CA - Disinflation: A Gift That Keeps Giving

2023-12-24 09:00:00 ET

Summary

- U.S. equity markets extended their winning streak to an eighth week - the longest in five years - after inflation data both domestically and abroad showed a further cooling of price pressures.

- Extending its weekly winning streak to the longest since 2017, the S&P 500 posted gains of another 0.9% on the week, lifting the benchmark to within 1% of record highs.

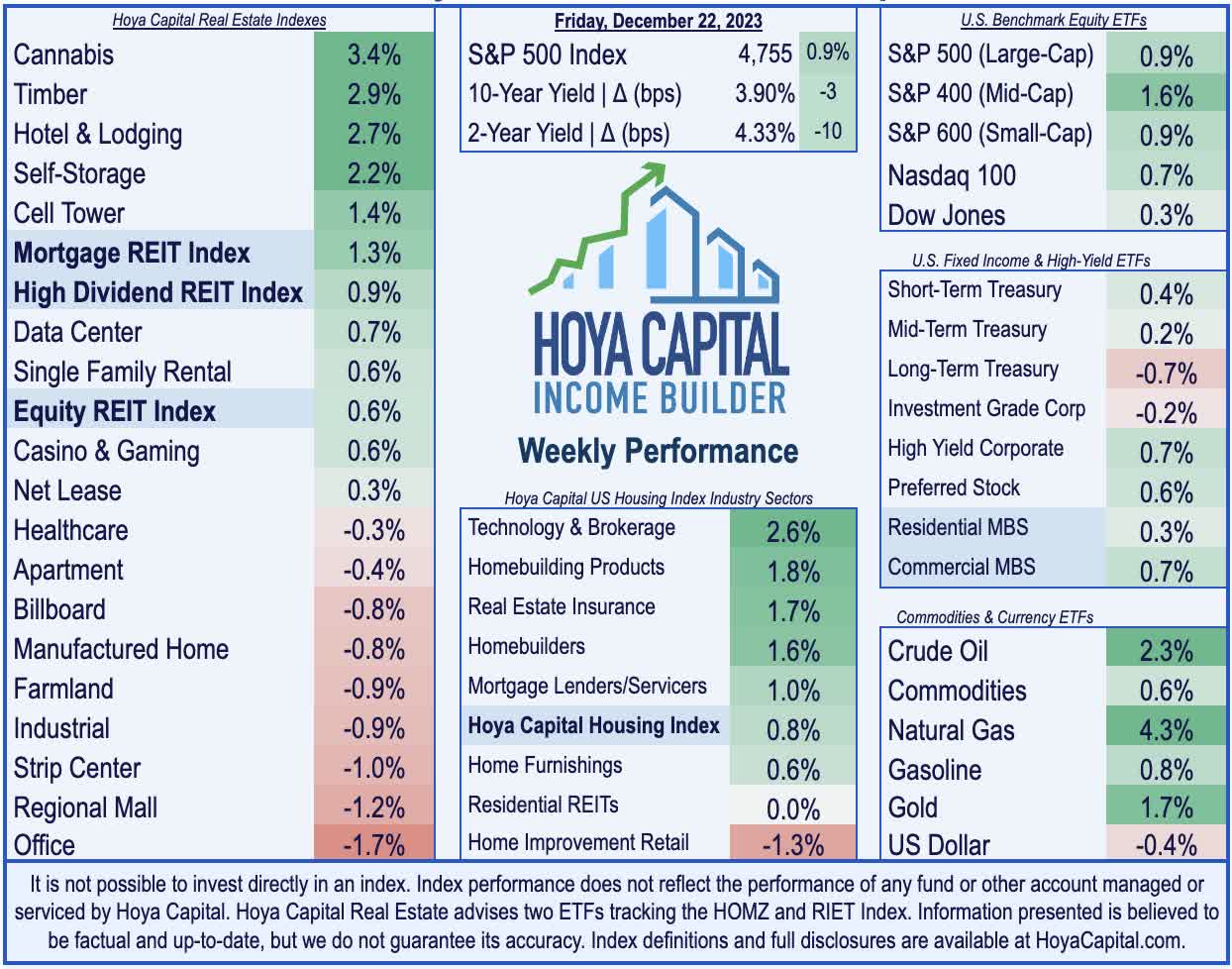

- Pushing their eight-week rebound to over 25%, the Equity REIT Index gained 0.6% this week, with 9-of-18 property sectors in positive territory, while the Mortgage REIT Index gained 1.3%.

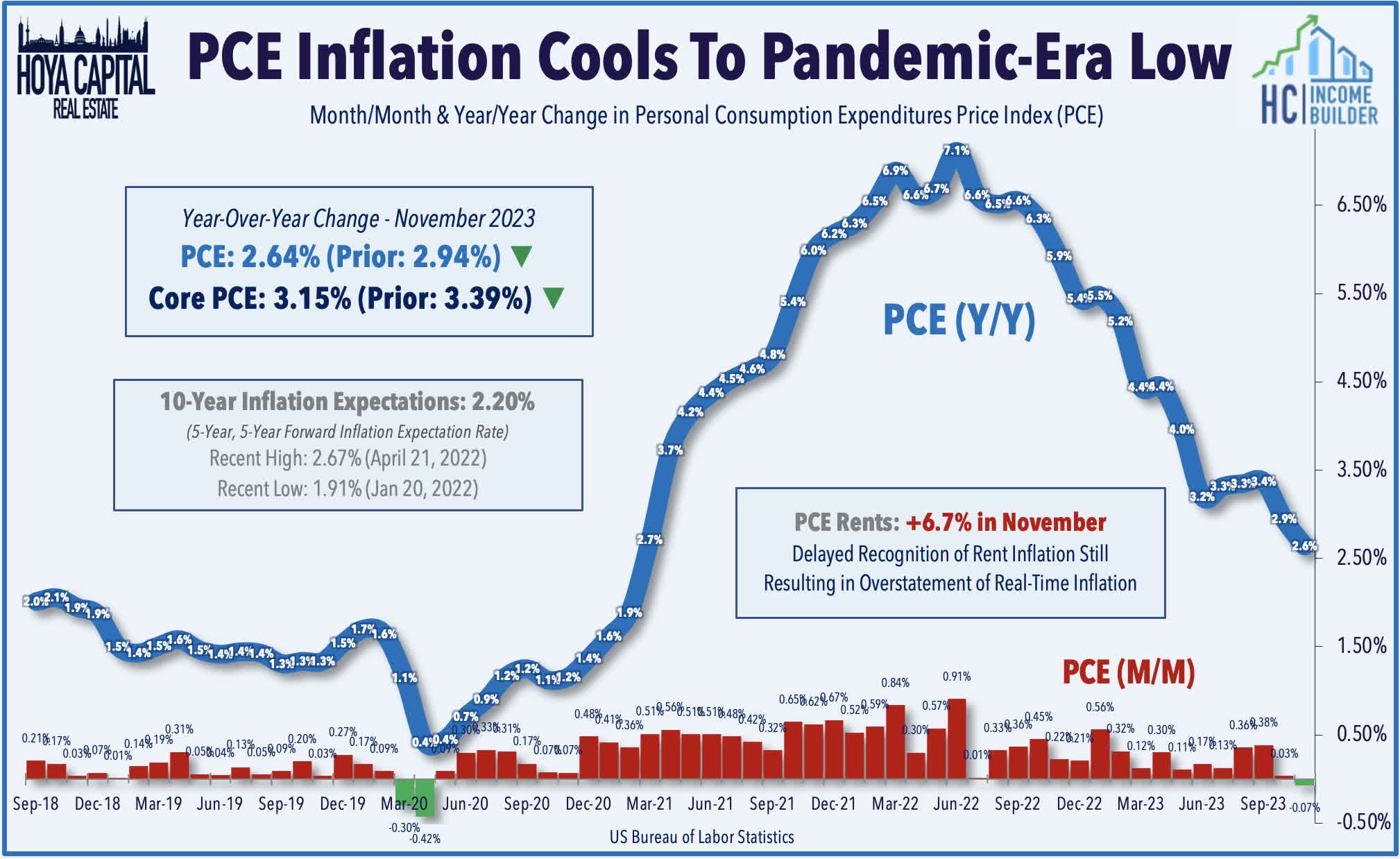

- The Core PCE Index - the Federal Reserve's preferred inflation metric - was up just 1.9% on a six-month annualized basis, below the Fed’s 12-month target, while Core PCE ex-Housing is higher by just 1.1%.

- Another week, another wave of REIT dividend hikes and special dividends. Veris Residential hiked its dividend, while Apple Hospitality and Rayonier each declared special dividends, lifting the full-year total to over 80 REIT dividend increases.

Real Estate Weekly Outlook

U.S. equity markets extended their weekly winning streak to an eighth week - the longest in five years - after inflation data both domestically and abroad showed a further cooling of price pressures in November, with several closely watched metrics within the data series now trending below the Fed's inflation objective. Markets were largely unfazed by an attempted pushback from several Fed officials and by renewed supply chain concerns impacting Europe, keeping alive a dramatic year-end rally and lifting the major benchmarks to the cusp of record highs.

{kind=link}

Extending its weekly winning streak to the longest since 2017, the S&P 500 posted gains of another 0.9% on the week, lifting the benchmark to within 1% of record highs. The Mid-Cap 400 and Small-Cap 600 - which lagged their large-cap peers throughout the rate-hiking cycle - again led the gains this week, outpacing their large-cap peers for the sixth week of the past eight. The tech-heavy Nasdaq 100 notched a series of record highs this week and remains on pace for its best year since 1999. Pushing their eight-week rebound to over 25%, the Equity REIT Index gained 0.6% this week, with 9-of-18 property sectors in positive territory, while the Mortgage REIT Index gained 1.3%. Homebuilders and the broader Hoya Capital Housing Index also outperformed this week as housing market data showed the early positive effects of the pullback in mortgage rates from three-decade highs.

{kind=link}

The chorus of hawkish remarks from Fed officials did little to spoil the holiday cheer ahead of the Christmas holiday, nor did the final flurry of major economic reports of the year. Fed Presidents Goolsbee and Mester echoed the sentiment from Williams and Bostic in the prior week that it is "too early" to declare victory on inflation, but data throughout the week provided mounting evidence of a decisive disinflation tailwind across both the U.S. and Europe. The encouraging inflation news provided fresh fuel for the two-month-long bond rally, as the 10-Year Treasury Yield declined by three basis points on the week to close at 3.90% - hovering just above its lowest close since July - while the policy-sensitive 2-Year Treasury Yield declined by ten basis points to 4.33%, its lowest close since early June. The US Dollar dipped to five-month lows on expectations of Fed rate cuts beginning by mid-2024. WTI Crude Oil rebounded 2% on concern over the impact on supply chains of recent attacks on commercial ships in the Red Sea en route to the Suez Canal. Despite the lift this week, oil prices remain about 25% below their highs in late September.

{kind=link}

Real Estate Economic Data

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

{kind=link}

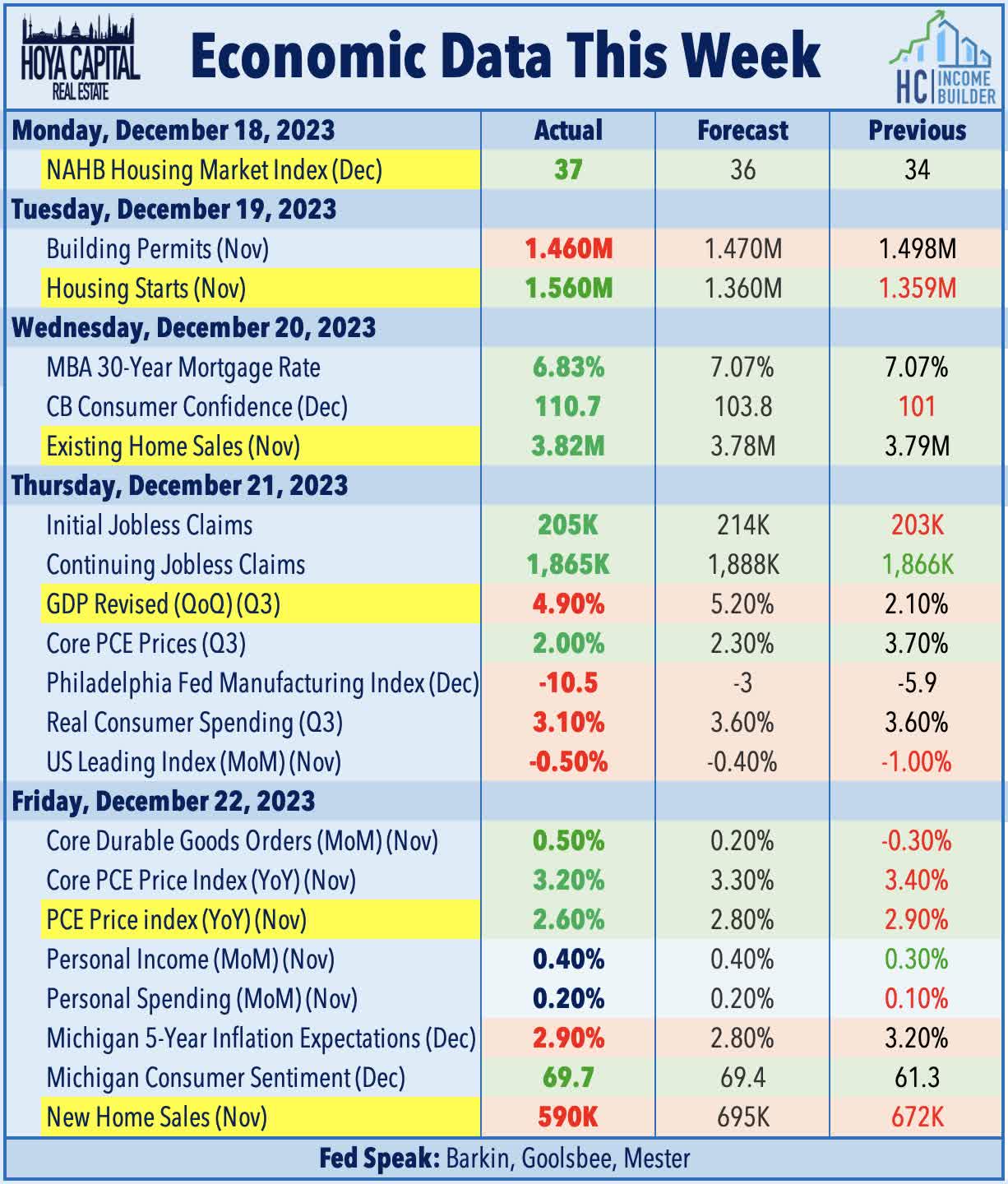

Following cooler-than-expected Consumer and Producer Price Index data earlier this month, PCE Price Index data released this week provided further evidence that price pressures continued to moderate in November. Core PCE - the Fed's preferred gauge of inflation - rose just 0.1% in October and 3.2% from last year - cooler than consensus estimates and the lowest annual increase since April 2021. Headline PCE declined by 0.1% on the month - also below expectations - which pulled the year-over-year increase to 2.6%. Goods prices declined 0.7% for the month, driven by a 2.7% dip in energy prices following a late-summer resurgence. Services prices rose 0.2%, an increase that is still being driven largely by the delayed recognition of housing inflation seen 9-18 months ago. We've noted that real-time shelter inflation - as measured by a half-dozen private market data providers - is closer to the 0-2% range, far below the 6.7% increase reported in government data. On a six-month annualized basis, core PCE was up just 1.9% - below the Fed’s 12-month target - while Core PCE ex-housing is higher by just 1.1%.

{kind=link}

Homebuilders and the broader Hoya Capital Housing Index were again leaders this week on data showing that the housing industry appears to be emerging from its two-year slump resulting from stiff interest rate headwinds. Consistent with data showing an uptick in Homebuilder Sentiment for the first time in five months, the Census Bureau reported that Housing Starts jumped to a six-month high in November, rising to a 1.56 million annualized rate - well above the consensus forecasts of 1.36M. The long-sluggish single-family segment drove the rebound in November, with single-family starts jumping to their highest level since April 2022. The average rate on a 30-year fixed mortgage dropped back below 7% for the first time since August, according to the data last week from Freddie Mac. Building Permits, however, decreased to a 1.46 million pace - slightly below consensus estimates - due to a drop in multifamily starts. Apartment construction activity has moderated in recent months amid a cooldown in rent growth from the historic double-digit increase seen in 2021.

{kind=link}

Data this week also showed that Existing Home Sales rose in November - snapping a streak of five-straight monthly declines - as the retreat in mortgage rates from the October peak at three-decade highs appears to be starting to unleash some deferred housing market activity. The NAR reported that Existing Sales rose 0.8% from October to a seasonally adjusted annual rate of 3.82 million in November. On a year-over-year basis, however, sales remained lower by 7.3%. Total housing inventory at the end of November stood at 1.13 million units, down 1.7% from October but up 0.9% from one year ago (1.12 million). Unsold inventory sat at a 3.5-month supply at the current sales pace - down from 3.6 months in October - and well below the long-term historical average of roughly six months. New Home Sales data was less upbeat, however, showing that sales of new homes slid 12.2% from last month to a 590k annualized rate - the lowest level in a year. That said, since the Census Bureau records gross rather than net new sales, we've noted that New Home Sales data can become temporarily distorted if there are sudden shifts in cancellation rates, resulting in an overstatement of sales early in a downturn and an understatement of sales early in an upswing.

{kind=link}

Equity REIT Week In Review

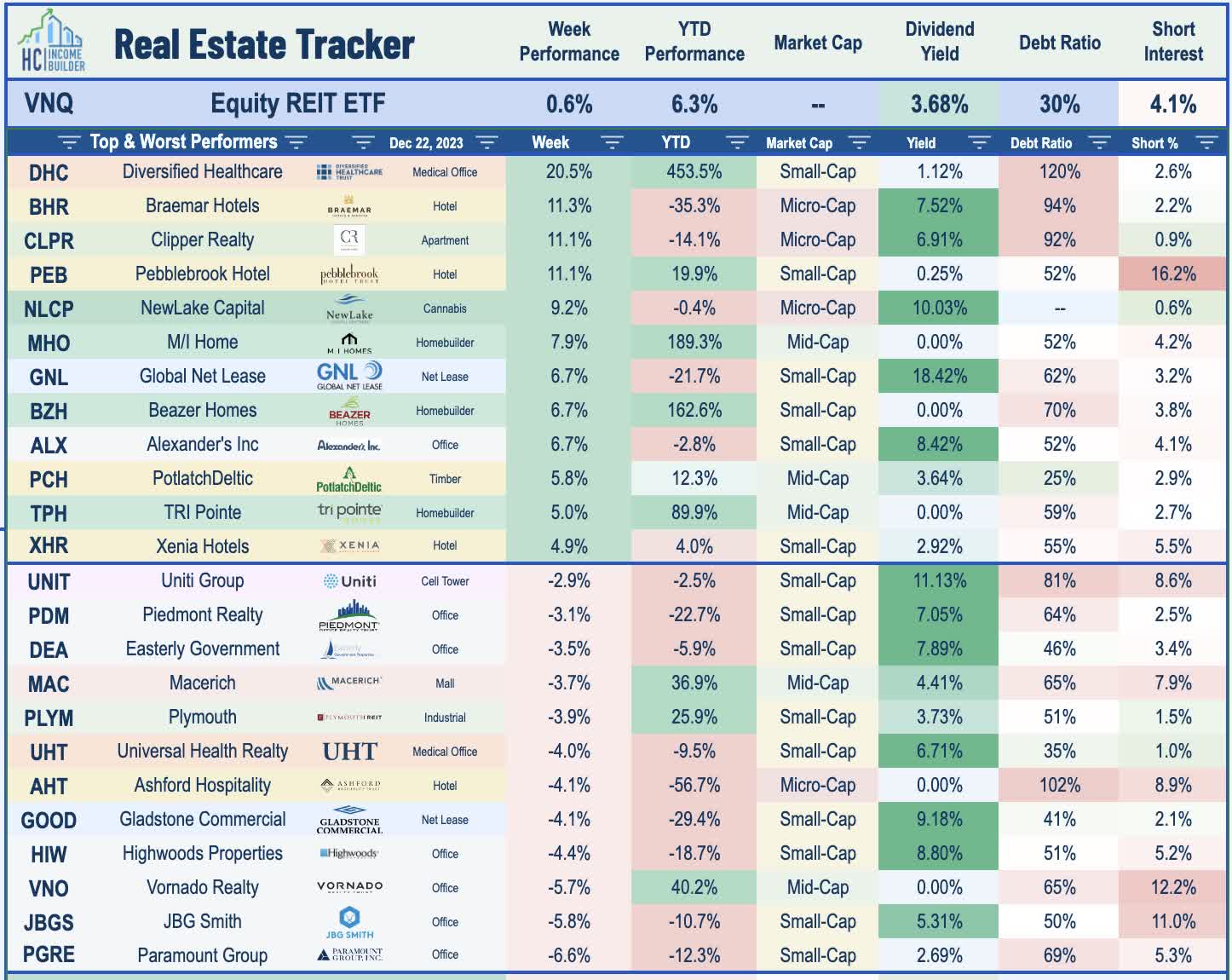

Best & Worst Performance This Week Across the REIT Sector

{kind=link}

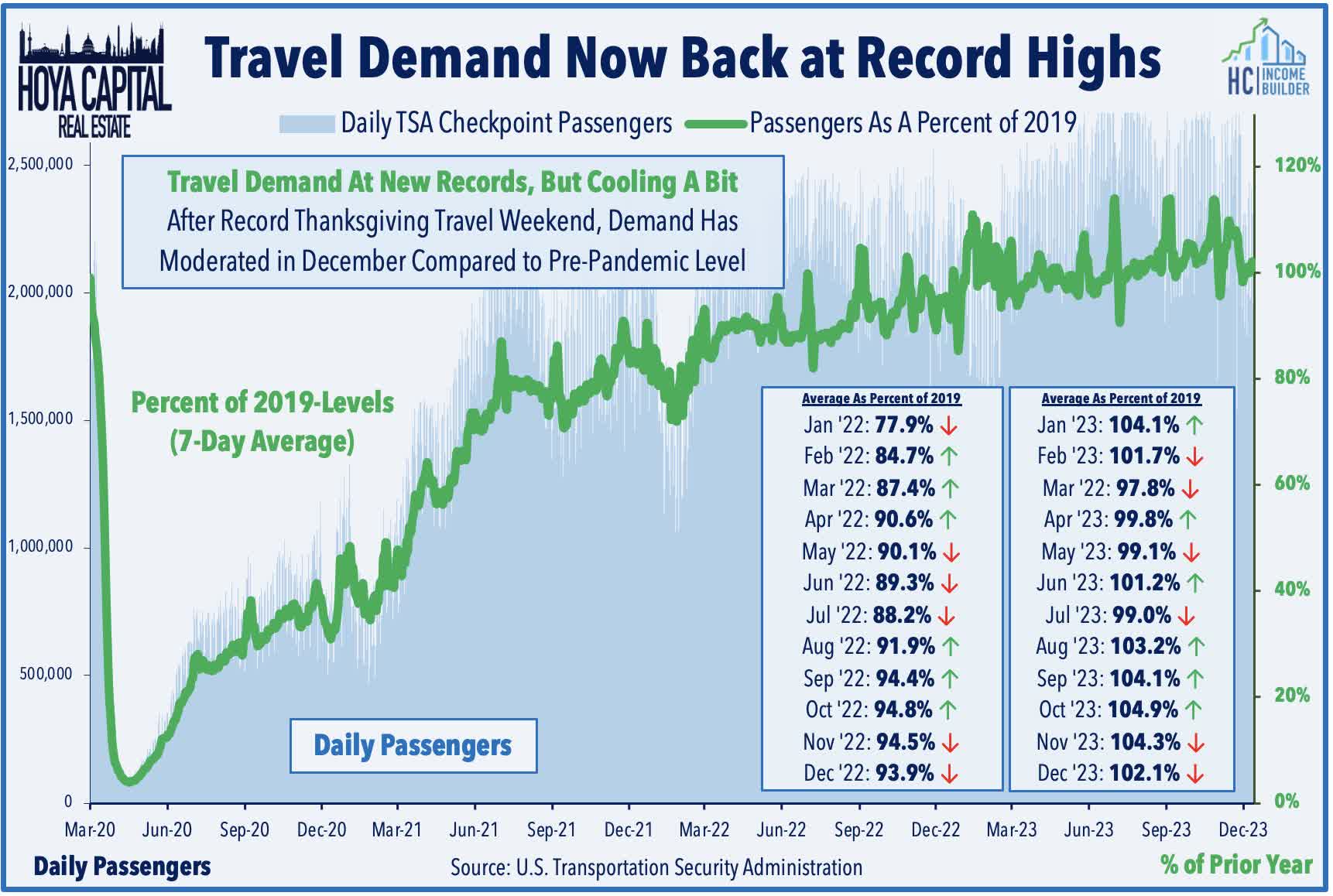

Hotels : Expect a busy airport this holiday season. Pebblebrook Hotel Trust ( PEB ) rallied 11% this week after providing a strong operating update in which it noted that Revenue Per Available Room ("RevPAR") climbed 6.4% year-over-year in November - its strongest comparable of the year. PEB - which owns 46 hotels and resorts with a heavy presence in California, Florida, Boston, and DC - noted that a recovery in its urban portfolio drove the outperformance, which offset a moderation in its resort segment. Citing "robust business transient and group business," PEB's urban RevPAR rose 10%, led by strength in San Francisco, Washington DC, and Boston, while its resort RevPAR was flat. Park Hotels ( PK ) rallied 3% after reporting similar trends, noting that its RevPAR was up 14.5% year-over-year in November, which is roughly 5% above pre-pandemic levels. Park also cited strong recent performance from its urban portfolio driven by an acceleration in business travel in Boston, Chicago, New York, and Denver. Park reaffirmed its full-year 2023 outlook, calling for RevPAR growth of 8.3%. TSA checkpoint data shows that throughput climbed to over 105% of 2019 levels during November - the highest since the pandemic - and has averaged about 102% of pre-pandemic levels thus far in December. Hotel data provider STR reports that industry-wide RevPAR was 13% above 2019 levels in November, as a roughly 18% relative increase in Average Daily Room Rates ("ADR") offset a roughly 4% relative drag in average occupancy rates.

{kind=link}

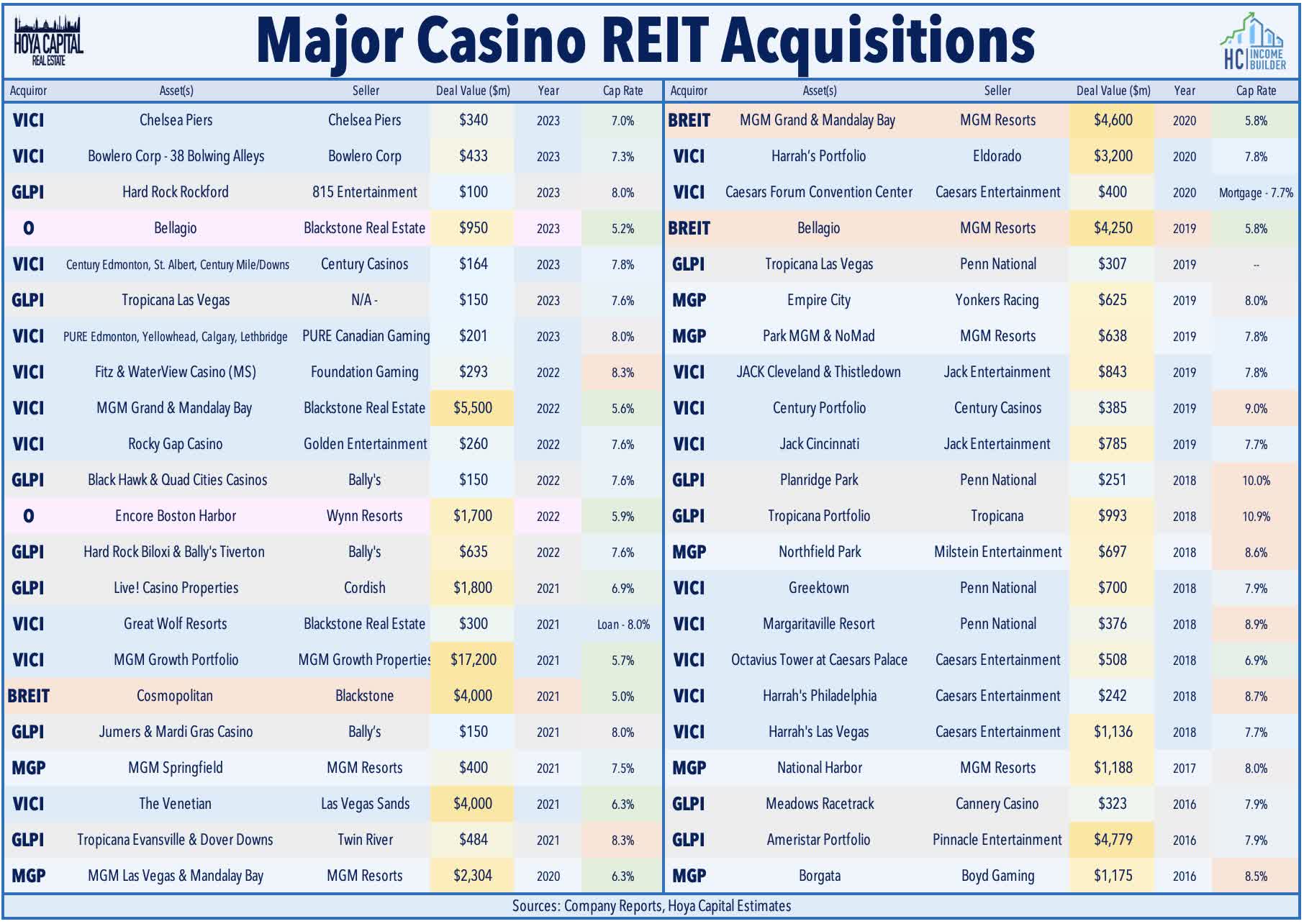

Gaming : VICI Properties ( VICI ) traded flat this week after announcing a pair of deals with two existing tenants, continuing a gradual shift from a pure-play casino owner towards a broader "experiential-focused" strategy. VICI announced that its $72M loan to NYC-based recreational facility Chelsea Piers - which was initiated in 2020 - will convert into a leasehold interest, with VICI paying roughly $340M to acquire the property (roughly $270M in incremental capital), representing VICI's first debt-to-equity conversion. Under the sale-leaseback for the 780k square foot property, Chelsea Piers will lease the property from VICI for an initial term of 32 years with a 10-year extension option. Separately, VICI also announced that it originated a new loan facility to golf resort operator Cabot for its resort in Saint Lucia and announced an agreement in principle to provide a loan facility for its resort in Scotland. VICI had previously initiated a $120M loan to Cabot for its Cabot Citrus Farms golf resort in Florida in June 2022. The deal expanded VICI's total committed capital across the three resorts to approximately $300M. These loan facilities - which bear an average interest rate of around 9% - also include conversion options for VICI to own the underlying real estate. VICI noted that the combined deals with Chelsea Piers and Cabot represented committed capital of $550M at a blended investment yield of approximately 8%.

{kind=link}

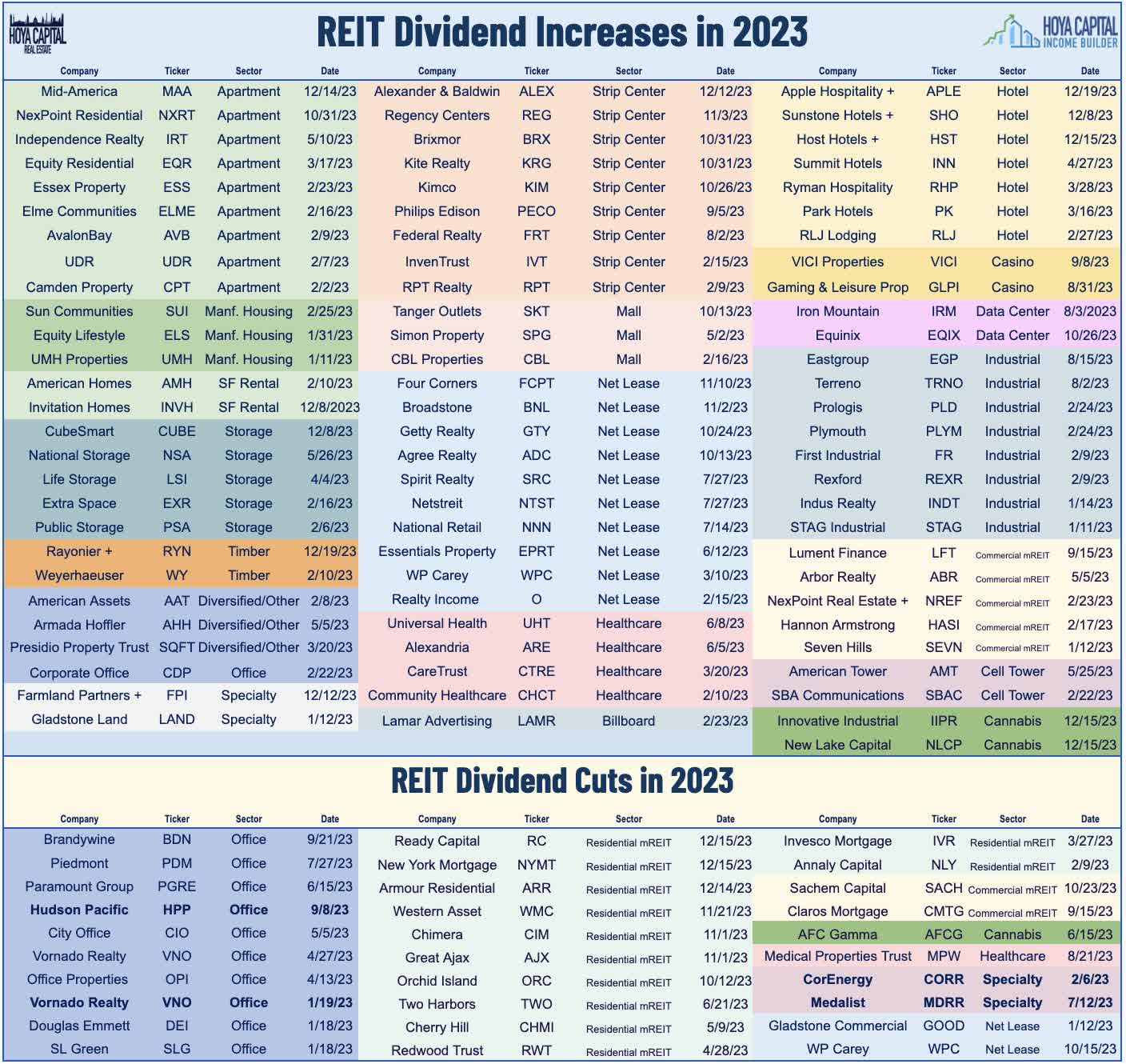

Another week, another wave of REIT dividend hikes and special dividends. Apartment REIT Veris Residential ( VRE ) gained 4% this week after it hiked its quarterly dividend by 5% to $0.0525/share (1.4% dividend yield). VRE - formerly known as Mack-Cali Realty - resumed paying its dividend this past September for the first time since the sale of its office portfolio and its strategic shift to focus on multifamily. Apple Hospitality ( APLE ) - which we own in the Focused Income Portfolio - declared a special cash dividend of $0.05/share, while maintaining its monthly dividend at $0.08/share (5.7% dividend yield). Timber REIT Rayonier ( RYN ) - which we added to the Hoya Capital Housing Index this past month - declared a special one-time cash dividend of $0.20/share. We've now seen 82 REITs raise their dividend this year (including 7 special dividends declared over the past two weeks), while 30 REITs have lowered their payouts. In our State of the REIT Nation report last week, we noted that FFO growth has significantly outpaced dividend growth since the start of the pandemic, which has resulted in a REIT dividend payout ratio of just 66% in Q3 - below the 20-year average of 80%.

{kind=link}

Office : Credit ratings agencies were the "Grinch" for the office sector this week, however, which lagged after posting a powerful rebound over the prior seven weeks, which lifted the Office REIT Index by around 40%. Brookfield Property ( BPYPP ) - the real estate-focused subsidiary of Canada-based asset manager Brookfield Corporation ( BN ) - received a credit rating downgrade by S&P, which cut its issuer credit rating to so-called "junk" status at BB, down two notches from its prior investment-grade rating of BBB-. Brookfield Property owns approximately $130B in total assets, of which roughly half is invested in office assets and the other half invested in regional malls - two of the most structurally troubled property sectors. S&P cited weak office demand and the company's looming debt maturities, noting that its weighted-average debt maturity shrunk below three years in recent quarters, to 2.6 years, which “poses elevated risks.” Brookfield and its subsidiary funds have defaulted on a number of individual office loans over the past year, including $750M in mortgages across a pair of Los Angeles office properties and a $161M mortgage for 12 offices around Washington, DC.

{kind=link}

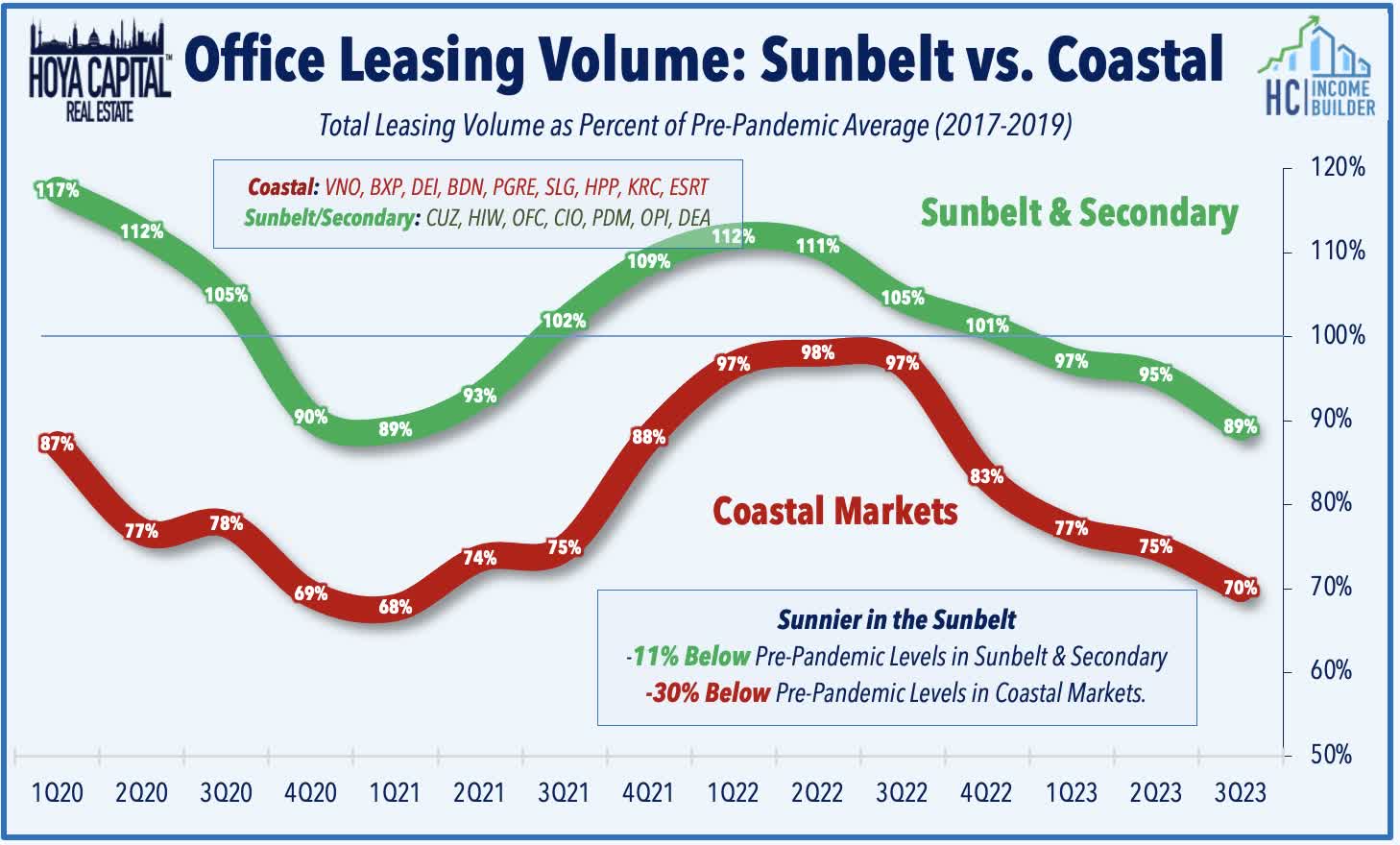

Fitch Ratings published a note this week outlining its downbeat outlook on credit trends in commercial real estate, forecasting that the overall U.S. CMBS loan delinquencies will double from 2.25% today to 4.5% in 2024 and 4.9% in 2025, driven primarily by a "deterioration" in office properties. Vornado Realty ( VNO ) slumped 6% this week after it received a credit rating downgrade from S&P, which lowered its issuer credit rating to “BB+” from “BBB-“ with a negative outlook. Boston Properties ( BXP ) declined 1% after Moody's lowered its senior debt rating to “Baa2” from “Baa1,” but revised its outlook to stable from negative. Highwoods ( HIW ) slipped 4% after S&P affirmed its investment-grade "BBB" credit rating, but revised its outlook to negative. S&P noted that HIW's Sunbelt-focus positions it better than its peers but is "not immune to the broader challenges facing the overall office sector." As noted in our Earnings Recap , leasing volumes for the average Sunbelt-focused office REIT were only about 10% below pre-pandemic levels in the third quarter compared to a 30% relative decline from coastal-focused REITs.

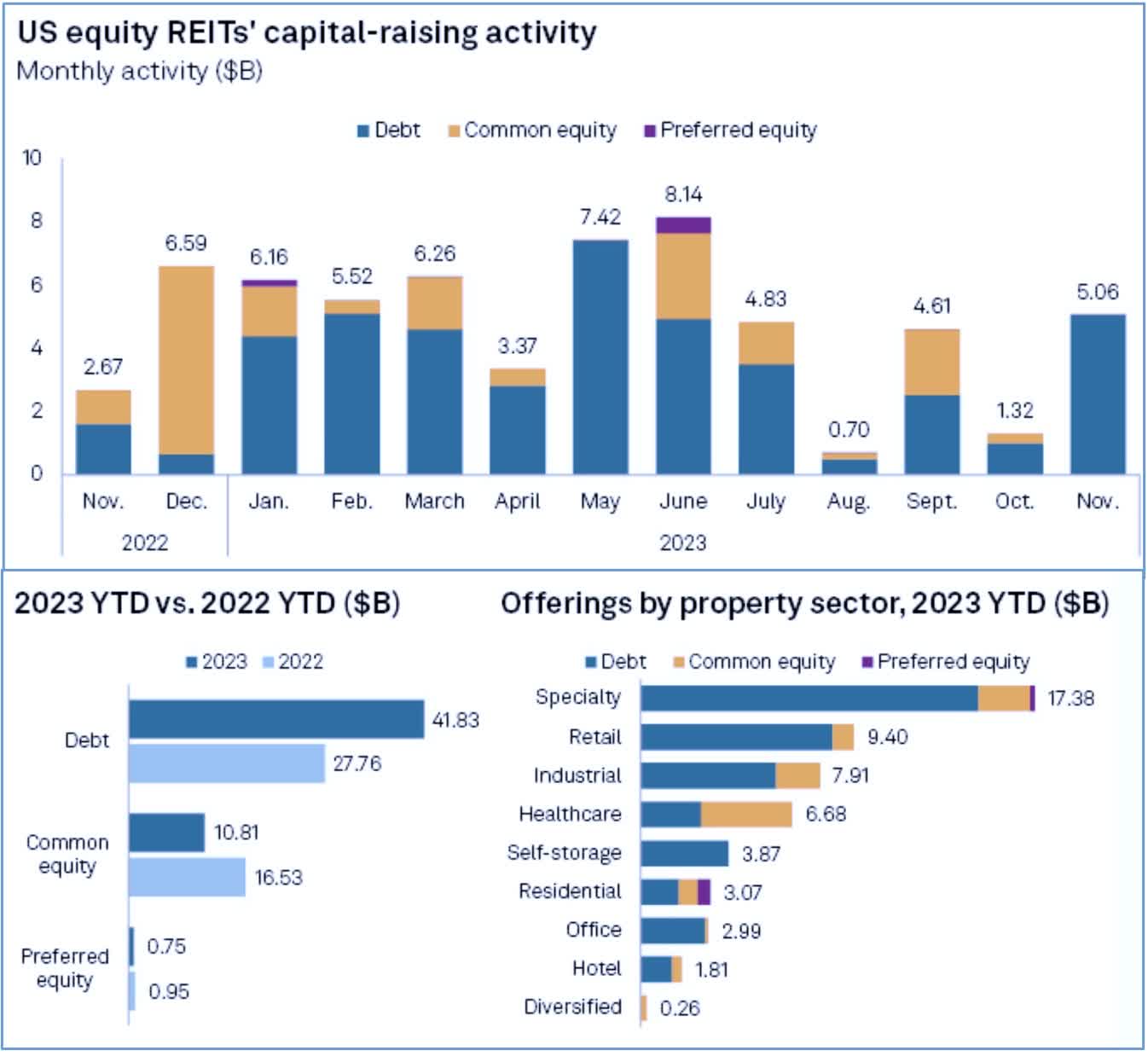

{kind=link}

Healthcare : Sticking with the credit rating theme, Medical Properties Trust ( MPW ) lagged about 3% this week after it received a credit rating downgrade from S&P Ratings, which lowered its issuer credit rating to “B+” from “BB” with a negative outlook. On the upside, small-cap REIT Diversified Healthcare ( DHC ) - which had been teetering on the edge of insolvency earlier this year under its substantial debt load - rallied another 20% this week to lift its year-to-date over 400% after it raised $750M through the issuance of senior notes maturing in January 2026 which will cover all of its outstanding debt maturing in 2024, and for general business purposes. This week, S&P released its monthly report on capital-raising activity across the real estate sector this morning, which showed that many REITs have quickly taken advantage of the pullback in interest rates. REIT capital market activity soared in November, with the industry pulling in $5.06 billion during the month, a massive increase from $1.32 billion raised in October. The total was 89.3% higher than the $2.67 billion the industry collected in November 2022. Nearly all of the capital raised in November came via debt as REITs secured $5.05 billion through note offerings. Common equity offerings accounted for $2.7M, while the remaining approximately $900,000 was obtained through preferred equity offerings.

{kind=link}

Mortgage REIT Week In Review

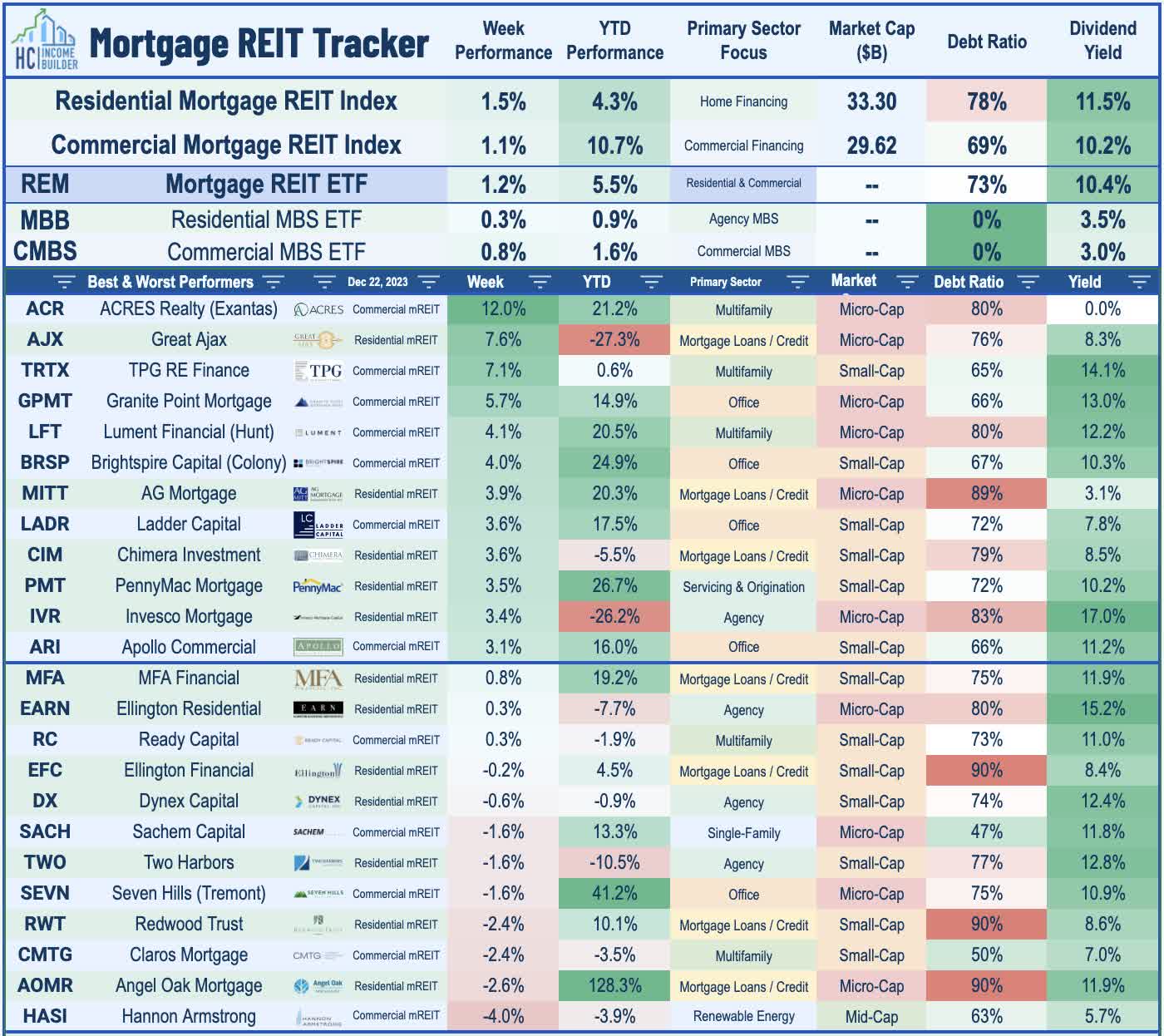

Mortgage REITs were again among the leaders this week, extending their two-month resurgence amid expectations of a pivot towards less-hawkish monetary policy, with the iShares Mortgage Real Estate Capped ETF ( REM ) advancing another 1.2% to push their eight-week gains to over 30%. Granite Point ( GPMT ) rallied 6% in the week after it provided a business update, noting that it resolved a $93M senior loan on a San Diego office property that was on nonaccrual status through a coordinated sale of the collateral property. GPMT provided the new ownership group with a $49 million senior floating rate loan supported by fresh cash equity capital invested in the property by the new sponsor. It will realize a loss of $30M in Q4, which had been "largely reserved for through the previously recorded allowance for credit loss on this loan."

{kind=link}

Granite Point also maintained its quarterly dividend at $0.20/share (13.3% dividend yield), one of six mREITs to maintain their dividends at current levels this week. Invesco Mortgage ( IVR ) maintained its quarterly dividend at $0.40/share (17.7% dividend yield). TPG RE Finance ( TRTX ) maintained its quarterly dividend at $0.24/share (15.2% dividend yield). Franklin BSP Realty ( FBRT ) maintained its quarterly dividend at $0.0355/share (10.0% dividend yield). Two Harbors Investment ( TWO ) maintained its quarterly dividend at $0.45/share (12.8% dividend yield). Cannabis-focused mREIT Chicago Atlantic Real Estate ( REFI ) maintained its quarterly dividend at $0.47/share (11.8% dividend yield). The average residential mREIT now pays a dividend yield of 11.5%, while the average commercial mREIT yields 10.2%.

{kind=link}

On the downside this week, renewable energy-focused lender Hannon Armstrong ( HASI ) dipped 4% after it announced that its Board of Directors had approved a plan to revoke its Real Estate Investment Trust status and become a taxable C-Corporation, effective January 1, 2024. HASI - which converted to a REIT back in 2013 - remarked that its existing net operating losses ("NOLs") effectively negate the tax benefits of REIT status, noting that the conversion "is not expected to have any material impact... [but] provides greater flexibility." HASI was the only REIT focused on renewable energy markets, and manages an $11.5B portfolio ($5.5B on its own balance sheet) comprised primarily of senior debt and preferred equity investments in solar and wind energy projects. HASI has been the target of several "short reports" over the past year and is currently one of the most heavily shorted REITs with a short interest of over 15%. Muddy Waters released a short report in July alleging that HASI is engaged in misleading accounting practices related to the valuation of their renewable energy portfolio.

{kind=link}

2023 Performance Recap & 2022 Review

With just one week left in 2023, the Equity REIT Index is now higher by 6.3% on a price return basis for the year (10.2% on a total return basis), while the Mortgage REIT Index is higher by 5.6% (+17.5% on a total return basis). This compares with the 22.7% gain on the S&P 500 and the 13.1% gain for the S&P Mid-Cap 400 . Within the real estate sector, twelve property sectors are now in positive territory on the year, led by Data Center, Regional Malls, and Hotel REITs, while Net Lease and Farmland REITs have lagged on the downside. At 3.90%, the 10-Year Treasury Yield has climbed by 2 basis points since the start of the year - up from its 2023 intra-day lows of 3.26% in April - but down sharply from peaks above 5.0% in mid-October. Following the worst year for bonds in decades, the Bloomberg US Bond Index is higher by 5.0% this year. WTI Crude Oil - perhaps the most important "swing" inflation input - is now lower by 2.0% this year, while Natural Gas has dipped 64.3%.

{kind=link}

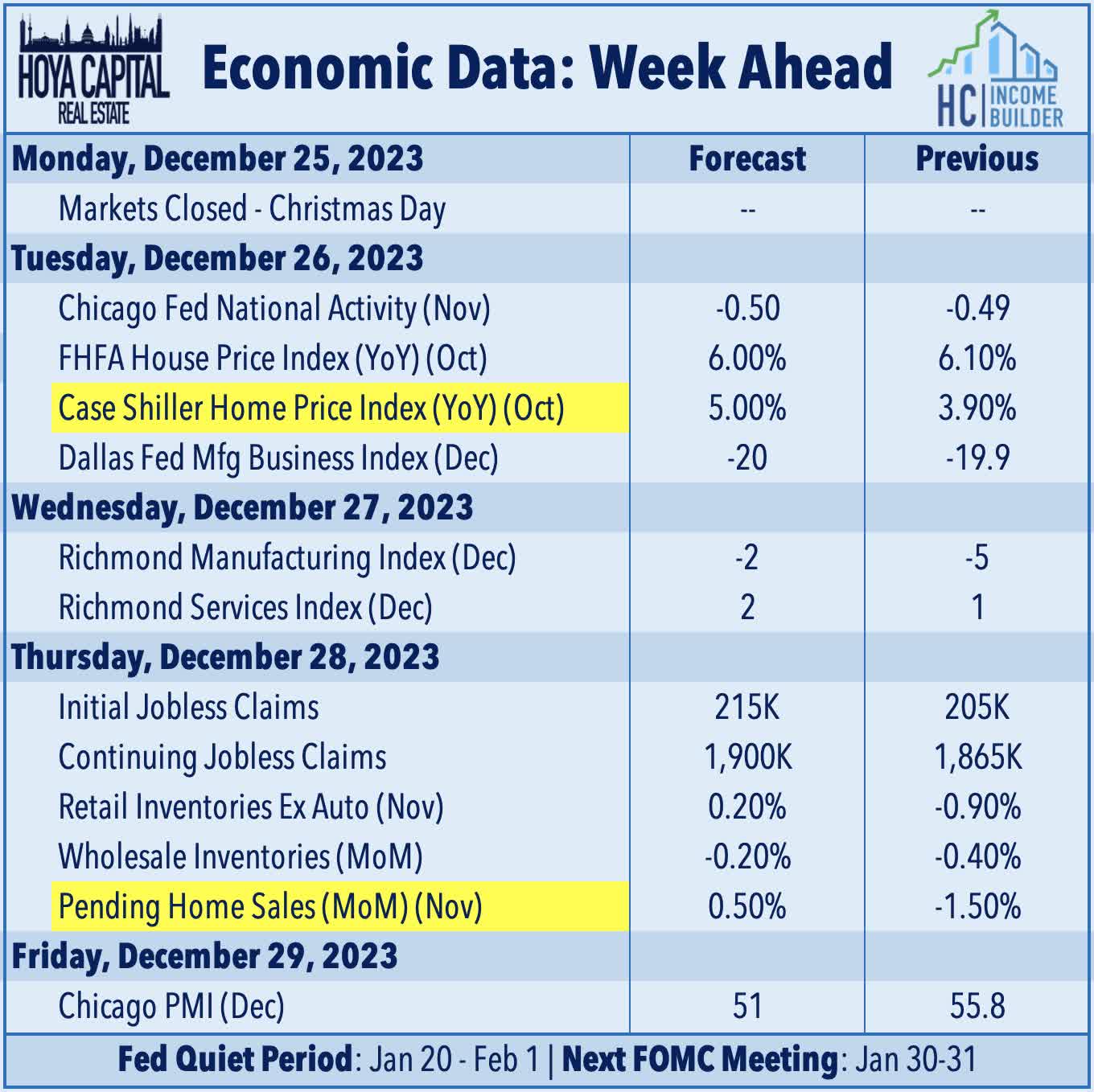

Economic Calendar In The Week Ahead

The economic calendar slows down in the holiday-shortened week ahead. US equity and bond markets will be closed on Monday for Christmas. On Tuesday, we'll see home price data via the Case Shiller Home Price Index and the FHFA Home Price Index , which are expected to show a continued reacceleration in home price appreciation since posting monthly declines in seven-straight months from late 2022 through early 2023. Historically low inventory levels - a function of a decade-long period of underbuilding of single-family homes after the Great Financial Crisis - have outweighed the headwinds on valuations from soaring mortgage rates. On Thursday, we'll see Pending Home Sales data for November, which is expected to show the first monthly increase in sales activity in six months, reflecting some of the early positive effects on housing market activity from this pullback in mortgage rates. We'll also be watching Jobless Claims data on Thursday, and several notable PMI reports throughout the week. Merry Christmas!

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

Disinflation: A Gift That Keeps Giving