AMZN - Designer Brands Is Not A Fashionable Buy

2023-09-01 07:30:04 ET

Summary

- Designer Brands Inc. operates as a popular retailer of footwear and accessories, with a market cap of $688.33M, but the stock is down 37% over the last year.

- The company has seen a 12% increase in share price YTD and has room to expand its significant market share in the U.S. footwear industry under certain conditions.

- There are a slew of risks retail value investors ought to consider since we assess the stock to be a Hold at the current time.

The Affirmatives

Designer Brands Inc (DBI) operates as a popular retailer under names like DSW Designer Shoe Warehouse, The Shoe Company, and DSW. It is one of the largest designers, manufacturers, and retailers of footwear and accessories. A great deal of gravitas is riding on the next earnings announcement expected on September 7, 2023.

The share price is up YTD, we think primarily, because of an announced buyback program, in anticipation of a higher EPS than last quarter, and global footwear consumption is set to increase this year and next. We suggest investors sit tight, accentuate the positive, eliminate the negative, and latch on to the affirmative if interested in a long-term investment. We rate the stock a Hold in the near term but find it attractive.

Some affirmative factors underpinning our positivity about Designer Brands include

- YTD the shares are up ~12%, in part, because in June '23 the company announced a buyback of shares up to $100M.

- Sentiment seems to be favorable with bloggers turning more bullish about Designer Brands.

- Designer Brands has room to grow market share with its market power; its market cap is $688.33M in a $88.5B U.S. footwear industry expected to have an annual global growth rate of 3.47% CAGR for 2023 through 2028.

- Corporate insiders made 11 open market buys and 4 sells in the last three months; more shares were bought than sold.

- Hedge funds bought nearly 600K shares in the last quarter when the price tumbled; it was +$15 in November '22 down to less than $7 in June '23.

- There is a new CEO at the helm and another named in July as president of DSW Designer Shoe Warehouse responsible for stores and e-commerce development.

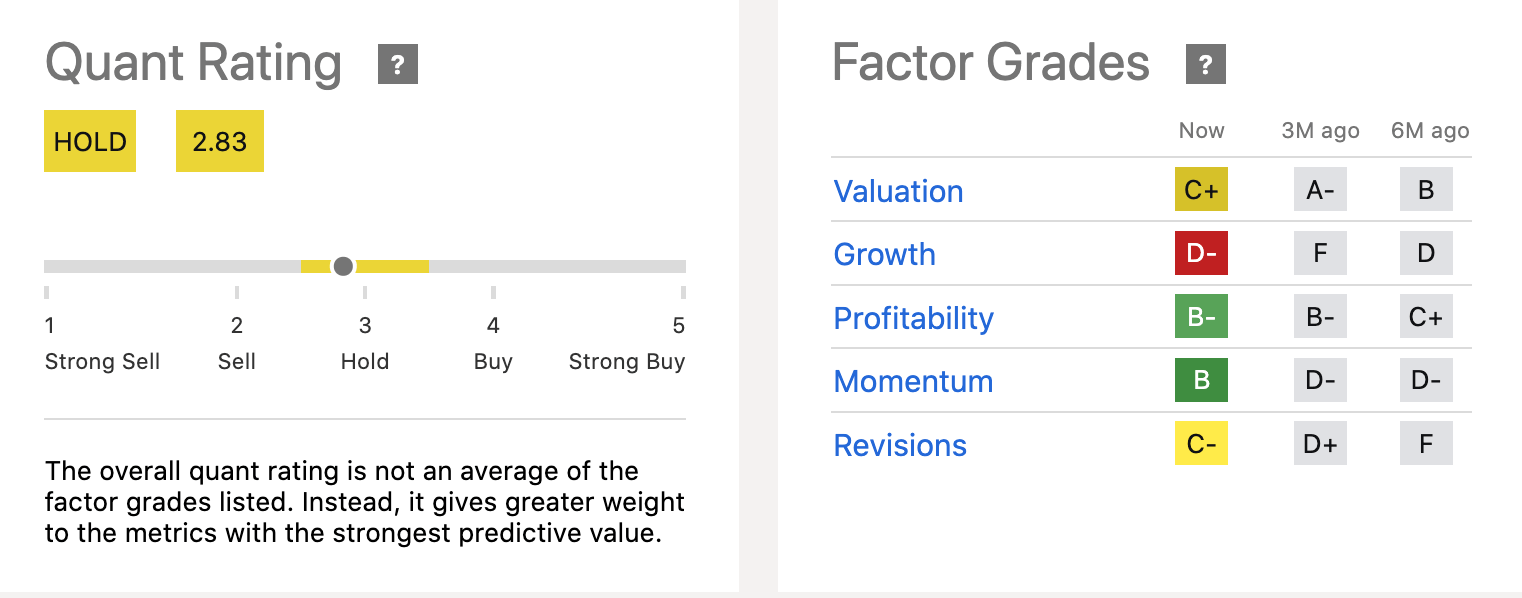

- Seeking Alpha's Quant Rating recently moved from a year-long Sell rating to a Hold.

Retail value investors are going to be presented with a better opportunity to enter the highly competitive footwear and accessories investment market if the Designer Brands share price slips after the next earnings announcement.

Closer Look

The stock is covered by a few Wall Street analysts. Nine Seeking Alpha analysts wrote about the stock over the last 18 months. Seven were positive, rating it a Buy and 2 a Hold. Seeking Alpha's Quant Rating assessed the stock as worth a Buy rating through 2022; since the fall of 2022, SA dropped its Quant Rating to Sell. In August, after the share price began to tick up, SA upgraded its assessment to Hold despite the stock being tagged with lower Factor Grades for valuation and growth. Suspicions for better profitability and greater momentum seem to be defining a more positive outlook.

{kind=link}

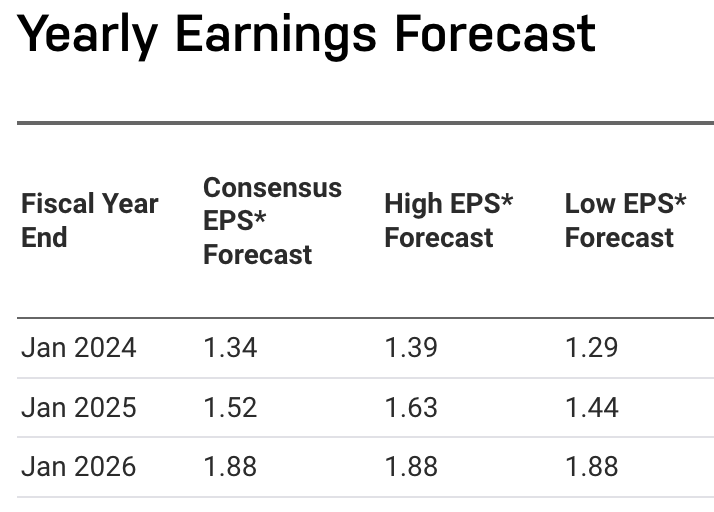

The stock is -37.4% over the last year. Despite store traffic increasing 22% in FY '22, net sales in Q1 '23 fell 10.7% Y/Y, and gross profit, and gross margin both were lower; the EPS was 12.5% lower than analysts' estimates . Yet, the quarterly EPS of $0.21 reported in June 2023 compared favorably to the $0.07 EPS reported in January '23. Last year's second-quarter EPS was $0.62. NASDAQ.com forecasts increased EPS each year through 2026:

{kind=link}

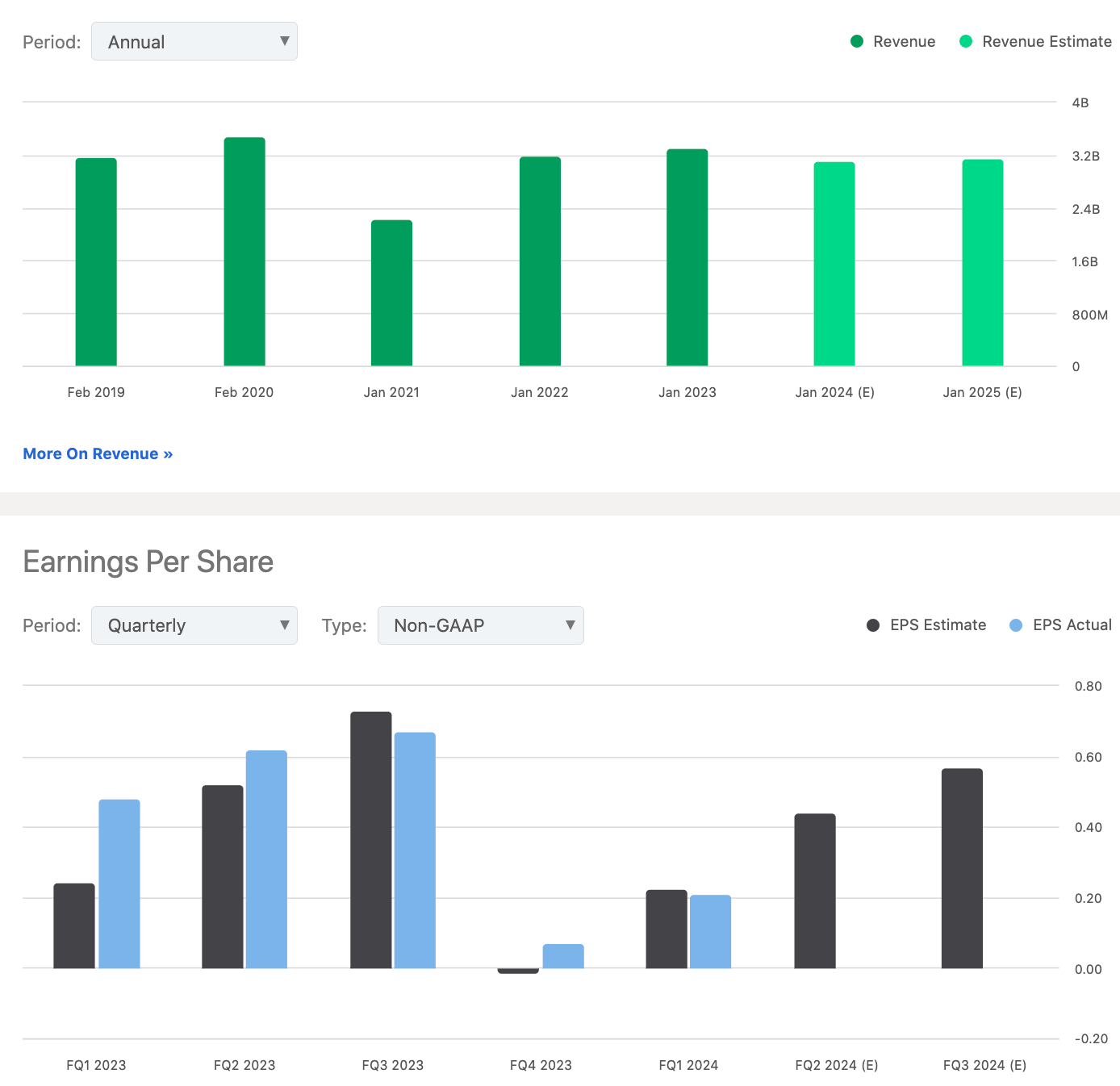

We expect Q2 '23 to be reported 30% lower than last year's perhaps in the low to mid-$0.40 per share but that is more than twice the $0.21 EPS reported last quarter. In other words, the trend is positive. Revenue was up each of the last three years, as were quarterly earnings.

Revenue & Earnings Designer Brands Inc.

{kind=link}

Designer Brands Inc.'s focus is on brand building, according to the new CEO much of it through acquisitions. The company bought Keds, Le Tigre, and Topo Athletic to fuel growth the CEO told shareholders in June. It bought 5 companies, 3 in the last 5 years, 60% in footwear and apparel and consumer products.

Risks

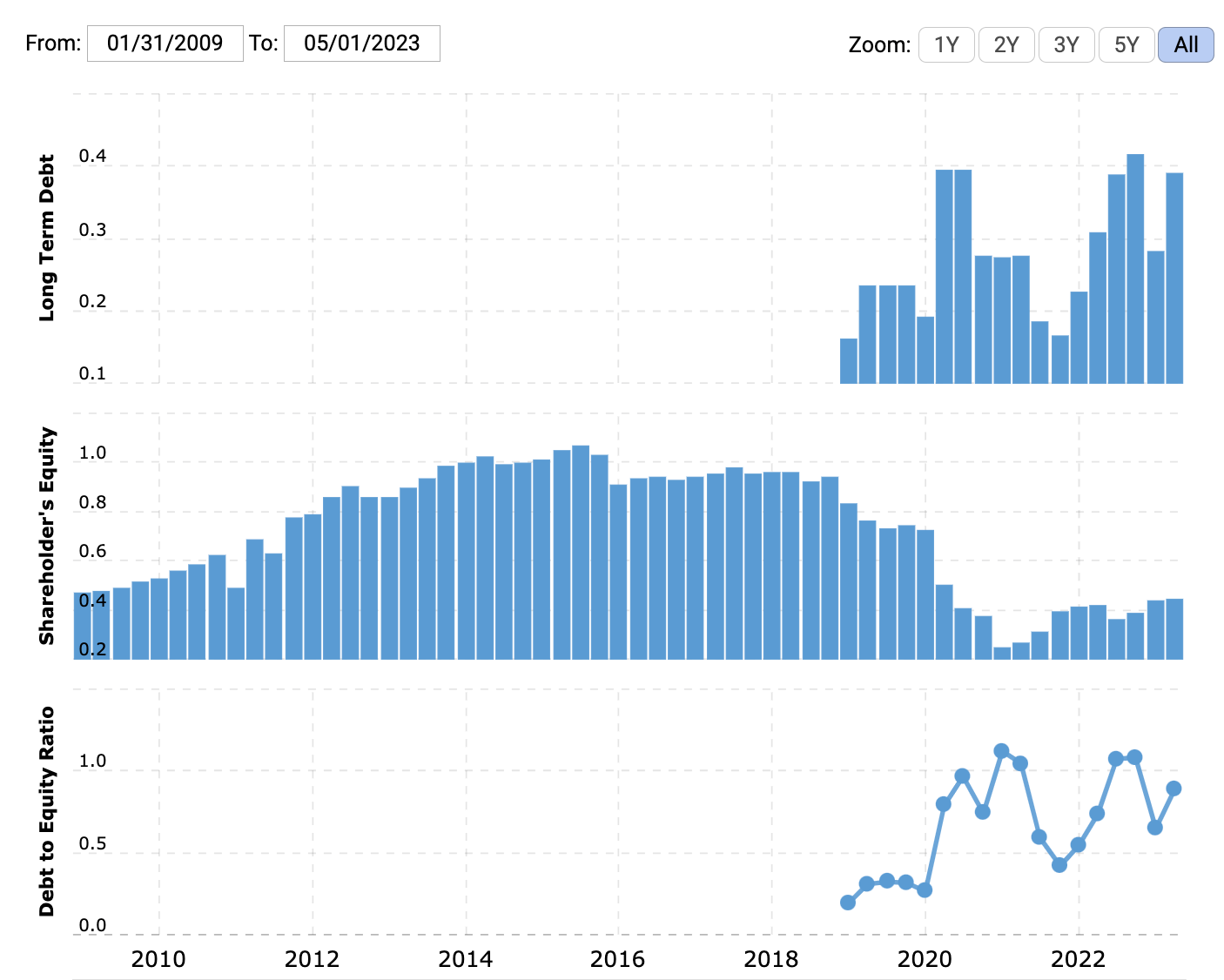

Somewhat worrisome is that in Q1 '23 cash and equivalents fell 10% from $54.8M in Q1 '22 to $50.6M. Debt rose to $390.9M at last report from $306M for the first quarter last year.

{kind=link}

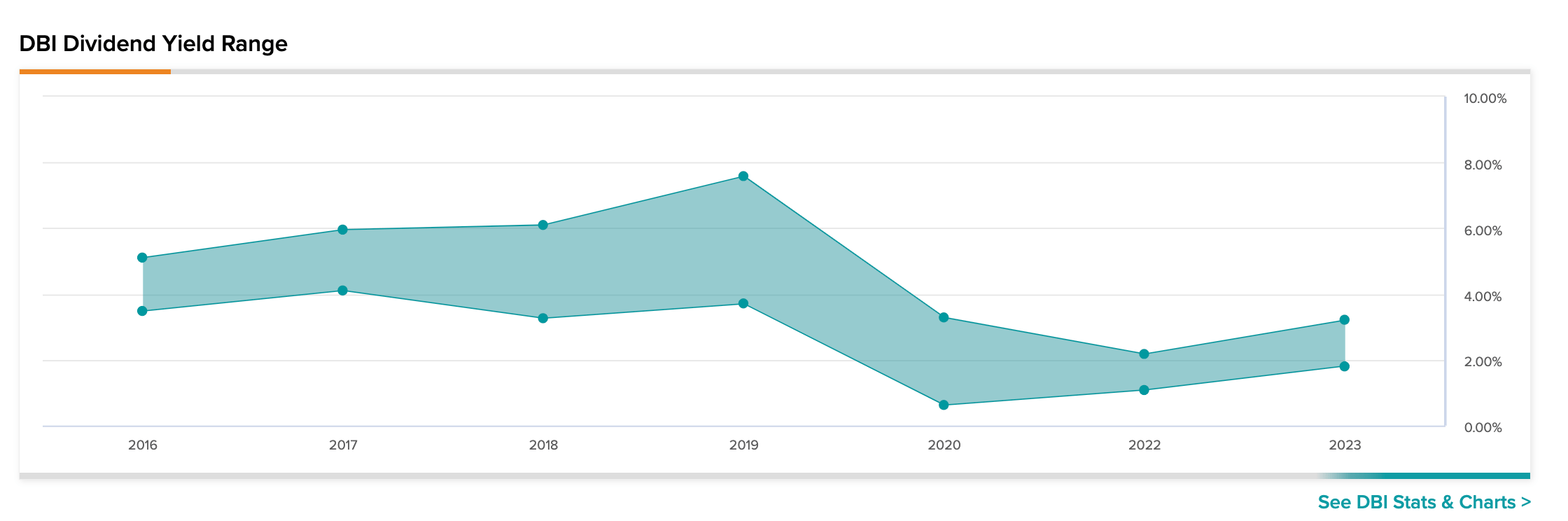

The dividend is barely an issue because the yield is a mere 1.9%, which is far below the +6% it yielded in 2017 through 2019. The yield has moved up since 2020 as the share price fell. Compared to the S&P 500 Dividend Yield of 1.54%, Designer Brands' yield is fair. It is below the industry's 2.83%. Its payout ratio is 12.7%, whereas the payout ratio for the larger apparel industry is +54.3%. We do not consider the dividend safe or consistent, let alone expect it to grow. The dividend is covered by cash from operations.

Cash from operations grew from $171.4M in January 2022 to $201.4M in January 2023 and to $264.6M TTM. Free cash flow per share grew in the same periods from $1.90 to $2.17 to $3.17. It appears the debt is being used advantageously to grow the company in a strikingly tough market; nevertheless, cash and receivables fall short of covering liabilities. In a skittish market and a stoic Federal Reserve, debt can put a company at risk. On the affirmative side, net debt is a conservative 1.5xs EBITDA.

{kind=link}

Another risk is the high short interest of +13%. This adds to our notion of a potential drop in the share price in the near term.

We were disappointed the CEO did not discuss during the last shareholders the company's e-commerce business, especially with a new chief of the sector. 2B users will buy footwear over the internet in 2023. Internet revenue is hitting $135B. Hopefully, we will hear more definitive financial information at their next meeting, with breakouts from e-commerce in their earnings report. We can only wonder if Designer Brands is missing a mass market and has generational gap issues that give short shrift to internet marketing and selling.

{kind=link}

If The Shoe Fits, Buy It

We do not believe there is a significant upside for retail value investors at the present time. There is potential with new management and less talk of a recession. Designer Brands Inc. will likely do better in a gusto economy. The company operates financially conservatively. The 8.02 PE and earnings make it a potential opportunity.

All footwear retailers face the biggest challenge from Amazon.com Inc (AMZN). Amazon generates more than double the annual revenue from online footwear sales than Designer Brands. It will not help the margins at Designer Brands by selling more over the internet but it is the primary path to greater revenue. More marketing to build in-store traffic is like a boxer throwing ineffective punches.

Other risks like weighty competition and the spiraling costs of retail locations contribute to the B- valuation and D- growth leaving earnings and margins wanting. SA assigns a Hold Quant Rating to a host of peers and that is telling. If Designer Brands is a good fit for a retail value investor's portfolio then it is reasonable for the long-term. Currently, we assess it as a stock to Hold.

For further details see:

Designer Brands Is Not A Fashionable Buy