CA - Diversified Royalty: This 9.5% Yielder Lives Up To Its Name

2023-11-15 04:29:22 ET

Summary

- Diversified Royalty earns a royalty stream from a varied group of businesses in North America.

- While we like the equity, we own the debt.

- We review the recent results to see if the equity valuation is compelling at this time.

All values are in CAD unless noted otherwise.

We have covered Diversified Royalty Corp. ( BEVFF ) ( DIV:CA ) fairly regularly on this platform. This is partly because we have skin in the game, in the form of debt ownership, but also because this business has grown at a fair pace over the last several years.

For the uninitiated, DIV is a top line royalty corporation, earning revenue from a diverse group of businesses, located across North America.

{kind=link}

Of the seven royalty partners noted above, two are very recent. Stratus was added in November 2022, whereas barBurrito became part of the Diversified family subsequent to Q3 of this year. The aim of this company is twofold:

The Company's primary objectives are to: (i) purchase stable and growing royalty streams from Royalty Partners, and (ii) increase distributable cash per share, by making accretive royalty purchases.

Source: Q3-2023 MD&A

The revenue agreements are based on either a percentage of the gross sales, fixed annual payments with contractual escalators, or in the case of the real estate franchise in the mix, the number of agents in the pool. Besides royalties, it also earns management fees from several of its royalty partners. Its expenses are few and comprise salaries and benefits, general and administrative, professional fees and interest on credit facilities.

We have been buyers of the debt, rather than the common stock of this company over the last few years. The verdict after reviewing the Q2 results was no different. The results, along with its resiliency against inflationary pressures are impressive. The 8.5% dividend yield was not unappealing either. The valuation, however, did not compel us to buy the equity, especially since the risk-free rates were close to 5% then. Offering a 9.45% yield to maturity, the debt got our vote and the 4X debt to normalized EBITA sealed the deal.

So debt to EBITDA is 4.0X and you have to ask yourself whether you think at least a 4.0X EBITDA multiple makes sense for those business. That answer is of course a strong "yes". Currently, as shown a little higher up in the article, the EV to EBITDA multiple is near 10.0X, but by buying the debt you just need to it be worth more than 4.0X to have a safe investment. We really like the debentures here and will allocate some additional money over the next few months.

Source: Diversified Royalty: The 9.4% YTM Debentures Remain A Safe Bet

The price of the Diversified Royalty Corp. 6.00% Convertible Unsecured Subordinated Debentures was $90 at the time of writing that piece. While it appreciated at the of writing that piece was $90.01, and while it went as high as $94 in the interim, it is back to $90 now.

{kind=link}

We continued holding the debentures through the short-lived euphoria, with the eye firming on the YTM prize. The common equity on the other hand has not done well for its investors.

Let us dive into the Q3 results and see if the equity valuation is juicy enough for a bite.

Q3-2023 Results

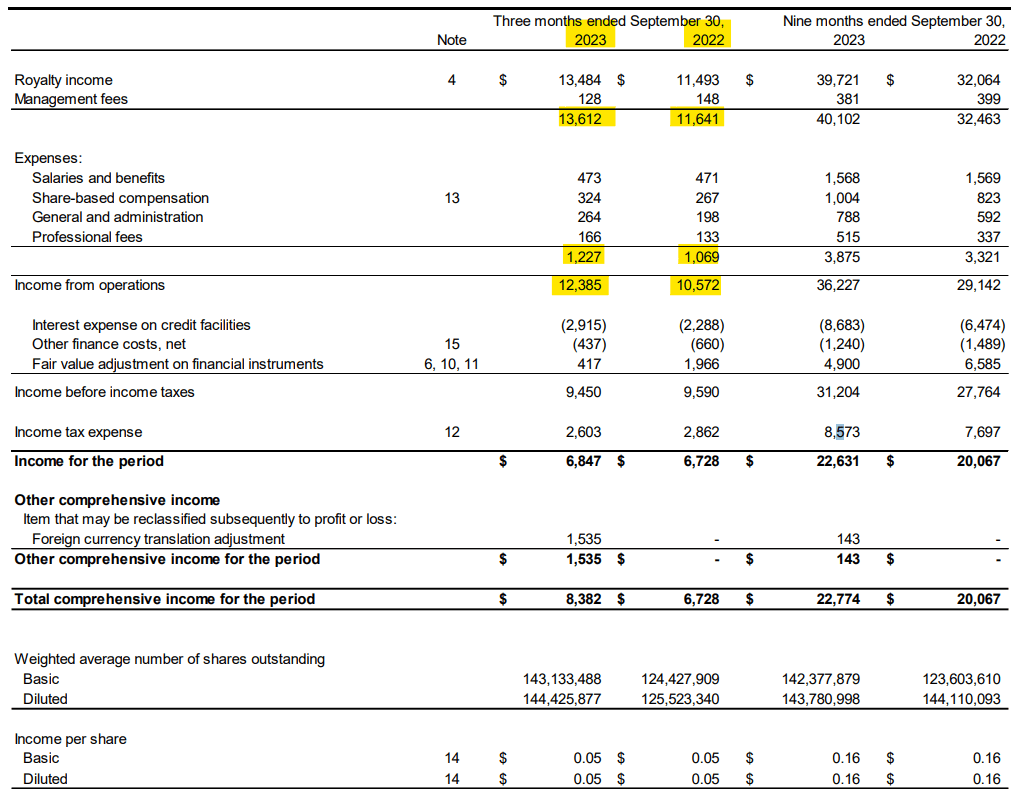

Top line revenue increased by close to 17% year over year. The increase in operating expenses was slightly less at around 15%. The year over year growth in the net income from operations was less than what we saw in Q2 (29%), but still a healthy 17%.

{kind=link}

Next we dug deeper into the revenue growth.

{kind=link}

- Mr. Lube royalties are tied to the system sales of the automotive business, and they continue to witness year over year growth. That, along with the increase in the number of stores in the royalty pool, increase the take home portion for DIV.

- Stratus , a commercial cleaning and building maintenance business, partnered with DIV in November 2022. Here, the royalty payments are fixed with annual increases built in. The revenue has been steady every quarter, with minor fluctuations due to foreign exchange as it predominantly does business in the U.S.

- The royalties for Oxford Learning , a tutoring service that operates in Canada and the U.S. are tied to the system sales, that remained steady in relation to the comparative quarter.

- The AIR MILES reward program continues to feel the pain from the Sobeys exit. DIV's revenue is tied to the gross billings of the Canadian loyalty program, and with that taking a hit, this royalty play saw a close to 38% decline in its piece of the pie.

- The casual dining chain, Mr. Mikes , pays DIV royalties based on its top line sales, which increased by around 3.6% year over year. The Q3-202 numbers include around $580 thousand in deferred royalties from the pandemic era. Q3 of 2023 also includes some of that, but less than a tenth of the prior year amount.

- Sutton , a residential real estate business, has 2% annual contractual increases built into its agreement with DIV. This increase is effective July 1 each year. Accordingly, we can see that reflected in the year over year uptick in DIV's Sutton sourced revenue in the above table.

As noted earlier in the piece, barBurrito was added subsequent to the third quarter of this year. This burrito chain's royalty agreement with DIV calls for an annual payment of $8.3 million/year, with 4% annual increases built in for the first seven years. Effective 2031, DIV's revenue will be tied to the gross sales of the eatery, with possibilities of six rate increases in increments of 0.25%.

Discerning readers may have noted that one of the royalty partners, Nurses Next Door , is missing from the revenue itemization table. Since this business has the option to repurchase its rights after November 15, 2026, it is recognized as an asset on DIV's books. The inflow from this source increased as expected based on 2% annual increase effective October of each year.

{kind=link}

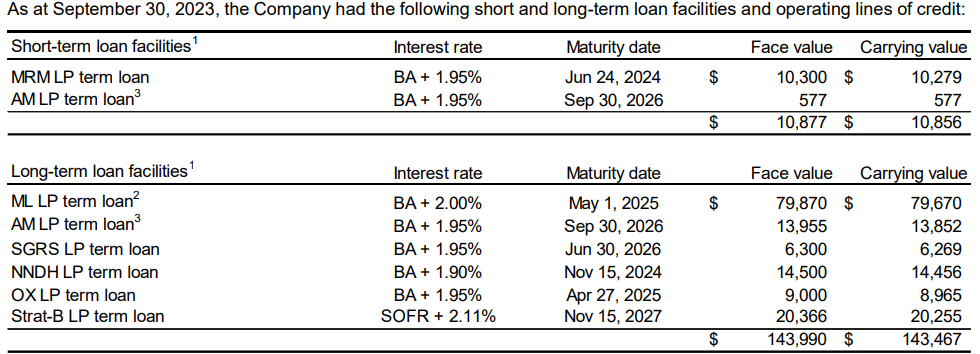

Now that we have reviewed the revenue sources, let us talk about the elephant in the room. The 27% increase in interest paid on credit facilities compared to Q3-2022 ($2,915 versus $2,288). Things cost money, and DIV bought two royalty streams within the span of one year, Stratus in November 2022 and barBurrito in October of this year. All of the borrowings are of the variable rate kind.

{kind=link}

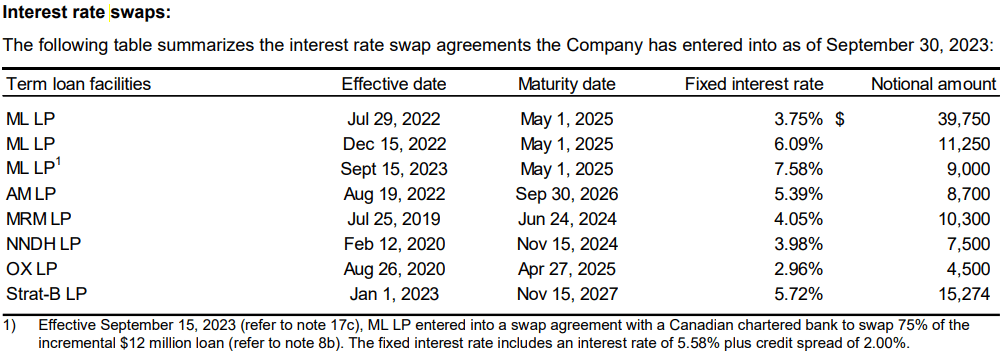

Over 70% of the above is however fixed via swaps. These swaps provide good protection against further rate hikes with the last ones covering the company till late in 2027.

{kind=link}

The Q3 numbers exclude the borrowings that pertain to the barBurrito acquisition. Of the total $108 million paid, $72 was funded by cash, most of which came from borrowings.

The cash portion of the Purchase Price was funded with (i) $50.0 million drawn from DIV's Acquisition Facility, (ii) DIV's cash on hand of $2.0 million, (iii) $10.0 million drawn from a new senior credit facility issued to BARB LP, and (iv) $10.0 million drawn from a new senior term credit facility issued to DIV (the "Additional Term Facility").

Source: Q3-2023 Report

The net income continues to keep pace with the increase in interest expenses and the coverage remains around 4.0X.

Outlook

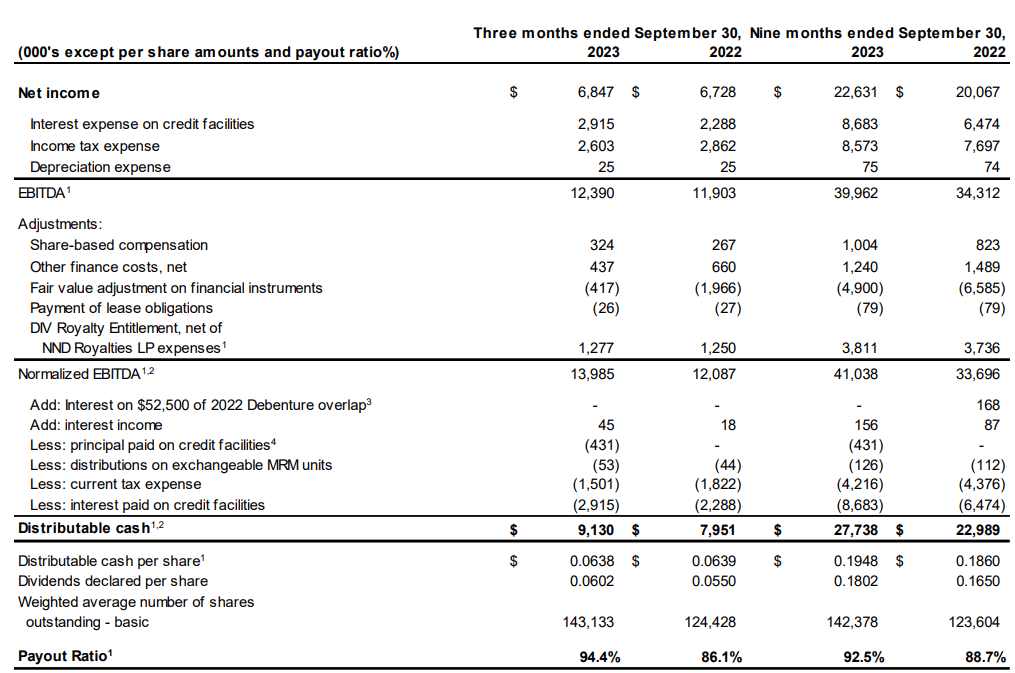

DIV works as an inflation hedge in the sense that its revenue does not depend on the costs to operate the businesses of its royalty partners. Its inflow is tied to the top-line revenue or based on fixed payments, with annual contractual increases built in. With increases in its net inflows, the company passes on the bounty to its shareholders in the form of dividend hikes. That is reflected in the payout ratio, which is in the 90s.

{kind=link}

It recently increased its monthly payout from 2 cents to 2.04 cents and at the current price of $2.58 yields close to 9.5%. The valuation has got even more inexpensive since our coverage of Q2, with the common equity trading at over 10% free cash flow yield (9.5% yield /92.5% YTD payout ratio). Additionally, unlike a few other royalty companies that we have covered in the past, Pizza Pizza Royalty Corp. ( PZA:CA ) and A&W Royalties Income Fund ( AW.UN:CA ), this company has its hands in a diverse set of businesses. The company has issued equity accretively to fund its growth and you can see that revenue per unit has also moved up over time.

We are still sticking with the debentures as we are getting around the same YTM (9.64%), while staying higher in the capital hierarchy. But the stock has appeal at these levels and we can see the possibility of equity outperforming the bonds from here.

For further details see:

Diversified Royalty: This 9.5% Yielder Lives Up To Its Name