DM - Desktop Metal: High Ambitions Despite Macroeconomic Pressures

2023-06-16 05:09:19 ET

Summary

- Desktop Metal has a clear mission to achieve a significant market share in additive manufacturing.

- The company is strategically focused on driving organic revenue, cost reduction, and customer-centricity.

- Q1 2023 earnings showed revenue decline but steady repeat business and growth in service revenues.

- Aggressive cost-cutting measures are expected to improve gross margins and drive toward EBITDA break-even by the end of 2023.

- Despite financial challenges, management remains optimistic, aiming for sustained growth through innovation and expansion.

Desktop Metal ( DM ) has a clear mission:

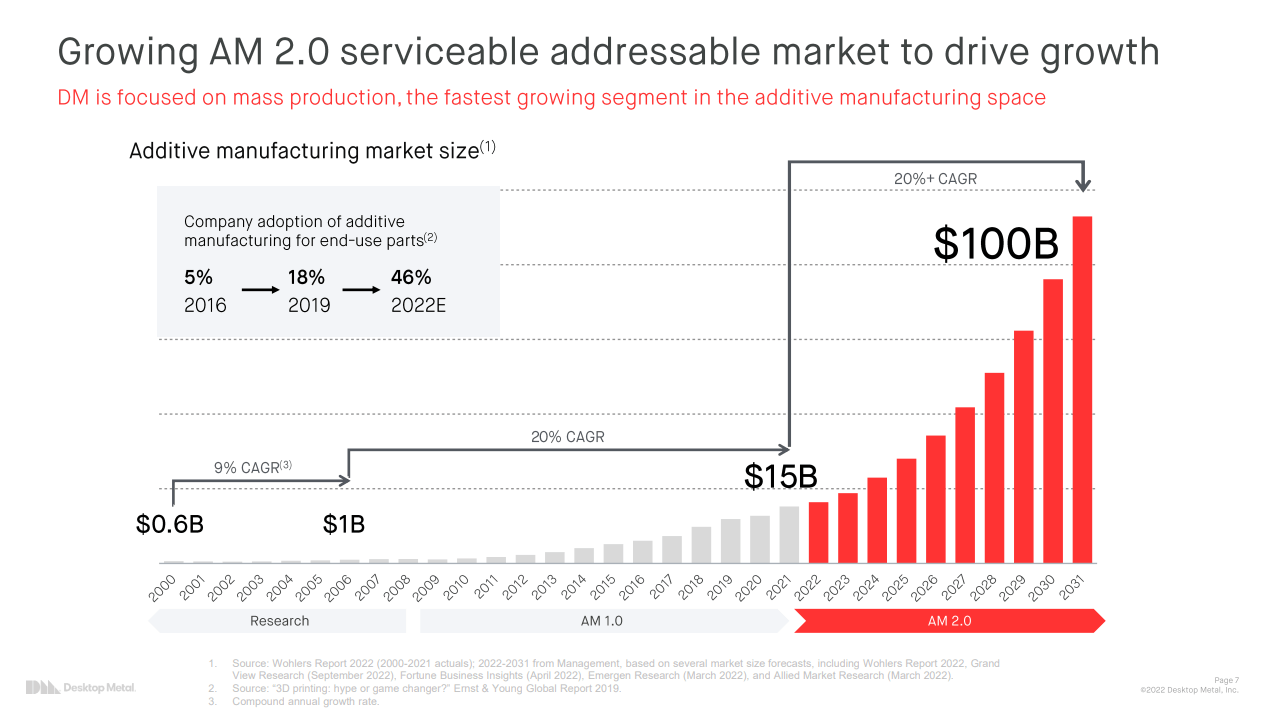

Enable mass production via AM 2.0 and achieve a double-digit share of the ~100B additive manufacturing market by the end of the decade (2023 Investor Presentation).

I believe the company has positioned itself to achieve this goal by setting strategic priorities such as driving organic revenue at scale, executing a path to profitability, focusing intensely on customers, and streamlining operating expenses. Execution thus far has been inorganic through acquisitions attempting to vertically integrate and achieve economies of scale. In 2021 alone, Desktop Metal acquired ten companies, and many of these acquisitions had niche expertise in their respective industries, allowing Desktop Metal to manage its ecosystem of 3D printers, materials, and software services. As a result, they have lower operating expenses, improved delivery timelines, drove predictable volumes, and improved their integration process.

However, there's no denying the financial challenges that Desktop Metal currently faces. With macro headwinds and sub-optimal margins making investors cautious, the company's financial health appears uncertain, but management execution is critical. Management's focus on innovation and expansion through acquisitions promises growth, but it will only materialize if they improve gross margins and drive organic growth.

{kind=link}

Q1 2023 Earnings Results

Desktop Metal's current state of business tells a complex and evolving story. In their most recent Q1 2023 earnings, the company posted EPS results slightly below expectations. Revenues declined by 5% y/y, resulting from some deals falling into the back half of this year. Product revenues declined -7% y/y while service revenues grew 9.2% y/y.

Management affirmed that they were seeing steady repeat business and introduced a new concept they call "Super Fleet Customers." These customers have purchased multiple units and implemented DM's technology for mass production. Super Fleet customers have high adoption rates and are a sustained revenue stream for the company, contributing to both short-term financial performance and long-term business growth. As of Q123, Desktop Metals has 370 super fleet customers.

The company's focus has been on an aggressive cost-reduction strategy, and it began its second $50m initiative in February, which involves six facility closures and a 15% reduction in headcount. In addition to their 2022 initiative, the company expects to drive total annualized cost savings of $100 million and put them on track to achieve EBITDA break-even by the end of 2023. These cost-cutting actions are expected to significantly improve fixed cost absorption, leading to substantial gross margin expansion throughout 2023.

The management team is executing its cost reduction strategy from an operating expenses (OpEx) perspective, evidenced by a y/y decrease of 32%. Moreover, OpEx as a percentage of sales decreased from 119% to 85% from FY 2021 to FY 2022, respectively, and has maintained this trend into 2023 Q1.

Company Reports Company Reports

However, the company has experienced some hurdles in managing its costs of revenues (COGS), as indicated by the Q1 2023 gross margin of 18%, falling short of its pre-COVID (FY2021) average of 28%. This dip can be attributed to lingering recessionary headwinds that began influencing operations in the second half of 2022. COGS as a percentage of sales increased from 73% to 82% from FY 2021 to Q1 2023, respectively.

The management team addressed the challenges of compressed gross margins and believes monetizing its current inventory, especially in sectors where demand is expected to surge, will significantly alleviate cost pressures. Additionally, the company is targeting an improved product mix to optimize cost structure further, thereby enabling an increased gross margin. They also anticipate that the ongoing cost reduction measures, combined with a potential increase in revenue, primarily from Super Fleet customers, will lead to sustained gross margin expansion throughout 2023 and beyond.

Despite the current economic challenges, the management remains optimistic about the company's future financial health. Once fully enacted, they project that these strategic initiatives will place them in a stronger position to navigate any ongoing macroeconomic challenges and achieve their goal of EBITDA break-even by the end of 2023.

SWOT Analysis

Several factors are essential in determining if Desktop Metal can provide investors with long-term outperformance. While the company has plenty of strengths, the irrefutable weaknesses have kept me on the sidelines for now.

Strengths

- New Product Releases : Desktop Metal is at the forefront of the additive manufacturing industry, consistently releasing new and innovative products. Their offerings, such as the Figur printer for sheet metal and the FreeFoam resin for form parts, are driving customer engagement and establishing their market leadership.

- Broad Customer Base Spanning Multiple Sectors : The company's vast array of additive manufacturing solutions has garnered interest from various industries, including automotive, consumer products, aerospace, and healthcare. This diversification reduces dependence on one sector and provides a broad base for growth.

- Strategic M&A : Desktop Metal's strategic M&A moves have expanded its product portfolio and customer base. Many of its acquirees had niche expertise in their respective markets and were able to leverage existing capabilities and enter new markets.

Weaknesses

- Sub-Optimal Margins : Despite its growth, the company struggles with relatively low profit margins and high cash burn in the short term. These financial stressors highlight the company's current growing pains as it integrates its acquisitions and scales its operations.

- Continued Guidance Misses : Historical misses on financial guidance have led to concerns over management's credibility. Meeting financial expectations will restore investor confidence and the company's overall reputation.

- Acquisition Integration Risks : With numerous acquisitions come the challenges of integrating different companies, cultures, and technologies. Desktop Metal must manage these integration risks to ensure seamless transitions and maximum benefit from these acquisitions.

Opportunities

- High-Margin Revenue Streams : As Desktop Metal continues to innovate and expand its product portfolio, it can forge new partnerships to drive high-margin revenue streams, fueling further growth.

- M&A in Fragmented Industry : The additive manufacturing industry is relatively fragmented, offering many potential acquisition targets. Desktop Metal can seize this opportunity to acquire complementary businesses and enhance its product portfolio, expanding its reach and market share.

- Margin Scalability Through Cost Optimization : Opportunities for margin improvement exist through cost optimization strategies and forming new partnerships.

Threats

- Mass Adoption Risk : The risk that manufacturing industries will not transition to 3D printing, or if the adopting of 3D printing is slower and more costly than traditional manufacturing.

- Sustained Macroeconomic Headwinds : Economic uncertainties, like supply chain disruptions or a global recession, could delay orders or impact on the company's operations, threatening its cost-reduction strategy.

- Competitive Pressures : The additive manufacturing industry is highly competitive, with numerous companies vying for market share. Pricing pressures with suppliers may remain elevated given the new entrants in the market.

Valuation

In terms of valuation, assessing Desktop Metal based on a forward Enterprise Value (EV) to revenue multiple appears most appropriate, considering the company is yet to reach profitability. PE or cash flow multiples may not accurately depict the company's current value relative to its peers, as it will be a few more years before DM reaches consistent profitability.

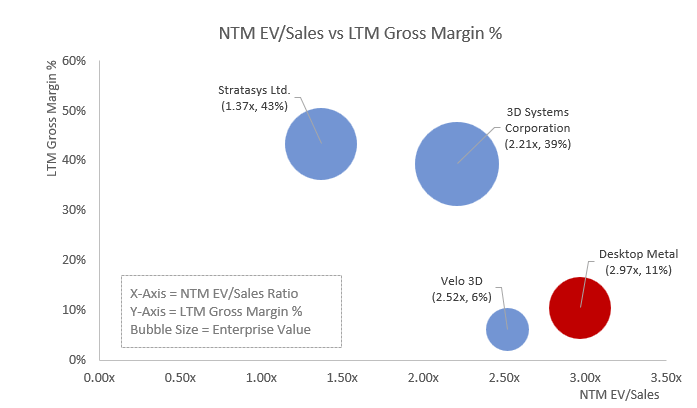

Desktop Metal operates in a highly competitive landscape, with significant players like Stratasys ( SSYS ), 3D Systems ( DDD ), and Velo3D ( VLD ) being the top contenders. These companies are considered Desktop Metal's closest comparable due to their operational similarities within the 3D printing industry. Given their similarities in business model, growth profile, and exposure to similar macroeconomic conditions, these peers provide a relevant benchmark for determining whether DM is valued fairly.

Desktop Metal trades at a forward multiple of 2.97x, while its peers exhibit a median trading multiple of 2.21x. This suggests a premium on DM's valuation despite its cost structure being less optimal than that of Stratasys and 3D Systems.

{kind=link}

If Desktop Metal were to trade at the peer median multiple of 2.21x, its implied enterprise value would be around $502.6 million. Accounting for cash and short-term investments of $149.8 million and deducting total debt of $136.5 million, we would be left with an implied equity value of approximately $515.9 million.

Given that about 322 million shares are outstanding, this results in an implied share price of $1.60. This implies a discount of 38% compared to its current share price of $2.21, suggesting that Desktop Metal's current valuation might be higher than the valuation derived from the peer median multiple.

Capital IQ

In conclusion, Desktop Metal's path forward is paved with both opportunities and challenges. If the management successfully executes its outlined initiatives, the company will become a more attractive investment proposition capable of providing substantial long-term value to its shareholders. For now, I will closely monitor next quarter's results for indications of progress in gross margin expansion from both cost optimization and revenue growth.

For further details see:

Desktop Metal: High Ambitions Despite Macroeconomic Pressures