INST - Docebo Focuses On Upmarket Approach As It Awaits Improved Macro Environment

2023-10-17 16:35:28 ET

Summary

- Docebo Inc. sells online learning technologies with AI-enhanced functions for improved learning results.

- The global e-learning services market is expected to exceed $1 trillion by 2032, driven by technological innovation and increased demand due to the COVID-19 pandemic.

- Docebo's financial trends show continued revenue growth, but operating income has worsened, and earnings per share have turned negative.

- I remain Neutral [Hold] on Docebo Inc. shares for the near term.

A Quick Take On Docebo

Docebo Inc. ( DCBO ) sells online learning technologies coupled with AI-enhanced functions to improve learning results.

I previously wrote about Docebo with a Neutral Hold outlook.

Management is positioning the company to benefit from a return to macroeconomic growth, but I’m cautious as to when that will occur in any meaningful way due to growing negative geopolitical risks.

I remain Neutral [Hold] on Docebo Inc. in the near term.

Docebo Overview And Market

Canada-based Docebo Inc. was founded to develop an integrated learning management system [LMS] for organizations to provide internal and external training capabilities.

The firm is led by founder and Chief Executive Officer Claudio Erba, who was previously project leader at MHP Srl and product manager at Selpress.

The company’s main capabilities include:

-

Learn LMS

-

Impact Measurement

-

Analytics

-

Shape

-

Content

-

Flow

-

Instructure.

The company seeks new customers via its direct sales and marketing efforts, through inbound and outside sales teams.

Docebo’s average contract value was approximately $48,100 as of June 30, 2023.

According to a 2023 market research report by Global Market Insights, the global market for e-learning services was an estimated $339 billion in 2022 and is expected to exceed $1 trillion in value by the end of 2032.

This represents a forecast CAGR (Compound Annual Growth Rate) of 14.0% from 2023 to 2032.

The primary drivers for this expected growth are ongoing technological innovation and growing Internet penetration worldwide.

Also, the COVID-19 pandemic has brought forward demand from many users to pursue their education in an online environment, increasing the industry's growth prospects in the years ahead.

Below is a graphic with various characteristics of the market through 2032:

{kind=link}

Major competitive or other industry participants include:

-

Instructure

-

Absorb LMS

-

SAP SuccessFactors Learning

-

Saba Cloud

-

Tovuti LMS

-

Cornerstone Learning

-

Captivate Prime

-

360Learning

-

SumTotal Learning.

Docebo’s Recent Financial Trends

Total revenue by quarter has continued to grow; Operating income by quarter has worsened in the most recent quarter.

Seeking Alpha

Gross profit margin by quarter has trended slightly higher recently; Selling and G&A expenses as a percentage of total revenue by quarter have been reduced in recent quarters.

Seeking Alpha

Earnings per share (Diluted) have been volatile and have turned negative in the most recent quarter:

Seeking Alpha

(All data in the above charts is GAAP.)

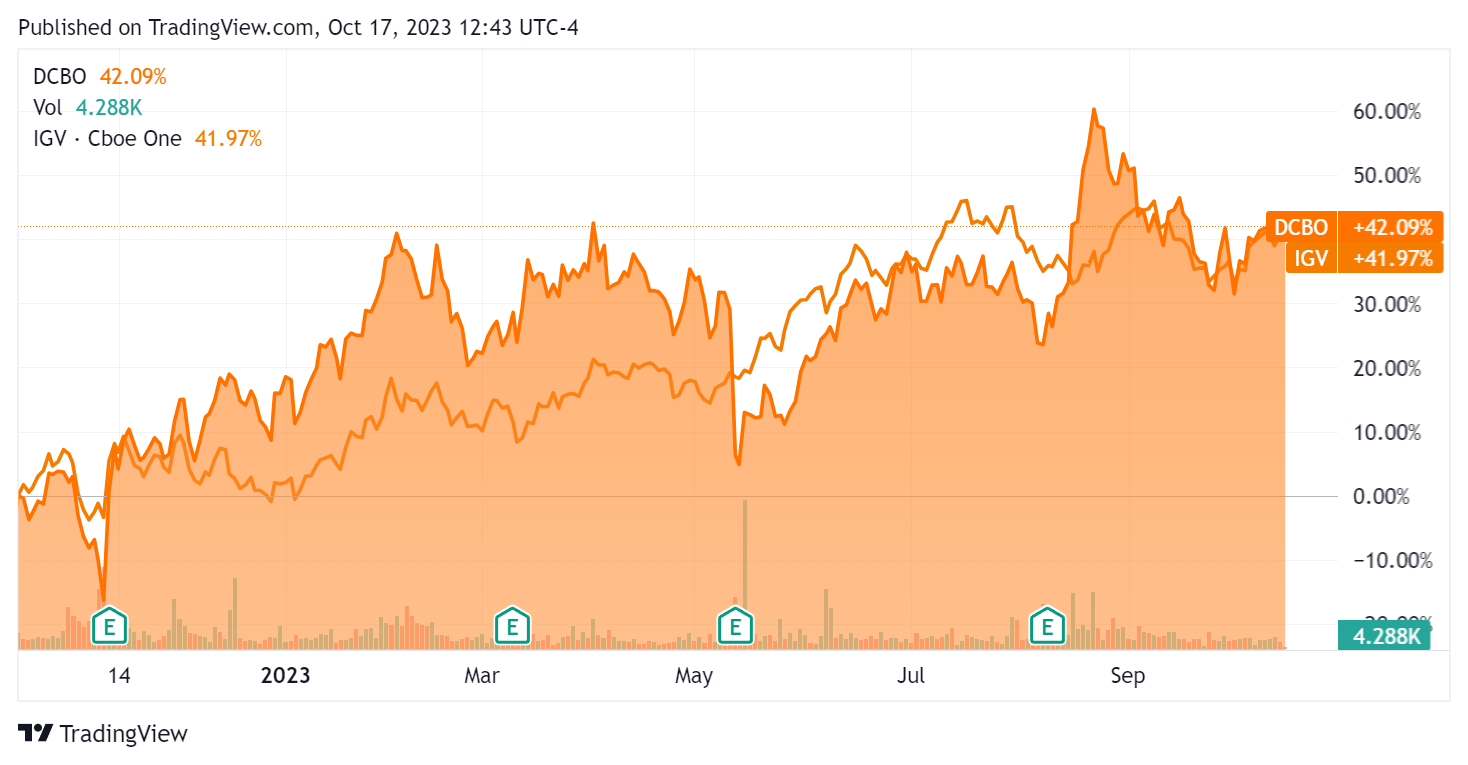

In the past 12 months, DCBO’s stock price has risen 42.09% vs. that of the iShares Expanded Tech-Software Sector ETF’s ( IGV ) rise of 41.97%:

{kind=link}

For balance sheet results, the firm ended the quarter with $203.9 million in cash and equivalents and no debt.

Over the trailing twelve months, free cash flow was only $5.6 million, during which capital expenditures were $0.8 million. The company paid $4.7 million in stock-based compensation in the last four quarters.

Valuation And Other Metrics For Docebo

Below is a table of relevant capitalization and valuation figures for the company:

| Measure [TTM] |

| Amount |

| Enterprise Value / Sales |

| 6.9 |

| Enterprise Value / EBITDA |

| NM |

| Price / Sales |

| 8.4 |

| Revenue Growth Rate |

| 30.0% |

| Net Income Margin |

| 4.6% |

| EBITDA % |

| -2.0% |

| Market Capitalization |

| $1,300,000,000 |

| Enterprise Value |

| $1,100,000,000 |

| Operating Cash Flow |

| $6,440,000 |

| Earnings Per Share (Fully Diluted) |

| $0.21 |

| Free Cash Flow Per Share |

| $0.17 |

| SA Quant Score |

| Hold - 3.38 |

(Source - Seeking Alpha.)

As a reference, a relevant partial public comparable would be Instructure Holdings, Inc. (INST):

| Metric [TTM] |

| Instructure |

| Docebo |

| Variance |

| Enterprise Value / Sales |

| 8.1 |

| 6.9 |

| -15.4% |

| Enterprise Value / EBITDA |

| 27.4 |

| NM |

| --% |

| Revenue Growth Rate |

| 13.7% |

| 30.0% |

| 118.2% |

| Net Income Margin |

| -7.6% |

| 4.6% |

| --% |

| Operating Cash Flow |

| $142,050,000 |

| $6,440,000 |

| -95.5% |

(Source - Seeking Alpha.)

DCBO’s most recent unadjusted Rule of 40 calculation was 27.9% as of Q2 2023’s results, so the firm’s results have dropped and are in need of improvement in this regard, per the table below:

| Rule of 40 Performance (Unadjusted) |

| Q1 2023 |

| Q2 2023 |

| Revenue Growth % |

| 33.0% |

| 30.0% |

| EBITDA % |

| -1.7% |

| -2.0% |

| Total |

| 31.3% |

| 27.9% |

(Source - Seeking Alpha.)

Sentiment Analysis

The chart below shows the frequency of various keywords from the firm’s most recent earnings conference call with analysts.

Seeking Alpha

The chart indicates that the firm and its clients are facing macroeconomic headwinds and ongoing challenges in the current environment.

Analysts asked leadership about enterprise sales cycles, generative AI uses and positioning for future growth.

Management responded by saying that the firm is moving upmarket and larger enterprises want more sophisticated solutions for internal and external requirements.

AI solutions are solving problems like multilingual content generation and automation of repetitive tasks.

Leadership said it is strategically positioning the company to benefit from a return to a macro growth environment, and they are improving their ability to navigate large enterprise purchasing processes.

Commentary On Docebo

In its last earnings call (Source - Seeking Alpha ), covering Q2 2023’s results, management’s prepared remarks highlighted exceeding its previous revenue and adjusted EBITDA guidance ranges.

The firm is seeing "signs of stabilization" for spending within the enterprise segment, although the SMB segment continues to be cautious with its spending decision-making.

By region, Europe has produced no spending gain while the U.S. is "beginning to pick up."

Management intends to leverage the generative AI services of a large, unnamed company to "transform the delivery of personalized learning at scale and integrate cutting-edge features and functionalities into the Docebo learning platform."

Total revenue for Q2 2023 rose by 24.9% year-over-year while gross profit margin increased by 0.5%.

The firm’s gross retention rate was flat sequentially.

Selling and G&A expenses as a percentage of revenue fell by 1.6% YoY, a positive signal, but operating losses worsened by 18.5% to ($3.2 million).

The company's financial position is solid, with ample liquidity, no debt and small positive free cash flow generation.

DCBO’s Rule of 40 performance has been middling and in need of improvement.

Looking ahead, full-year 2023 top line revenue growth is expected to be around 25.4% over 2022.

If achieved, this would represent a drop in revenue growth rate versus 2022’s growth rate of 37.3% over 2021.

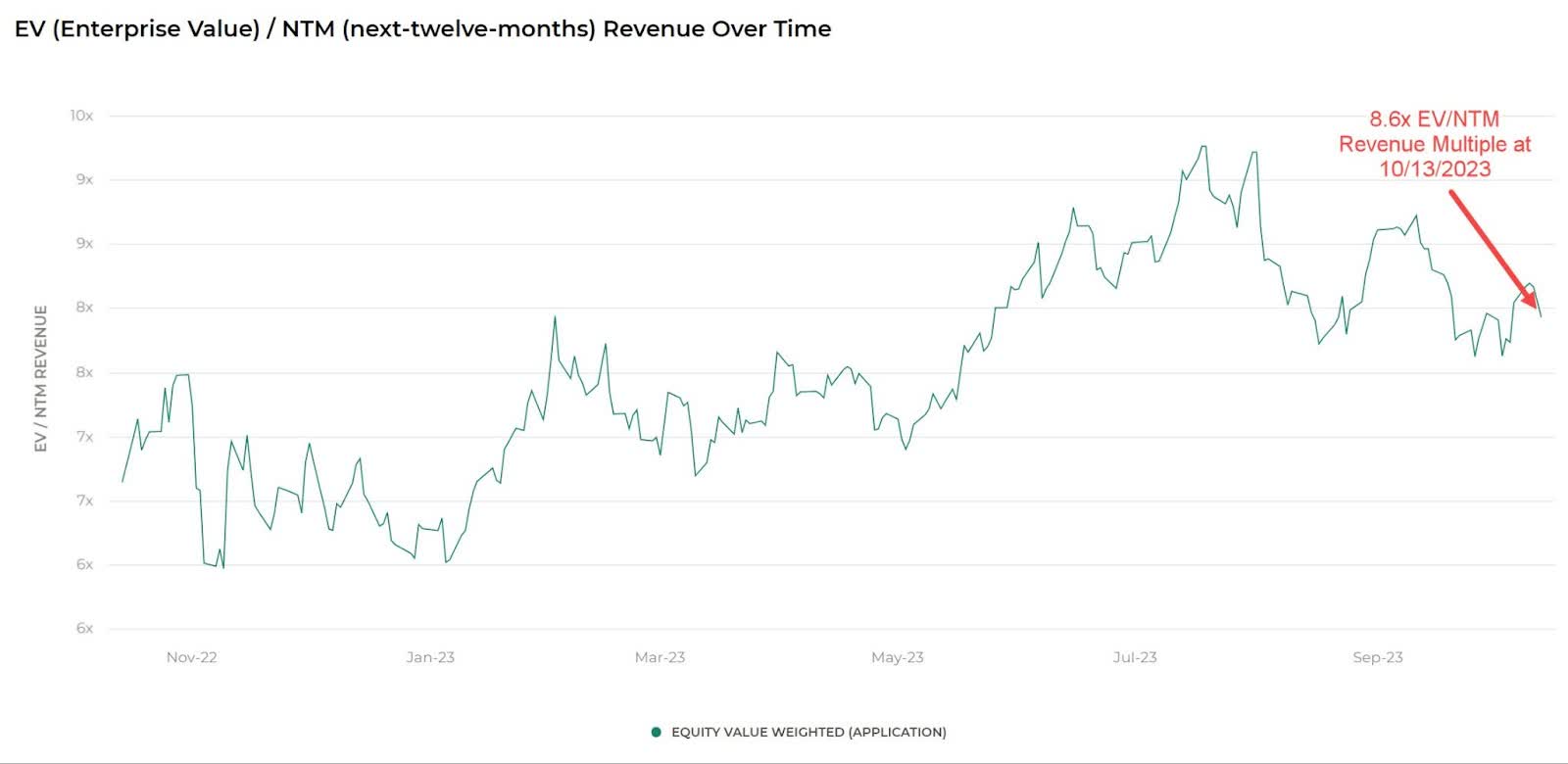

Regarding valuation, the market is valuing DCBO at an EV/Sales multiple of around 6.9x on TTM revenue growth rate of 30% against a median Meritech SaaS Index implied ARR growth rate of around 19% ( Source ).

The Meritech Capital Index of publicly held SaaS application software companies showed an average forward EV/Revenue multiple of around 8.6x on October 13, 2023, as the chart shows here:

{kind=link}

So, by comparison, DCBO is currently valued by the market at a discount to the broader Meritech Capital SaaS Index, at least as of October 13, 2023, despite a faster revenue growth rate.

Risks to the company’s outlook include an extended macroeconomic slowdown, reduced credit availability, which may affect customer/prospect spending plans and lengthening sales cycles, which may reduce its revenue growth potential in the near term.

In sum, Docebo is expecting a lower revenue growth rate in 2023 amid a continuing focus on moving upmarket to larger enterprise deals, which may be slow to materialize in the currently uncertain macroeconomic environment.

The stock appears reasonably valued at its current level, but given the prospect for slow macroeconomic growth, increasingly negative geopolitical developments and the firm’s focus on slower and larger enterprise and government deals, I’m still cautious about DCBO.

I remain Neutral [Hold] on DCBO for the near term.

For further details see:

Docebo Focuses On Upmarket Approach As It Awaits Improved Macro Environment