REIT - Disinflation Loses Energy

2023-08-13 09:00:00 ET

Summary

- U.S. equity markets slumped for a second-straight week while long-term benchmark interest rates pushed higher after inflation data showed some firming in price pressures amid a rebound in energy prices.

- Following declines of more than 2% last week, the S&P 500 declined 0.3% this week, while the tech-heavy Nasdaq 100 dipped 1.6% to extend its two-week skid to over 5%.

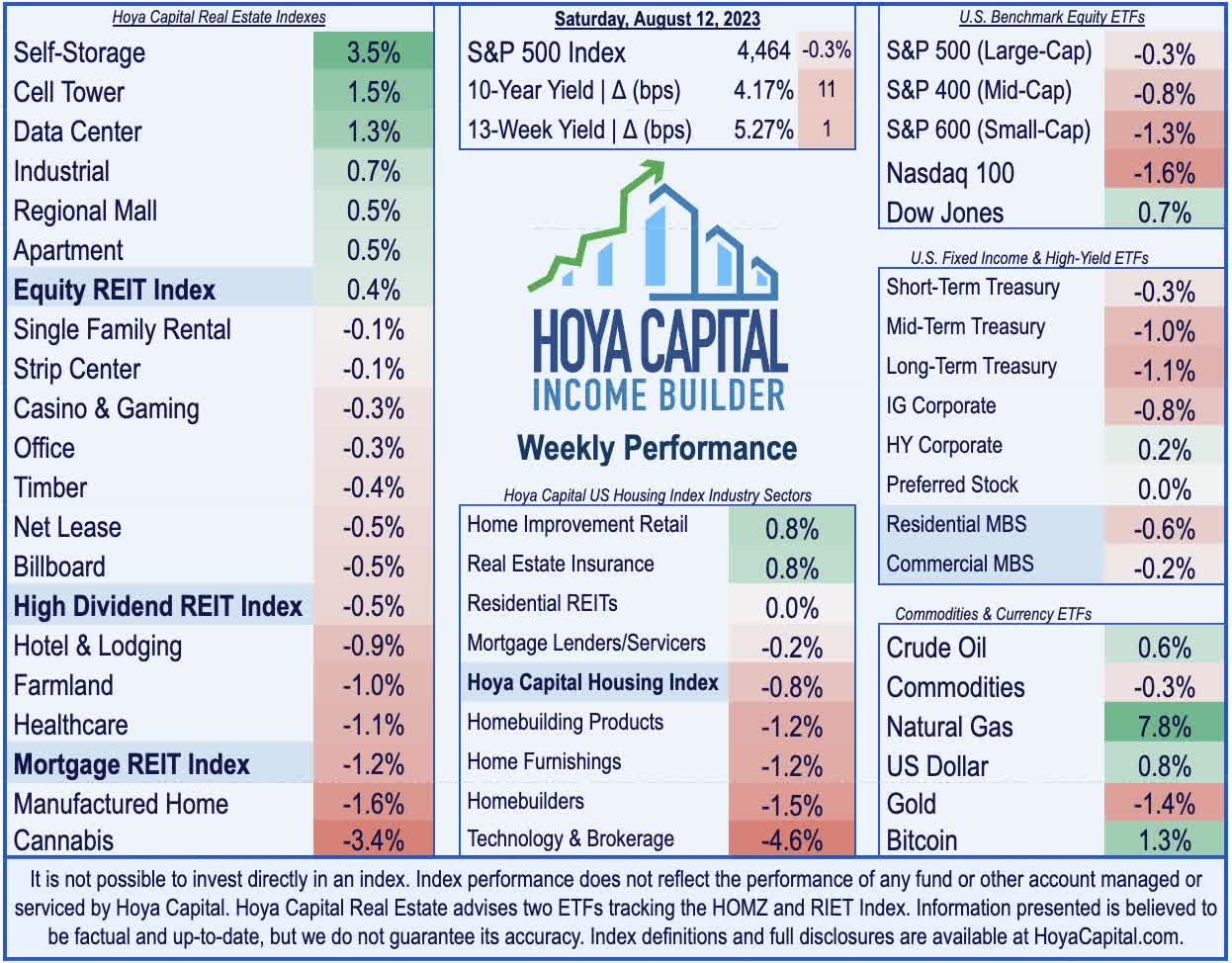

- Despite the upward pressure on benchmark interest rates, real estate equities were among the leaders this week as REIT earnings season wrapped up with a handful of encouraging reports.

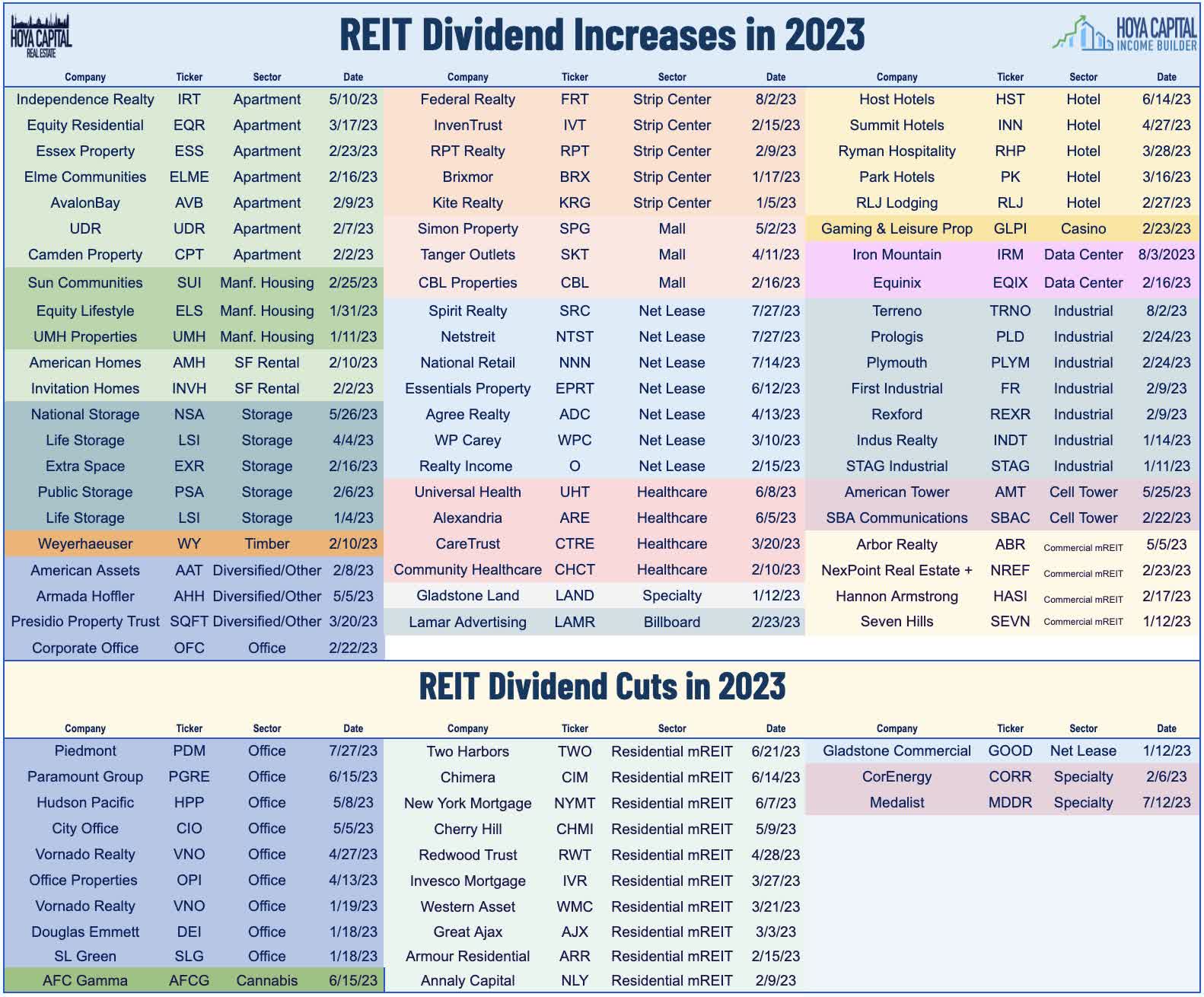

- Net lease REIT Spirit Realty was among the upside standouts this week after reporting solid results and hiking its dividend, becoming the 64th REIT to raise its dividend this year.

- On the downside this week, hospital owner Medical Properties Trust dipped more than 15% this week after trimming its full-year outlook and reporting ongoing operating struggles with two of its largest tenants.

Real Estate Weekly Outlook

{kind=link}

U.S. equity markets slumped for a second-straight week - while long-term benchmark interest rates pushed higher - after inflation data showed some firming in price pressures amid a rebound in energy prices - removing a key marginal driver of recent disinflation. Following declines of more than 2% last week, the S&P 500 declined 0.3% this week, while the tech-heavy Nasdaq 100 dipped 1.6% to extend its two-week skid to over 5%. Despite the upward pressure on benchmark interest rates, real estate equities were among the leaders this week as REIT earnings season wrapped up with a handful of encouraging reports but also several downside surprises. The Equity REIT Index advanced 0.4% on the week, with 6-of-18 property sectors in positive territory, but the Mortgage REIT Index slipped 1.2%.

{kind=link}

Real Estate Economic Data

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

{kind=link}

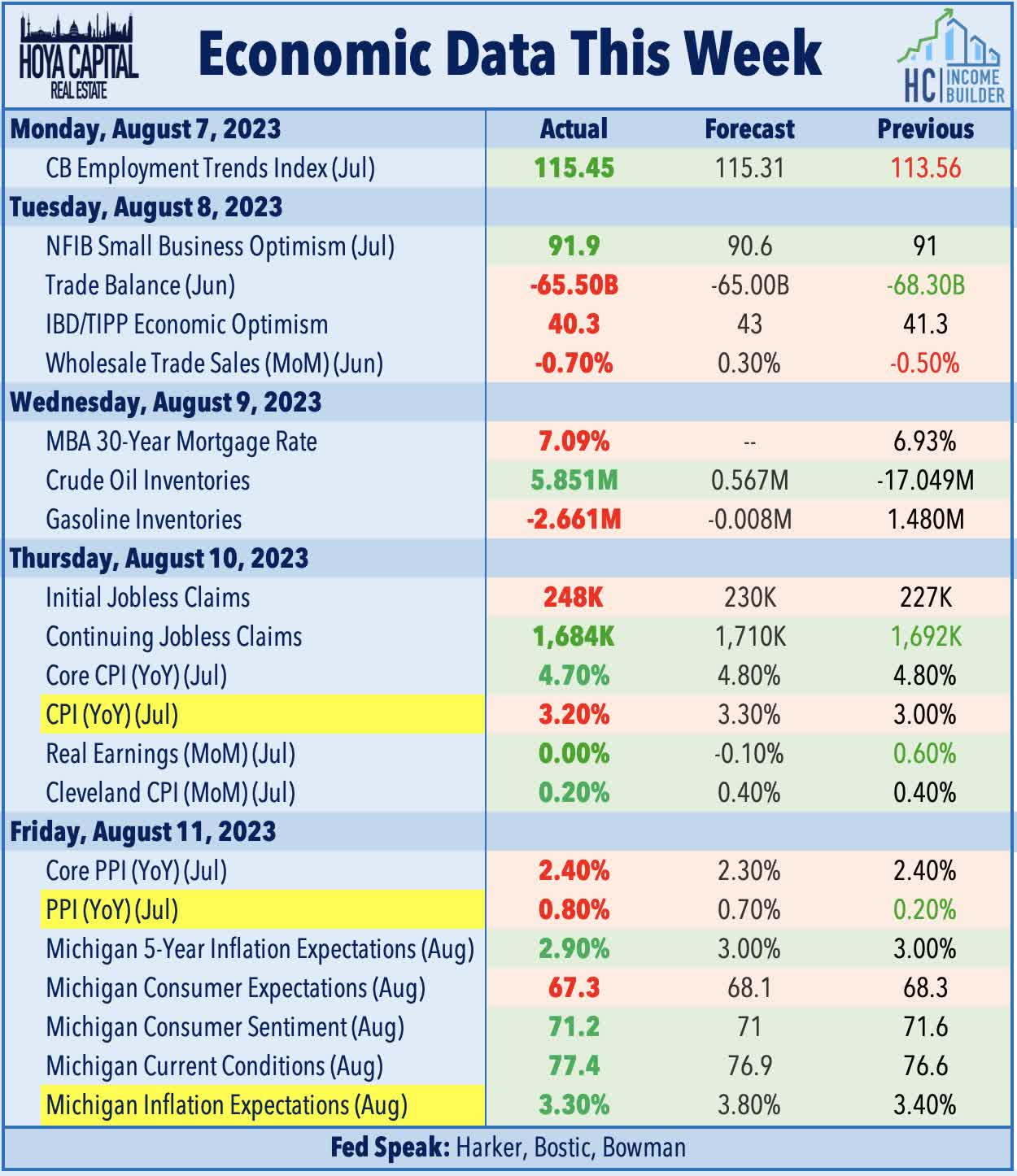

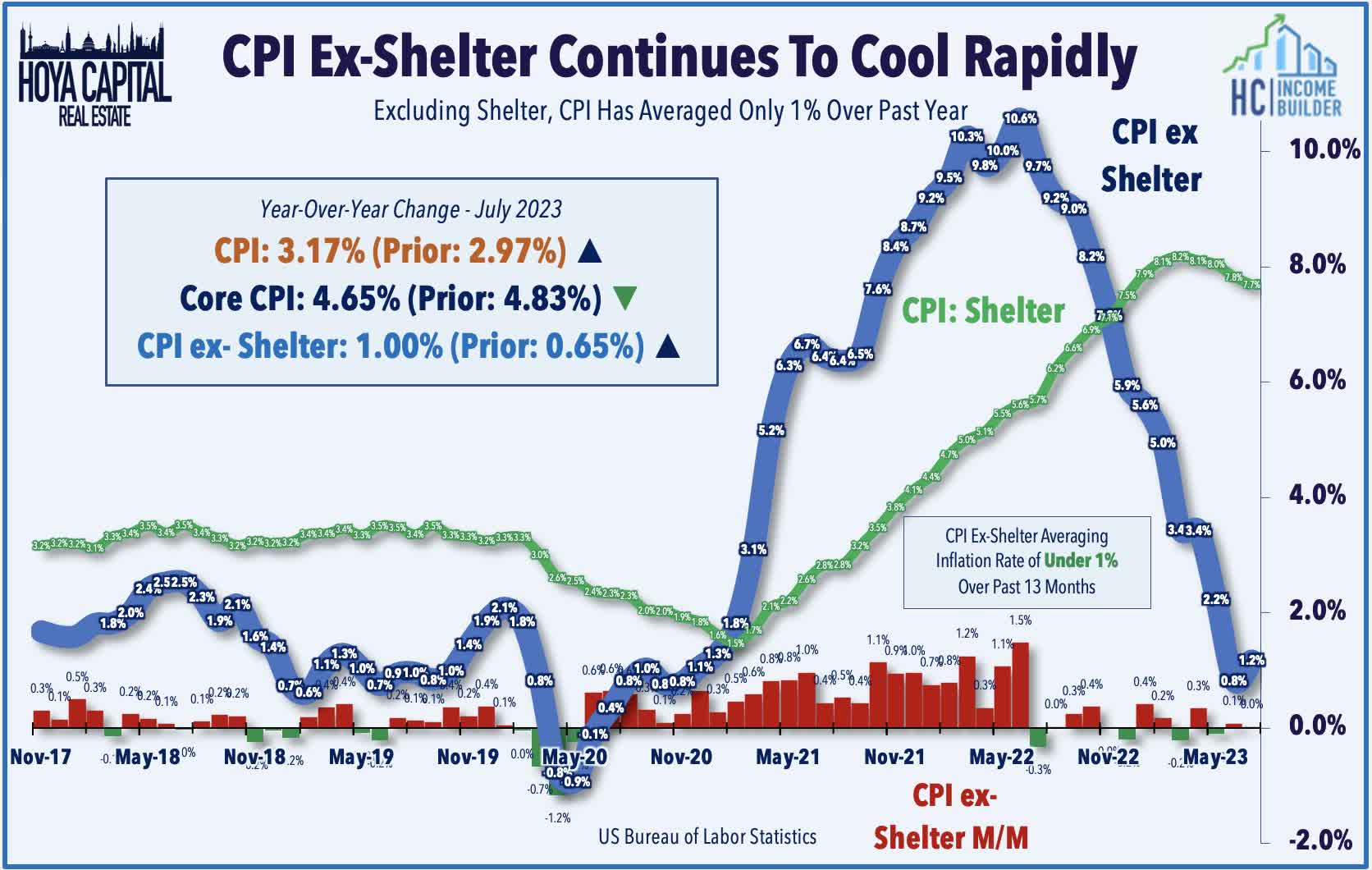

All eyes were on the Consumer Price Index report this week, which showed a continued cooldown in inflationary pressures from the four-decade-high levels seen last summer, but the pace of disinflation shows signs of moderating amid an energy price rebound. Headline CPI inflation posted a 3.17% year-over-year increase in July - below the consensus estimate of a 3.3% increase - but up slightly from the 2.97% increase last month. As we've discussed since early in the pandemic, the delayed recognition of shelter inflation continues to heavily distort the headline and core metrics, resulting in an incorrect illusion of "sticky" inflation that has not existed in the corrected metrics. While the CPI Shelter Index continues to show a nearly 8% year-over-year increase in rents, real-time shelter inflation data via Zillow, Case Shiller, and Apartment List show annual increases in rent and home prices ranging from -0.5% to 2.0%. The metric that we watch most closely - CPI-ex-Shelter Index - posted just a 1.00% year-over-year increase in July, as shelter inflation accounted for over 75% of the overall increase in the year-over-year headline CPI figure.

{kind=link}

While the Shelter component will start to become a disinflationary tailwind later this year, and while the Median CPI series has shown an encouraging "broadening-out" of disinflation in recent months, the recently-favorable path of disinflation - and by extension, the 'soft landing' - will become considerably more challenging if the Energy component suddenly stops pulling its weight. Energy has been the leading downside contributor to headline inflation since last June and - despite only holding a 7% weighting in the CPI basket - was still able to knock off over a full percentage point from the annual headline rate in July. The downward contribution was below that of June, however, and the comparables will get increasingly less favorable in the months ahead. WTI Crude Oil prices - the dominant input in the CPI energy basket - peaked in June 2022 at roughly $120/barrel and had declined as much as 45% from those levels to $67/barrel at recent lows in June before rebounding to above $80/barrel in recent weeks. Retail gasoline prices, meanwhile, also peaked in June 2022 at $5.11/gallon and bottomed in late December at $3.20, but have since increased by 23% from those levels to $3.94/gallon.

{kind=link}

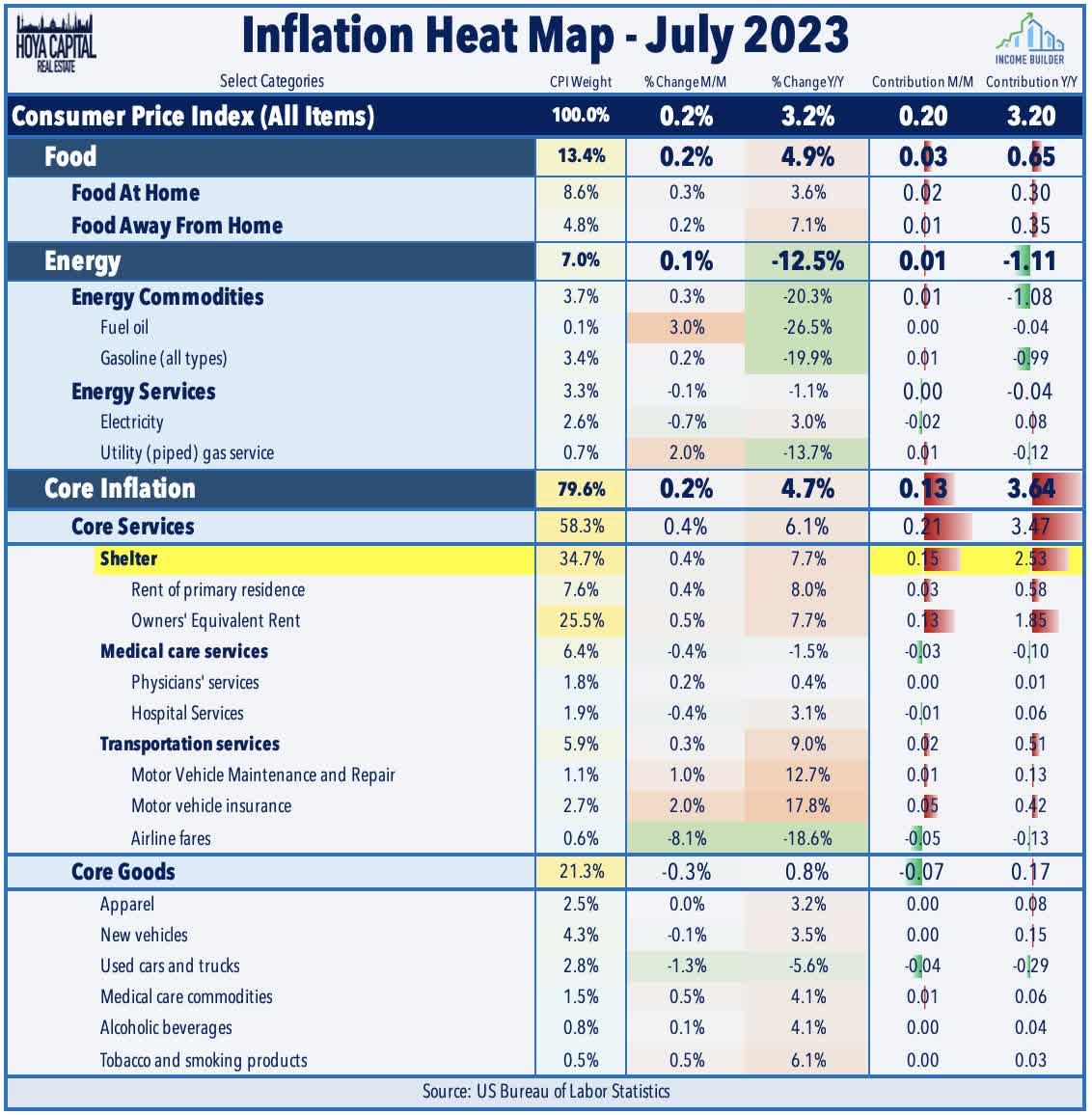

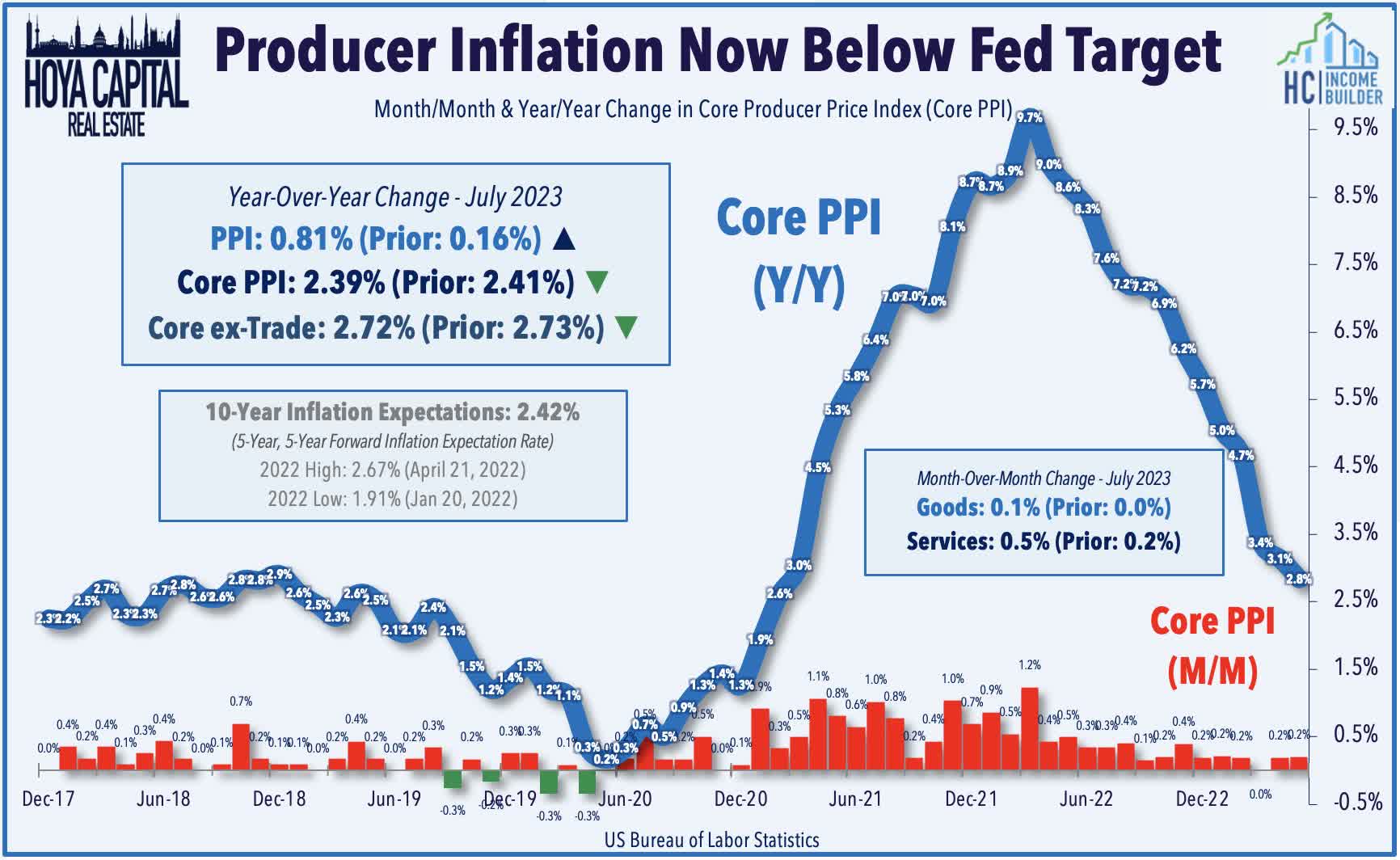

The Producer Price Index data the following day showed similarly mixed trends across the Headline and Core metrics and within the Goods and Services categories, providing evidence for both sides of the inflation debate. The headline PPI rose 0.3% in July - slightly hotter than consensus expectations - which lifted the year-over-year increase to 0.8%, up from 0.2% in the prior month. As with the CPI report, the two Core PPI metrics (PPI ex- Food/Energy and PPI ex-Food/Energy/Trade) continued to trend lower. The Services index increased 0.5% in July - the largest rise since August 2022 - but nearly half of the increase was traced to a single category: portfolio management, a category that is swung around by stock market valuations. The PPI Index for Core Unprocessed Goods - reflecting prices earlier in the production pipeline - declined by the most since last October.

{kind=link}

The most encouraging inflation report of the week came via the Michigan Survey of Consumers data on Friday, which showed a decline in 1-year consumer inflation expectations to the lowest levels since early 2021 and a decline in 5-year inflation expectations to the lowest in six months. The report also showed that overall Consumer Sentiment ticked down slightly in early August from the highest levels since 2021, as a slightly more upbeat view of current conditions was offset by a modestly more pessimistic consumer outlook. Earlier in the week, the IBD Consumer Sentiment index showed a more significant dip in consumer sentiment, with its headline metric declining to 12-month lows in its August report. Notably, the Personal Financial Outlook sub-index - which had previously been one of the more positive signals - returned to negative territory for the first time in six months.

Hoya Capital

Equity REIT Week In Review

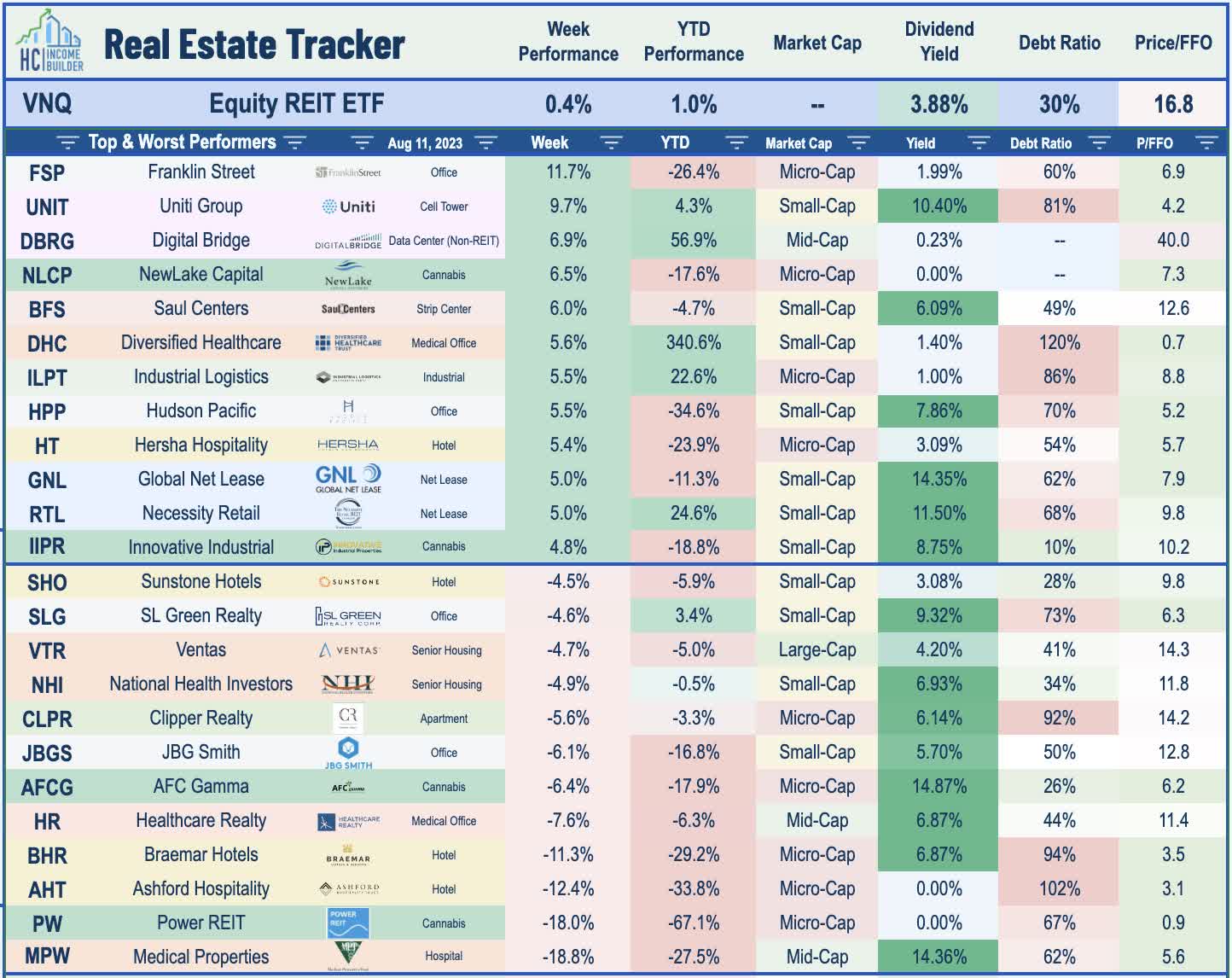

Best & Worst Performance This Week Across the REIT Sector

{kind=link}

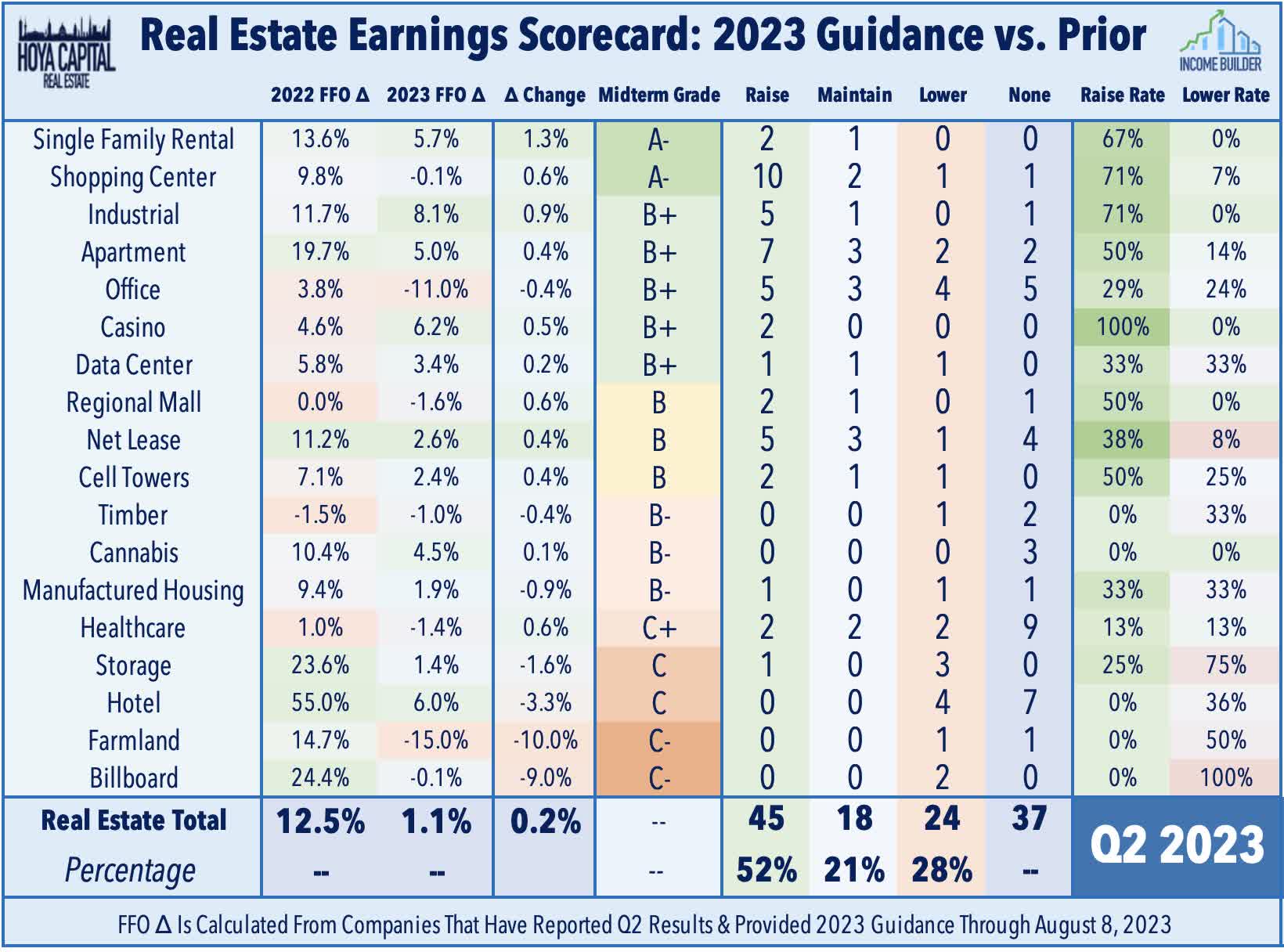

The final two dozen REITs reported earnings results this week. As noted in Winners of REIT Earnings Season , of the 86 equity REITs that provided full-year Funds from Operations ("FFO") guidance, 52% raised their full-year earnings outlook while 28% lowered guidance, a "raise rate" that was below Q1 but slightly better than the S&P 500 average. Buoyant residential rent growth- particularly in the supply-constrained single-family space - was one of the prevailing themes of the quarter, fueling a particularly strong set of reports from residential REITs. Retail REITs have enjoyed an under-discussed revival over the past 18-24 months as store openings have considerably outpaced store closings over the past two years, driving occupancy rates to record highs and fueling impressive double-digit rent growth. Office REITs posted the strongest stock performance this month as results have been "less bad" than feared, and there are signs that the "return to the office" has picked up steam.

{kind=link}

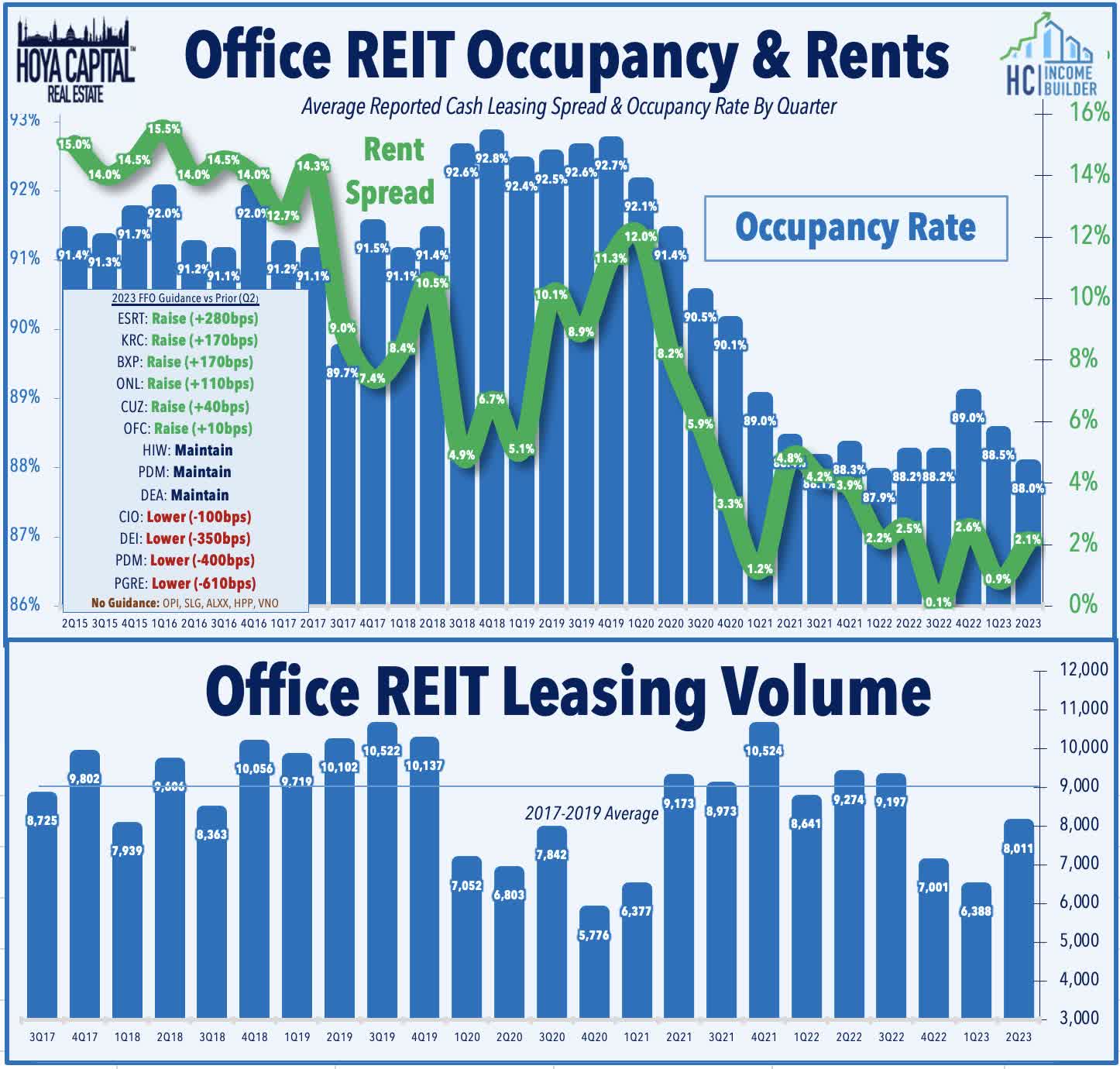

Office : Beginning with the upside standouts this week, Orion Office (ONL) - the office REIT that spun-out from Realty Income following its merger with Vereit - rallied 6% this week after reporting strong report and raising its full-year outlook. The sixth office REIT to raise its full-year FFO guidance this earnings season, ONL now expects FFO growth of -10.6% this year, a 110 basis point improvement from its prior midpoint of -11.7%. DC-focused JBG SMITH (JBGS) dipped more than 6% this week, however, after reporting mixed second-quarter results and noting that, based on tenant discussions, it expects significant vacancies in its National Landing property, where it has 1.8 million square feet of office space (27% of annualized rents). JBGS now expects vacancies totaling 1.2 million square feet after Amazon halted plans to expand its "HQ2" earlier this year. In our Earnings Recap , we noted that the battered office REIT sector have led the gains this earnings season on the heels of a slate of surprisingly solid reports showing that leasing activity and pricing trends do indeed appear to have rebounded in recent months, with total volume trending toward levels that are only slightly below the pre-pandemic averages after two historically weak quarters.

{kind=link}

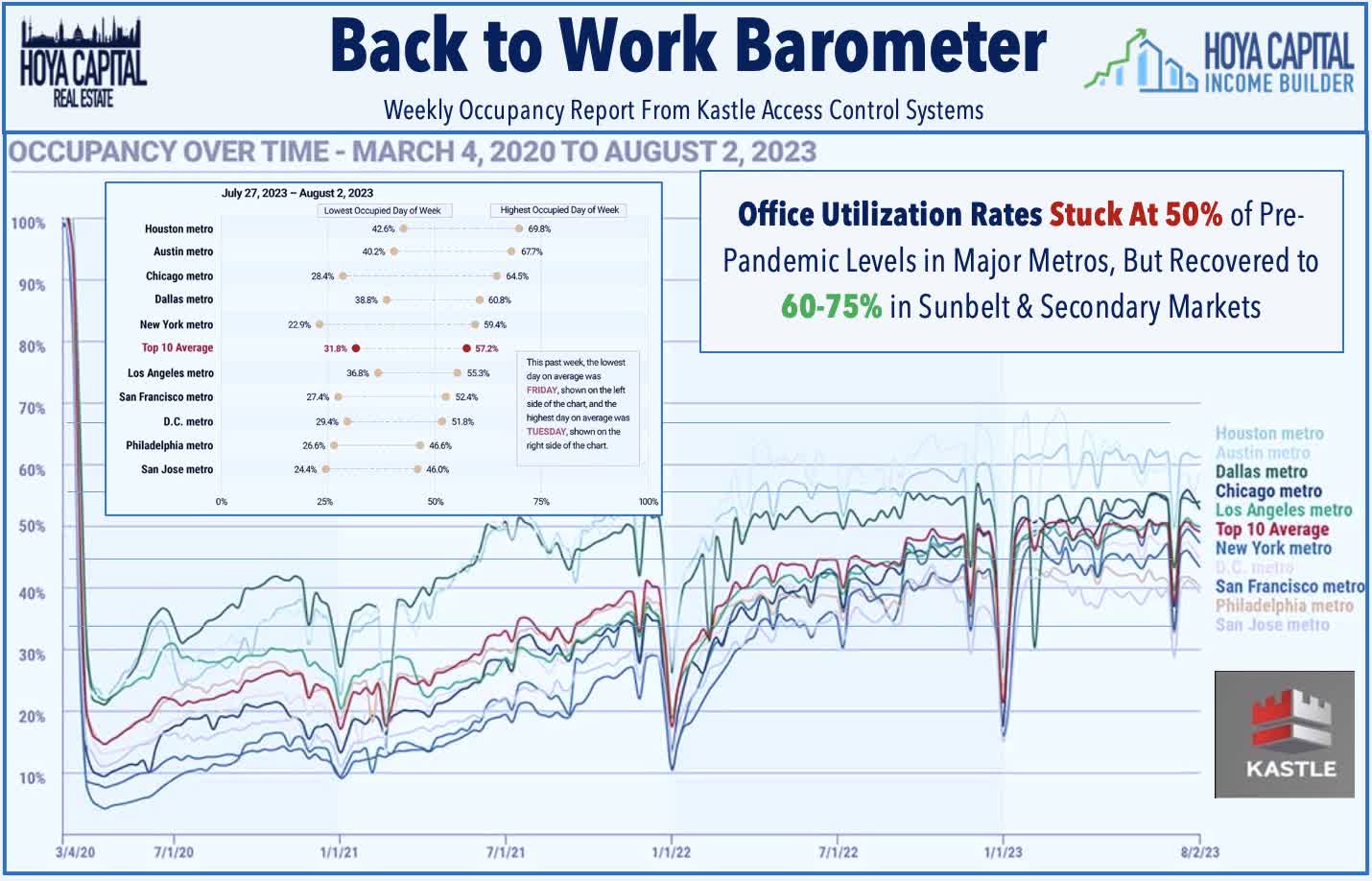

Office REITs also received some potentially good news this week from an unexpected source, as tech firm Zoom - a company that has been the "poster child" of the Work from Home Era - made a splash by calling its employees back to the office. A memo to employees detailed a new "hybrid" approach to WFH whereby employees who live near a Zoom location must be on-site at least two days per week, a move that comes alongside a recently-announced workforce reduction, consistent with the theory that office utilization rates will actually improve as job growth cools and as workers yield some negotiating leverage. Recent Data from Kastle Systems shows that office utilization rates has remained "stuck" at around 50% of pre-pandemic levels in Coastal markets and around 60-75% in Sunbelt and secondary markets. Office REITs were also impacted this week by WeWork's statement that it sees "substantial doubt" in its ability to continue to operate, citing sustained losses and canceled memberships to its office spaces. WeWork’s stock has plunged 98% since the company went public in October 2021.

{kind=link}

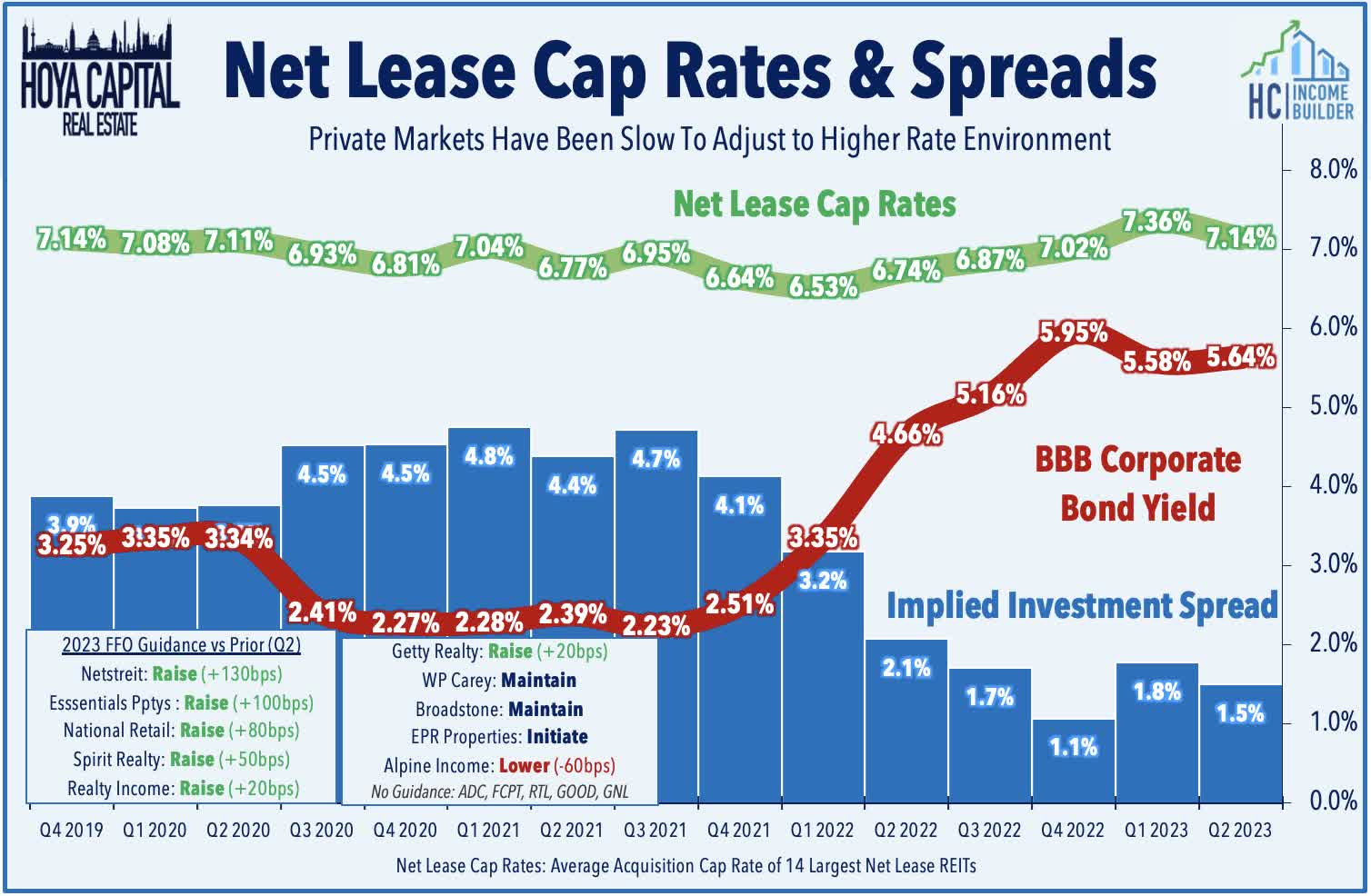

Net Lease : Spirit Realty (SRC) gained 1% this week after reporting solid second-quarter results and raising its full-year FFO outlook. Spirit also hiked its dividend by 1% to $0.6696/share (6.7% dividend yield), becoming the 64th REIT to raise its dividend this year, offset by 23 dividend decreases. SRC now expects full-year FFO growth of 0.8% - up 80 basis points from its prior outlook - and trimmed its full-year net acquisitions target to 400M from $450M. SRC echoed commentary from other net lease REITs that private market property owners have generally been slow to adjust their valuation expectations to the higher interest rate environment, which has prompted most net lease REITs to scale-back acquisition plans until either market cap rates increase or financing costs decrease. During the quarter, SRC acquired $168.6M at a capitalization rate of 8.0%, which was 160 basis points higher than its acquisition cap rate a year ago. On average, net lease REIT acquisition cap rates increased 60 basis points from last year to roughly 7.1%, during which time benchmark financing rates increased by over 100 bps.

{kind=link}

Gladstone Commercial (GOOD) rallied 4% this week after reporting better-than-expected results highlighted by strong leasing activity, which lifted its occupancy rate by 10 basis points to 96.0%. GOOD - which owns a roughly 50/50 mix of triple-net leased industrial and office properties - recorded 502k square feet in lease renewals in Q2, up from 356k in the prior quarter. GOOD reported core FFO of $0.41/share - above analyst estimates of $0.36 - and covering its $0.30/share dividend. Postal Realty (PSTL) - which owns roughly 1,500 properties leased to the US Postal Service - gained 1% after reporting in-line results, noting that it also continues to collect 100% of rents. PSTL reported Adjusted Funds from Operations ("AFFO") of $0.27/share - which covered its $0.2375/share dividend - and noted that it acquired 39 USPS properties during the quarter for $15.8 million. In our Earnings Recap, we noted that s ix of the ten net lease REITs that provide guidance raised their full-year outlook, as strong underlying retail performance has helped to offset a more challenging acquisitions and financing environment.

{kind=link}

Hotel : Service Properties Trust (SVC) rallied 4% this week after concluding hotel REIT earnings season with a solid report and highlighting recent moves to shore up its balance sheet. SVC's limited-service hotels generated EBITDA growth of 26% from last year, which offset a 3% decline in EBTIDA at its full-service hotels - a theme of limited service outperformance that we've observed across the hotel REIT sector this earnings season. Providing color on demand trends, SVC noted that its "certainly seeing the softening of leisure travel in our portfolio" and cited a combination of "revenge travel" moderation, lower consumer discretionary income due to higher interest rates, and the strength of outbound international travel without an offsetting increase in inbound international travel. Hotel REIT earnings season was overall quite disappointing with four of the five REITs that provide full-year FFO guidance lowering their outlook, while four of six that provide Revenue Per Available Room ("RevPAR") guidance lowered their outlook. Overall, the six guidance-providing hotel REITs now expect RevPAR to increase by 8.2% this year, down from the 8.6% outlook last quarter. Recent TSA Checkpoint data shows that throughput was at 99% of pre-pandemic levels in July, a slight downshift from the 101% average in the first-half of 2022.

{kind=link}

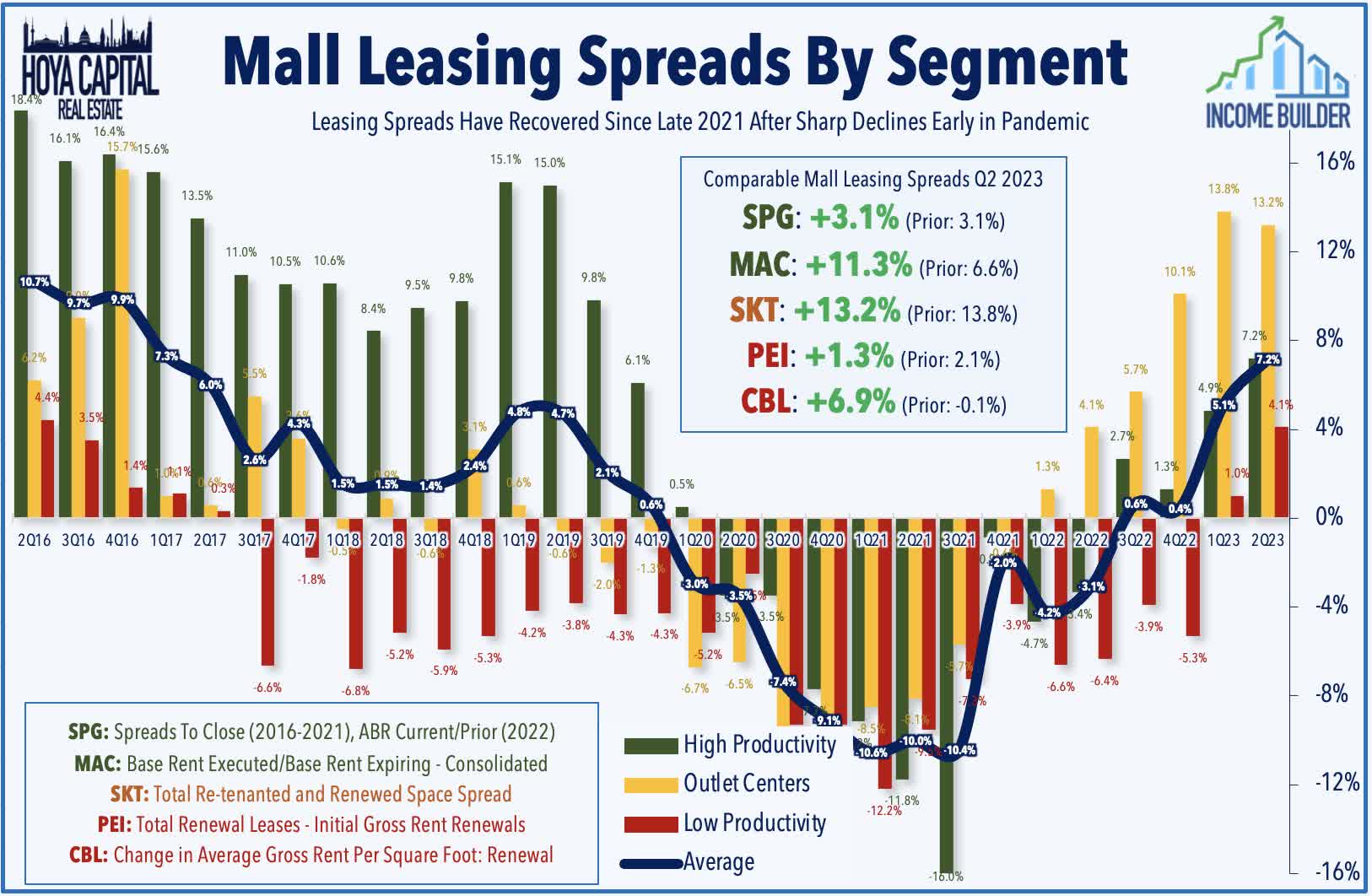

Malls : Macerich (MAC) finished modestly higher this week after reporting decent second-quarter results and maintaining its full-year earnings outlook. As with its mall peers Simon (SPG) and Tanger (SKT), which reported results the prior week, leasing volumes and pricing were the highlights of MAC's report. Consolidated portfolio occupancy increased to 92.6% - up 170 basis points from last year - well above the pandemic lows of 87.9% but still below the roughly 95% pre-pandemic average. Re-leasing spreads increased by 11.3% on a trailing twelve-month basis, up from 6.6% last quarter and marking its strongest quarter since 2019. Leasing volumes, meanwhile, were up 34% through the first six months of this year compared to the same period last year. MAC reiterated its guidance calling for FFO decline of 8.2% this year as interest expense remains a significant drag on its earnings. CBL & Associates Properties (CBL) slipped 1% this week despite reporting solid second-quarter results and raising the midpoint of its full-year FFO guidance driven by its strongest quarter of leasing activity since before the pandemic. CBL signed 875,000 square feet of leases in Q2 and achieved blended rent spreads of 6.9% on these leases - its strongest quarter of rent growth in nearly a decade.

{kind=link}

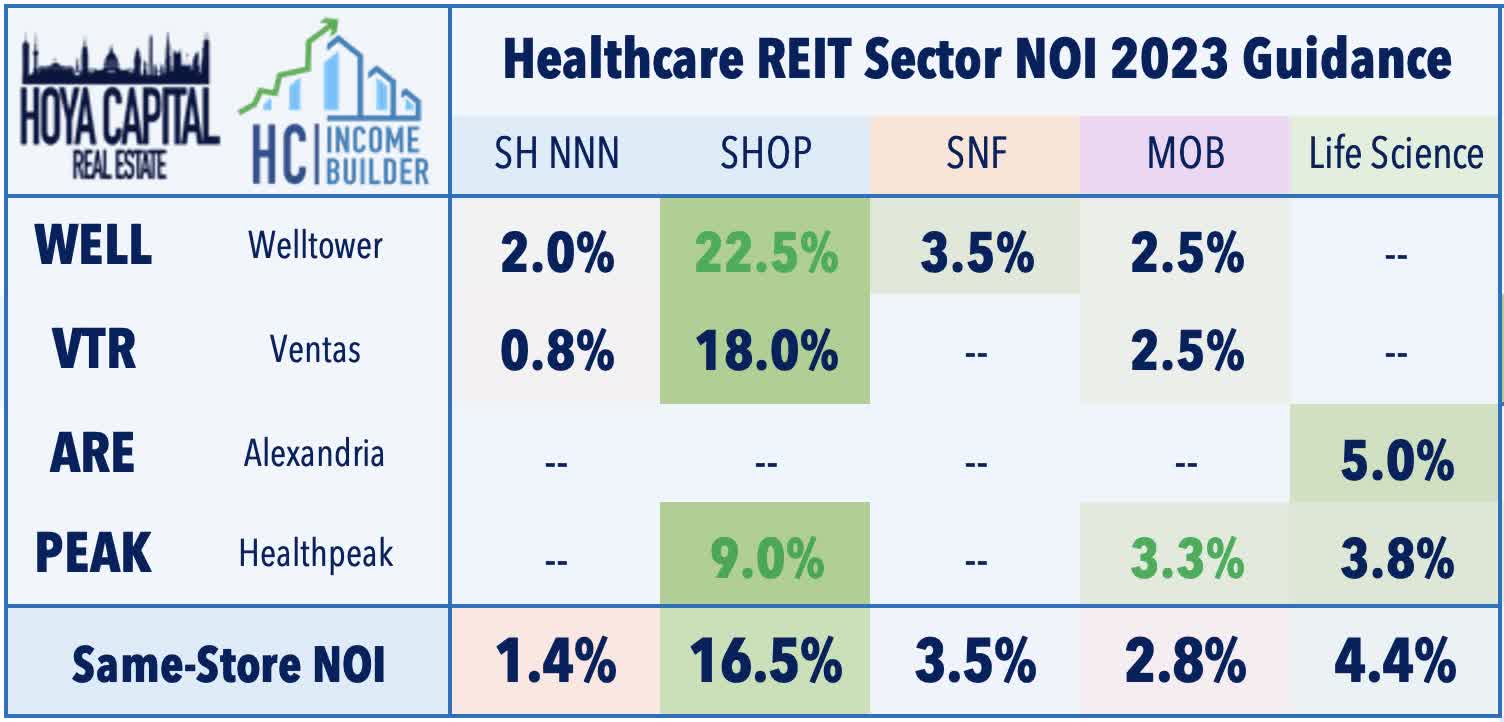

Healthcare : On the downside this week, hospital owner Medical Properties Trust (MPW) dipped more than 15% this week after trimming its full-year outlook and reporting ongoing operating struggles with two of its largest tenants - Steward Health Care and Prospect Medical - which have faced industry-wide headwinds resulting from elevated labor expenses and the waning of COVID-era relief programs. MPW noted that it would contribute up to $140M as part of a $600M credit facility to Steward - its largest tenant at roughly 20% of annual revenues - as part of a private credit lending syndicate. MPW also noted that Prospect - its fourth largest tenant at 6% of revenues - paid equity in lieu of cash for its 2023 rent, an equity interest that was appraised at $655M. Medical office building owner Healthcare Realty (HR), meanwhile, dipped 7% after reporting mixed results and soft leasing activity in Q2 with total volume of 1.04M, down from 1.46M in Q2. For the five MOB-focused REITs, FFO is lower by an average of 7.3% through the first half of 2023 amid pressure from higher interest rate expenses and a downshift in leasing activity.

{kind=link}

Sticking in the healthcare space, National Health Investors (NHI) - which focuses on triple-net-leased senior housing and skilled nursing facilities - dipped 6% after reporting soft results and lowering its full-year FFO outlook, citing higher rent concessions and higher interest rate expense. NHI now expects full-year FFO growth of 0.7% - down from its prior outlook of 2.2% growth - which would be well below that of its two senior housing REIT peers, Welltower (WELL) and Ventas (VTR), which reported strong results earlier in earnings season led by strength in their Senior Housing Operating Portfolio ("SHOP"). NHI reported that it failed to collect full rent payments from two senior housing operators, citing lingering labor-related margin pressures. NHI's SHOP performance - which recorded minimal occupancy gains compared with the prior quarter - has also lagged behind its peers. NHI commented, "We anticipated that the persistent industry pressures could lead to uneven quarterly results."

{kind=link}

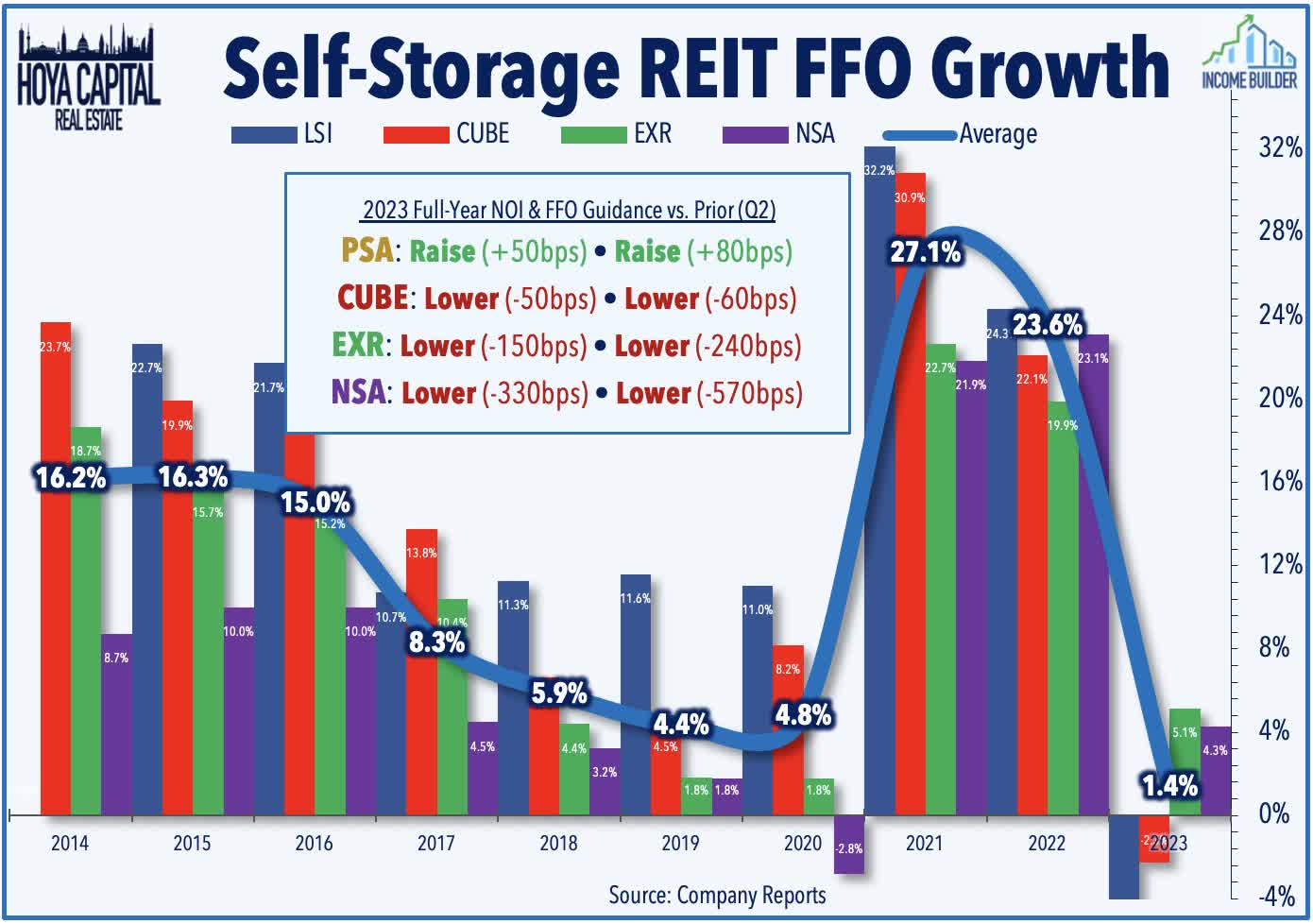

Storage : National Storage (NSA) finished flat this week after reporting soft second-quarter results and lowering its full-year NOI and FFO outlook, rounding out a surprisingly weak quarter for the storage REIT sector in which three-of-four REITs lowered their earnings outlook. NSA - which focuses on cheaper storage units in secondary and tertiary markets compared to its larger peers - commented that it "experienced a softer spring leasing season, and the interest rate environment was tougher than expected." NSA now expects its FFO to decline by 5.3% this year - a sharp downward revision from its prior outlook for 0.4% growth - and expects to report same-store NOI growth of 1.0% - down from its midpoint of 4.25% last quarter. All four self-storage REITs reported double-digit declines in "street rates" on new customers in Q2, but this pricing weakness was more-than-offset by high-single-digit rent growth on renewal leases, resulting in a total rent PSF increase of about 6.5% during the quarter compared with last year. Since the start of the pandemic self-storage rents have increased by roughly 30%.

{kind=link}

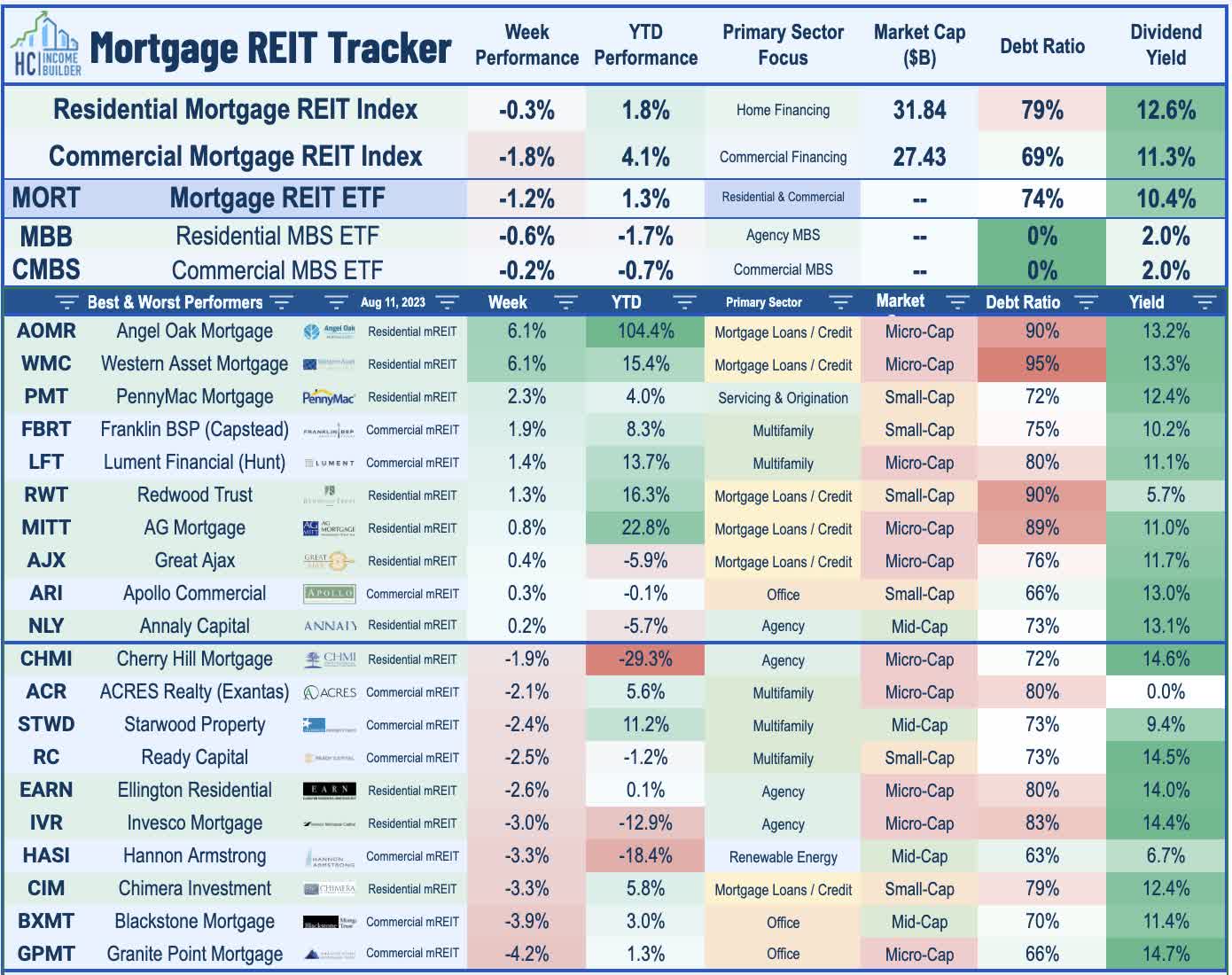

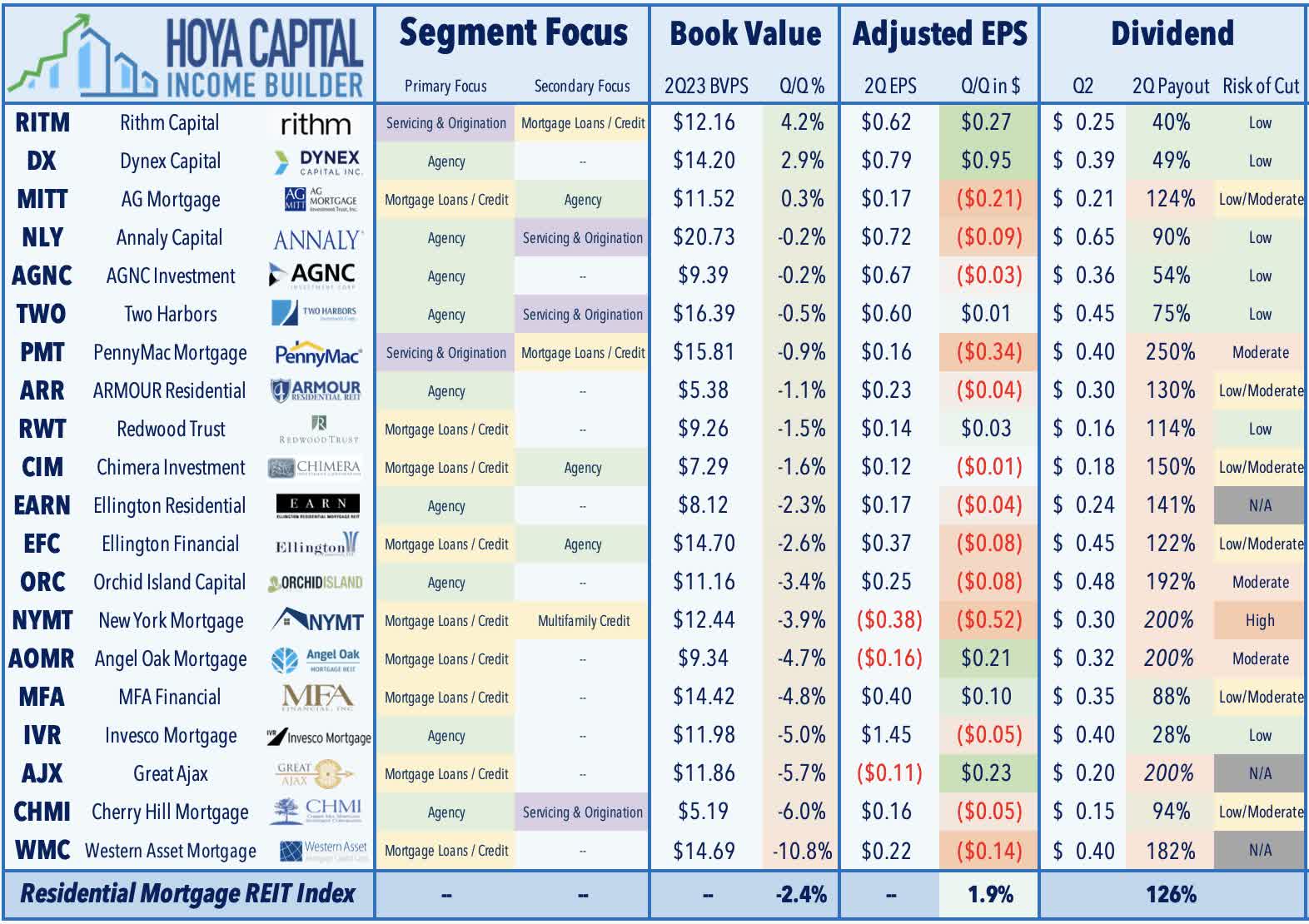

Mortgage REIT Week In Review

Mortgage REITs finished slightly lower this week, with the iShares Mortgage Real Estate Capped ETF (REM) slipping 1.2%, as earnings season wrapped up with results from nearly a dozen mREITs. On the upside this week, Western Asset (WMC) rallied 6% after it terminated its previously announced acquisition agreement with non-traded REIT Terra Property and will instead be acquired for higher consideration by fellow mREIT AG Mortgage (MITT). MITT will pay $11.23 per WMC common share, consisting of stock consideration of $10.11 per share and cash consideration of $1.12 per share, representing a 34% premium to WMC’s closing stock price before the initial announcement on July 12.

{kind=link}

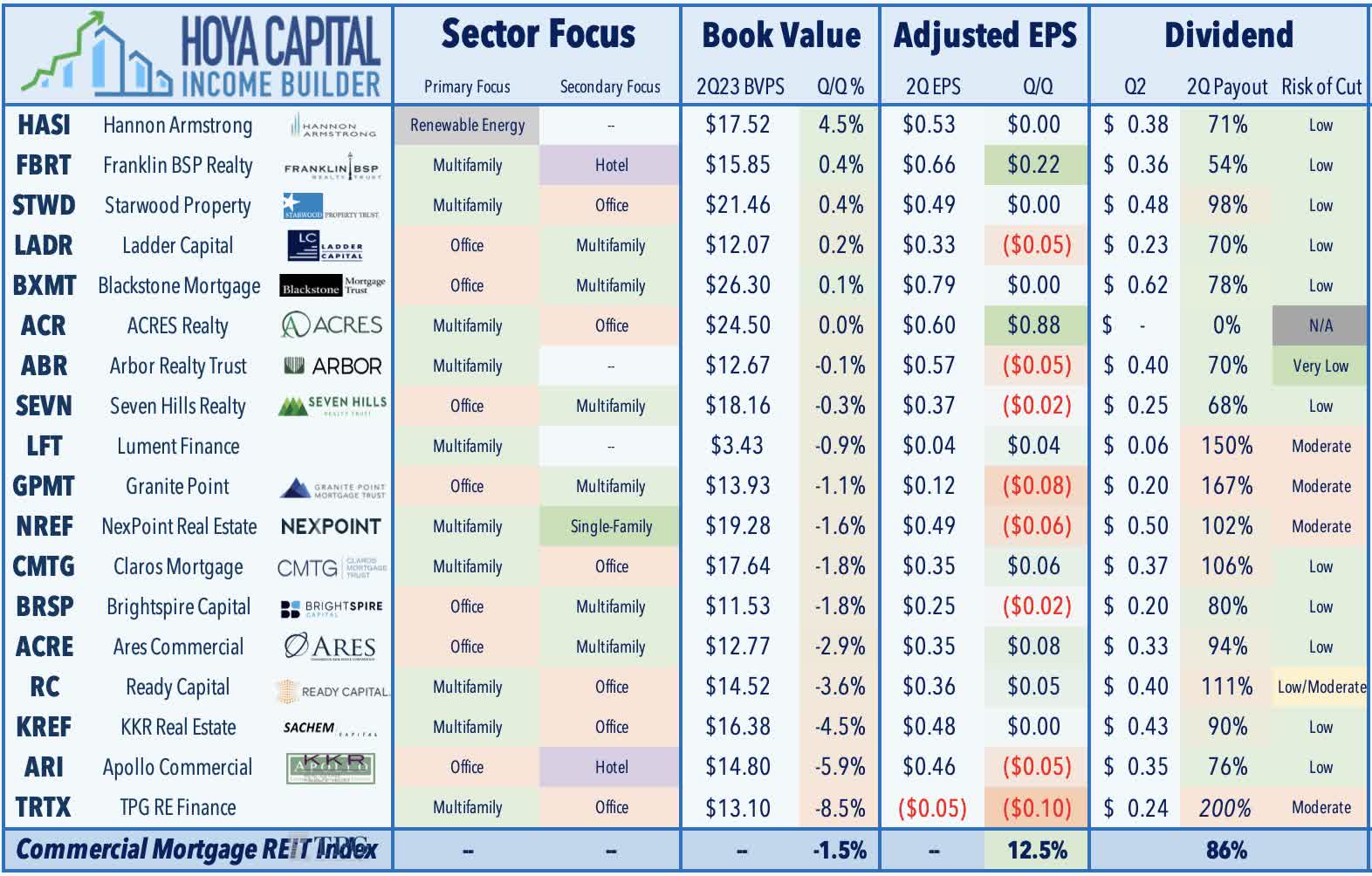

On the downside this week, office-focused lender Granite Point (GPMT) slipped 4% after reporting distributable EPS of $0.12 - below consensus estimates and shy of its $0.20 dividend - resulting from the default of a $29M loan on a Phoenix office property. GPMT also noted that its Book Value Per Share ("BVPS") declined 1.1% to $13.93 due to an increase in its Current Expected Credit Loss ("CECL") to 4.1% of its loan book, up from 3.8%. Small-cap multifamily-focused lender Lument Finance (LFT) was among the upside standouts after reporting a sequential increase in its distributable EPS, while its BVPS declined by less than 1% during the quarter to $3.43. For commercial mREITs, Book Values have declined by an average of 2% sequentially in Q2 - a relatively steep decline by historical standards - losses which have been driven almost entirely by increases in allowances for office-related assets.

{kind=link}

On the residential mREIT side, Angel Oak (AOMR) - which went public in 2021 - was among the leaders this week after reporting modestly improving earnings metrics, noting that its distributable EPS improved to -$0.16 in Q2 from -$0.37 in the prior quarter. Ellington Residential (EARN) was among the laggards, however, after reporting comparable EPS of $0.17 - down from $0.21 in the prior quarter - while noting that its BVPS declined 2.3%. Residential mREITs have reported an average BVPS decline of 2.4% in Q2 - roughly consistent with expectations - but adjusted EPS has increased by roughly 2% sequentially, providing marginally more support for these REITs' dividends. Commentary was generally more upbeat than recent quarters with many firms seeing healthy incremental investment spreads and citing the increased capital requirements on traditional banks as a long-term tailwind.

{kind=link}

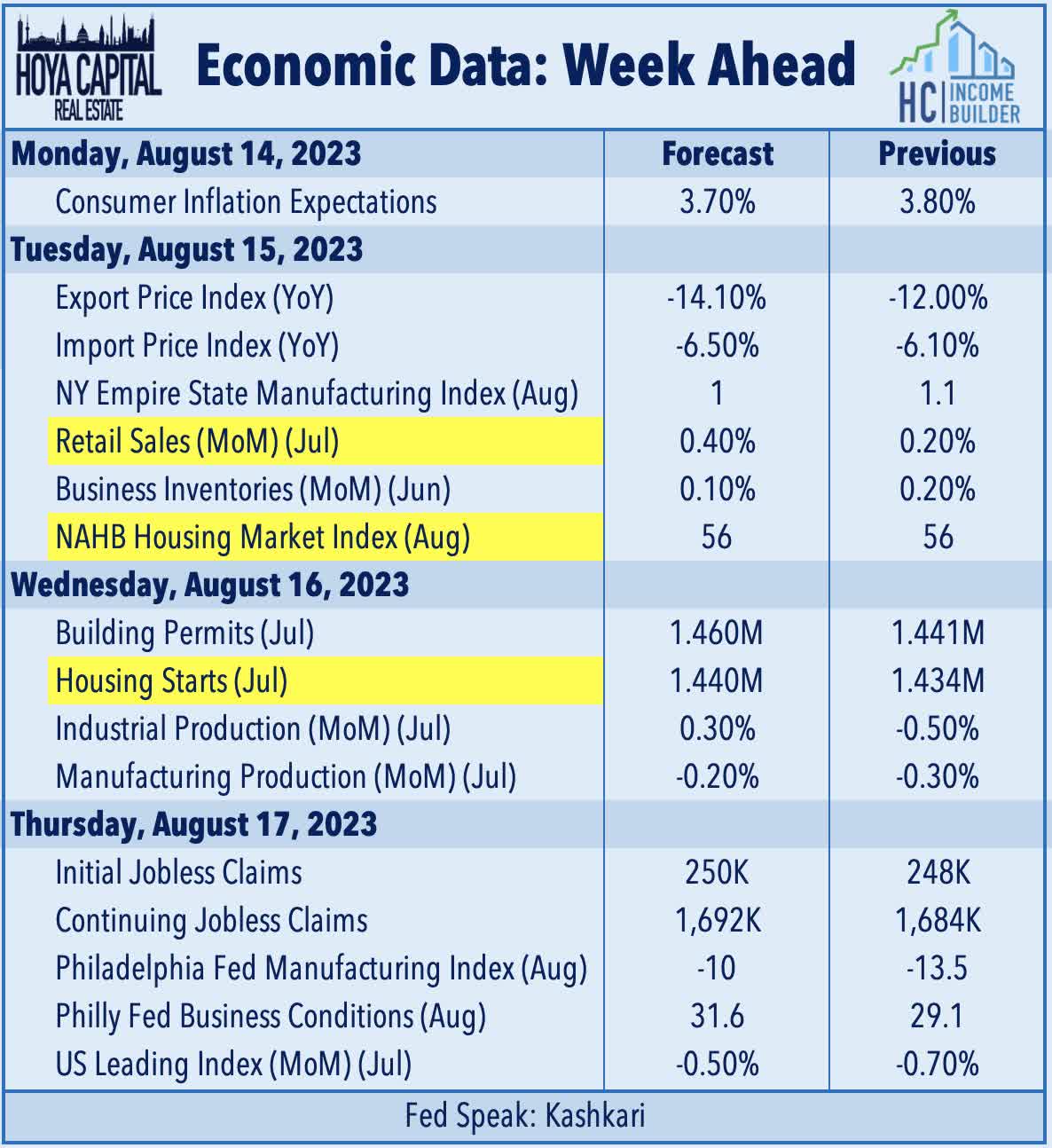

Economic Calendar In The Week Ahead

The state of the U.S. housing market will be in focus in the week ahead. The busy week starts on Tuesday with the NAHB Homebuilder Sentiment data for August, which looks to extend its streak of seven-straight monthly increases after dipping to near-15-year lows late last year. On Wednesday, we'll see Housing Starts and Building Permits data for July, which are expected to accelerate slightly after the pullback in June. We'll also see Retail Sales on Tuesday, which is expected to post modest gains for a fourth-straight month, which follows a stretch of four-of-five monthly declines. We'll also be watching weekly Jobless Claims data on Thursday.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

Disinflation Loses Energy