TMUS - Deutsche Telekom: Unsurprisingly Strong

2023-05-11 09:03:30 ET

Summary

- Deutsche Telekom reported its Q1 results on May 11 and performed in line with analyst and management expectations.

- There were no real surprises in the earnings report as Deutsche Telekom does not seem to be impacted by macroeconomic issues. Stability and consistency were key.

- The German operating segment saw strong and accelerating customer net add growth which is a positive sign for the years to come. Also, underlying metrics improved.

- I remain bullish on Deutsche Telekom stock as the EPS growth outlook looks strong, driven by significant margin improvement over the next several years.

Investment Thesis

I lower my rating on Deutsche Telekom AG (DTEGY) from a strong buy to a buy and update my revenue and EPS estimates following the company’s Q1 results which contained little surprise and were in line with the guidance from Wall Street analysts.

This telecommunications company stands as a global leader in its industry, boasting its position as the largest in Europe and one of the largest worldwide. With a significant presence across various European nations, what truly captivates my enthusiasm is its extensive reach across both Europe and the United States. By possessing nearly 50% ownership of T-Mobile US ( TMUS ), Deutsche Telekom strategically situates itself on both continents. Operating across all verticals of the telecommunications industry, including mobile subscriptions, fixed-network lines, and wireless networks, this telecom giant demonstrates its pure moat. And it is this moat that drives great revenue stability and predictability, allowing it to outperform when times get rough.

And it is not just its stability, moat, and product necessity that make Deutsche Telekom an attractive investment today, but the company actually has a great EPS growth outlook, driven by the expectation for significant margin expansion over the next several years. Also, the company has been paying down its debt over recent years, improving the financial position of the company. Today, Deutsche Telekom is one of the best-positioned telecom companies in the world and is poised for solid growth.

Its Q1 results once again proved that the company can perform under any circumstances, resulting in a minor FY23 outlook upgrade from management. In this article, I will take you through the latest developments and financial results and update my estimates and view on the company accordingly.

Deutsche Telekom delivers another unsurprising and consistent quarterly report

Shareholders of Deutsche Telekom ((DT)) have not had much to complain about so far this year as shares of this ultra-defensive industry giant are up over 15% YTD, outperforming most of the global indices. Over the last year, shares are up 28%, showing a very impressive share price performance as the company finally reached new all-time highs for the first time since the dot-com bubble. Yes, it has been a while.

And this increase in share price has been completely justified as the company has been showing a very resilient performance over the last couple of years, with the business seeing little to no impact of all the negative economic developments like high inflation, rising interest rates, a (minor) banking crisis, and even a war on the European continent. In fact, shares have done precisely what you expect them to do; outperform when times get rough.

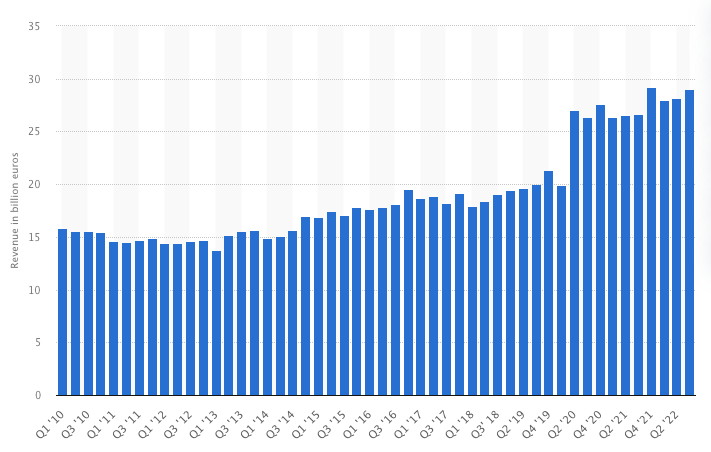

That the company is indeed in a great position today (its best one since the early 2000s) can also be seen in its steadily growing revenue. The company has shown that it can grow both its top and bottom line through any circumstances due to the simple necessity of its offering and the increasing importance of it. It’s hard to imagine life today without a solid broadband or 5G connection, right?

Deutsche Telekom Revenue Growth (Statista)

{kind=link}

That the company’s offering is sticky and resilient was once again confirmed when it reported its Q1 earnings early this morning, on May 11. The company reported revenue of €27.8 billion, up a minor 0.3% YoY. Revenue growth was driven by a 3.5% increase in services revenue which is the most important metric as this is the best indicator of company performance. Service revenue came in at €22.8 billion. Adjusted EBITDA AL was up 0.9% and came in at €10 billion, yet organically this was up 4.4%.

Net profit was up 289% as DT completed the sale of the tower business. As announced in July 2022, DT sold 51% of its tower business in Germany and Austria. I believe this was a good move by management as it improves the cost structure and maintenance liabilities by a bit. As a result, net income in the quarter totaled €15.4 billion.

Adjusted net income was €2 billion, down 12.5% YoY, primarily due to the interest effect in the measurement of liabilities and provisions. EPS declined accordingly to €0.39. Yet, recurring EPS was up 19.4% YoY to €0.37 which is a really strong performance and a great indicator of business health as this is derived from recurring revenue. Also, this is what DT bases its dividend on, so if this shows continued impressive growth, investors should expect a solid improvement in the dividend (3.3% yield) as well.

The sale of the tower business transaction also has had a very positive effect on the company’s net debt position as it allowed DT to lower this by €10 billion to €93 billion, improving the net debt/EBITDA AL ratio from 2.58 to 2.31. And while the debt position is still significant, this has been trending in the right direction and shows great capital allocation abilities from DT management.

Growth in Germany is accelerating

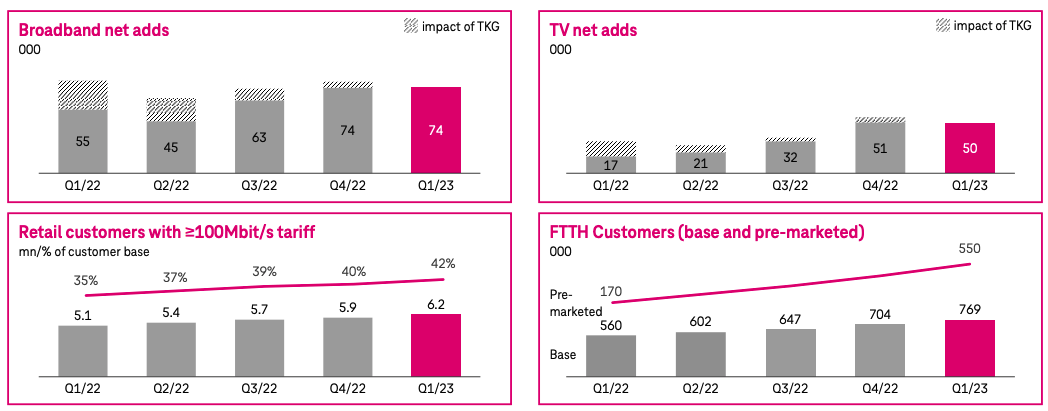

Revenue in the German operating segment increased by a solid 3% YoY to €6.1 billion and EBITDA AL increased by a slightly faster 4% YoY to €2.5 billion, making this the 26 th consecutive quarter of positive EBITDA growth. This is a perfect illustration of how consistent the performance of DT has been over recent years, despite a fair share of economic headwinds. This quarter, growth in the German segment was again solid, driven by growth across all business areas.

The main driver of this last quarter was growth in broadband which added 74,000 customers and grew revenue by 4.7% YoY organically. DT is seeing an increase in internet speeds chosen by customers as 42% of all customers now pay for 100 Mbit/s or higher. This is a great driver of customer value as higher internet speeds are more expensive while not driving up costs for DT. As a result, as customers upgrade their internet speed, this drives revenue growth without customer additions and improves margins. With the need for internet speed growing as a result of increased digital activity, as perfectly illustrated by data from HighSpeedInternet.com which shows that the average internet speed in the US increased from 42.86 Mbps to 99.3 Mbps from 2020 to 2021, this should bode well for DT over the remainder of the decade.

Back to the financial results for the German operating segment, service revenues grew 2.4% YoY, again driven by solid customer net adds across the board. Yet, the most important factor here is that we are seeing an acceleration in customer additions as DT continues to execute on upselling opportunities and drives higher customer value. Of course, adding customers is great, but this trend accelerating is even better as this indicates that the business still has plenty of growth ahead.

German segment Q1 (Deutsche Telekom)

{kind=link}

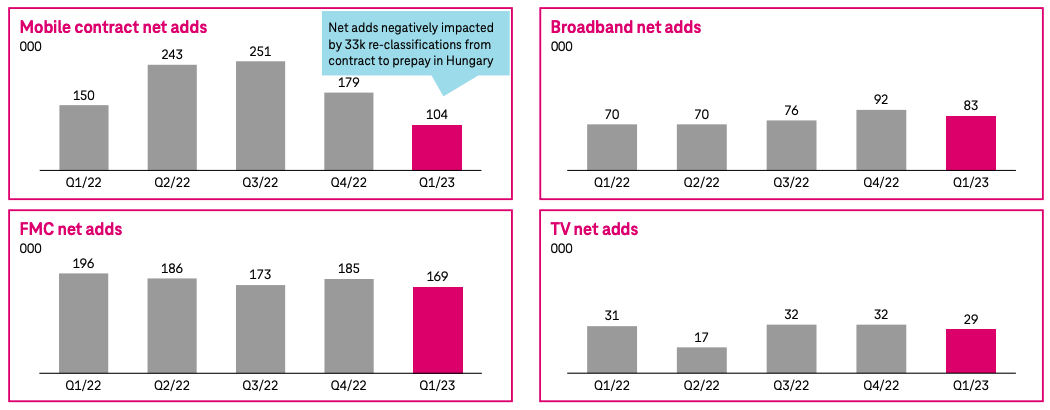

Telekom Deutschland added 274,000 new (mobile) customers, which drove services revenue for Mobile up 1.7% YoY. Again, this is the second-highest number of customer additions in the last 5 quarters, and much higher than the 193,000 net customer additions in 1Q22, showing a strong acceleration. And just like in broadband, DT has more growth opportunities in Mobile besides customer additions. For example, data usage is growing rapidly, especially with the pandemic lockdowns now out of the way, and this increased by 51% YoY to 11.4 GB per month per user on average. For DT, higher GB usage results in higher contract value and higher revenue per customer. We should expect this trend to continue in the following years as the total internet usage is accelerating. Finally, churn in mobile was also down from 1.2% last year to just 0.8% in Q1.

Europe was steady but not as impressive

Revenue in the European operating segment increased by 3.8% YoY (4.9% organically) to €2.8 billion. EBITDA AL grew by 0.7%, or 1.2% organically, to €1 billion, making this the 21 st consecutive quarter of positive EBITDA growth, despite high energy prices and tax headwinds weighing negatively on profitability.

Growth in Europe was driven by strong net adds across the board with broadband adding 83,000 customers and mobile adding 104,000 customers. Yet, unlike in Germany, growth in Europe was relatively steady over the last 5 quarters and showed no real acceleration in growth. Especially mobile contract net adds was unimpressive with the lowest number in the last 5 quarters. Still, growth remained resilient, and DT continues to be one of the leading telecommunications providers in Europe based on customer numbers.

Europe performance Q1 (Deutsche Telekom)

{kind=link}

T-Mobile US continues to be a growth driver

With DT owning a 50%+ stake in T-Mobile US, the results of this business are of importance to DT. And luckily so, as the US business has been firing on all cylinders over recent years, driving additional growth for DT.

Last quarter, the company grew service revenues by 2.8% to $15.5 billion. EBITDA AL increased by a faster 6.6% to $6.9 billion and resulted in a positive guidance update from T-Mobile management, also positively affecting the FY23 outlook for DT.

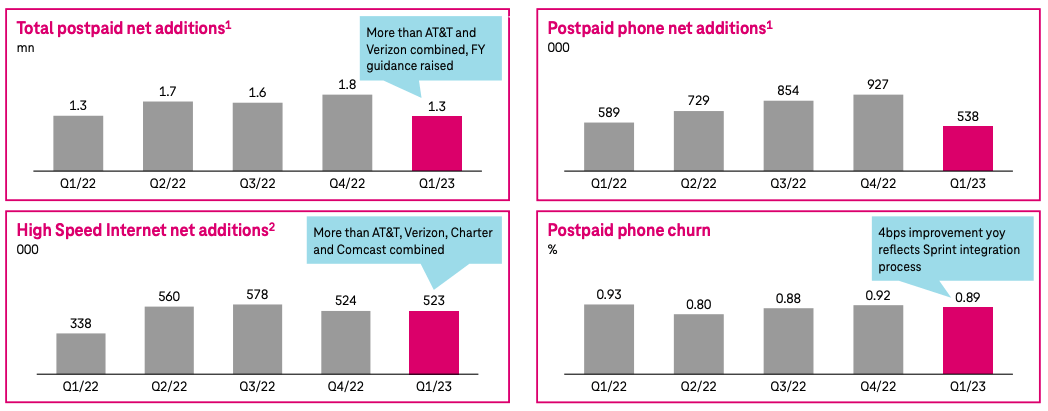

T-Mobile US added 1.3 million postpaid customers which was in line with the prior year, and more than AT&T ( T ) and Verizon ( VZ ) combined, illustrating that the company is still rapidly gaining market share. Still, this was down from previous quarters and across all business segments growth was relatively in line with previous quarters. Especially its wireless internet at-home offering was strong with the addition of 523,000 customers, resulting in a total of 3.2 million customers for this product.

T-Mobile US performance Q1 (Deutsche Telekom)

{kind=link}

Overall, growth for T-Mobile US was strong and the company continues to beat its competitors on pretty much all fronts. I expect T-Mobile to remain a growth driver for DT which has now reached its targeted stake in the company of above 50%. The telecom services outlook for the US is strong with an expected CAGR of 6.5% until 2030 which is slightly above the global growth expectation. With T-Mobile US gaining market share in this industry, I believe this one is well positioned for solid growth, which will also benefit DT.

Outlook & Deutsche Telekom stock valuation

Deutsche Telekom has largely maintained its FY23 outlook as the business performance was mostly in line with previous expectations in Q1. This is what I wrote following the Q4 earnings call:

This results in an expected EBITDA of around €40.8 billion of which €13.9 billion will be coming from the US. DT expects to see 3% EBITDA growth for the German segment, a little over 5% for the US, and Europe to remain flat YoY. Capex should come in much lower compared to 2022 at just €16.8 billion due to a significant Capex decrease for the US segment. As a result, free cash flow is expected to come in much higher at above €16 billion compared to €11 billion in FY22. This should also result in EPS of €1.60 which is above FY22 EPS excluding the one of benefits.

Yet, with T-Mobile US updating its FY23 outlook, this also had a slight positive effect on DT as management did increase its FY23 EBITDA AL guidance to €40.9 billion, up from €40.8 billion. While this is of course a positive development, it does not really move the needle or result in significant changes to the outlook.

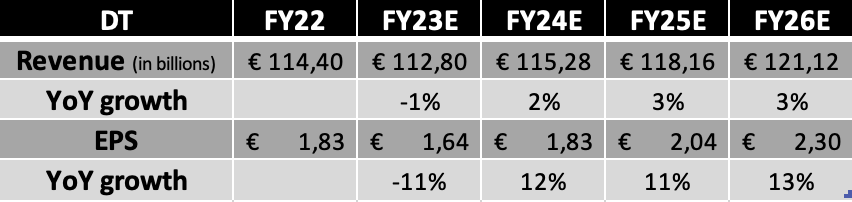

Following my research, the solid quarterly results, and the largely maintained outlook from DT, I now project the following results for the years until FY26.

{kind=link}

Shortly explaining these estimates, I now expect Deutsche Telekom to report a slight revenue decrease for FY23, combined with a more significant decrease in EPS, yet FY22 included a one-off positive of €0.32 on EPS, so correcting for this, EPS is actually expected to increase by 6% as DT continues to improve its margins. And I expect this improvement in margins and EPS to continue into the following years. DT has already guided for recurring EPS of above €1.75 for FY24 as it is projecting significant margin improvement, especially from its stake in T-Mobile US. Therefore, EPS is expected to show impressive growth over the next few years (FCF is expected to show similar strength). At the same time, revenue growth is projected to remain in the low-single digits, in line with the industry outlook.

Moving to the valuation, considering the impressive EPS growth projected for the next couple of years by me and analysts alike, the excellent consistency in the business, the strong outlook, and product necessity, I believe shares are still attractively priced, despite these trading near their all-time high. Shares are currently valued at a forward P/E of 13x which is not overly expensive when considering all factors, but compared to peers, also far from cheap after the share price has increased by quite a lot over the last year.

Considering its superior growth outlook and consistency, I believe DT deserves to be valued at a premium over its peers. Therefore, I believe a P/E of 13x is justified for this industry leader, resulting in a price target of €24 ($26), based on my FY24 EPS estimate. This leaves an upside of 11.7% for investors from a current share price of around €21.48.

Conclusion

Deutsche Telekom delivered solid and unsurprising quarterly results in Q1 which were roughly in line with analyst estimates and showed a resilient performance from the telecom giant. The company does not seem overly impacted by macroeconomic issues and continues to see high demand as it reported solid net adds and strong underlying improvements.

Overall, my stance towards this company remains unchanged and I continue to view it as the best choice in the telecom industry, driven by its exposure to both the European continent and the US, as well as a management team that continues to perform to perfection.

With significant margin improvement expected over the next several years, the outlook is very strong for DT, and investors should expect meaningful share price appreciation and a solid dividend yield. Also important to consider is the significant jump in FCF over the next several years which gives DT the ability to significantly lower its debt, increasing its risk-reward profile and financial stability.

Based on the current outlook until 2026, I maintain my price target of €24 ($26) per share and believe shares are currently trading around fair value. Still, the potential returns over the remainder of the decade and the solid dividend yield and growth outlook leave enough upside to warrant a buy rating on Deutsche Telekom, although lowered from a strong buy after the strong performance of the shares over the last year.

For further details see:

Deutsche Telekom: Unsurprisingly Strong