META - DocuSign: Growth Stalls Temporarily And Buyout Rumor Fades

2024-01-06 09:00:00 ET

Summary

- DOCU's top-line growth continues to decelerate at a time of elongated sales cycle and intensified market competition.

- Then again, the e-signature company continues to grow its consumer base and backlog over the next few quarters, with its profitability still impressive.

- DOCU also expands its partnerships while improving its offerings across e-signature and agreement management capabilities, with the latter likely to be a growth driver.

- Combined with its discounted valuations, we believe that the stock remains a compelling Buy for value oriented investors.

We previously covered DocuSign, Inc. (DOCU) in October 2023, discussing the stock's oversold status, attributed to its decelerating growth and uncertain macroeconomic outlook.

We had viewed this phenomenon as a positive Buy sign, since it remained highly profitable with its market leading offerings still sticky globally.

In this article, we shall address the unlikely buyout rumor with the recent lifting market sentiments already triggering the DOCU stock's overly rapid recovery, with the potential volatility offering interested investors with a minimal margin of safety.

While we continue to rate the stock as a Buy, attributed to its speculative turnaround story, investors may want to patiently wait for a moderate pullback for an improved upside potential.

DOCU's Investment Thesis Remains Robust After A Moderate Pullback

For now, DOCU has reported double beat FQ3'24 earnings, with revenues of $700.42M ( +1.8% QoQ / +8.5% YoY ) and adj EPS of $0.79 (+9.7% QoQ/ +38.5% YoY).

The accelerating bottom line is promising indeed, despite the notable deceleration observed in its top-line thus far, compared to FQ3'23 revenue growth rate of +3.7% QoQ/ +18.3% YoY and FQ2'22 rate of +6.5% QoQ/ +42.4% YoY.

While we understand that DOCU's growth rate largely hinges on the normalizing remote work trend, it is apparent that its subscription growth has been moderated to $682.4M (+1.9% QoQ/ +9.3% YoY) and remaining performance obligations to $2B ( +5.2% QoQ / +17.6% YoY ) by the latest quarter.

Dollar Net Retention [DNR] has also declined to 100% ( -2 points QoQ / -8 YoY ) and Consumer Base Growth decelerated to 1.47M (+0.03 QoQ/ +0.15M YoY), attributed to its lack of moat at a time of elongated sales cycle.

Readers must also note that the management has warned of " continued DNR pressure in Q4 ," implying that its contract wins/ renewals may be underwhelming ahead.

Then again, it is not all gloom and doom, since DOCU has balanced this headwind with robust adj gross margins of 83% (+1 points QoQ/ inline YoY) and stable adj operating expenses of $378.4M (-1% QoQ/ +1.5% YoY) in FQ3'24, after adjusting for stock-based compensations.

Eagle-eyed readers may also note that the company has been reducing its headcounts to 6.94K staffs (+197 QoQ/ -577 YoY), partly contributing to its improved Free Cash Flow profitability of $240.34M (+30.8% QoQ/ +566.5% YoY).

This implies its ability to sustain its operations, no matter the impacted growth prospects.

We are also quietly confident that the DOCU management may be able to revive the impacted growth prospects, with it already being the exclusive e-signature provider for Microsoft's ( MSFT ) Power Page Integration.

This is on top of the new WhatsApp ( META ) integration for e-signatures, with the social media platform used by over 2.7B people globally as of January 2024.

The DOCU management has also attempted to diversify its offerings beyond e-signature and into agreement management, with consumers able to seamlessly generate contracts with the aid of Generative AI solutions.

Interested readers may want to tune in to the upcoming Momentum User Conference in April 2024, since its future agreement management products may eventually be an excellent growth driver.

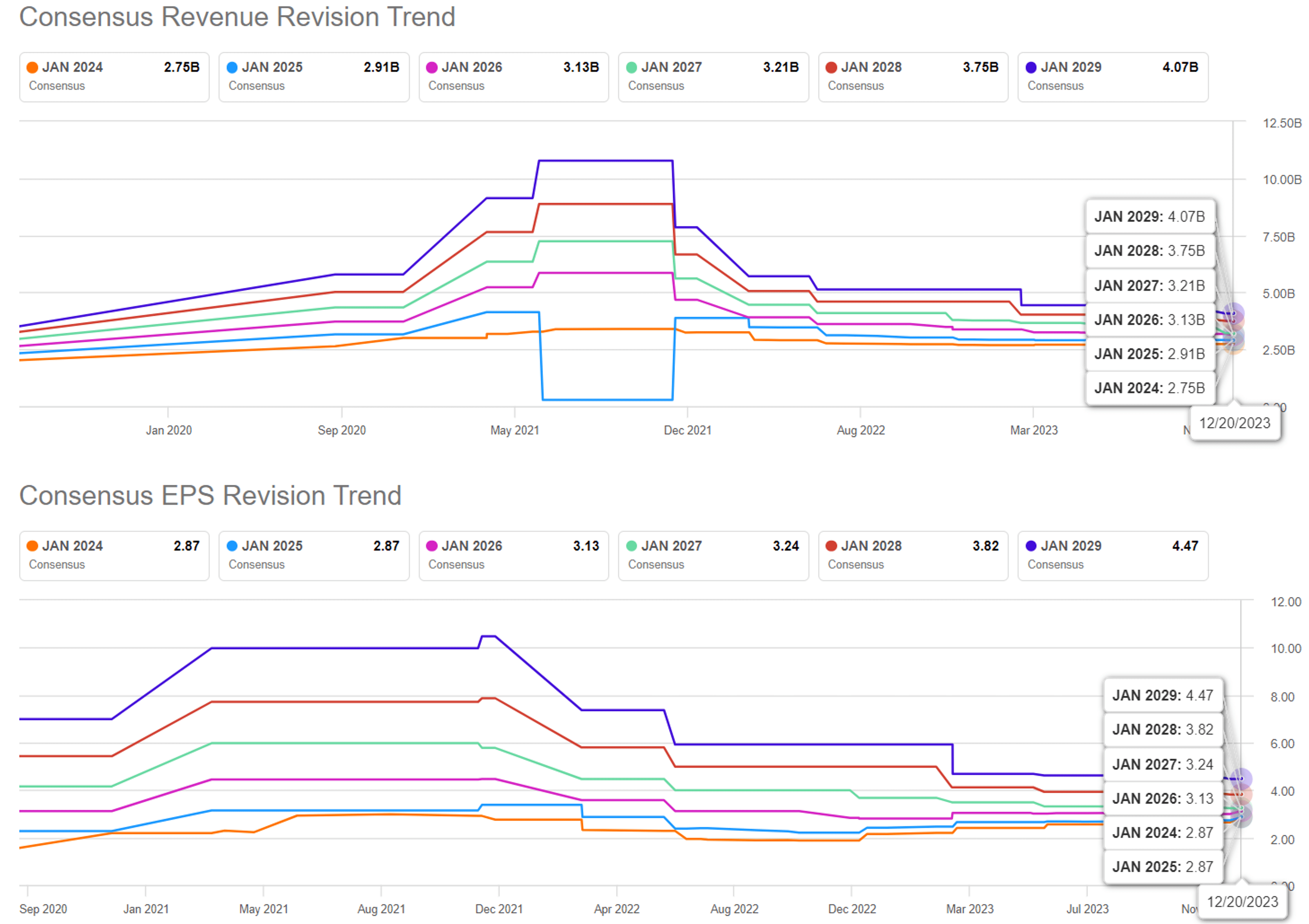

The Consensus Forward Estimates

{kind=link}

On the one hand, DOCU's forward estimates have been raised recently, with the company expected to generate a top/ bottom line expansion at a CAGR of +7.5%/ +15.5% through FY2026.

This is compared to the previous estimates of +10.4%/ +12.3%, though still lagging behind its historical growth at a CAGR of +44.3%/ +180.2% between FY2020 and FY2023, respectively.

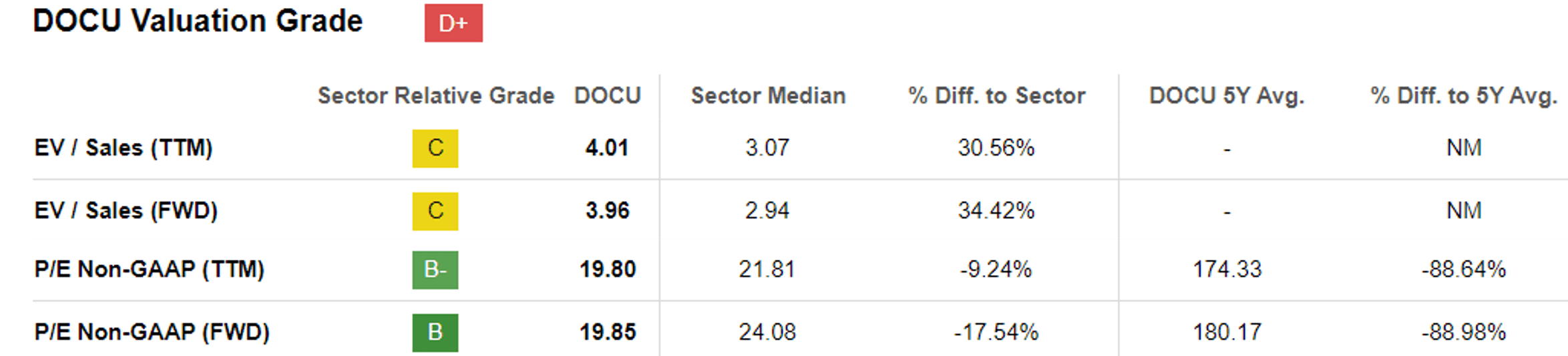

DOCU Valuations

{kind=link}

On the other hand, DOCU's FWD P/E valuation of 19.85x appears to be discounted, compared to its 1Y mean of 21.66x and sector median of 24.08x, implying Mr. Market's pessimism about its ability to return to its hyper-pandemic profitable growth rate.

Anyone following the buyout story may also want to keep their ears on the ground, with the recent rally already propelling DOCU to a Market Capitalization of $11.22B, up from $7.86B in the October 2023 bottom though still normalized from the $60.99B recorded in September 2021.

With the company already expensive at current levels, it remains to be seen if the deal may proceed, especially when borrowing costs are still elevated with the Fed yet to pivot.

While DOCU's balance sheet is highly commendable with effectively zero debt and growing cash hoard of $1.59B (+10.4% QoQ/ +63% YoY), it is uncertain what premium the company may command due to its decelerating top-line trend.

If any, we do not expect a consolidation deal to occur, based on the example we have observed with Adobe's (ADBE) failed acquisition of Figma, since "there is no clear path to receive necessary regulatory approvals from the European Commission and the UK Competition and Markets Authority."

As a result, readers may also want to temper their near-term expectations, with the buyout deal likely being a rumor at best, as many insiders cashed out their positions at the recent peak.

So, Is DOCU Stock A Buy , Sell, or Hold?

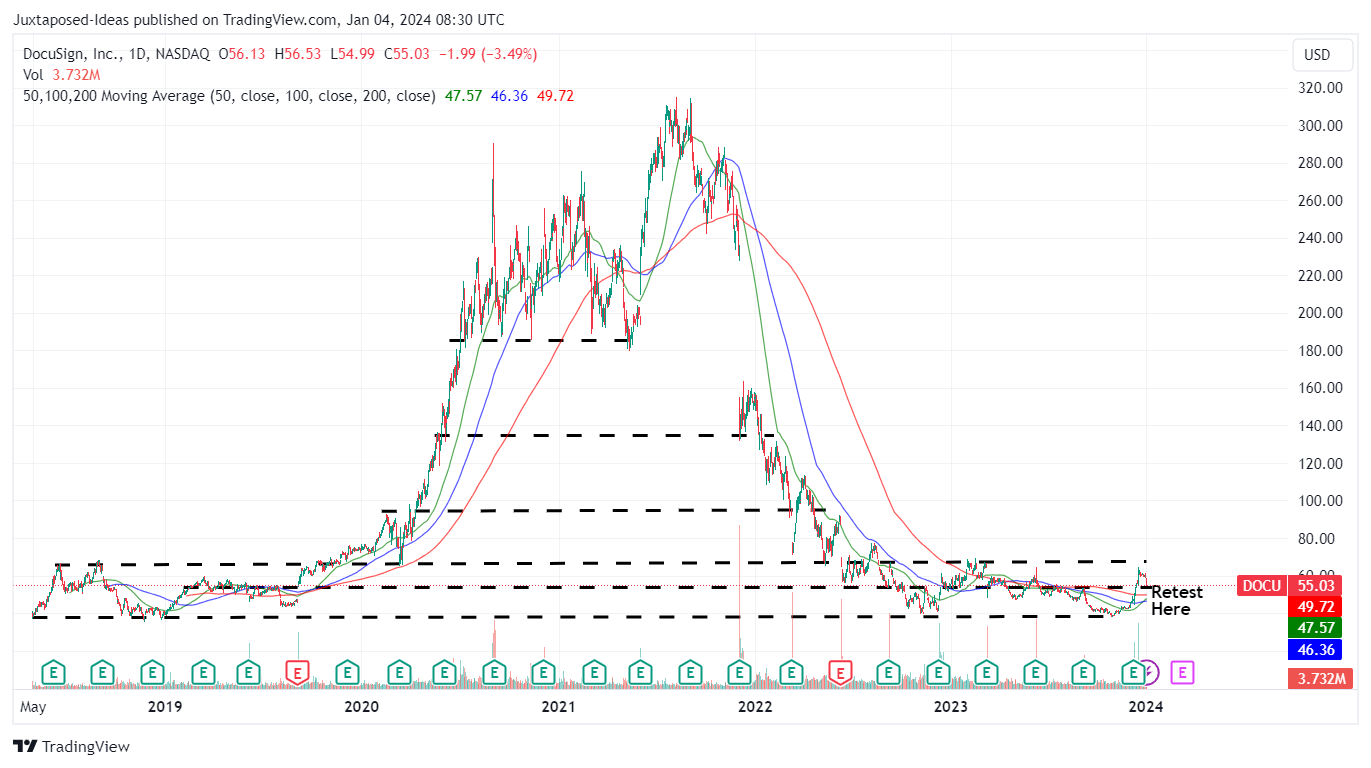

DOCU 5Y Stock Price

{kind=link}

For now, it is apparent that while the lifting market sentiments surrounding the cooling inflation and Fed's speculative pivot by Q1'24 have drastically boosted DOCU by +54.4% since the October 2023 bottom, the stock is not able to retain its gains as well.

We believe that the stock is likely to retrace to its previous support levels of $48s in the near term, implying a -12.7% downside from current levels, as traders take their gains at the recent December 2023 peak.

While DOCU appears to be trading near its fair value, we prefer to rate the stock as a value buy only after a moderate pullback for an improved margin of safety.

Assuming that it remains a standalone company ahead, the $48s will also offer an expanded upside potential of +29.3% to our long-term price target of $62.10, based on the estimated FY2026 adj EPS of $3.13 and its FWD P/E of 19.85x.

Patience for now.

For further details see:

DocuSign: Growth Stalls Temporarily And Buyout Rumor Fades