CME - Dividend Investors Take Note - CME Group Is Back

2023-07-27 12:20:45 ET

Summary

- CME Group's stock is up 18% year-to-date after strong earnings, validating the long-term bull case.

- The company saw growth in key segments like interest rates and commodities, demonstrating the scalability of its business model.

- CME's higher rate per contract indicates increased profitability, and its commitment to steady dividend distributions makes it an attractive investment opportunity.

Introduction

CME Group ( CME ) has been a core holding of my portfolio since 2022 when I decided that this financial corporation is one of the best ways to build wealth in a highly competitive sector: by buying a company that makes money every time someone trades its futures and/or options.

Unfortunately, the company has been one of my worst performers, as investors simply weren't interested in this company, despite the fact that it benefitted from elevated volatility like no other company.

Now, CME is gaining momentum. The stock is up 18% year-to-date after getting another 4% boost after its just-released earnings.

While volumes are down due to lower volatility, the company is reporting strong rates per contract and growth in key segments like interest rates.

I believe the just-released earnings validate my long-term bull case.

In this article, I'll give you the details.

So, let's dive in!

2Q23 Was A Terrific Quarter

Let's start with the headline numbers that hit the wires first.

In its second quarter, CME Group generated $1.36 billion in revenue, which is $20 million above estimates (we can ignore that) and 9.9% higher compared to the prior-year quarter.

Adjusted EPS came in at $2.30, which is $0.11 above the consensus estimate.

- Clearing and transaction fees grew by over 9%.

- Market data revenue increased by 8% compared to Q2 2022.

- Operating expenses remained flat compared to the first quarter at $452 million, excluding license fees.

- The adjusted operating margin expanded to 66.8%, up over 250 basis points from the same period last year.

Having said that, the company started its earnings call by mentioning that 2023 presents a favorable backdrop for risk management, attributing this to continued geopolitical uncertainty and increasing capital costs for businesses.

In this case, CME is one of the few companies that sees global insecurities as a tailwind, as it benefits from increased volatility.

This is what I wrote in my most recent article on CME, titled Why CME Group Is A Dividend Stock To Watch Right Now (emphasis added):

CME Group is a global derivatives marketplace that offers a wide range of futures, options products, and other risk management and investment tools. [...]

As a result, the company has a huge footprint in a wide number of futures and related options, including interest rates, equities (like the S&P 500 E-mini), agriculture (like wheat, corn, and soybeans), and energy (NYMEX WTI and Henry Hub futures).

What makes CME powerful is that it has a business model that can easily be scaled . After all, it has the infrastructure in place to offer a wide variety of financial instruments. This means that it does not need to boost capital spending in order to grow .

Also, during times of distress, elevated volatility tends to be a significant tailwind for CME , as it makes money on transactions.

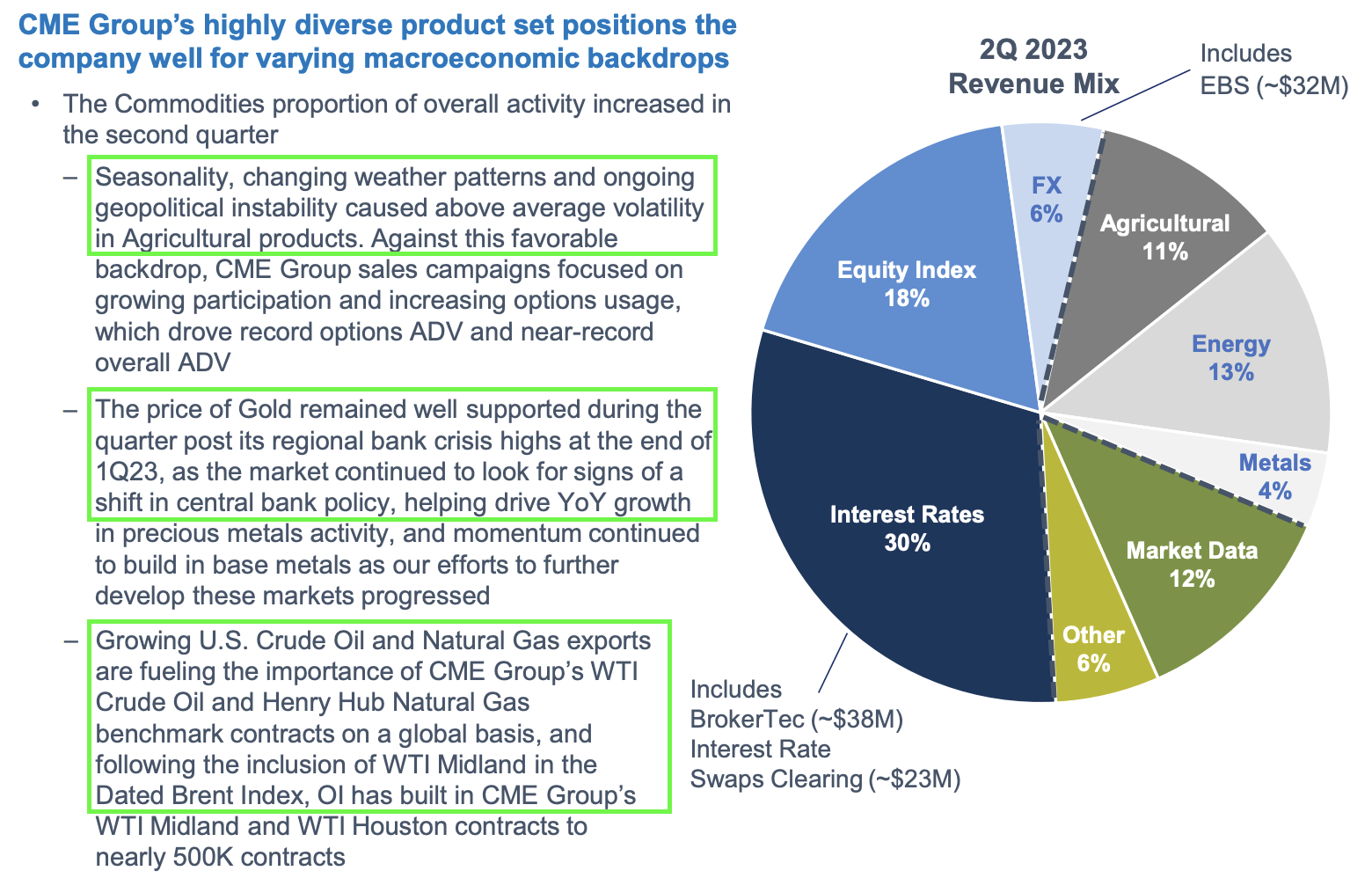

During the second quarter, the company saw outperforming growth in commodity asset classes, with agricultural products up 34%, metals up 27%, and energy up 9%. Interest rates also saw a 6% increase in average daily volume for the quarter.

Note that these asset classes account for 58% of the company's 2Q23 revenue mix. I also highlighted some of the company's comments, which explain specific volume changes.

CME Group (Author Annotations)

{kind=link}

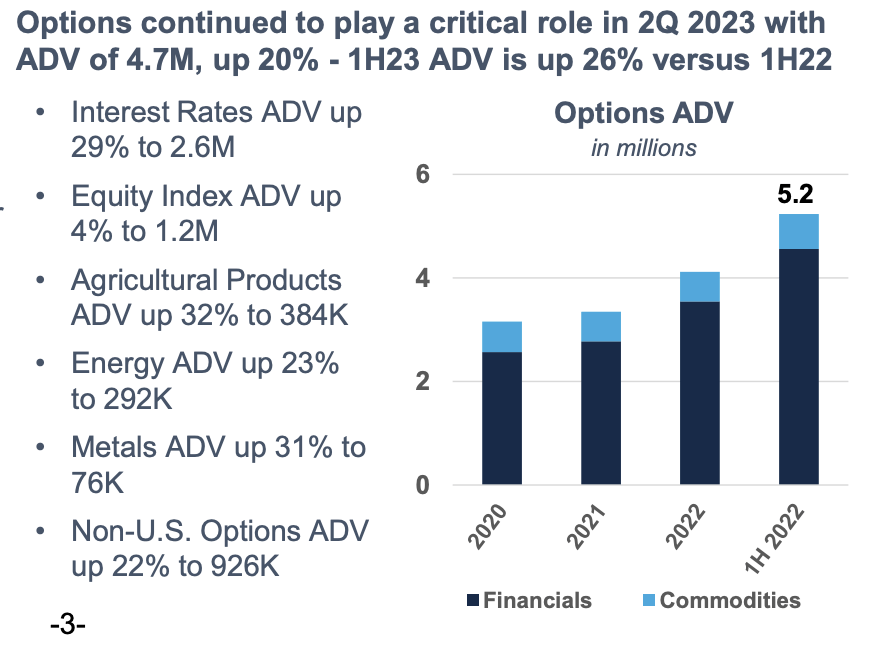

The company also witnessed strong growth in non-US markets, with an average daily volume of 6.3 million contracts in the second quarter. Options also played a crucial role in Q2, with a notable 20% growth in average daily volume to 4.7 million contracts, and agricultural options ADV reaching a record high with a 32% increase from the same quarter last year.

Furthermore, I found it quite interesting that the company highlighted that product innovation in options had driven this growth, which allowed the company to attract new participants and provide more risk management choices for clients in volatile times.

This is low-cost organic growth, which benefits both clients and shareholders.

Furthermore, the company saw huge tailwinds in its options business.

During 2Q23, equity options on futures were a strong driver of multi-year growth, with volume in same-day expiring options up 33% from last year.

Short-dated options are increasingly becoming a part of global customers' risk management and trading strategies, driving growth across all asset classes.

{kind=link}

Weekly options expirations were also in high demand, with volume up 21% year-to-date, and they are particularly popular for specific event risks, such as USDA crop reports and OPEC meetings.

Agricultural weekly options were up 168%, contributing to a record quarter for agricultural options overall. Energy and gold weekly options also saw significant growth.

I've seen similar developments in other financial companies, which note a high despite for short-term hedging tools and tools to speculate on certain short-term outcomes.

Having said that, and with regard to the aforementioned interest rate developments, the company believes that with the recent debt ceiling resolution, there's a greater hedging need in the future due to increased coupon issuance and ongoing debt financing.

On the commodities side, exports are boosting demand for risk management using CME Group's benchmark agriculture and energy products.

The company plans to accelerate growth through cross-margining opportunities for the treasury markets and ongoing product innovation and data services.

Furthermore, one of the most important developments is a higher RPC - rate per contract. Essentially, that's how much CME makes on each contract. The RPC is key, as higher volumes don't add value if the company makes less money on each contract.

According to the company:

Overall 2Q23 futures and options RPC was 72.4 cents, up from 66.4 cents in 1Q23, primarily due to a higher proportion of volume from commodity products, and reflected the first full quarter impact from the pricing changes put in place this year.

Especially in the micro equity segment, we see a steep increase in RPC.

{kind=link}

Having said all of this, I (obviously) agree with the market, which boosted CME's stock price after earnings.

Shareholder Distributions & Valuation

While CME cannot and will not even try to predict the future, they believe that the current environment for risk management is favorable, and the company aims to accelerate growth through customer expansion, new product and service innovation, and enhancing capital efficiencies.

Even better, the management team's goal is to deliver growth in the coming decade above historical averages, which would certainly help the bull case.

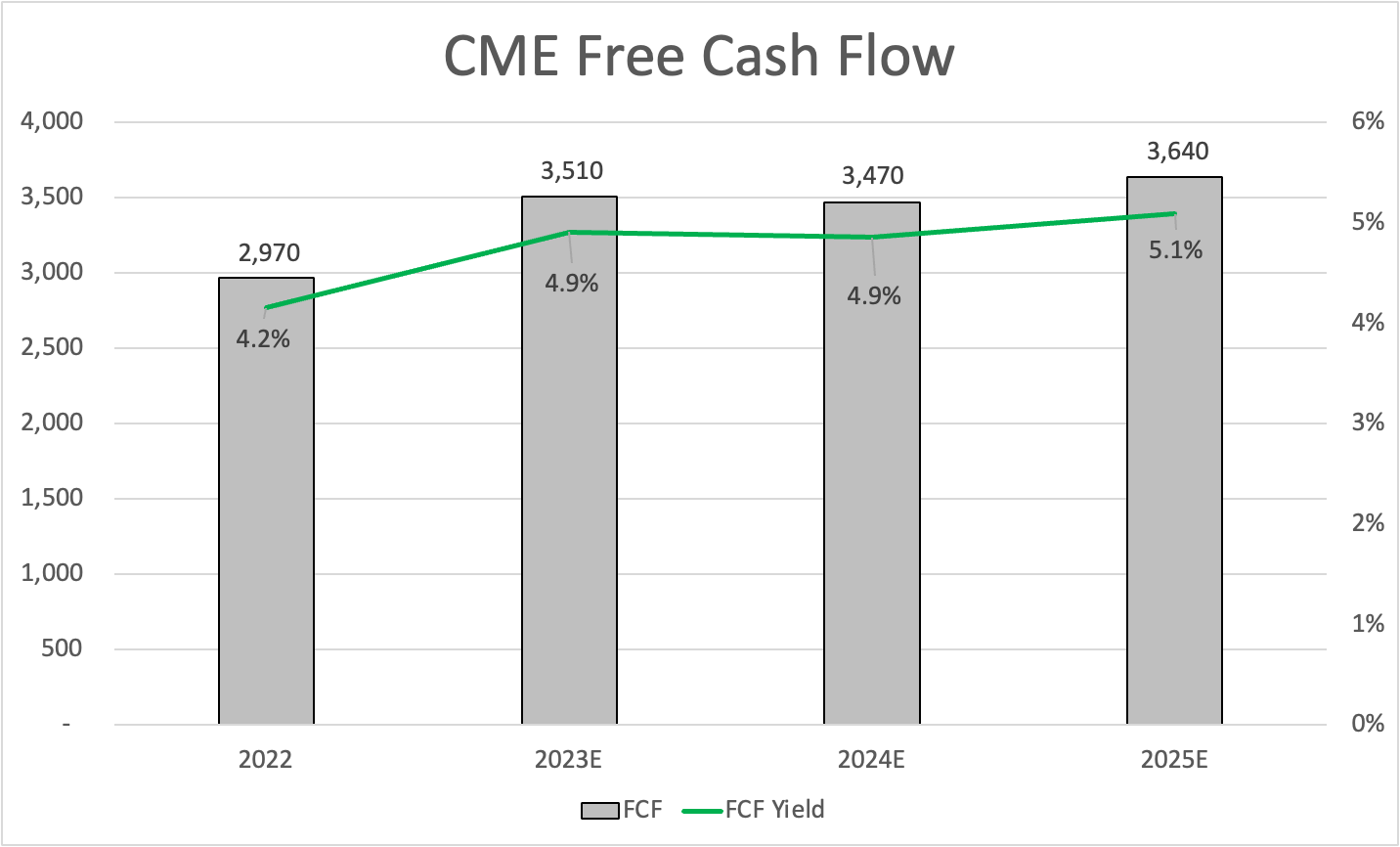

Based on that context, the company is expected to maintain steady free cash flow growth, resulting in a consistent free cash flow yield close to 5%.

{kind=link}

This indicates two things.

First of all, it means that investors remain in a good spot when it comes to dividend distributions. CME tends to distribute all of its free cash flow through consistently rising regular quarterly dividends and annual special dividends.

The current quarterly dividend yields 2.2%. This dividend has grown by 9.1% per year over the past five years.

When adding the special dividend, the yield gets a lot more juicy. Last year, the company paid $8.50 in dividends. $4.50 of this came from the special dividend, which was paid in January of this year. This translates to a 4.3% yield using the current stock price.

However, please bear in mind that there are no guarantees that this year's special dividend will be $4.50 again. It could be $4.50, lower or higher, but that depends on the remaining two quarters.

I don't expect a lower special dividend, but I just need to mention that these dividends are not guaranteed.

The second thing a high free cash flow estimate indicate is an attractive valuation.

Currently, CME is trading at 19.9x NTM EBITDA, which is a lofty valuation. However, I would make the case that we can somewhat ignore that. By that, I mean that CME needs to be valued using free cash flow. After all, the company has a >90% total payout ratio, as it simply does not require a lot of cash for investments in its business.

CME is currently trading at 20x expected free cash flow, which is a very attractive valuation. The historical median is close to 25, which would indicate a fair value 22% above the current price.

This would put the fair value at $243, which makes me one of the most bullish analysts, as the current consensus price target is $209.

While I do not believe that the company will reach this target within 12 months, I consider the company's success in boosting organic growth and its favorable long-term outlook of above-average growth as reasons to apply a higher free cash flow multiple than 20x.

After all, we're also dealing with a company that can withstand almost all headwinds we're currently dealing with, including high inflation, Federal Reserve interest rate uncertainties, and geopolitical turmoil.

I will continue to buy CME on future corrections.

Takeaway

My long-term investment in CME Group has been a rollercoaster ride, but just-released earnings show that the company is on the upswing. Despite facing challenges with lower volatility in equities, CME has managed to capitalize on increased global insecurities, benefiting from heightened volatility in key areas.

Hence, the second quarter was impressive, with strong growth in key segments like interest rates and commodities, demonstrating the scalability of CME's business model.

Moreover, the higher rate per contract is a positive sign of increased profitability.

As a shareholder, I find comfort in CME's commitment to steady dividend distributions, with a potential for attractive special dividends.

The current valuation might seem lofty, but when considering the company's high free cash flow estimate, it becomes a compelling investment opportunity.

Considering the company's resilience to various economic headwinds, including inflation and geopolitical uncertainty, I remain bullish on CME and will continue to buy on future corrections.

For further details see:

Dividend Investors Take Note - CME Group Is Back