REIT - Disinflation Is Back

2023-11-19 09:00:00 ET

Summary

- U.S. equity markets extended their rebound to a third-straight week as benchmark interest rates dipped on economic data and corporate earnings reports showing a more distinct cooldown in economic activity.

- Gaining for a third-straight week and extending its rebound to nearly 10% since dipping into "correction territory" at the end of October, the S&P 500 gained another 2.4% this week.

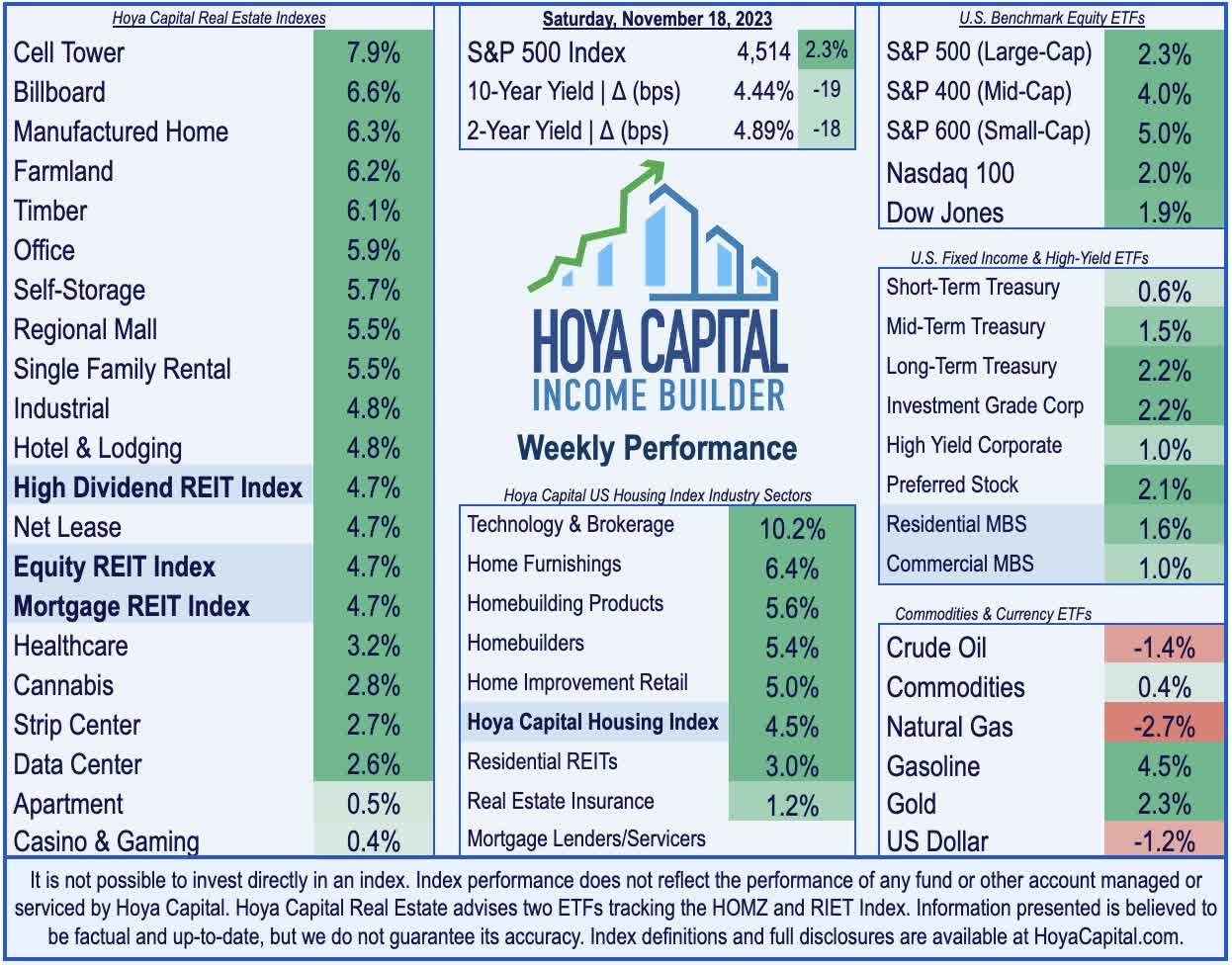

- Lifted by the retreat in benchmark interest rates, real estate equities have roared back to life over the past three weeks. Equity REITs and Mortgage REITs each gained another 4.7%.

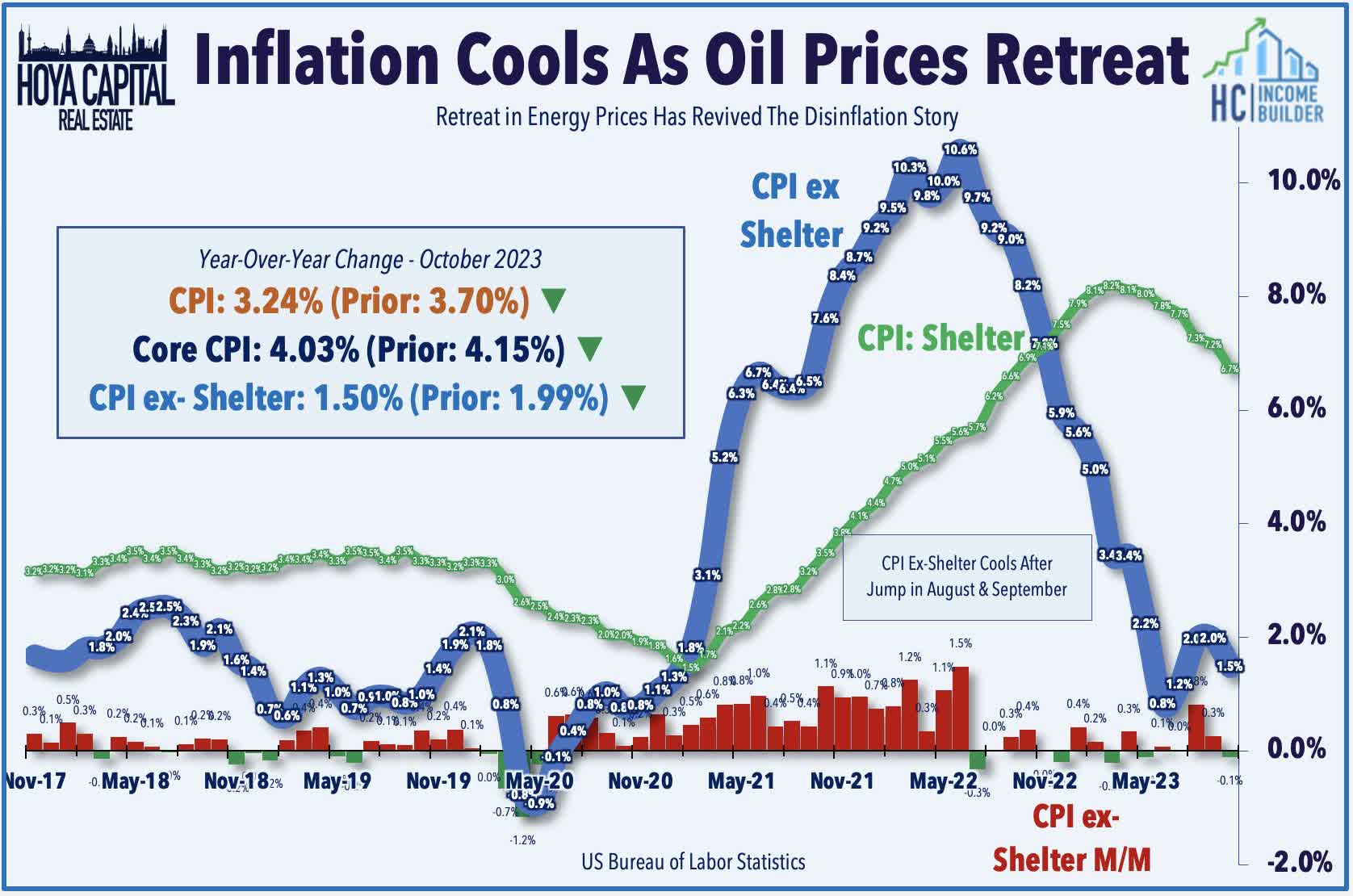

- The critical CPI and PPI reports showed an encouraging cooldown of inflationary pressures in October following a three-month reacceleration driven primarily by resurgent energy prices.

- The CPI-ex-Shelter Index - the metric we watch most closely - dipped back into deflation territory in October, pulling its year-over-year increase back down to 1.5% - below the Fed's stated 2% inflation objective.

Real Estate Weekly Outlook

U.S. equity markets extended their rebound to a third-straight week as benchmark interest rates dipped to the lowest levels since September on economic data and corporate earnings reports showing a more distinct cooldown in economic activity, bolstering the prospects that the Federal Reserve is done with its rate hike campaign. The critical CPI and PPI reports showed an encouraging cooldown of inflationary pressures in October following a three-month reacceleration driven primarily by resurgent energy prices. The CPI-ex-Shelter Index - the metric we watch most closely - dipped back into deflation territory in October, pulling its year-over-year increase back down to 1.5% - below the Fed's stated 2% inflation objective.

{kind=link}

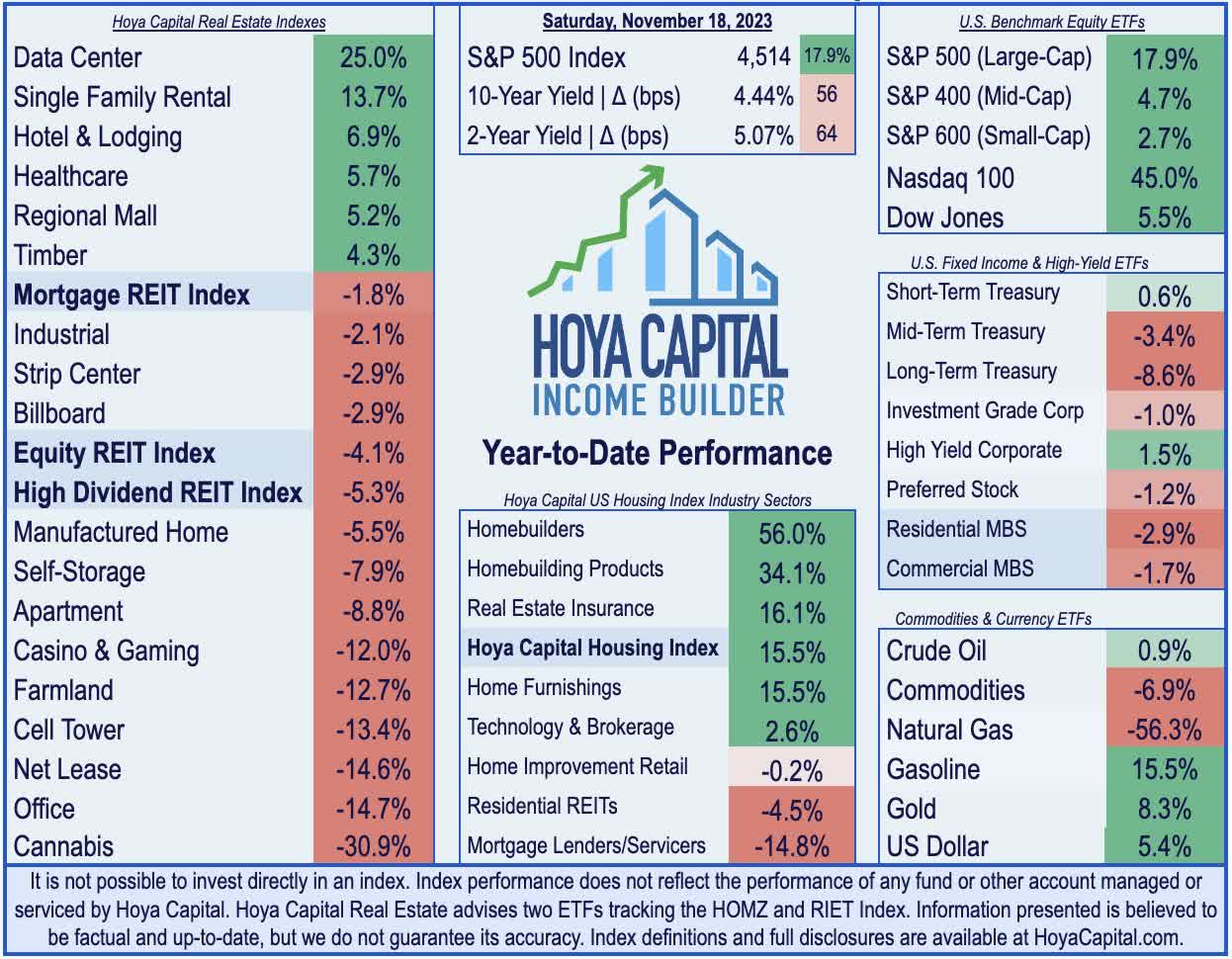

Gaining for a third-straight week and extending its rebound to nearly 10% since dipping into "correction territory" at the end of October, the S&P 500 gained another 2.4% for the week. Gains were notably broad-based this week, with the Mid-Cap 400 rallying 4.0%, while the Small-Cap 600 soared 5.0%, closing some of their historically wide underperformance gap this year relative to their large-cap peers. Lifted by the retreat in benchmark interest rates, real estate equities have roared back to life over the past three weeks. Now higher by nearly 12% since bottoming in late October, the Equity REIT Index gained another 4.7% this week, with all 18 property sectors in positive territory, while the Mortgage REIT Index also rallied 4.7%. Homebuilders surged 5.4% as mortgage rates retreated sharply to around 7.5% - the lowest level since August - after soaring to three-decade highs above 8% last month.

{kind=link}

Fueled by encouraging inflation data indicating that a 'soft landing' - a cooling of inflation without a recession - appears to be back on track, bonds rallied across the yield and maturity curve this week on expectations that the Federal Reserve is done with its historically aggressive rate-hiking cycle, with markets now pricing in the first rate cut by May 2024, and for the Fed Funds rate to end 2024 at a 4.5% upper-bound, down from the current 5.5% level. The 10-Year Treasury Yield closed the week at 4.44% - down 19 basis points to its lowest-level since mid-September. Cautious commentary from Walmart on the state of the consumer also fueled the bond bind, as the retail giant noted a slowdown in spending in October and commented that it's “managing through a period of deflation" in the months ahead. Speaking of disinflation, WTI Crude Oil declined for a fifth straight week to close around $76/barrel, entering "bear market" territory with declines of over 20% from its recent highs in late September. The US Dollar Index , meanwhile, posted its worst week in four months. All eleven GICS equity sectors finished higher on the week, with Real Estate ( XLRE ) and Materials ( XLB ) stocks leading on the upside, while Consumer Staples ( XLP ) lagged.

{kind=link}

Real Estate Economic Data

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

{kind=link}

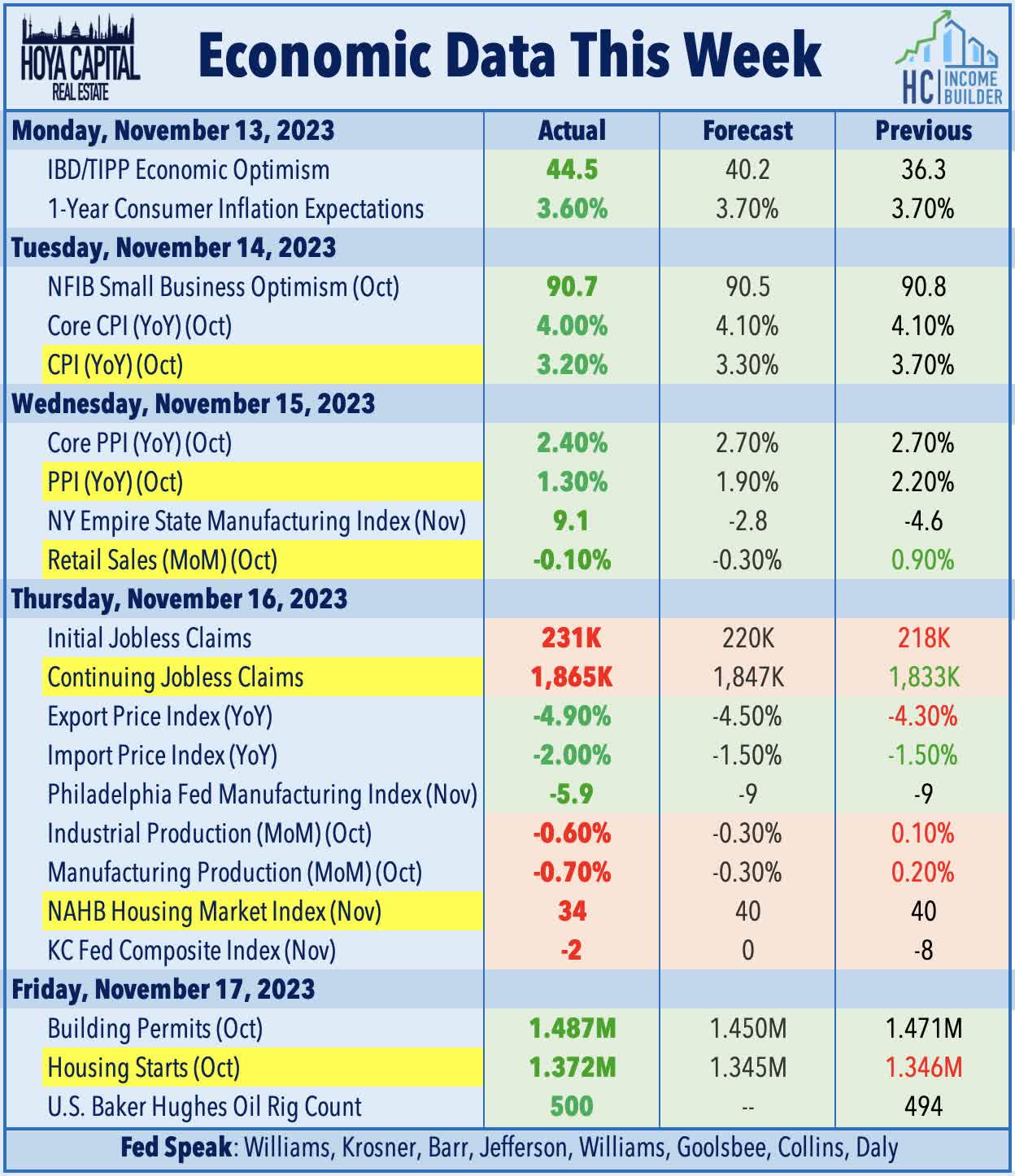

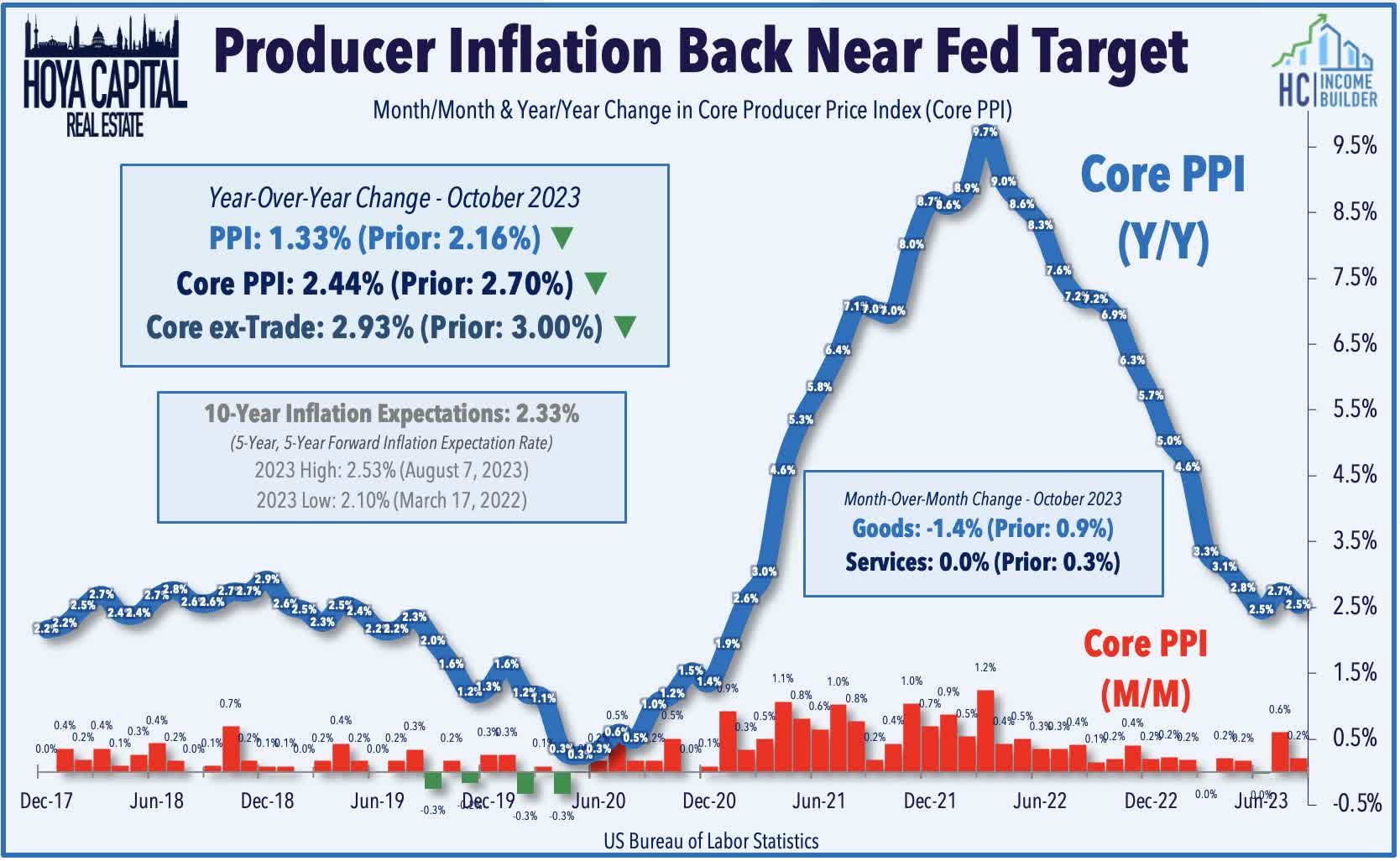

All eyes were on the Consumer Price Index report this week, which showed an encouraging cooldown of inflationary pressures in October following a three-month reacceleration from June through September driven primarily by resurgent energy prices - the key "swing" inflation input. Headline CPI was flat month-over-month and increased by 3.2% from a year ago, which was below consensus estimates of 0.1% and 3.3%, respectively. Core CPI - which excludes food and energy - was also cooler than expected, rising 0.2% on the month and 4.0% on the year, below expectations of 0.3% and 4.1%, respectively. The CPI-ex-Shelter Index - the metric we watch most closely given the substantial lags in the BLS' shelter inflation metrics - declined 0.1% during the month to pull its year-over-year increase back down to 1.5% - now below the Fed's stated 2% inflation objective. The BLS continues to show a 6.7% year-over-year increase in shelter inflation - down from the 8.2% peak in March - but still substantially overstating the real-time shelter inflation, which we estimate is actually slightly negative year-over-year.

{kind=link}

Following the cooler-than-expected CPI report, Producer Price Index data the following day showed an even sharper moderation of price pressures. The Headline PPI dipped 0.5% in October - well below the 0.1% increase expected - which, combined with downward revisions to prior months, dragged the annual increase to just 1.3%. Goods prices fell sharply in October, driven by a retreat in energy prices. Core PPI - which excludes food and energy - was flat in October, dragging the annual increase to 2.4%, which was the lowest since January 2021. Meanwhile, jobless claims data this week showed that continuing claims rose for an eight-straight week to the highest level in nearly two years, while initial claims rose to the highest level since August - softness that appears to confirm the notably weak nonfarm payroll report earlier this month showing a slowdown in hiring and in wage gains in recent months.

{kind=link}

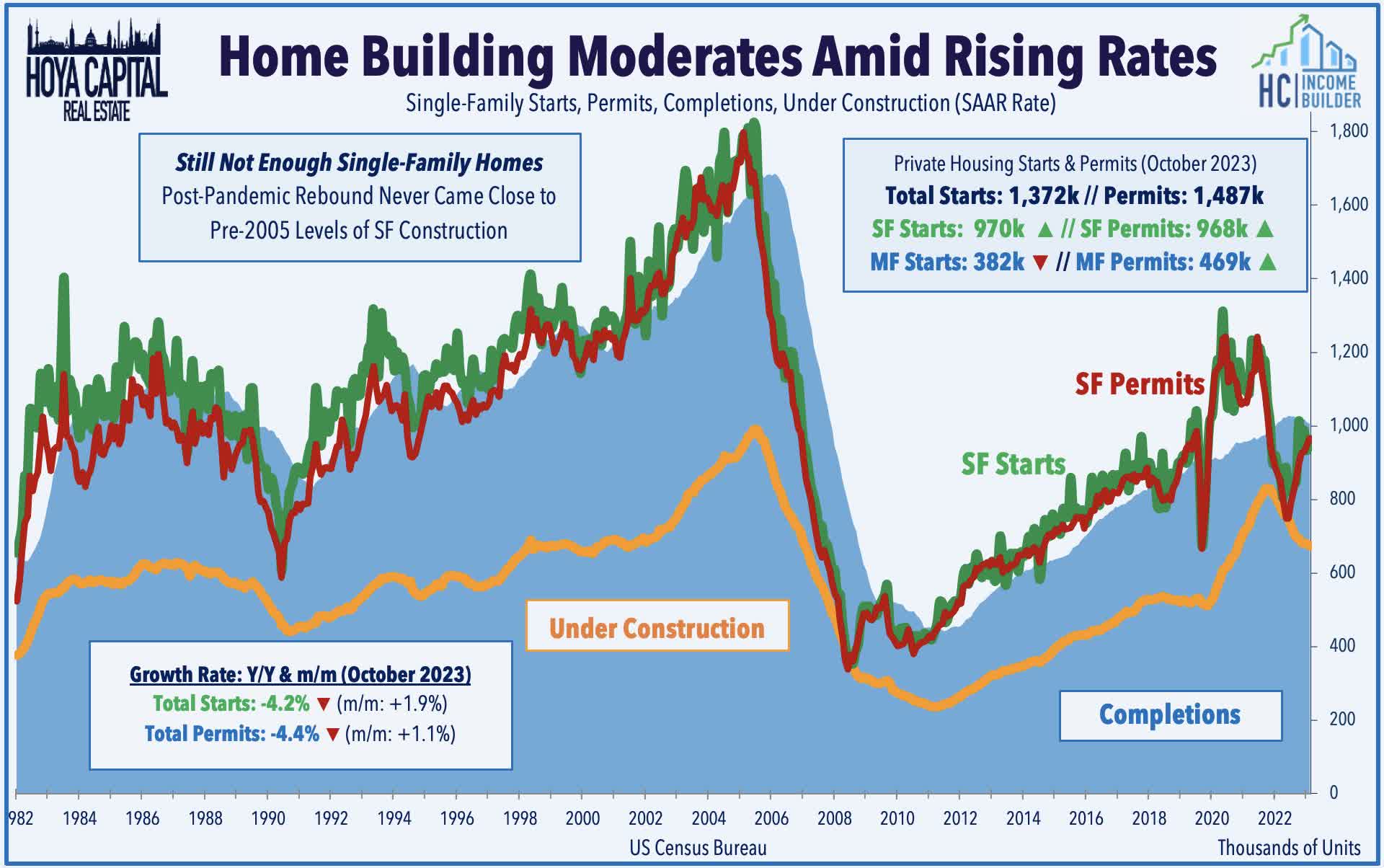

Housing data this week was generally a bit stronger-than-expected, however, consistent with the countercyclical trends of U.S. housing market through the post-GFC period. Housing Starts and Building Permits data this week showed a slight pick-up in home construction activity in October, consistent with recent earnings reports from the largest single-family builders showing modest but consistent demand for new homes despite the decade-high level on conventional mortgage rates. Housing Starts ticked up slightly from the prior month to a 1.372M seasonally adjusted rate - above the 1.350 consensus - which was 4.2% below the prior year. Building permits ticked up to a 1.487M annualized rate - above the 1.45M expected - but also down 4.4% from a year earlier. The relatively solid report follows softer data on Thursday from the NAHB, which showed that its Homebuilder Sentiment Index fell to 34 in November from 40 in October, with all three sub-components posting declines of at least 5 points. The report showed that 36% of builders said they cut home prices in October - the highest level in a year.

{kind=link}

Equity REIT Week In Review

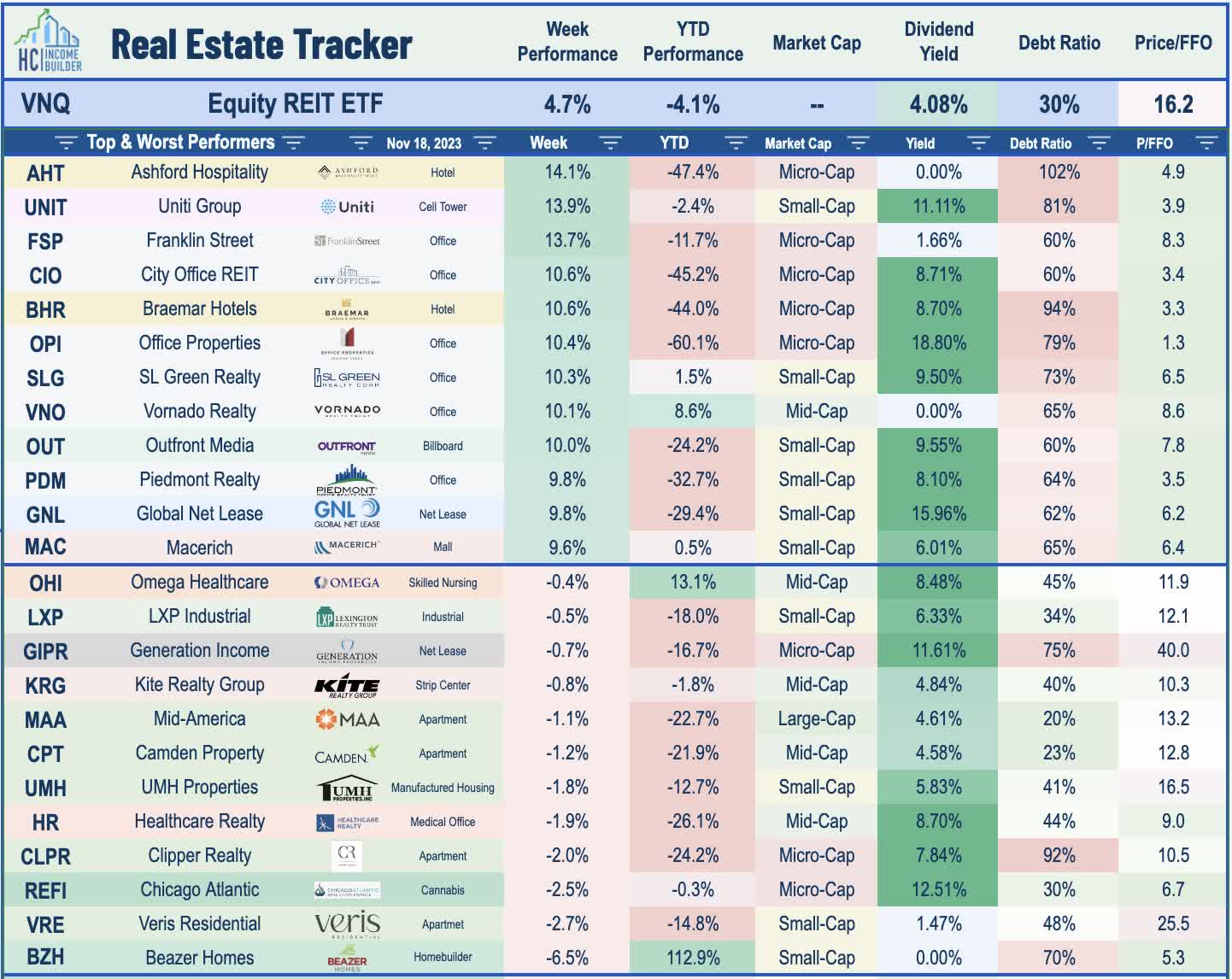

Best & Worst Performance This Week Across the REIT Sector

{kind=link}

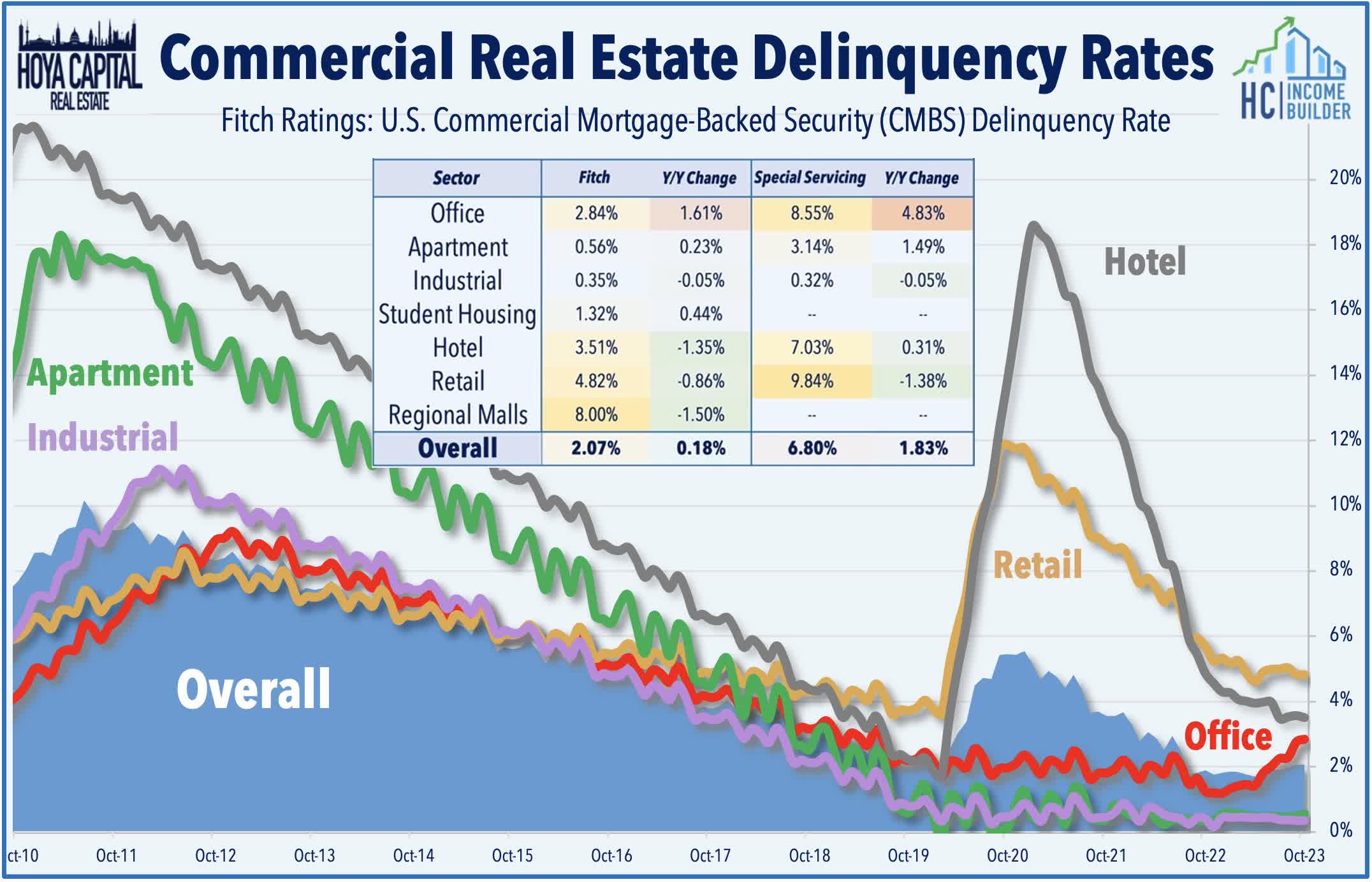

Real estate earnings season wrapped up this week with results from a final handful of small-cap REITs. After publishing Winners of REIT Earnings Season last week, this week we published Losers of REIT Earnings Season , concluding our two-part Earnings Recap. We noted that unlike the second quarter, which saw a handful of truly poor reports and unexpectedly steep guidance and dividend cuts, there were few major 'bombshells' this earnings season, but laggards this earnings season included Residential, Office, Mortgage, and Self-Storage REITs. Expense growth remained stubbornly persistent for residential REITs - which were responsible for the majority of the downward guidance revisions this quarter - with insurance and property taxes surging by double-digits across most markets and segments - while supply growth is an issue for multifamily, industrial, and self-storage. Surging interest expense was again the culprit behind the balance of the downward revisions. For lenders, defaults have accelerated as CRE property values have declined nearly 20% from recent peaks, but distress remains largely contained to the office sector and from "mom and pop" multifamily investors, which have been slammed by higher interest expense on variable rate loans.

{kind=link}

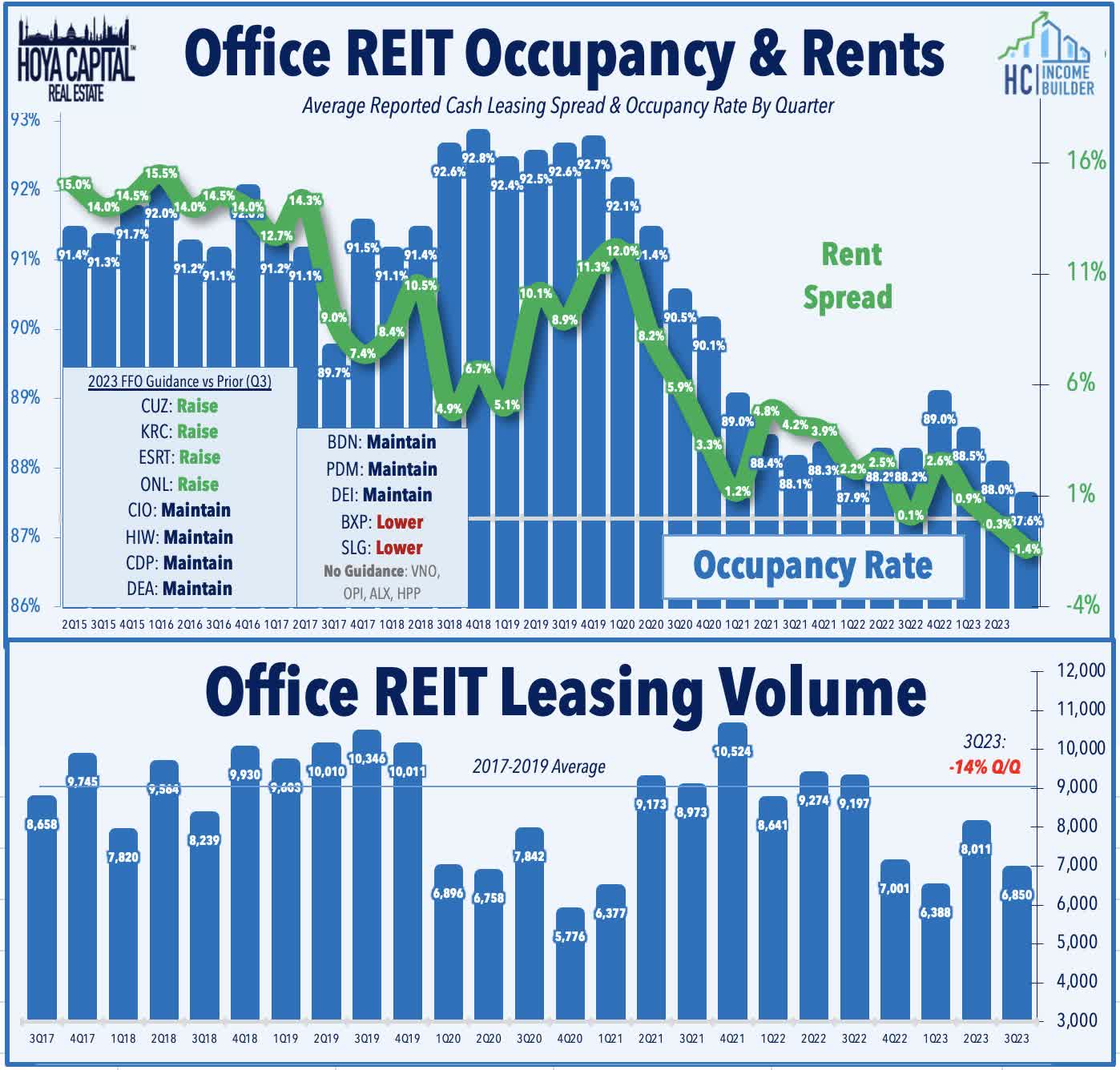

Office : On that note, office REITs were among the strongest performers this week in hopes that there's an end-in-sight to the stiff interest rate headwinds. Boston Properties ( BXP ) rallied 5% after it announced that it reached a deal to sell a 45% interest in two life sciences development properties in Cambridge, Massachusetts, to Norges Bank for $746.4M. The deal implies a gross valuation of $1.66B, or $2,050 per square foot, for the combined properties. BXP will retain a 55% stake in the joint ventures and will provide development, property management, and leasing services for the ventures. 290 Binney Street is pre-leased to AstraZeneca, with initial occupancy expected in April 2026 while 300 Binney Street is 100% pre-leased to the Broad Institute, with projected occupancy expected in January 2025. As noted in our Earnings Recap , BXP reported decent third-quarter results, highlighted by total leasing volume of 1.06M square feet - its highest in over a year - which lifted its occupancy rate higher by 50 basis points to 88.8%.

{kind=link}

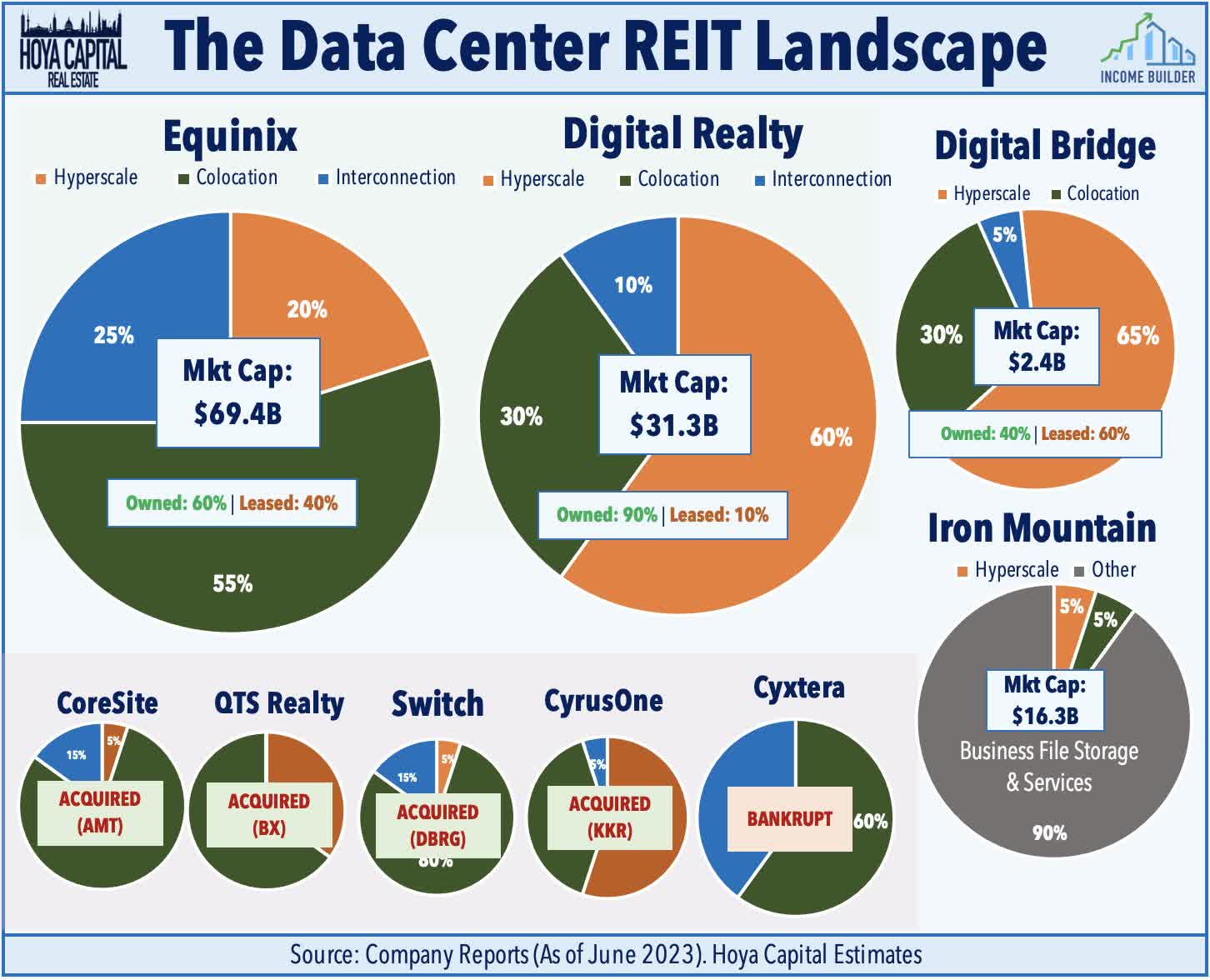

Net Lease & Data Center : Digital Realty ( DLR ) - the second-largest data center REIT - and Realty Income ( O ) - the largest net lease REIT announced a joint venture to build and own two full-leased data centers in Northern Virginia. Realty Income - which rallied nearly 6% on the week - will invest $200M for an 80% equity stake in the venture, while Digital Realty - which gained 4.5% on the week - will hold a 20% interest, with each partner funding its pro rata share of the remaining $150M estimated development cost for the first phase of the project, which is scheduled for completion in mid-2024. The 16MW data center is 100% pre-leased to an S&P 100 investment-grade client prior to construction and is expected to generate a 6.9% initial cash lease yield upon lease commencement in mid-2024. The facilities are subject to a 10-year initial lease term with extension options and 2.0% annual rent escalators. DLR noted that the move "bolsters and diversifies DLR's capital sources" while O noted that the move is consistent with its core strategy of "partnering with companies that are leaders in their respective industries." One of several notable recent non-retail investments for O, the move follows a $950M joint venture with Blackstone's BREIT for a 22% stake in The Bellagio announced in August.

{kind=link}

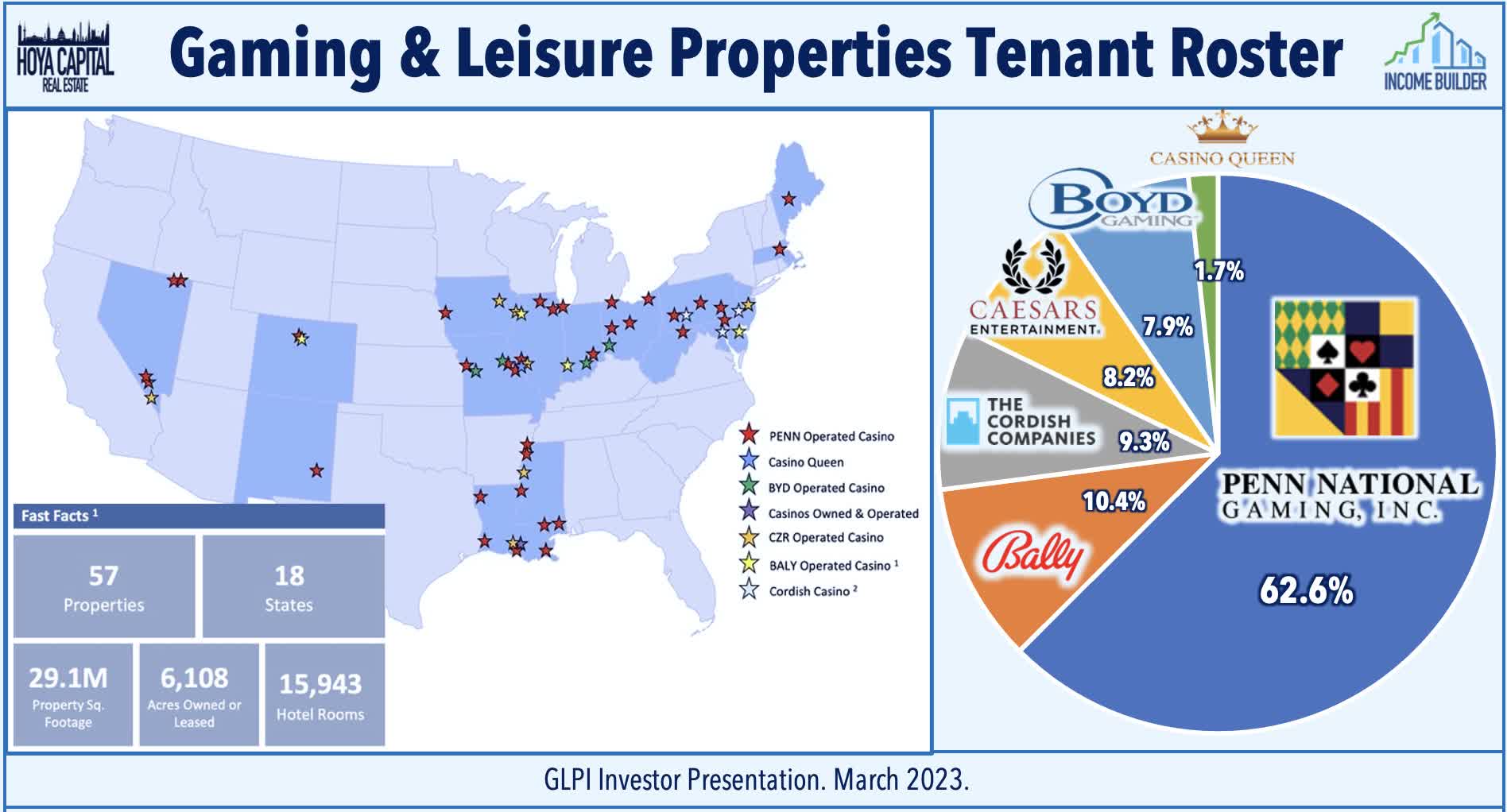

Casino : Speaking of casino REITs, Gaming and Leisure Properties ( GLPI ) was little-changed this week following the announcement by Major League Baseball that the league’s owners have approved the move of the Athletics (“A’s”) franchise to Las Vegas, with GLPI, "We are excited to develop and construct an entertainment and casino resort integrated with the new A’s stadium on GLPI's property to reinvent the site on the south end of the iconic Las Vegas Strip." The previously-announced stadium is expected to complement a casino resort redevelopment envisioned at GLPI’s 35-acre property owned by GLPI and leased to Bally’s. The letter of intent provides for the Athletics to be granted fee ownership of 9 acres of GLPI’s 35-acre site for construction of the stadium, which is expected to open in 2028.

{kind=link}

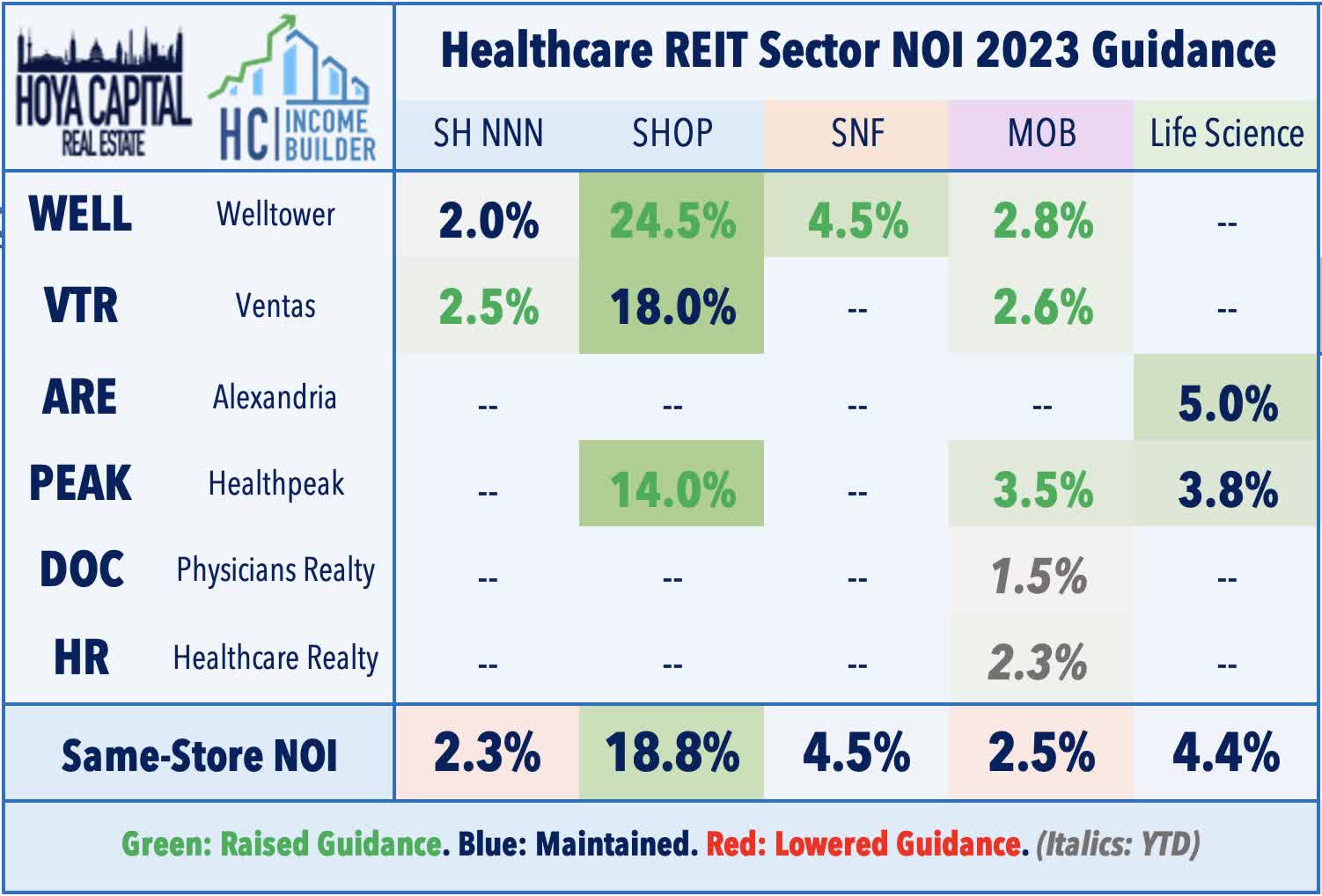

Healthcare : Senior housing REITs also delivered strong gains this week on the heels of very strong earnings results last week. Welltower ( WELL ) gained 2% in the week after announcing that it is acquiring 23 senior housing properties from Chartwell Retirement in an agreement to dissolve the joint venture. The incremental investment of $82.1M is priced at an estimated 30% discount to replacement cost, and retained assets are expected to stabilize at an "almost 10% yield and generate a low-double-digit unlevered IRR." Benefiting from COLA increases, pricing power remains robust across the senior housing sector, and, combined with moderating expense pressures, has driven a meaningful improvement in operating margins. Last week, Welltower raised its full-year outlook driven by a significant profitability recovery in its critical Senior Housing Operating Portfolio ("SHOP") segment. WELL now expects same-store NOI growth in this segment to increase by 24.5% this year, driven by rent growth of nearly 7% and by a gradual recovery in occupancy rates, which had been ravaged by the pandemic. Ventas ( VTR ) also reported strong third-quarter results last week and lifted its full-year outlook.

{kind=link}

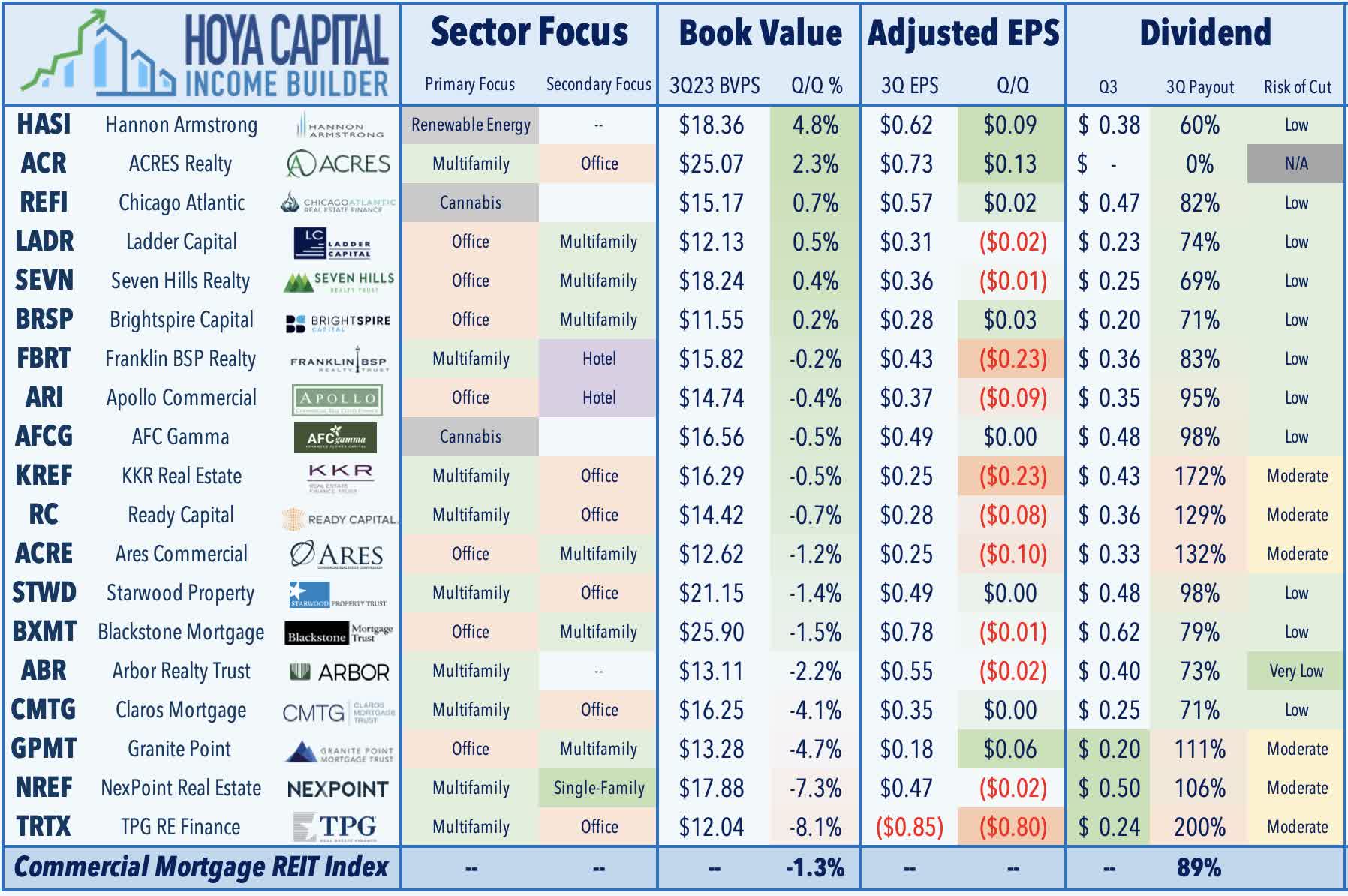

Mortgage REIT Week In Review

Extending its three-week gains to over 15%, mortgage REITs resumed their frenetic rebound last week from their October lows, with the iShares Mortgage Real Estate Capped ETF ( REM ) rallying another 4.7% this week. Arbor Realty ( ABR ) was the laggard this week, however, dipping 4% after the multifamily lender once again came into the cross-hairs of short-sellers. A short report from Viceroy Research alleges that ABR's "entire loan book is distressed and underlying collateral is vastly overstated" based on Viceroy's belief that multifamily cap rates should be re-stated at 7% given the current interest rate environment, up from ABR's latest appraised valuations of 4.7%. CBRE reported last month, however, that multifamily cap rates averaged 4.92% in the third quarter - up from lows in late 2021 of 3.40%. ABR had previously been the target of short reports from Ningi Research and Hedgeye earlier this year. After an initial sell-off in late March, Arbor had rallied more than 60% from April through July but has retraced much of this rebound after reporting downbeat second-quarter results, noting an uptick in delinquency.

{kind=link}

Earnings season wrapped up this week with results from the final four mortgage REITs. Beginning on the residential side, Ellington Residential ( EARN ) rallied 7% this week after reporting mixed results but outlining a strategy shift to invest outside of agency MBS into the Collateralized Loan Obligation ("CLO") space, which it notes "offer a good balance to Agency MBS," noting that CLO mezzanine debt tranches are floating rate, while our Agency MBS are typically fixed rate. EARN reported comparable EPS of $0.21 - up from $0.17 last quarter - but still shy of its $0.24/share dividend and noted that its Book Value Per Share ("BVPS") dipped 13.5% during the quarter - which was right around the average for agency-focused mREITs. Elsewhere, Arlington Asset Investment ( AAIC ) - which will be acquired by Ellington Financial ( EFC ) in a deal expected to close in early 2024 - gained 2% this week after reporting in-line results, noting that its BVPS declined 3.5% - the sixth-best among residential mREITs during the third quarter. Meanwhile, Orchid Island ( ORC ) and Dynex Capital ( DX ) each rallied more than 5% on the week after maintaining their monthly dividend at current levels.

{kind=link}

Elsewhere, Rithm Capital ( RITM ) gained 3% this week after it announced the completion of its $719.8M acquisition of asset manager Sculptor Capital for $12.70/share, concluding a months-long saga in which RITM fended off competitive bids from a rival shareholder group. One of the largest alternative asset managers in the world, Sculptor Capital (formerly Och-Ziff Capital) manages $32.8 billion in assets with a focus on real estate, credit, and multi-strategy hedging. RITM noted back in July that the deal is expected to be neutral to its 2024 earnings and accretive in 2025 and will be funded with cash on hand. On the commercial side, small-cap multifamily lender Lument Finance ( LFT ) was also an outperformer this week after it reported that its BVPS increased 1% during the quarter while recording distributable EPS of $0.11 - covering its $0.07/share dividend. Sachem Capital ( SACH ) rallied 3.5% after reporting EPS of $0.12 - covering its dividend of $0.11/share, which was reduced earlier this month from $0.13/share.

{kind=link}

2023 Performance Recap

With just six weeks left in 2023, the Equity REIT Index is now lower by 4.1% on a price return basis for the year (-1.1% on a total return basis), while the Mortgage REIT Index is lower by 1.8% (+7.5% on a total return basis). This compares with the 17.9% gain on the S&P 500 and the 4.7% gain for the S&P Mid-Cap 400 . Within the real estate sector, six property sectors are in positive territory on the year, led by Data Center, Single-Family Rental, and Hotel REITs, while Office and Net Lease REITs have lagged on the downside. At 4.44%, the 10-Year Treasury Yield has climbed 56 basis points since the start of the year - up sharply from its 2023 intra-day lows of 3.26% in April - but down from peaks above 5.0% in mid-October. Following the worst year for bonds in decades, the Bloomberg US Bond Index is slightly higher this year, producing total returns of 0.5% thus far. WTI Crude Oil - perhaps the most important inflation input - is higher by 0.8% this year, while Natural Gas -the primary fuel for electricity generation - is lower by over 50% this year.

{kind=link}

Economic Calendar In The Week Ahead

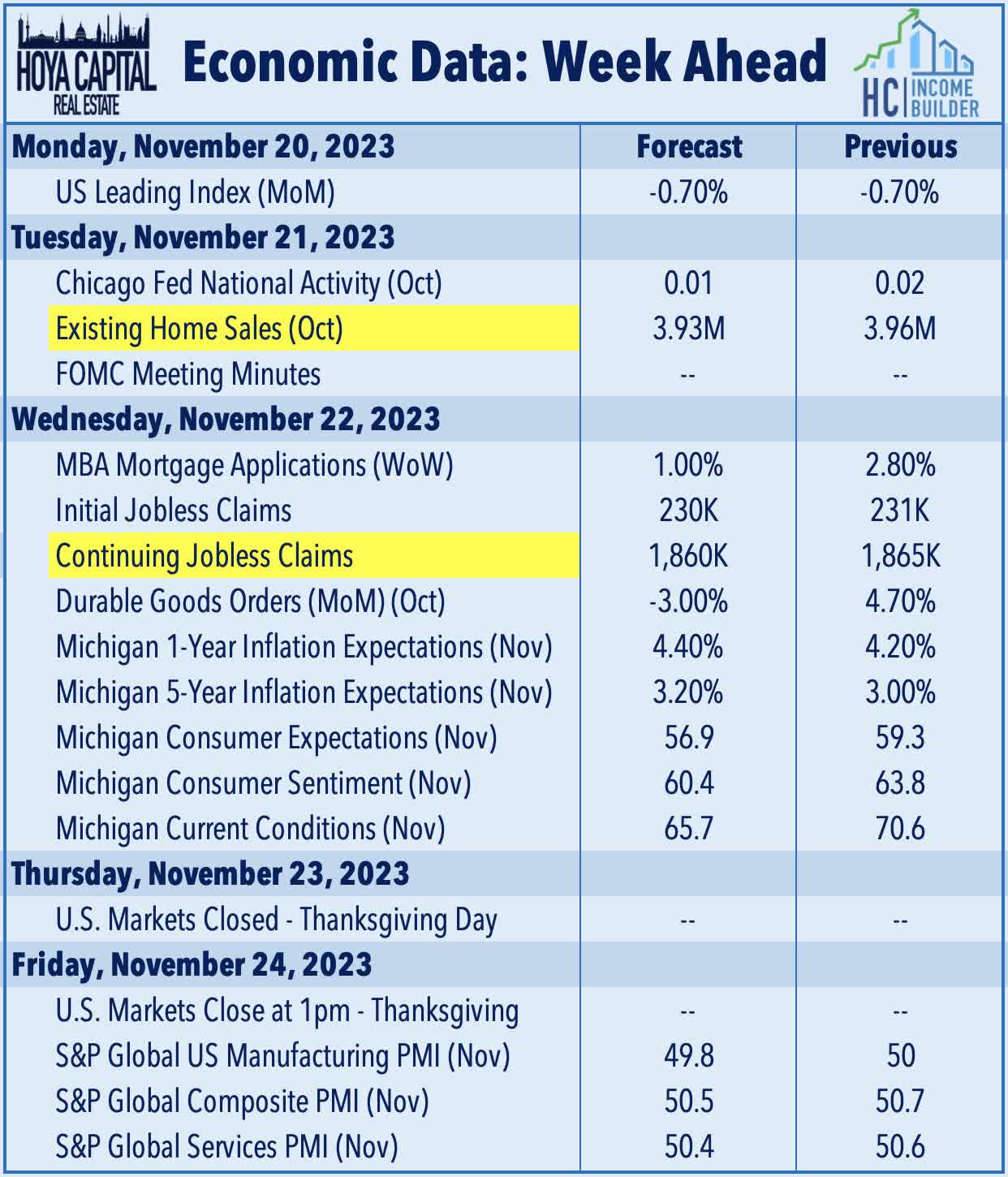

The economic calendar slows down in the holiday-shortened week ahead. U.S. markets will be closed on Thursday for the Thanksgiving holiday and will close at 1 pm ET on Friday. On Tuesday, we'll see Existing Home Sales data, which is expected to show a slowdown in sales velocity in October to a 3.93M annualized rate, which would be the second slowest month for home sales since 1995, eclipsed only by one month - August 2010 - at the depths of the GFC-induced slowdown. Despite the sales slowdown, housing inventory levels have remained near historically low levels this year due, in part, to the "lock-in" effect on existing mortgages and from the counterproductive slowdown in home building, which has kept a floor on home values and rental rates despite the stiff affordability headwinds. We'll also be watching Jobless Claims data on Wednesday to see if recent signs of labor market softness persist after Continuing Claims rose this past week to the highest in nearly two years. We'll also be watching the second look at November Michigan Consumer Sentiment data on Wednesday and PMI data from S&P Global on Friday.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

Disinflation Is Back