REIT - Disinflation Goes Global

2024-01-14 09:00:00 ET

Summary

- U.S. equity markets resumed their rally this week, while interest rates fell sharply after a critical slate of inflation data pointed towards a continuing "normalization" of inflation towards pre-pandemic levels.

- While CPI data was best characterized as "lukewarm" - showing some conflicting signals in December, PPI data along with reporting from China showed outright deflation in goods-related categories.

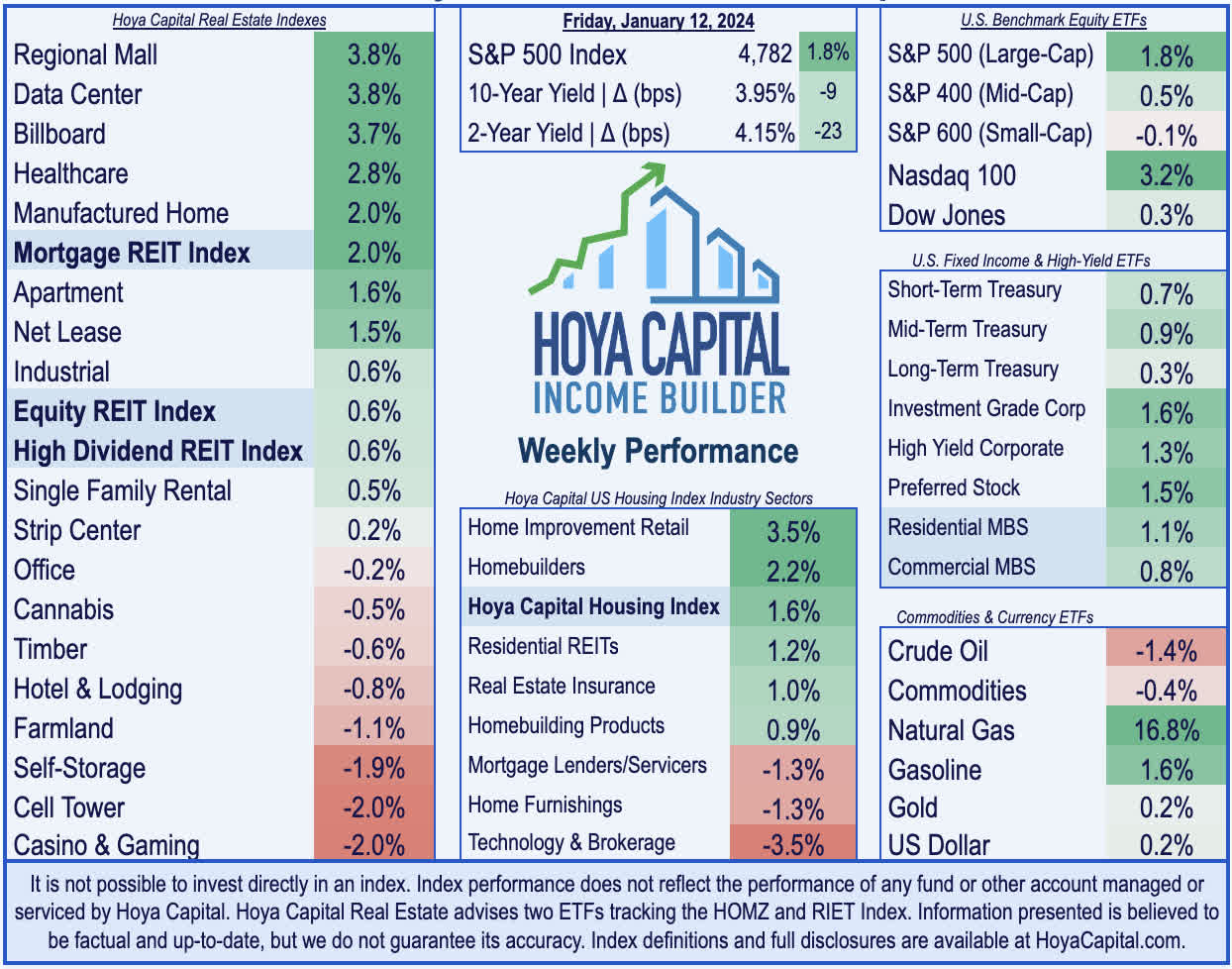

- Returning to the "win column" a week after snapping its nine-week winning streak, the S&P 500 advanced 1.8% on the week - closing within a half-percent of fresh record highs.

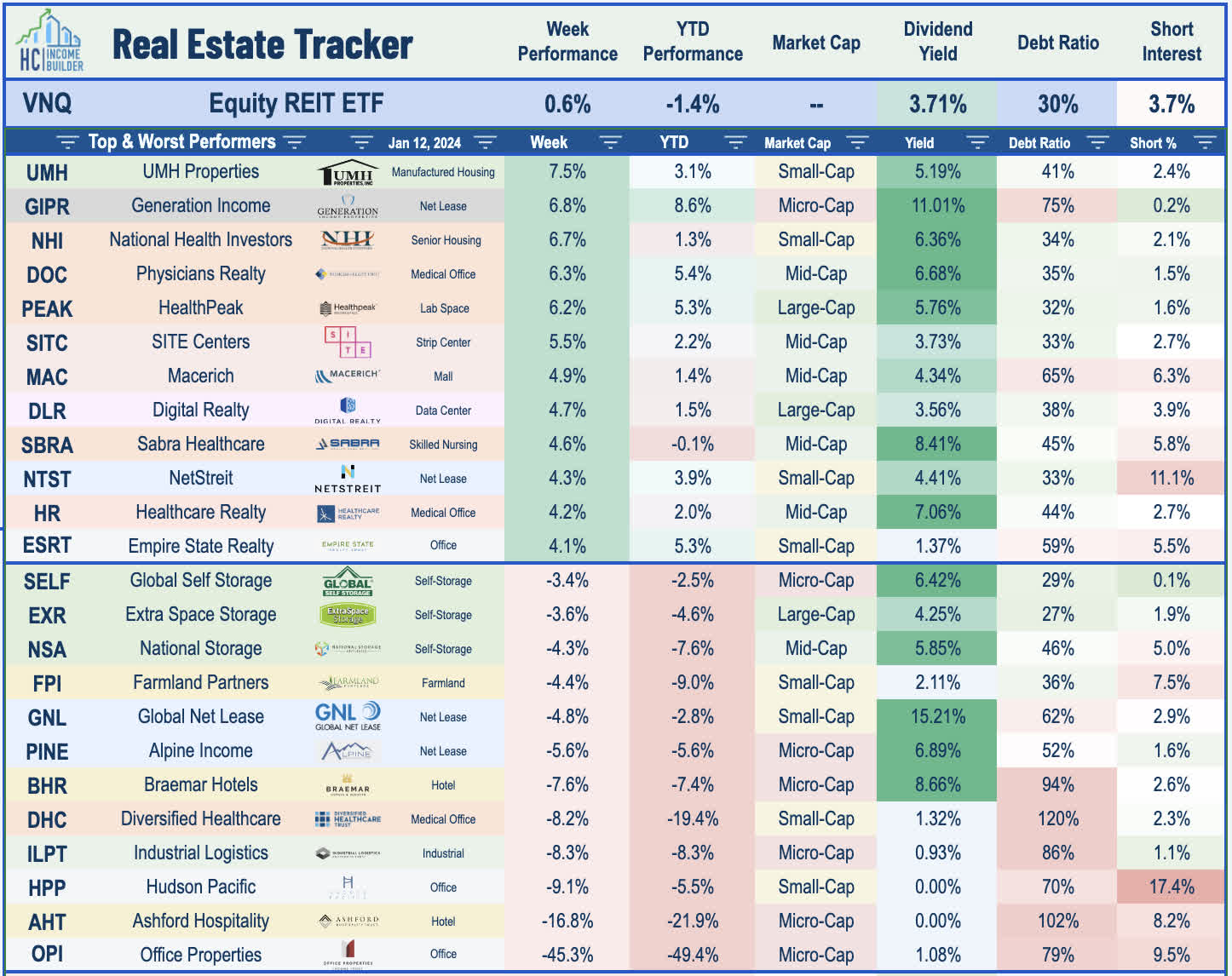

- Real estate equities were mixed this week as tailwinds from a continued retreat in benchmark interest rates were partially offset by some mixed business updates. The Equity REIT Index advanced 0.6% this week.

- REITs were very active on the capital-raising front this week, raising nearly $4B in fresh capital at a time when many private market peers continue to face extremely challenging financing conditions.

Real Estate Weekly Outlook

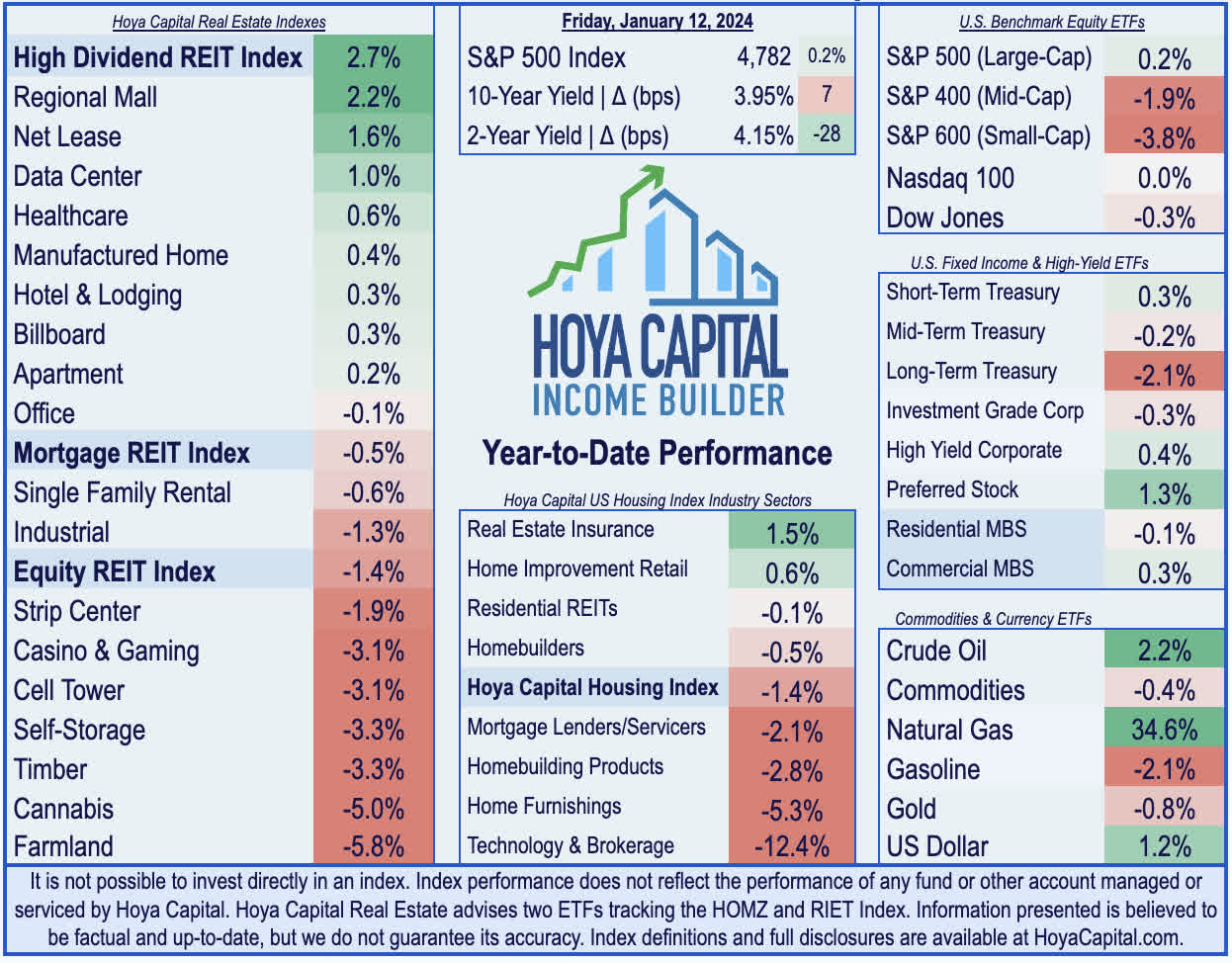

U.S. equity markets resumed their rally this week - advancing in 10 of the past 11 weeks - while benchmark interest rates fell sharply after a critical slate of inflation data - both domestically and across Asia and Europe - pointed towards a continuing "normalization" of inflation rates towards pre-pandemic levels and reinforced expectations of pending Fed rate cuts. While consumer price data was best characterized as "lukewarm" - showing some conflicting signals in December - producer price data was far more definitive, showing outright deflation across goods-related categories. Internationally, data from China showed that deflation remains the more pressing threat, with price levels across the region seeing their longest streak of declines since 2009.

{kind=link}

Hoya Capital

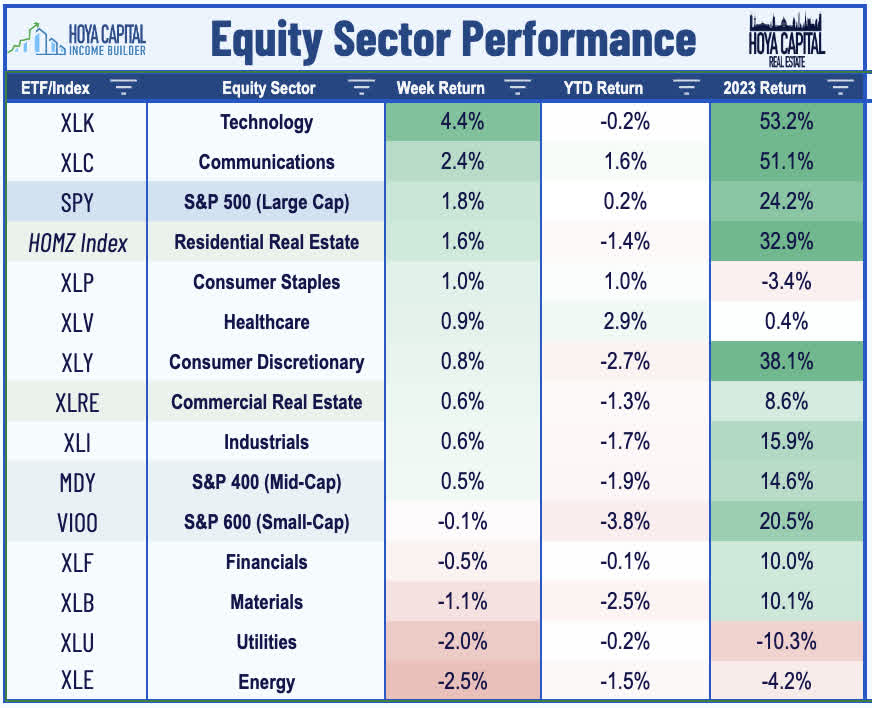

Returning to the "win column" a week after snapping its nine-week winning streak, the S&P 500 advanced 1.8% on the week - closing within a half-percent of fresh record highs. Gains were notably top-heavy this week, however, as the Mid-Cap 400 posted muted gains of 0.5%, while the Small-Cap 600 finished lower by 0.1%. The tech-heavy Nasdaq 100 - which surged over 50% in 2023 - picked up where it left off with gains of over 3% on the week. Real estate equities were mixed this week as tailwinds from a continued retreat in benchmark interest rates were partially offset by some mixed business updates ahead of REIT earnings season later this month. The Equity REIT Index advanced 0.6% this week, with 10-of-18 property sectors in positive territory, while the Mortgage REIT Index rallied 2.0%. Homebuilders were among the upside standouts following data showing a rebound in mortgage demand and after a healthy dividend hike from Lennar.

{kind=link}

Hoya Capital

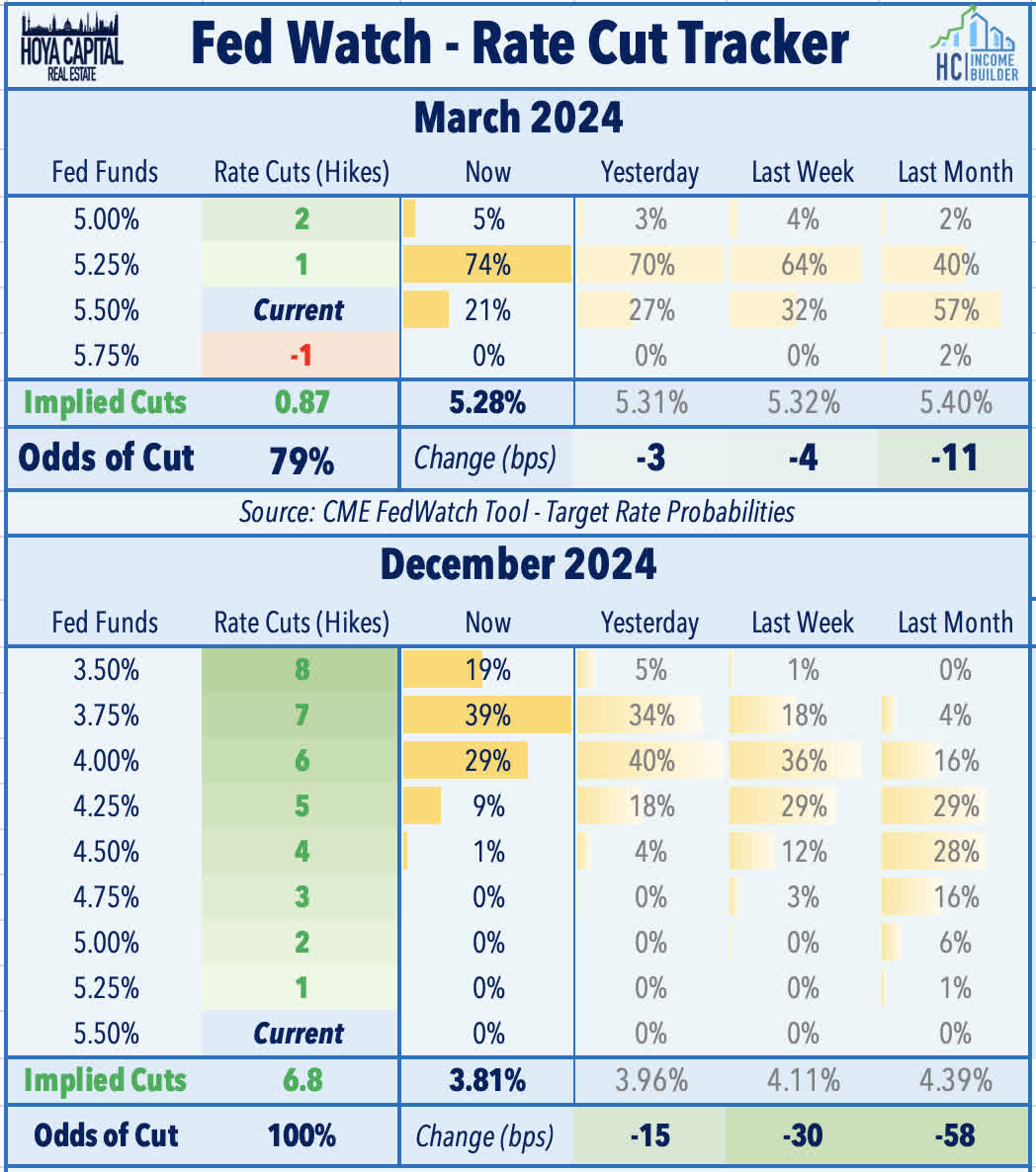

Bonds rallied across the maturity and credit curve this week as benchmark interest rates resumed their sharp retreat, reversing the prior week's jump on the heels of decent employment data. The policy-sensitive 2-Year Treasury Yield plunged by 23 basis points to 4.15% - its lowest close since May, and down from its late October highs of 5.22%. Movement on the longer-end of the curve was more muted, with the 10-Year Treasury Yield retreating by 5 basis points this week to 3.95% - still above the late-December low of 3.79%. Despite some hawkish pushback from a trio of Fed Presidents, swaps markets are now pricing in a 79% probability that the Fed will cut interest rates for the first time this cycle during its March meeting, up from 50% a week ago. Looking longer term, swaps markets still see a median year-end Federal Funds rate of 3.81%, implying nearly 7 quarter-point rate cuts during 2024. At its last FOMC meeting in December, the Fed's median forecast called for 3 cuts.

{kind=link}

Hoya Capital

Commodities remained in focus this week, given their significance for the near-term inflation outlook. WTI Crude Oil - the key "swing" inflation input - slipped 1.4% this week to $73/ barrel, which is 6% above the late-December low but 22% below the September highs. Consumer gasoline prices remained near two-year lows at $3.07/gallon, down about 40% from the 2021 peak. Natural Gas surged over 15% this week on forecasts of below-average temperatures across the Northeast and Midwest over the next several weeks. Six of the eleven GICS equity sectors finished higher on the week, led on the upside by Technology ( XLK ) stocks. Industrials ( XLI ) stocks were among the laggards as airplane maker Boeing ( BA ) plunged as its flagship 737 MAX faced new scrutiny after a door detached from a newly-delivered plane during an Alaska Airlines flight, promoting a successful emergency landing. Financials ( XLF ) stocks also lagged following a disappointing start to earnings season.

{kind=link}

Hoya Capital

Real Estate Economic Data

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

{kind=link}

Hoya Capital

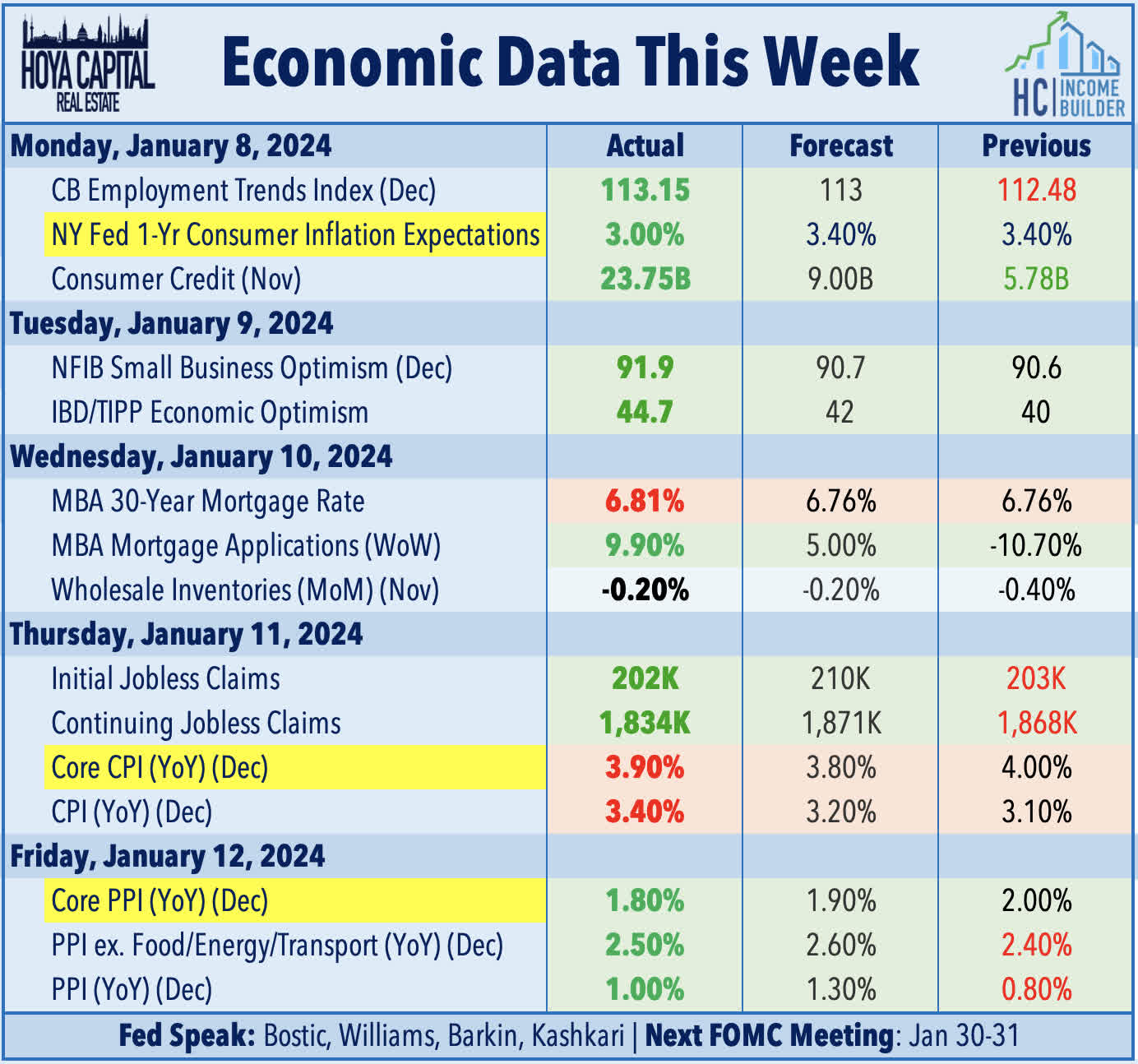

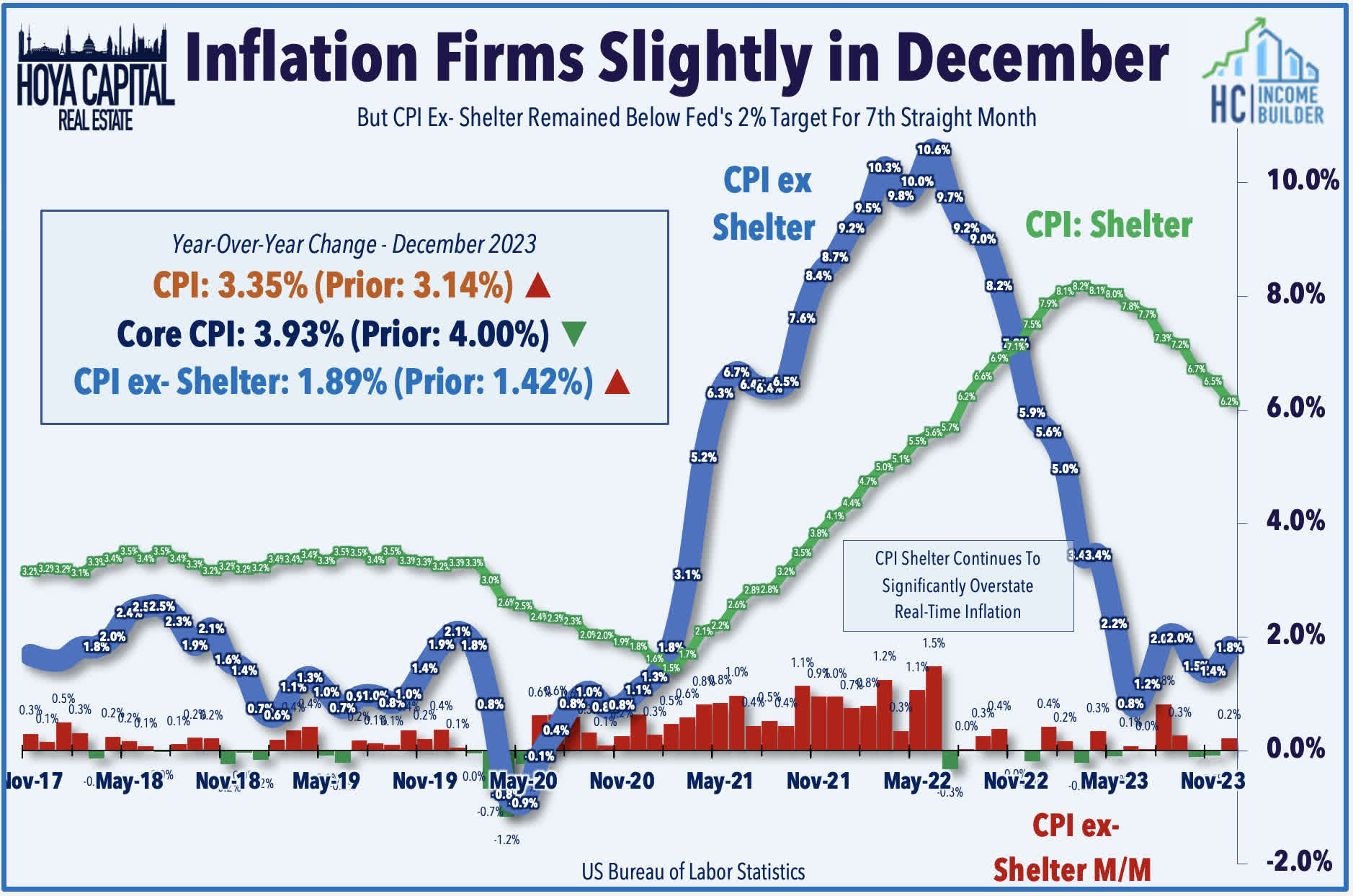

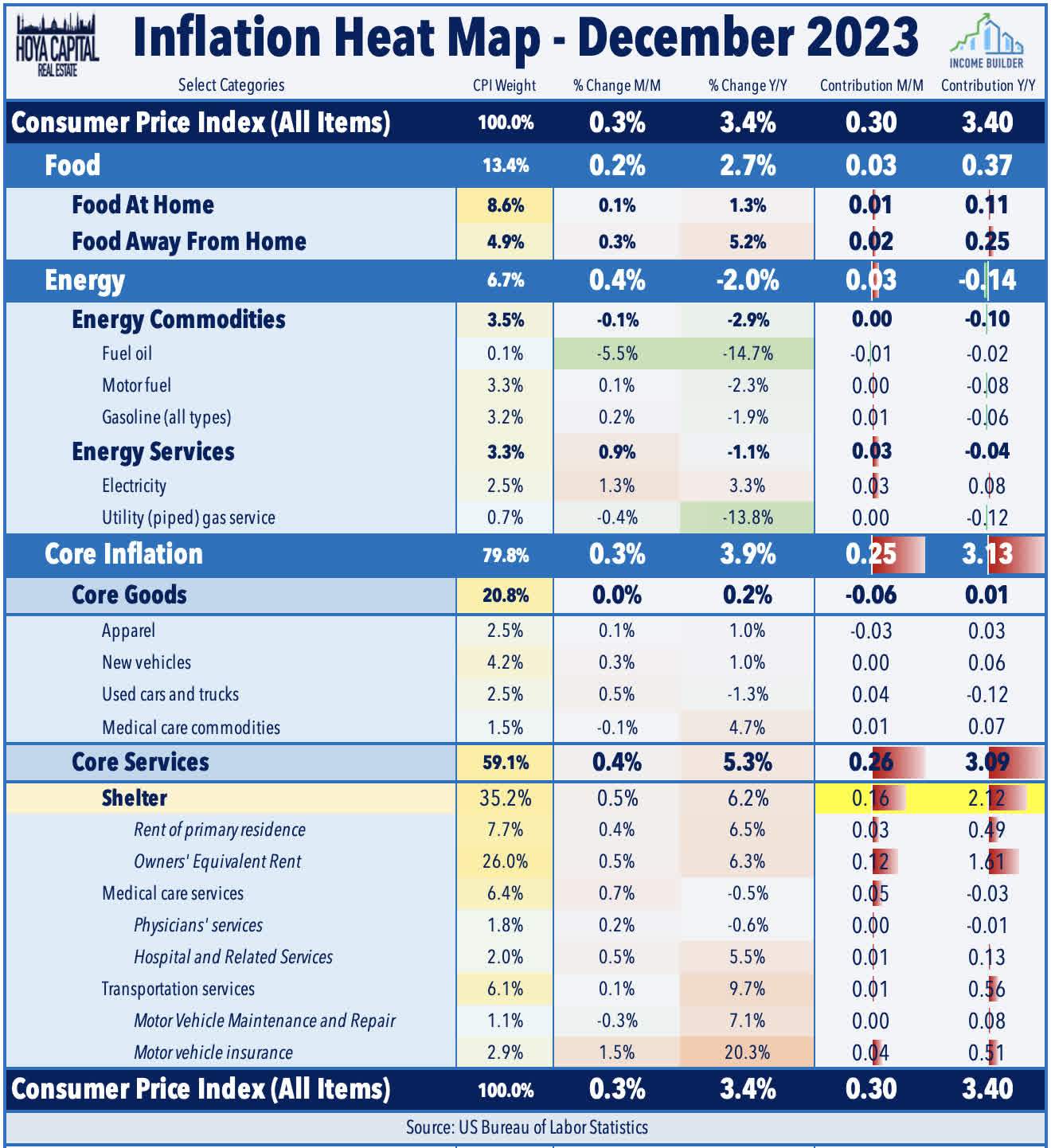

All eyes were on the Consumer Price Index report this week, which was perhaps best characterized as "lukewarm" - showing some conflicting signals in December following a period of definitive disinflation in the prior several months. Headline CPI increased 0.3% month-over-month and increased by 3.35% from a year ago - above consensus estimates of 0.2% and 3.2%, respectively. Core CPI - which excludes food and energy - rose 0.3% on the month and 3.93% on the year, which was also slightly above expectations. Beneath the surface, however, we see a continued distortion from the lagged recognition of shelter inflation, which accounted for more than half of the core CPI increase. CPI-ex-Shelter - the metric we watch most closely given the substantial issues in the BLS' shelter inflation methodology - rose a more modest 0.2% for the month and 1.89% for the year, which was the seventh consecutive month below the Fed's 2% policy objective.

{kind=link}

Hoya Capital

Diving deeper into the data, we note that a reported increase in gasoline inflation - despite being lower by an average of 6% during December per the EIA - also contributed to the upside surprise. Prior to the CPI report, New York Fed data on Monday showed that inflation expectations declined in December to their lowest level since early 2021, easing some concern over an entrenchment of elevated inflation levels. Per the Survey of Consumers, Americans expect the inflation rate to average 3.0% over the next year - down from 3.4% last month and 8.5% at the peak in early 2022. Three-year inflation expectations eased to 2.6% - down from a peak of 4.2% and below the 2015-2019 average of 3.0%.

{kind=link}

Hoya Capital

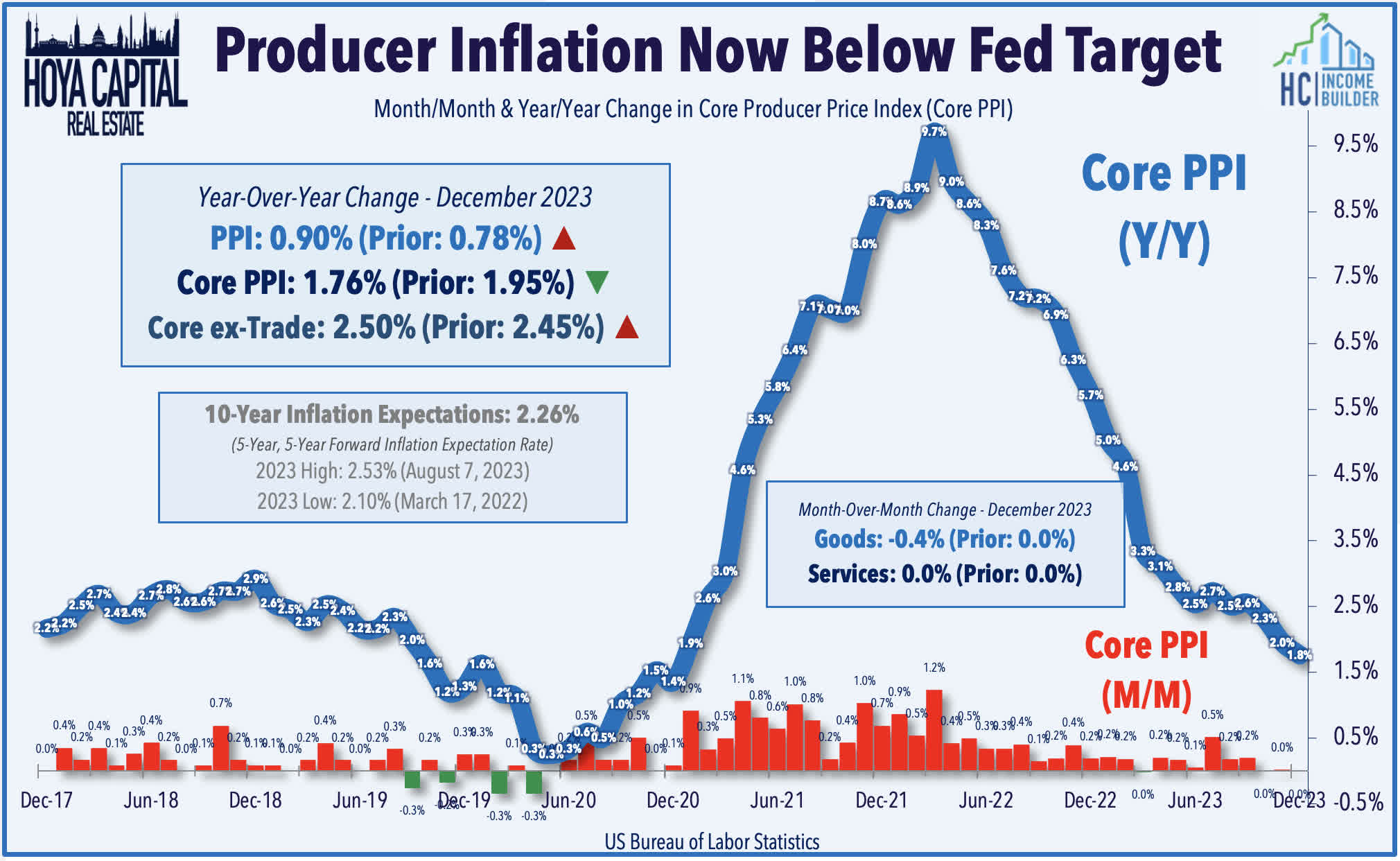

Following the slightly hotter-than-expected CPI report, the Producer Price Index the following day showed a more definitive moderation in price pressures in December. The Headline PPI declined 0.1% in December - below the 0.1% increase expected - which, combined with revisions to prior months, resulted in a year-over-year increase of just 0.9%. Declines in fuel and transportation costs - both on the goods and services side - continued to drive the deflation in December. Core PPI - which excludes food and energy - was flat on the month, which dragged its year-over-year increase to 1.8% - down sharply from the peak of 9.3% in early 2022. Of note, the PPI Services index - which had been an area of "sticky" inflationary trends - was flat for a third straight month, pulling the annual increase down to 1.8%. The PPI Goods index declined by -0.4% for the month and was lower by -0.7% from last year. The forward-looking metrics within the report showed further deflation coming through the pipeline. The index of partially finished goods declined 0.6% on the month while prices of raw materials plunged 4.4%.

{kind=link}

Hoya Capital

Equity REIT Week In Review

Best & Worst Performance This Week Across the REIT Sector

{kind=link}

Hoya Capital

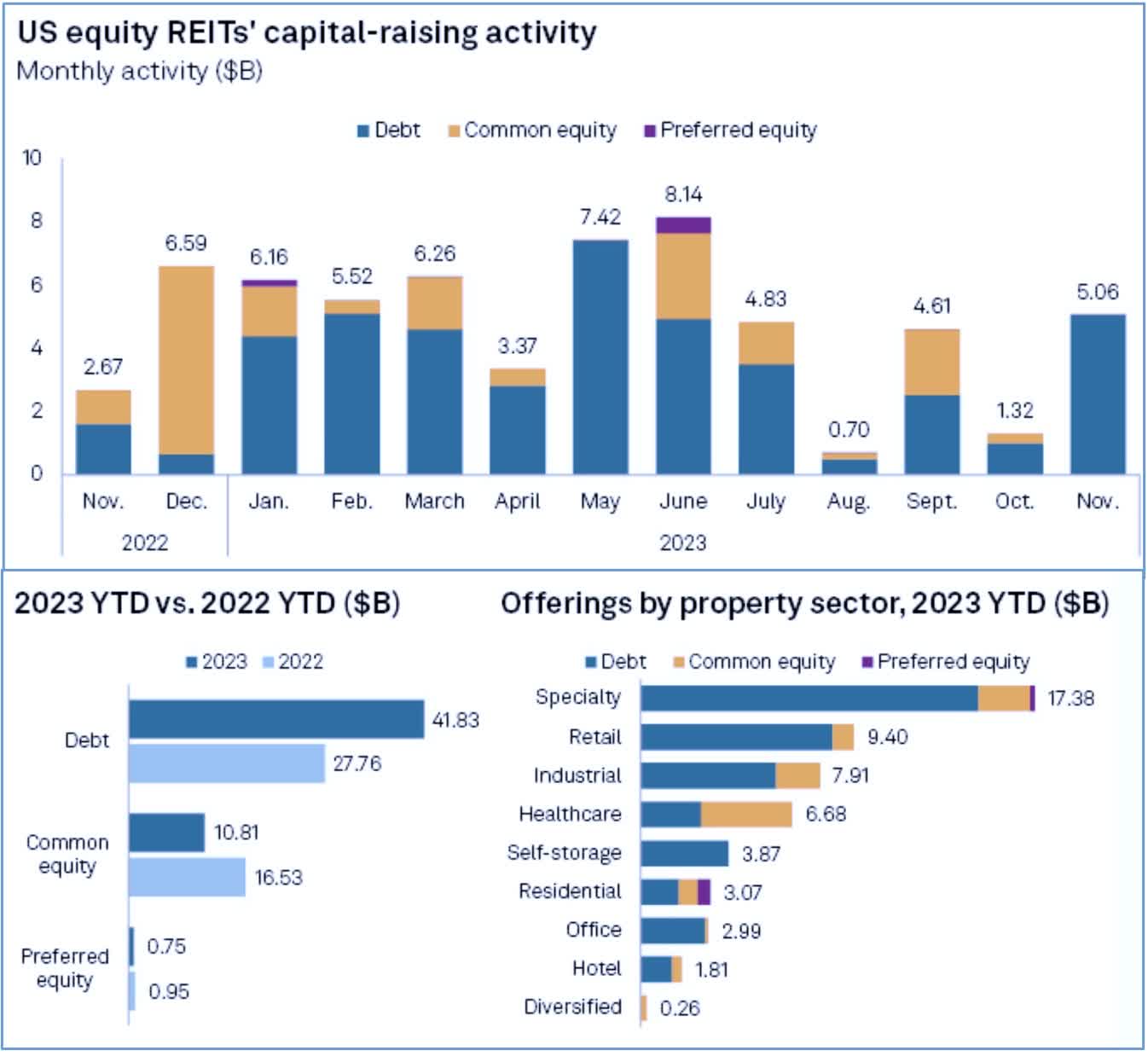

REITs were very active on the capital-raising front this week, raising nearly $4B in fresh capital at a time when many private market peers continue to face extremely challenging financing conditions. Net lease REIT Realty Income ( O ) raised $1.25B in debt across two tranches: $450 million in five-year notes at a 4.75% interest rate and $800 million of ten-year bonds at a 5.125% rate. Four strip center REITs combined to raise over $1.5B in long-term bonds: Regency Centers ( REG ) raised $400M in ten-year unsecured bonds at a 5.25% interest rate, Brixmor ( BRX ) raised $400M in ten-year unsecured bonds at a 5.50% rate, Federal Realty ( FRT ) raised $425M in five-year exchangeable notes at a 3.25% interest rate, and Kite Realty ( KRG ) raised $350M in ten-year unsecured notes at a 5.50% rate. Elsewhere, office REIT Kilroy ( KRC ) raised $400M of twelve-year unsecured bonds at a 6.25% interest rate. Two retail-focused REITs raised equity capital: Acadia Realty ( AKR ) raised $116M in common equity through a secondary offering of 6.9M shares at $16.75/share, while NETSTREIT ( NTST ) raised $173M in common equity through a forward sale agreement of 9.6M shares at $18/share. S&P reported last month that REIT capital market activity picked-up considerably in the final months of 2023.

{kind=link}

Hoya Capital

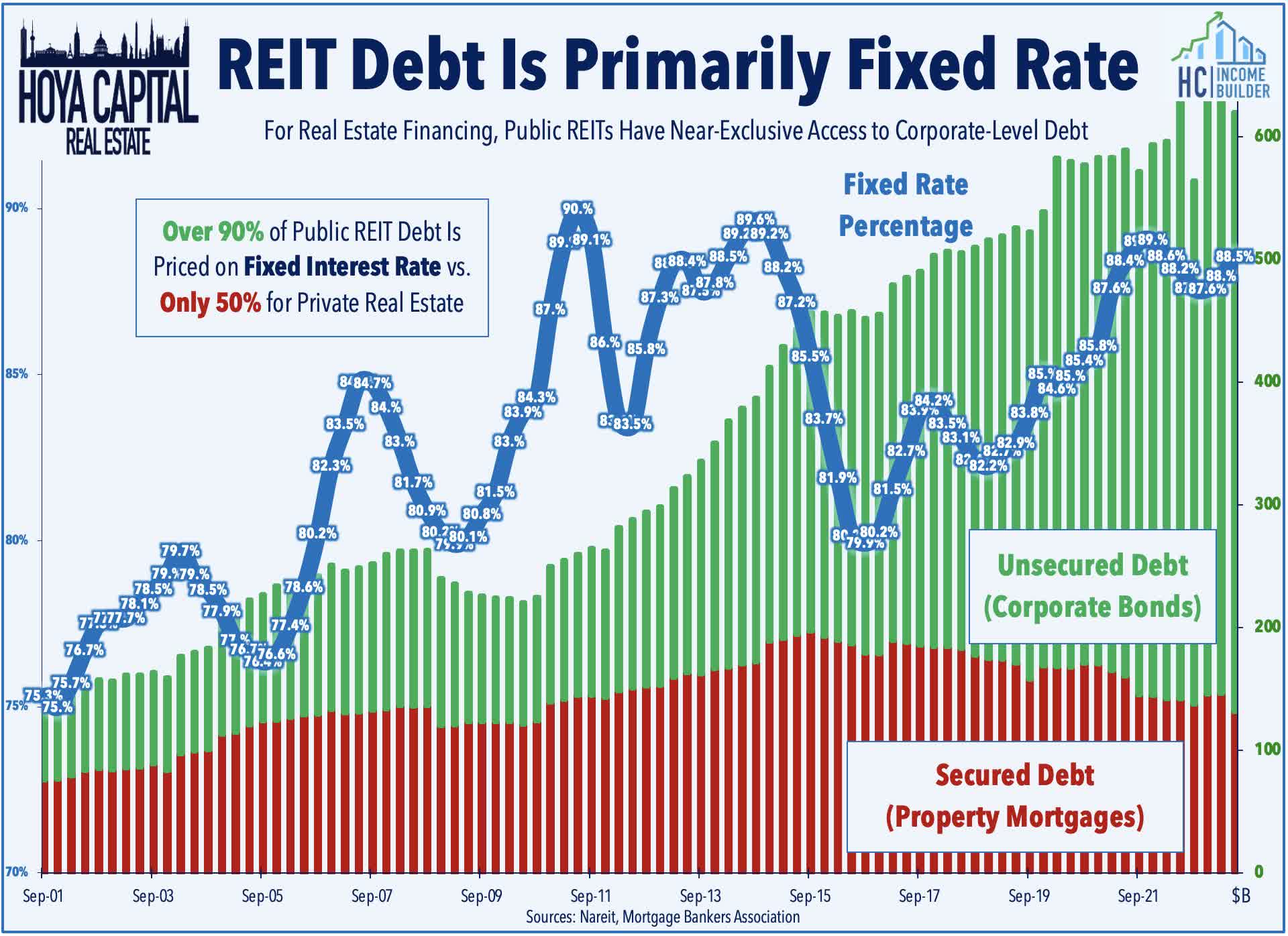

Office: Underscoring the continued headwinds facing the more highly-levered real estate portfolios, small-cap Office Properties Income ( OPI ) plunged more than 40% this week after slashing its dividend to $0.01/share (0.65% dividend yield), a -96% decrease from its prior dividend of $0.25. OPI - which had previously cut its dividend in half in early 2023 - cited a "deterioration in market conditions since the first half of 2023" and the need to increase liquidity. Three of the four REITs that are externally-managed by RMR Group ( RMR ) have now slashed their dividend to $0.01/share over the past two years, with OPI now joining Diversified Healthcare ( DHC ) and Industrial Logistics ( ILPT ). The suite of four RMR-advised REITs entered the rate-hiking period with balance sheets that were among the weakest across the public REIT sector with characteristics - high usage of mortgage debt and variable rate loans - that are more commonly seen among private equity real estate portfolios. Access to long-term debt is perhaps the most distinct competitive advantage of the public REIT model, but it's an advantage that hardly gave public REITs much of an edge when debt capital was cheap and plentiful in the "zero-rate" economic environment of the 2010s. Compared to private institutions, publicly-traded REITs have far greater access to fixed-rate unsecured debt - which is usually in the form of 5-10 year corporate bonds.

{kind=link}

Hoya Capital

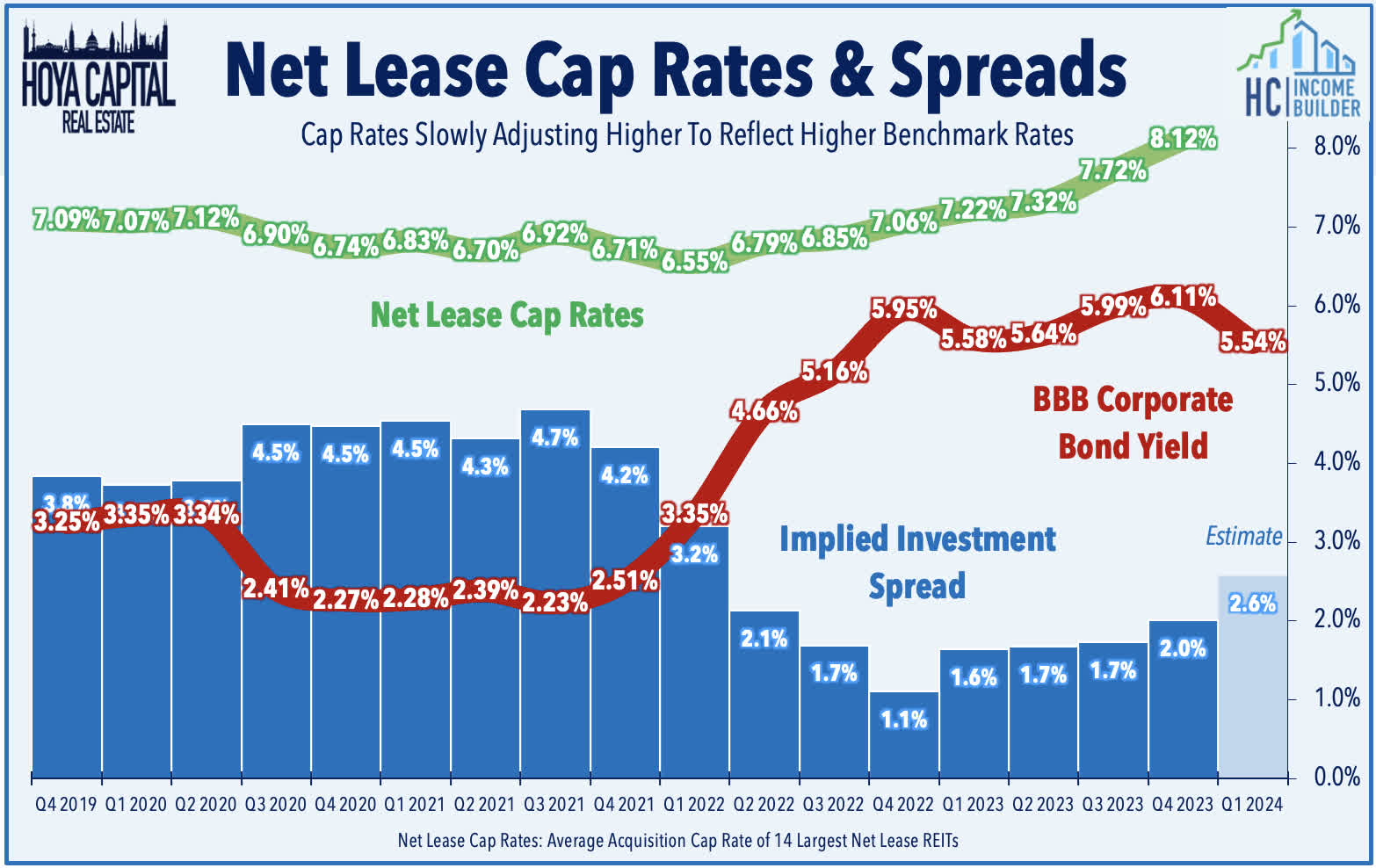

Net Lease : We saw business updates from a half-dozen net lease REITs this week, which together showed that private market cap rates are slowly-but-surely adjusting to the higher rate environment, providing more attractive investment spreads for these net lease REITs. Realty Income ( O ) - the largest net lease REIT - advanced nearly 2% after it reported that it completed $2.7B in acquisitions in Q4 2023 and $9.5B for the full year 2023 at initial cap rates of 7.6% in Q4 and 7.1% for the full year. Both of these reported cap rates were the highest since 2012, and compare to a pandemic-era low of 5.3% in 2021. Small-cap NETSTREIT ( NTST ) rallied 4% after it affirmed its 2023 guidance and provided a solid initial outlook for 2024. NTST continues to expect FFO growth of 5.2% this year - above the sector average of around 1% - and sees 2024 FFO growth of 3.3% at the midpoint of its range. NTST also noted that it completed $119M in acquisitions in Q4 and $481M for full-year 2023, each at an average cap rate of 7.2%. By comparison, NTST's reported acquisition cap rate was 6.7% in 2022 and 6.5% in 2021. Getty Realty ( GTY ) - which focuses on gas and truck service stations - was little changed after initiating 2024 guidance calling for full-year AFFO growth of 2.4%, representing a slight deceleration from the 4.9% growth achieved in 2023.

{kind=link}

Hoya Capital

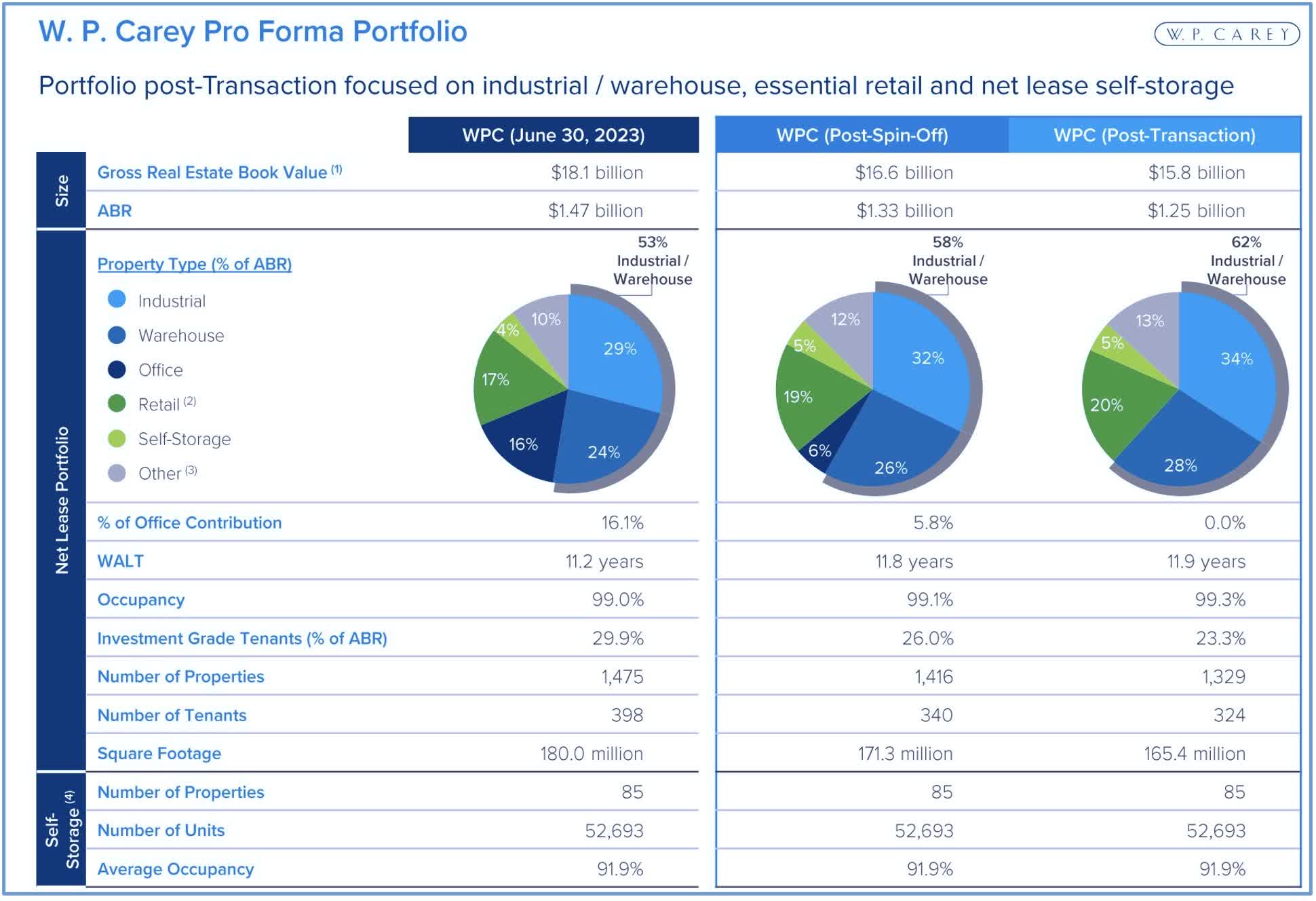

Sticking in the net lease space, Postal Realty ( PSTL ) was little-changed after it reported that it acquired 75 properties leased to the USPS for $20.7M. For full-year 2023, it acquired 223 properties for $78M at a weighted average cap rate of 7.7% - up from 6.7% in 2022. Gladstone ( GOOD ) gained 3% after it provided a leasing update, noting that it signed 1.43M square feet of leases in full-year 2023 with a weighted average lease term of 10.8 years, achieving straight-line rent increases of 13%. W.P. Carey ( WPC ) - which is in the midst of a portfolio shift to focus on industrial properties - rallied 4% this week after it detailed its recent acquisition activity, noting that it completed $320 million of investments in the fourth-quarter at a 7.7% average cap rate. WPC reported a continued uptick in acquisition cap rates to 7.7%, which compares to the recent lows of 5.6% in Q2 of 2022. WPC also announced that it sold a portfolio of 70 office properties net leased to the State of Andalusia for approximately $359M, marking further progress in its "strategic exit from office" which WPC announced last November. The portfolio was the largest component of its Office Sale Program - the office assets that were retained by WPC and excluded from the spin-off into Net Lease Office Properties ( NLOP ). Concurrently, NLOP rose nearly 30% this week after it announced the sale of four office properties in December 2023 for gross proceeds of $43.1M. After the sale, NLOP owns 55 office properties: 50 in the U.S. and five in Europe.

{kind=link}

Hoya Capital

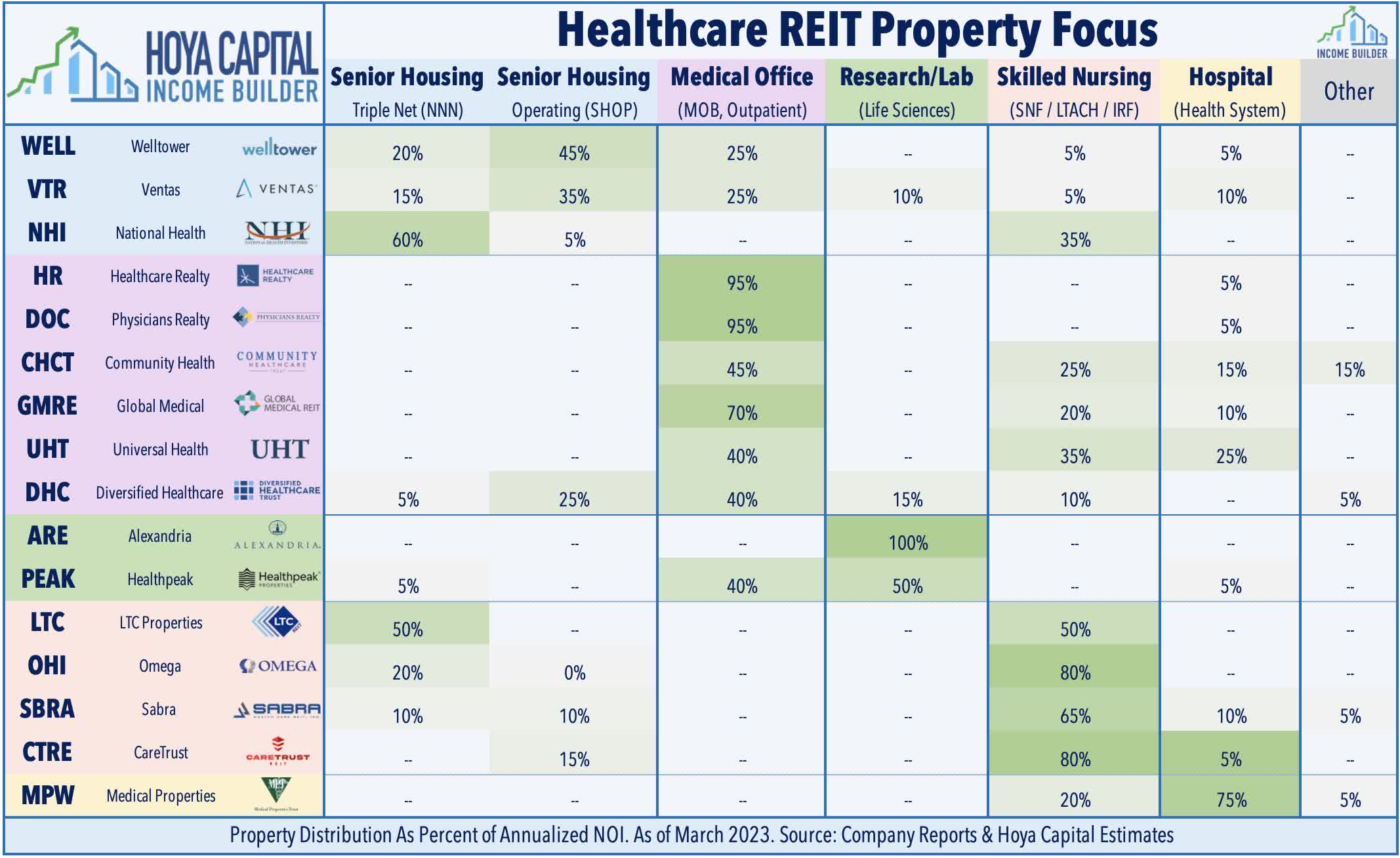

Healthcare : A handful of healthcare REITs provided business updates as well. Medical office REIT Healthpeak ( PEAK ) rallied 6% this week after it sold a 65% interest in its recently-completed Callan Ridge lab campus in San Diego to Breakthrough Properties at a $236M valuation, which generated $130M in proceeds for PEAK. The partial sale of the full-leased two-facility campus was completed at a cash capitalization rate of 5.3% ($1,275 per square foot) - a strong print that lifted its MOB-focused peers this week as well. Healthcare Realty ( HR ) rallied 4% after reporting that it completed $338M of asset sales during the fourth quarter, bringing its full-year sales total to $656M at an average cap rate of 6.6%. With the proceeds, HR was able to fully repay the balance on its revolving credit facility. Skilled nursing REIT LTC Properties ( LTC ) rallied 4% after it completed its transactions involving its 35-property Brookdale Senior Living portfolio - a deal initially announced in early 2023 after Brookdale chose not to renew its master lease with LTC. Of the 35 properties, 17 were ultimately re-leased to Brookdale under a new master lease, while 8 were sold, 5 were transferred to Oxford Senior Living, and 5 were transferred to Navion. With the deal, LTC reduced its exposure to Brookdale from roughly 8.4% of NOI to 5%. LTC noted that all rent has been fully replaced, and that it generated $17M in net gains from the sales.

{kind=link}

Hoya Capital

Single-Family Rental : Invitation Homes ( INVH ) - the largest single-family rental REIT owning roughly 85,000 homes - was little-changed this week after it announced a deal to provide third-party property management services to 14,000 single-family homes for an undisclosed partner. The homes will be within its existing markets - predominantly Atlanta, Phoenix, Dallas, Carolinas, Orlando, and Tampa. The partner is presumed to be Starwood Capital , as Bloomberg reported last October that it had obtained a letter indicating that INVH would take over management of 8,500 homes owned by Starwood Capital, but INVH had declined to confirm or deny the report. INVH commented that it marks the "next phase of evolution" for the company, leveraging its existing scale and operations in these markets to create a "capital light" fee-based business. We've forecast for several years that SFRs would eventually enter the third-party property management business, similar to how self-storage REITs have leveraged their scale and operational expertise to develop a sizable high-margin ancillary revenue stream.

{kind=link}

Hoya Capital

Apartment : We discussed similar themes in our updated Apartment REIT Rankings report. Apartment REITs were among the weakest-performing property sectors for a second-straight year in 2023 - lagging even the battered office sector - despite delivering relatively solid mid-single-digit earnings growth. Following two years of record-setting rent growth, residential rents decelerated in 2023 alongside a broader cooling of inflationary pressures, with multifamily rents seeing a particularly sharp cooldown amid supply headwinds. The wave of pandemic-era development - started at a time when rents were rising double-digits - resulted in a record-year of new deliveries in 2023 with similarly elevated supply levels. The pundit-predicted rental market "crash" has remained elusive, however, as demand has stayed surprisingly robust, driven by the combination of resilient job growth, homeownership unaffordability, favorable demographics, and elevated inbound immigration. Pockets of rate-driven distress have remained isolated to the most highly-indebted corners of the private markets, but this distress spells opportunity for well-capitalized REITs. As with single-family rentals, there exist dozens of large-scale private equity institutional owners of multifamily properties with portfolios of 10k or more units and hundreds more "family office" investors with portfolios of 1-20k units. While we saw few private-to-REIT IPOs or acquisitions over the past decade during the period of ultra-low interest rates, the new higher-rate conditions are riper for public REITs to finally regain market share from their private peers.

{kind=link}

Hoya Capital

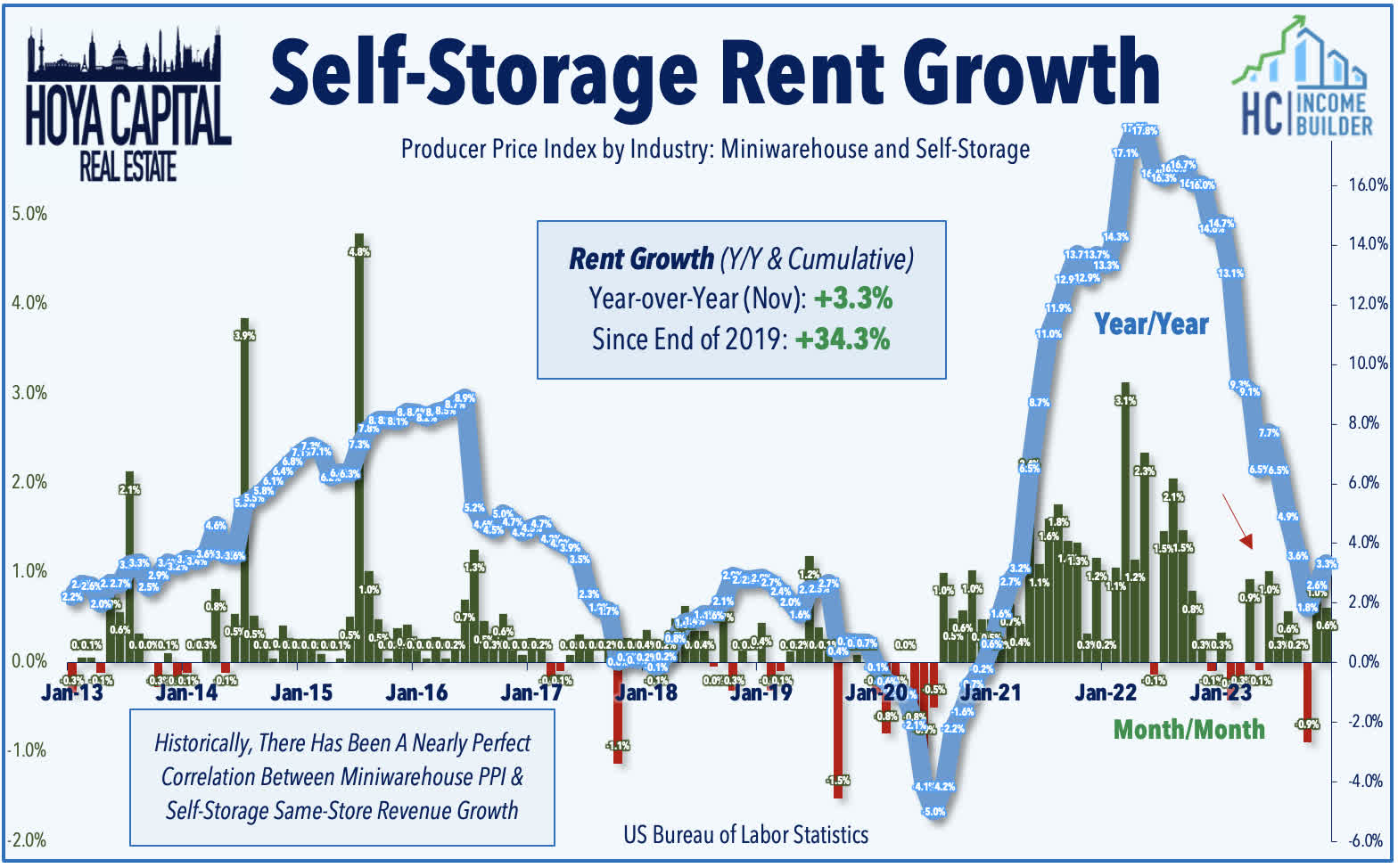

Self-Storage : Last but not least, a trio of business updates from the three largest self-storage REITs showed that fundamentals remained soft in the final months of 2024, but there were some early indications that an upward inflection in housing market activity is starting to revive some demand. An updated investor deck from Public Storage ( PSA ) - the largest storage REIT - showed that same-store occupancy rates declined to 91.6% at the end of the quarter, which was the lowest since Q4 of 2018. However, PSA noted "improving trends throughout the quarter" and noted that its average rent per square foot was still higher by 1% year-over-year as steady mid-single-digit rent growth on renewals has offset a sharp 15-20% decline on new leases. Reports from CubeSmart ( CUBE ) and Extra Space ( EXR ) showed similar trends, with both REITs reporting their lowest occupancy levels since at least 2019, but also showed some solid demand trends. The Producer Price report this week provided further encouragement, indicating that storage rent growth rebounded for a second-straight month in December.

{kind=link}

Hoya Capital

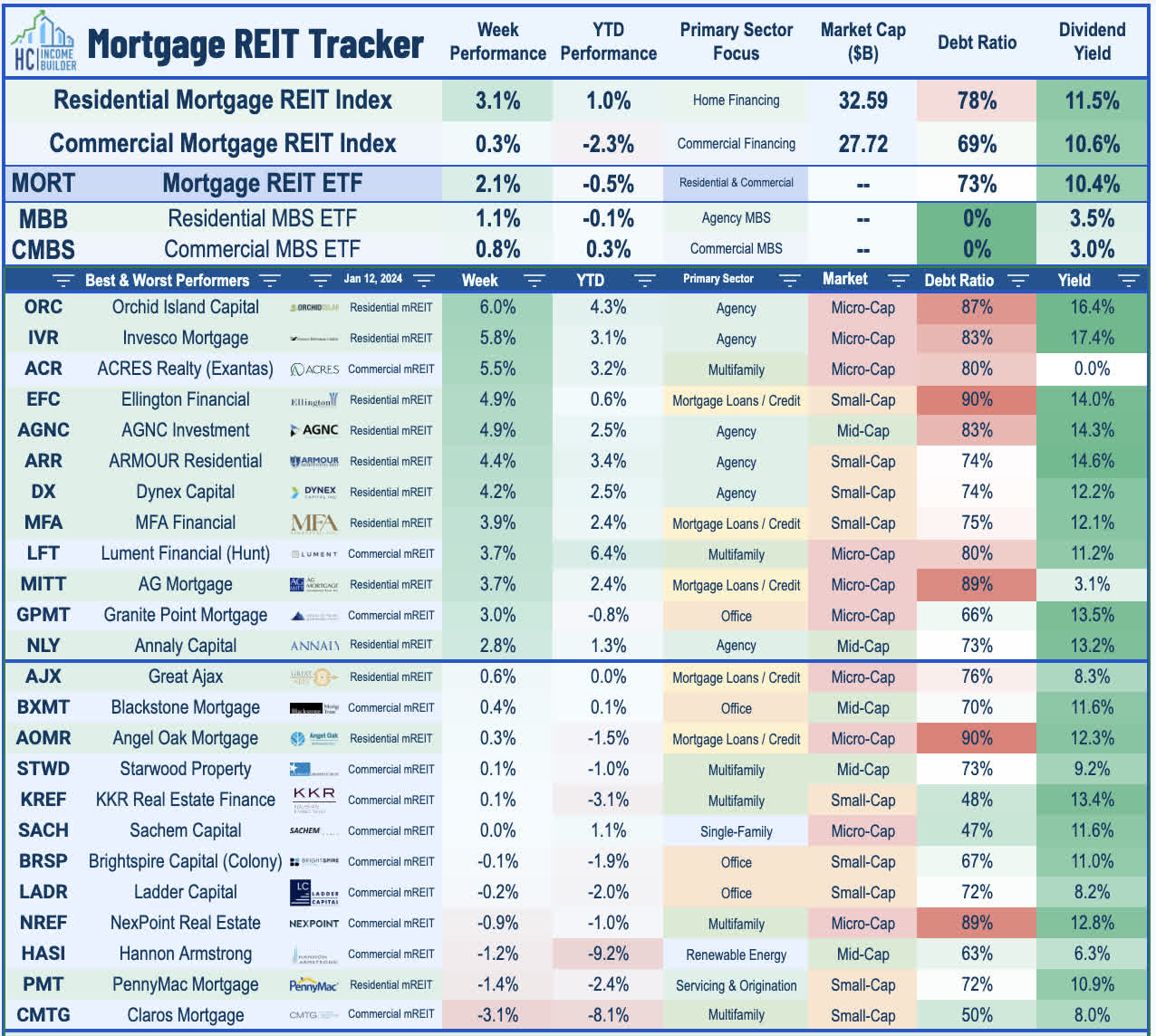

Mortgage REIT Week In Review

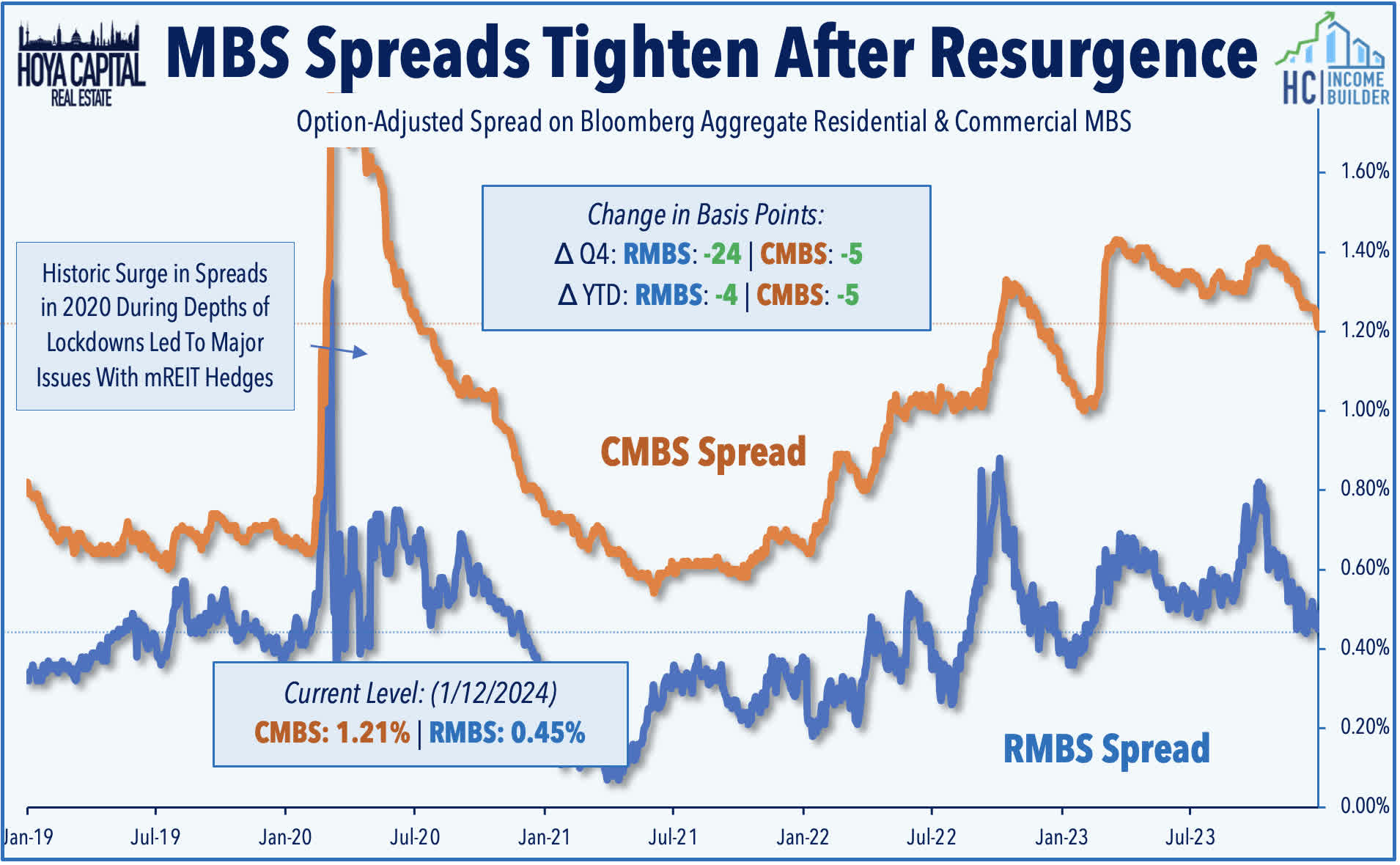

Following a two-week skid, Mortgage REITs rebounded this week as benchmark interest rates dipped while MBS spreads tightened. Led by strength from agency-focused mREITs, the iShares Mortgage REIT ETF ( REM ) rebounded 2.1% this week. Small-cap mREIT Orchid Island Capital ( ORC ) rallied 6% this week after it provided preliminary Q4 earnings metrics on Wednesday, noting its estimated book value per share climbed 2% during the quarter to $9.10. ORC also reported an estimated GAAP EPS of $0.52 for the quarter, which covered its $0.36/share dividend. As discussed in our Weekly Outlook , mortgage REITs are likely to report their best quarter for underlying Book Values since the start of the pandemic. The Residential MBS ETF ( MBB ) - which tracks the un-levered performance of RMBS - posted total returns of 7.3% in Q4 - one of its strongest quarters on record. The Commercial MBS ETF ( CMBS ) - which tracks the un-levered performance of RMBS - posted gains of 5.0% in Q4, also one of its strongest quarterly gains on record.

{kind=link}

Hoya Capital

Mortgage REITs were also active in the REIT capital raising wave. MFA Financial ( MFA ) rallied 4% after raising $100M in five-year senior notes at an 8.875% interest rate, which will be listed on the NYSE under ticker MFAN. The Notes will mature on February 15, 2029, and may be redeemed, at the company’s option, on or after February 15, 2026. Meanwhile, each of the six REITs that declared dividends this week held their payouts steady with current levels: Ellington Financial ( EFC ) maintained its monthly dividend at $0.15/share (14.2% yield). Ellington Residential ( EARN ) held its monthly dividend at $0.08/share (15.7% yield), AGNC Investment ( AGNC ) held its monthly dividend at $0.12/share (14.4% yield), Dynex Capital ( DX ) held its monthly dividend at $0.13/share (12.3% yield), Seven Hills ( SEVN ) held its quarterly dividend at $0.35/share (10.3% yield), and the aforementioned Orchid Island maintained its monthly dividend at $0.12/share (16.5% yield).

{kind=link}

Hoya Capital

2024 Performance Recap & 2023 Review

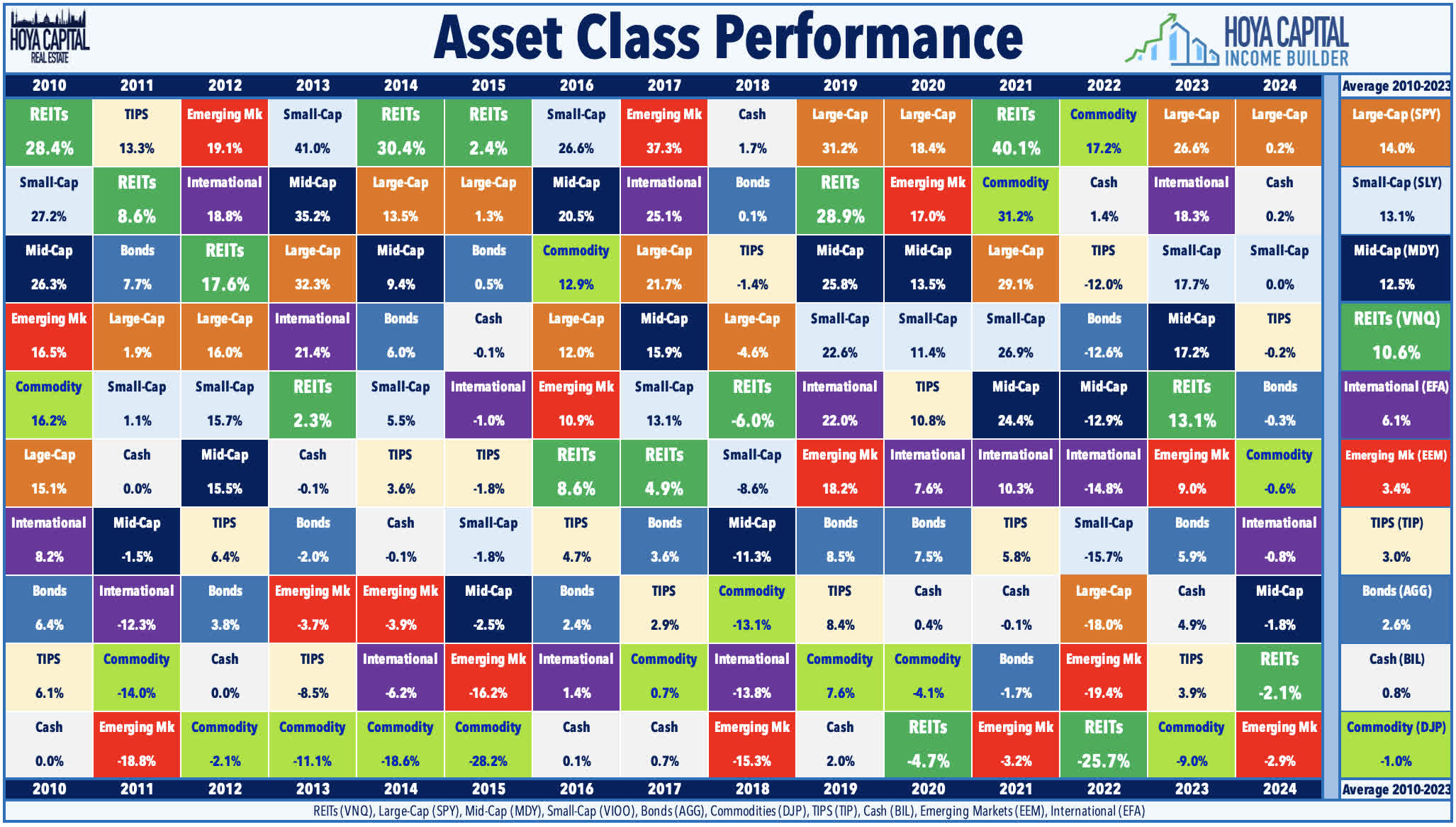

Through two weeks of 2024, the Equity REIT Index is lower by -1.4%, while the Mortgage REIT Index is lower by -0.5%. This compares with the 0.2% gain on the S&P 500 , the -1.9% decline for the S&P Mid-Cap 400 , and the -3.8% decline for the S&P Small-Cap 600 . Within the REIT sector, 8 of 18 property sectors are higher for the year, led by Regional Malls, Net Lease, Data Center, and Healthcare REITs, while Farmland and Timber REITs have lagged on the downside. At 3.95%, the 10-Year Treasury Yield is higher by 7 basis points on the year, but the 2-Year Treasury Yield has dipped 28 basis points to 4.15%. Following a late-year rally in the final months of 2023, the Bloomberg US Bond Index is lower by 0.3% this year. WTI Crude Oil is higher by 2.2% this year, while Natural Gas has rallied 35%.

{kind=link}

Hoya Capital

{kind=link}

Hoya Capital

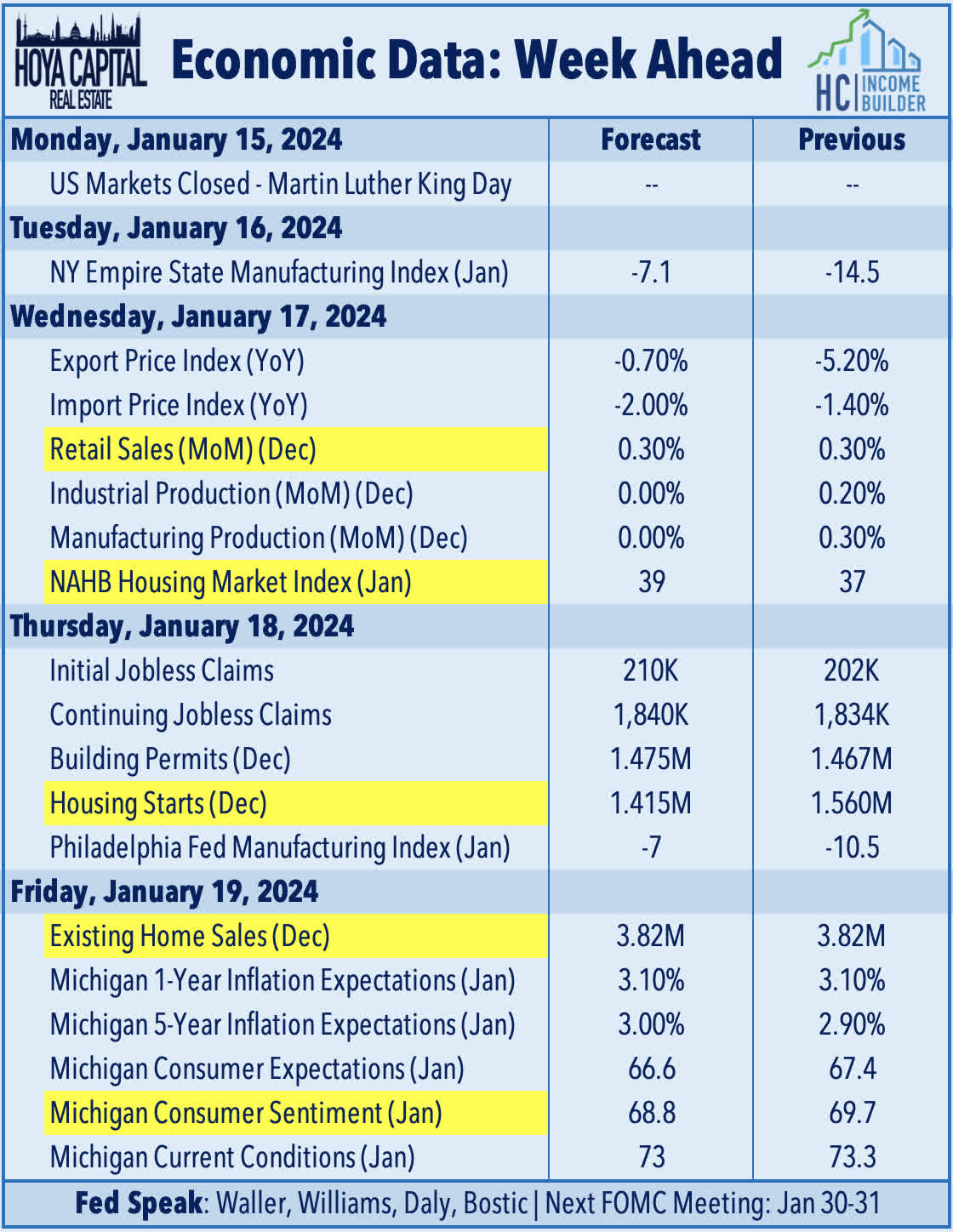

Economic Calendar In The Week Ahead

The state of the U.S. housing market will be in focus in the week ahead - the segment that bore the brunt of the Fed's rate hiking cycle. U.S. equity and bond markets will be closed on Monday for Martin Luther King Day. On Wednesday, we'll see NAHB Homebuilder Sentiment data for January, which is expected to show a second-straight monthly rise in builder optimism following four straight months of declines. We'll also see Retail Sales data on Tuesday, which will provide final numbers on the critical holiday retail spending season. On Thursday, we'll see Housing Starts and Building Permits data for December, which is expected to show a continued moderation in construction activity amid a still-challenging financing environment for both single-family and multi-family development. On Friday, we'll see Existing Home Sales data, which is expected to show sales velocity in December at a 3.82M annualized rate - hovering around the slowest-levels since 1995. This slate of data could very well represent the "bottom" of the rate-driven downturn, as the housing industry appears poised to finally rebound in 2024 following two years of stagnation. We'll also get our first look at Michigan Consumer Sentiment data for January, which includes a closely watched inflation expectations survey. Last month, sentiment rebounded sharply as inflation expectations cooled on the heels of lower gasoline prices.

{kind=link}

Hoya Capital

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

Hoya Capital

For further details see:

Disinflation Goes Global