DM - Desktop Metal: Teetering On The Edge

2023-09-29 07:48:42 ET

Summary

- Desktop Metal (DM) went public through a SPAC with high revenue projections but has faced significant challenges with profitability and maintaining its balance sheet.

- Despite large claims about its total addressable market (TAM), DM has struggled to translate this into sustained revenue growth without acquisitions.

- Outside of relying on acquisitions and mergers, there does not seem to be a sustainable plan to steer the company.

- The failed merger with Stratasys adds more uncertainty to the company's future, making it a speculative investment with an uncertain future.

- Despite the grim outlook, I am rating it as a Hold as there could be potential in its technology, but the path forward is very uncertain.

Desktop Metal (DM) belonged to a rare breed of companies to become public through a SPAC that only realized their revenue projections but also beat their own estimates. The premise was interesting as well. It was part of a revolution (like how many SPACs proclaimed themselves during that time) of an advanced way of manufacturing (additive manufacturing). The end market was huge with the industry projected to grow 11 times over this decade. After exhibiting a meteoric rise of almost 250% from its entry into the public market, the stock is down more than 95%. So what happened? This is a case of expenses going out of control and mismanagement of the balance sheet despite the great promise shown by the technology.

The technology

There are many articles out there that get into the weeds of their technology so I will keep this one short. Desktop Metal is a company that specializes in additive manufacturing, commonly known as 3D printing. Their business revolves around manufacturing metal 3D printing systems and related materials in a rapid and cost-effective way for industries such as aerospace, automotive, healthcare, and consumer goods. Currently, they boast of being the market leader in many of the technologies within the 3D printing space.

1. First platform of its kind to digitally shape standard sheet metal forming on demand. Presented a TAM of $300B

2. Global market leader in 3D printed hydraulic parts. Presented a TAM of $50B

3. Configured FreeFoam, a revolutionary expandable 3D printable foam for mass production. Presented a TAM of $170B

4. Binder Jetting (Fastest print process with the lowest cost of parts): Has the best-selling binder jet system, fastest binder jet printer, and largest metal binder jet envelope. Presented a TAM of $70B.

5. Has best-in-class photopolymer systems. Presented a TAM of $200B

If one had to believe their technologies, they are potentially addressing a market, the size of almost $800B!

Reality

While the company likes to showcase the potential of its technology and throw big numbers in its presentations I find them guilty of TAMSanity. The term coined by Jim Chanos, our generation's famous short seller, is a play on the abbreviation for Total Addressable Market. In essence, what this means is that companies cite big numbers on the addressable market and since they are going after it, it is implied and sometimes explicitly said that it would translate to their topline. It is up to the investors to take this with a grain of salt. So the reality from their earnings for the last two years and recent quarters is a lot more somber.

In pursuit of growth, the company has splurged on acquisitions. Just in the last 3 years, the company has acquired 5 companies and spent $875M in the last two acquisitions alone. At the time when they announced their last acquisition, it was more than 25% of their market cap and is a good indication of the size of the acquisition they were going after. I especially dislike scenarios where companies buy their way out of growth especially when it's coming from big acquisitions. The last company they acquired ExOne, was bringing in almost $60M of annual revenue. So it was no surprise that the company was beating its projections.

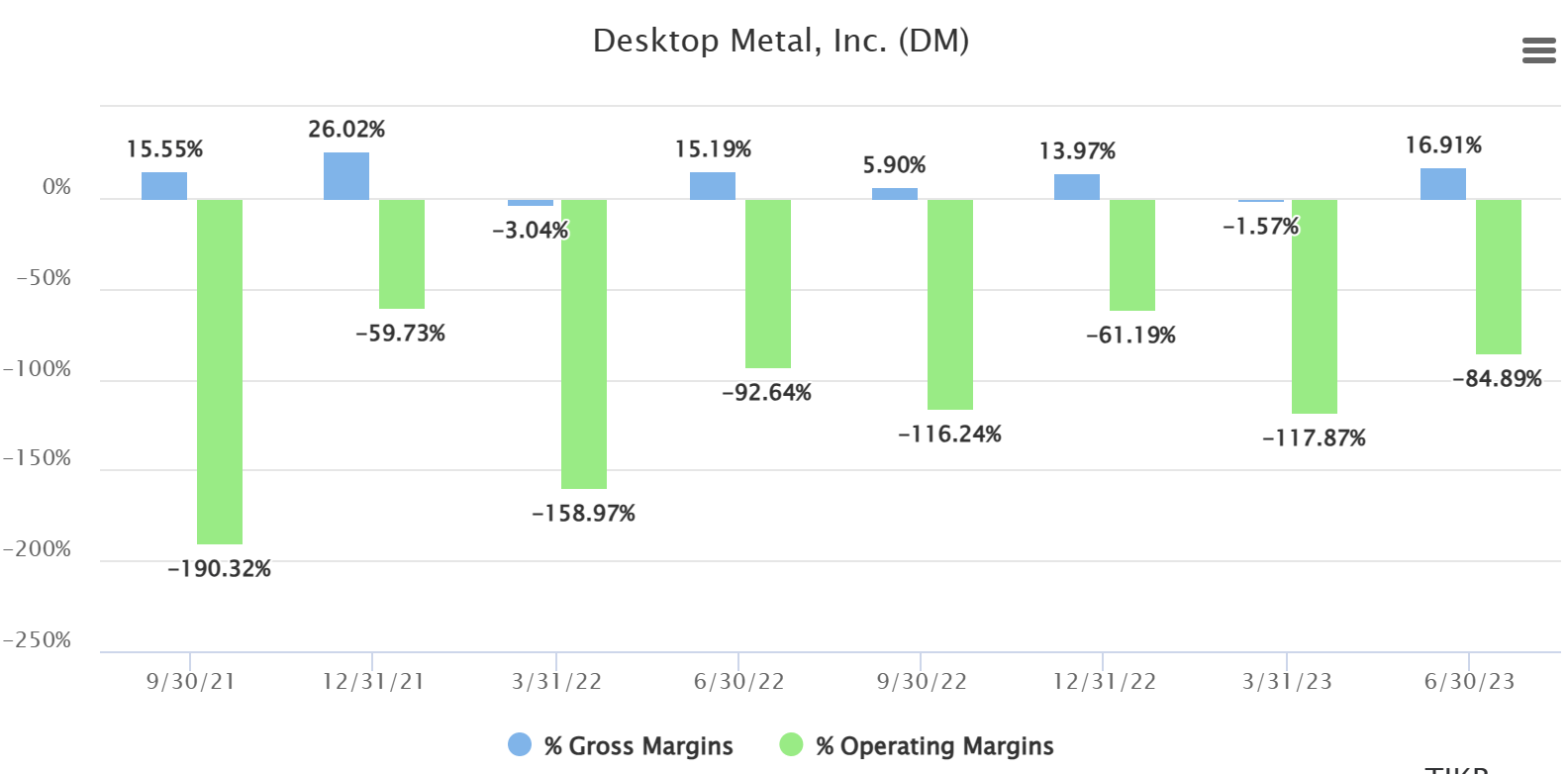

Even their income statement does not inspire confidence either. Their claim that their technology reduces the costs upon adoption is laudable. But what about their own costs?

{kind=link}

Gross margins and operating margins are improving but it is still far from bringing them any profitability. However, the company claims that it will reach adjusted EBITDA profitability this year.

Every time you hear 'EBITDA' substitute it with 'bull**** earnings

- Charlie Munger

EBITDA is already a made-up metric (non-GAAP) and strips many items and with adjusted EBITDA it can strip even more items till the number suits a story. In my opinion, this does inspire confidence in the company's future especially when the company is losing copious amounts of OCF (-$33M for the latest quarter) and has only $127M as cash in its balance sheet. Currently, its liquidity ratios are sound as the company's debt position is manageable at this point.

Quick Ratio: 2

Current Ratio: 3.5

But looking at its cash runway, it is likely that the company will have to look at external financing. In this high interest-rate environment, this is not a good look for the company. Its equity has been in continuous decline and sees bigger declines after it splurges on acquisitions and then goodwill gets adjusted periodically. Personally, I am not a big fan of what's happening here as well.

Valuation

The market currently values the company at its book value so no complaints there. I believe it is fair based on the risks involved. But its revenue multiple is 2.2x and compared to the industrial sector it is far outside the median at 1.3x. This is where it gets tricky. Desktop Metal is in a mature industry but its whole goal is to disrupt the industry. If the company can still follow through with its vision, the premium on its sales multiple could be completely justified. It's claims of upending more than half a trillion dollar industry means even a minor slice of that industry could completely turn around its fortunes.

During the second quarter of 2022, the company was able to provide guidance and the outlook was it would grow its revenues by 131% YoY. Unfortunately, the story has drastically changed for the 2023 outlook with guided revenues between $210 - $260M. Even at its mid-point of $235M, it only represents a 12% growth in revenues! (For reference, its projection from the SPAC presentation was $329M and a 100% organic growth case) This means its forward PS will remain mostly unchanged and would still be around 2x approximately. So where is the promised land of capturing TAM? Even with the lead the company claims to have in the industry, when will it capture its share? I guess the company needs more acquisitions again.

Latest news

In its latest quarter results, the company mentioned its merger with Stratasys. The benefits of the merger included being the first company to achieve additive manufacturing at scale for metals and polymers, a diversified bigger product portfolio, multi-million dollar synergies, cross-selling potential, and most important of all a big revenue boost from mass production solutions (+50%). Probably, this could have rescued the company from its current state.

But from the latest news, this fell through, and Stratasys no longer wants to pursue Desktop Metal. It did not have enough support from shareholders and decided to call off the vote which means we are back to square one; Huge TAM, barely enough growth, no plans for profitability, and a shrinking balance sheet (a small upside with Desktop Metal to be compensated by a break-up fee from the failed Stratasys deal).

A long road

For this thesis to change, it could be a long road for the company. Fortunately, the Stratasys saga helps Desktop Metal's balance sheet. If the company is able to pull through long enough for the world to start adapting its technologies en masse then there could be a path to profitability for the company. This is quite important in the current environment. There could also be other potential suitors who are interested in what Desktop Metal has built so far. It is undeniable that the company is sitting on a lot of IP and a company with deeper pockets and better execution can steer the company. Either way, it is a speculative investment and while I do make room for speculative investments in my portfolio, in this case, I prefer to be on the sidelines as the path forward seems mired with uncertainty. I rate this company as a Hold.

For further details see:

Desktop Metal: Teetering On The Edge