DESP - Despegar.com: Attractive Valuation With Growth Potential

2023-06-15 14:48:30 ET

Summary

- Despegar.com, an online travel agency in Latin America, has faced underperformance due to macroeconomic conditions, the impact of COVID-19, and an initially high valuation.

- Despite not being profitable yet, Despegar's Q1 2023 financial results show record revenue and growth, with potential for further expansion and new business segments like fintech.

- The company is currently undervalued compared to its peers, and it represents an attractive long-term investment opportunity.

Editor's note: Seeking Alpha is proud to welcome Reconquista Capital as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Thesis Snapshot

When a company is having its best operational performance of all time but its stock is still near its all-time lows it is worth a deeper look. This is the case with Despegar.com ( DESP ). The company's business has fully recovered from COVID while its share price is still near the March 2020 lows. We believe this represents a perfect opportunity to go long on the stock.

Company Background

Despegar is an online travel agency (OTA) that operates in 19 countries across Latin America. The company operates marketplaces where its suppliers can manage the distribution of their products and its customers can compare, plan, and purchase travel-related products. Through its website and mobile app, the company offers airline tickets, hotel reservations and other travel packages and services.

It was founded more than two decades ago, but it has only been public for 6 years now. In 2017, the company completed a successful IPO on the NYSE, priced at $26/share. However, shares are now trading around $7, more than 80% away from its all-time high. So, how did Despegar get here?

Why has Despegar underperformed for so long?

Despegar's underperformance can be explained because of a few reasons. Firstly, Despegar operates in Latin America where macroeconomic conditions have been deteriorating for some years now. Currently, for example, Argentina is in a deep economic and political crisis with inflation running north of 100% per year. This is important because around ~15% of Despegar's revenue comes from Argentina. Moreover, most currencies of Latin America have depreciated a lot against the US Dollar during the last few years. This means that, although it is cheaper for tourists to come to Latin America, it is more expensive for locals to travel abroad.

Another obvious reason is COVID. The pandemic hit the travel industry the most and Despegar was no exception. The company had to raise $200 million to face the losses through the sale of convertible and non-convertible preferred shares and warrants. We will discuss more about this later.

Lastly, we can consider the fact that the initial valuation at which Despegar started trading was expensive. The company generated $90 million in EBITDA in 2017 while its enterprise value was $1.53 billion. This means that it was trading at 17x EV/EBITDA. But right now the story is very different. Despegar's financial performance is near its best in history but is worth a fraction of what it was in 2017.

Q1 2023 results

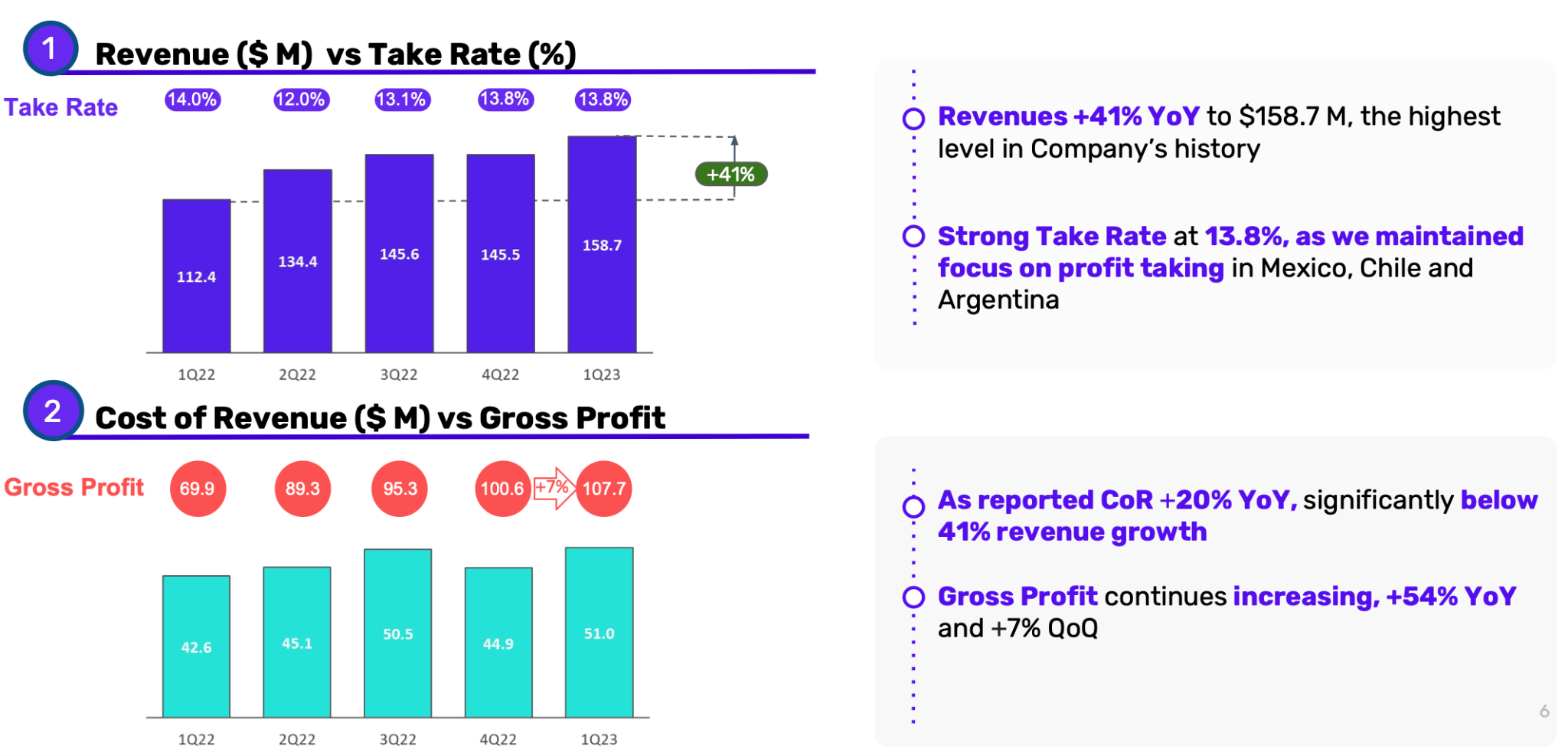

Despegar reported Q1 2023 financial results on May 18, 2023. Revenue came in at $158.7 million, increasing 41% YoY and reaching a record quarterly level. Moreover, trailing twelve-month revenue was also at an all-time high. Looking at this it seems like the business is growing like crazy. However, part of it is the recovery from COVID. We expect that revenue growth will moderate in the coming quarters, but still grow in the double-digits YoY.

Gross bookings ((GB)) grew 44% YoY to $1.1 billion and Despegar managed to maintain a high take rate of 13.8% vs 14% in Q1 2022. Total number of transactions increased 5% YoY to 2.06 million. Because GB grew much more than the total number of transactions, the average selling price ((ASP)) increased from 36% YoY to $558. This means that consumers are spending more per transaction than a year ago. This is a great trend and one we expect to continue as Despegar is able to cross-sell more products and raise prices due to inflation.

On the other hand, the cost of revenue increased only 20% YoY, significantly below revenue growth. One of the reasons is that the "Packages, Hotels and Other Travel Products" segment, which has a higher margin than the "Air" segment, represented 34% of the GB, up from 30% a year earlier and 21% two years ago.

{kind=link}

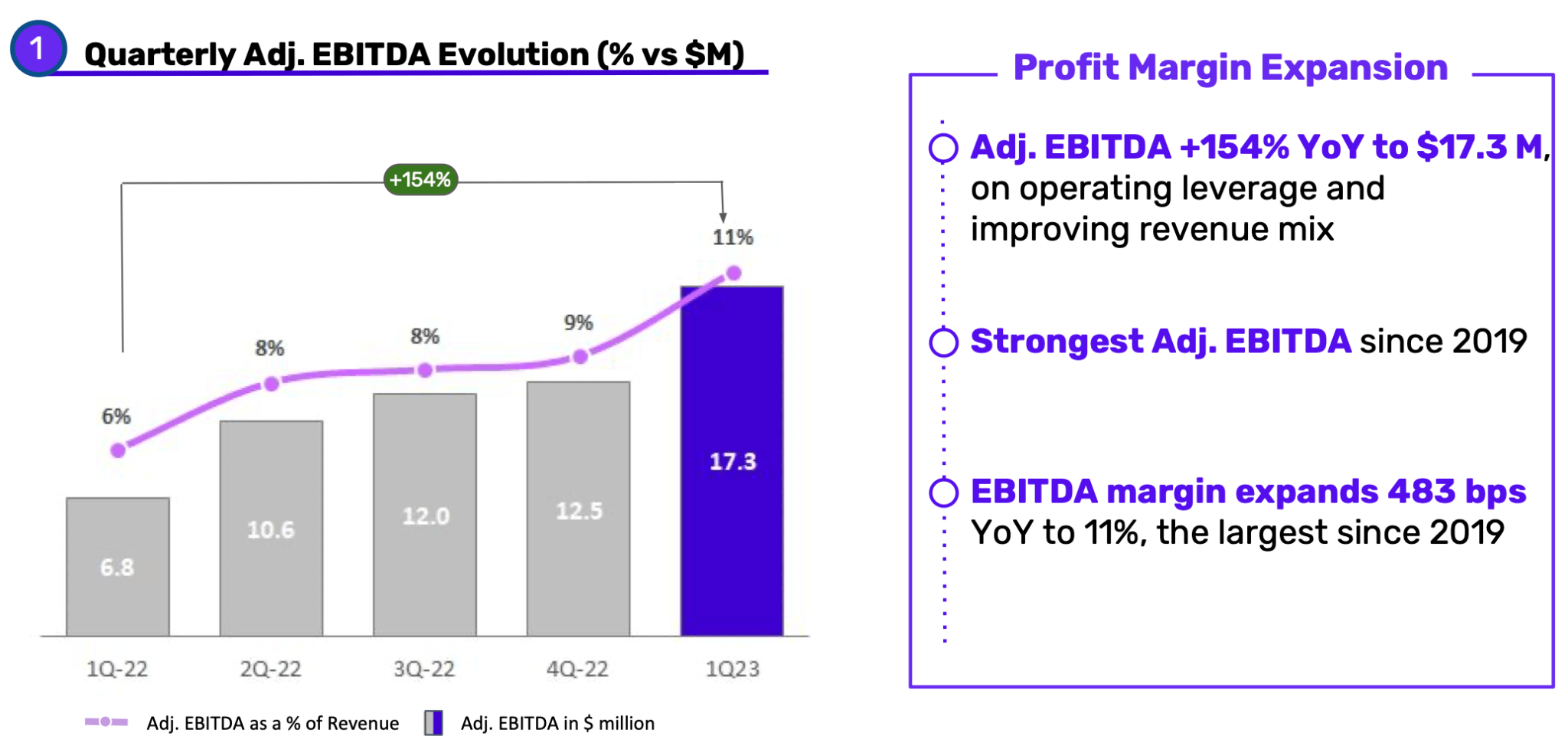

??Despite the growth in the top-level financials, Despegar is not profitable on the bottom line yet. Although costs grew less than revenue YoY, it reported a net loss of $0.7 million, or $0.10 per diluted share, compared to a loss of $30.9 million a year earlier. Adjusted EBITDA, on the other hand, was $17.3 million positive, growing 153% YoY. This was the highest Adjusted EBITDA in Q1 since 2018. Adjusted EBITDA as a percentage of revenue expanded 483 basis points to 11%.

{kind=link}

Currently, the management projects they can achieve revenue between $640 million and $700 million in 2023, growing 24.5% YoY at the midpoint. Also, management estimates Despegar will generate between $80 million and $100 million in EBITDA for the full year. In our view, this goal is highly achievable. Typically Q1 and Q2 are seasonally weaker than the second half of the year because it is when summer ends and winter begins in the southern hemisphere. If Despegar can keep this performance during the rest of the year, and management made it very clear in the earning call that they can, the projections should be right on target.

In regards to the financial position, Despegar ended March with $228 million in cash on its balance sheet, while having only $20 million in short-term debt and virtually no long-term debt. Free cash flow was negative $3 million during the quarter against $24 million positive in Q1 2021. Additionally, it is important to take into consideration that the company pays dividends on the preferred shares issued in 2020. The Serie A shares carry a 10% dividend yield while the Serie B shares pay a 4% dividend yield. This translates into $17 million in yearly dividend expenses that could instead go into marketing expenses, share repurchases or just cash in the balance sheet.

Despite this, Despegar's financial position is very strong. We don't see the need for the company to issue more debt or shares to fund its operations, as they are on the brink of profitability.

Growth Catalyst

The company is in a unique position to continue to benefit from the travel recovery in Latin America and maintain its position as a leader in the region. A key growth engine will be customer growth and retention. In addition to the efforts being made in sales and marketing (expenses in this category grew 70% YoY in Q1 2023), in the first quarter of 2023 Despegar's loyalty members program increased 343% YoY to 14.0 million people. Moreover, the Net Promoter Score (NPS) for the company was 67.3% at the end of March 2023.

Customers coming back and a high NPS score are a sign that the company's value proposition is great. This can raise the opportunity for cross-selling products. Rather than just selling plane tickets or hotel reservations, Despegar is aiming to be a place where you can buy everything you need for your trip: from plane tickets and car rentals to hotel reservations and excursion trips. As we mentioned earlier, the "Packages, Hotels and Other Travel Products" segment has a higher margin than the "Air" segment and has been growing consistently as a percentage of GB in the last few years. If the trends continue, we can expect higher margins in the future.

Furthermore, Despegar is expanding into new business segments. In 2020 the company acquired the fintech company Koin in Brazil. Koin provides point-of-sale installments loans, buy now pay later (BNPL) services and fraud prevention services. However, they are taking things slowly. Koin maintained a conservative approach to loan origination throughout 1Q 2023. As such, TPV decreased 12% YoY to $18 million in the quarter and Adjusted EBITDA was negative $2.5 million compared to negative $4.6 million in 1Q 2022. The management estimates Koin remains on track to reach EBITDA breakeven in the second half of 2023. We believe that once Despegar grasps a better knowledge about the financial segment and continues to improve on how to measure risk effectively, Koin should become an important source of growth for the overall business.

Lastly, Despegar has a history of acquiring OTA's through Latin America. Because of this, we cannot overlook the fact that the company may pursue growth through acquisitions. Management said during the first quarter earnings call that they are "having very promising conversations with a series of targets". We trust the management on this topic as the previous acquisitions have proven to work out. We believe this is a great growth strategy as long as they acquire exceptional businesses at reasonable prices.

Risks

As any company does, Despegar faces many risks. The two more common risks are location and competition. Despegar operates its business in Latin America, a highly volatile region where economic and political crises are common, and faces competition from bigger, more established OTA's such as Expedia ( EXPE ), Booking ( BKNG) , and now Airbnb ( ABNB ).

However, these aren't risks that concern us because: a) Latin America may be a volatile region but it has a huge growth potential and b) the Despegar brand resonated more with locals and offers a wider variety of products and services. Nevertheless, they shouldn't be overlooked. But we believe the main risk for Despegar's business is maintaining and building new relationships with suppliers. The suppliers are the airlines, hotels, car rentals, bus operators, etc. that offer their products and services on the Despegar website.

In our view, Despegar is trying to become a one-stop shop for travelers to book everything they need for their trip. If the company isn't able to capture new suppliers, or even worse lose suppliers, the value proposition may be severely affected. Regarding this topic, we should mention the deal struck between the company and Expedia in 2015, under which Despegar relies on Expedia for substantially all of the hotel and other lodging products that they offer for all countries outside Latin America. In exchange, Expedia pays monthly marketing fees calculated based on the GB and bought 14.52% of Despegar's outstanding shares. This deal is important because if it were to be terminated, which is highly unlikely because of several covenants, Despegar would be left with virtually no suppliers outside Latin America. Building a network of hotels, car rentals, tour operators and more is not something that can be done easily. Also, it represents around 6% of the yearly revenue. We see no reason why this deal would break since it would harm both more than it would benefit them. Nonetheless, it is something to have in mind: Despegar has very few suppliers of their own outside Latin America.

Is Despegar stock undervalued?

We believe Despegar is undervalued relative to its peers on a multiple-comparative analysis. Despegar is currently trading at 3.3 times EV/Forward EBITDA, almost half of what Expedia trades at. We also compare it to Booking, but it is important to note that Booking trades at a much higher multiple because of its superior margins.

The company also trades at a discount on a price-to-sales basis. At the moment, Despegar shares are trading at 0.8x TTM revenue.

In these charts it is evident that Despegar's multiples have always traded relatively close to those of Expedia. Yet, today the spread between them is higher than usual. However, the situation is not the same with the forward P/E ratio. Despegar trades at a much higher forward P/E ratio than its competitors, although we don't think it is very relevant because they haven't been profitable for a long time. 2023 would be the first profitable year for Despegar since before the pandemic, whereas Expedia and Booking were already profitable last year.

To round up, in our opinion there is no reason for Expedia to trade at a much higher multiple than Despegar. For Despegar to trade at the same P/S multiple as that of Expedia, its shares would need to rise about 75% and to trade at the same EV/EBITDA multiple it should increase by 30%.

Conclusion: Buy Despegar for the long term

Given Despegar's history since IPO, its current financial position, growth prospects, and valuation, we believe it represents an attractive risk-reward opportunity in a turmoil market. It may not have fancy AI or machine learning technology, but the business survived the pandemic, came out even stronger than before and, in our opinion, has a bright future ahead of it.

For further details see:

Despegar.com: Attractive Valuation With Growth Potential