melanoma.

It's not clear why all of this momentum seems to have been checked, but DermTech does comment in its 10-K that:

With Medicare and TRICARE coverage (for DMT without TERT assay), Veteran Affairs coverage (for DMT), contracts covering the DMT (without TERT assay) with 6 out of 10 insurers associated with the Blue Cross Blue Shield Association ("Blues plans"), plus a favorable policy of the DMT (without TERT assay) with the second largest lab benefit manager in the United States, and increased test volume, we believe the DMT (without TERT assay) is being reviewed for coverage by additional large commercial payors.

Perhaps DermTech shareholders simply need to be more patient, and once the product receives more widespread coverage and awareness increases, the revenues will begin to accelerate.

Conclusion - DermTech Is Either A Contract Win Away From Doubling Its Share Price, Or A Year Away From Bankruptcy

2023 feels as if it could be a "make or break" year for DermTech. Clearly, the company has been able to generate optimism in the market for its unique product in the past, and a superficial review of the product seems to suggest that it could still benefit hundreds of thousands, if not millions of people.

Balanced against this however is a the reality that the product is not selling very well (some 3 years after DermTech listed on the Nasdaq) and funds are beginning to run low.

My conclusion in relation to DermTech is therefore that if the company cannot find a commercial partner, a smoother path to reimbursement with a much higher average selling price in play, or a fresh source of funds this year its share price may continue to decline. DermTech notes a handful of small company competitors in its 10-K submission, and states that:

In general, medical devices have capital equipment costs and maintenance requirements, do not integrate well into clinical practice, and do not have clear mechanisms to provide physician payment.

My suspicion is however that somewhere or somehow DermTech's product or business model may be flawed. Perhaps the testing process is too expensive, or possibly DermTech's criticism of the current market standard is overblown. There is too large a discrepancy between current earnings figures and management's ambitious goals to convince me that there are no underlying flaws.

With all that said, DermTech could be one of those rare gem-like companies that are hiding in plain sight, waiting for a larger company to see the logic in their product. Perhaps the business model and product are sound, and all that is required is a cash injection, better marketing, and an experienced Pharma partner.

Back in July 2021 I covered a company of similar size, with a similar product - a wearable patch to aid people with diabetes. Since my bullish article however Nemaura (NMRD) stock is down >90%, however, therefore I will remain firmly on the sidelines with DermTech.

I hope this post has at least alerted some readers to an apparently exciting opportunity to improve melanoma testing - an area where there is unmet need and where current standards of care may not be completely adequate.

From a prospective investors' perspective, I would be looking out for evidence that commercial payors are genuinely willing to embrace DermTech's products at a higher price point, and this can likely be tracked when Q123 earnings become available - management will doubtless acknowledge any progress, and provide an updated ASP. I would also pay close attention to the search for a new CEO.

When medical device specialist iRhythm Technologies (IRTC) was struggling with changes to reimbursement policies that threatened to slash the average selling price of its heart monitors in 2021, for example, the company appointed a new CEO, Quentin Blackford, who had formerly worked at Dexcom, where he played a key role negotiating reimbursement deals.

I wrote about iRhythm at the time, suggesting that fixing the reimbursement issue could fix the share price, and that is precisely what happened - the share price is up >100% since my note, after the punitive new reimbursement measures were ultimately not enforced.

For further details see:

DermTech: Intriguing Product, Tough Market. Pivotal Year Ahead!