NOW - DocuSign: Risk Reward Remains Skewed To The Downside

2023-05-01 17:54:44 ET

Summary

- Future growth for DocuSign relies on expanding its customer base and promoting its broader suite of Agreement Cloud products.

- DocuSign may experience a slowdown in short-term billing and revenue growth as it seeks to establish a sustainable growth trajectory post-pandemic.

- The company faces challenges, including leadership changes, a sales reorganization, and the need to navigate a changing business environment.

- I believe the risk/reward ratio at this point is tilted toward the downside, and hence keep a sell rating on the stock.

Thesis

DocuSign, Inc. ( DOCU ) is a leading software company in the contract-lifecycle management market, known for its leading eSignature solution that has revolutionized the industry. The company experienced a surge in growth during the pandemic as businesses rapidly transitioned to electronic signatures and contracts. However, as the pandemic-related tailwinds subside and near-term growth slows, DocuSign's future growth depends on expanding its existing customer base and promoting its broader suite of Agreement Cloud products. Although DocuSign operates in a vast total addressable market ((TAM)) estimated at over $50 billion, its short-term billing and revenue growth may decelerate as it grapples with establishing a sustainable growth trajectory in a post-pandemic landscape. I believe the risk/reward ratio at this point is tilted toward the downside, and hence keep a sell rating on the stock.

DOCU stock price movement (Seeking Alpha)

Several Reasons To Be Bearish

After providing a preliminary FY24 outlook during its earnings call that investors likely viewed as conservative and setting an achievable growth bar, DocuSign provided full-year guidance that falls a bit short on the top line and PF operating margin guidance that does not seem to allow for much of the recent headcount reductions to flow through. I continue to respect the company's logical and responsible steps to recalibrate the business, but the combination of deteriorating demand trends, clear competitive presence of Adobe (ADBE), and the likelihood of emerging competition from Microsoft (MSFT), CFO departure, exposure to challenged end-markets in real estate and VC-based fundraising spaces, and downside comps that trade at materially lower multiples seem to tilt the risk/reward profile downward.

The core eSignature business of DocuSign, which represents over 90% of the company's revenue, is facing a challenging competitive environment. The growing perception of basic electronic signatures as commoditized tools for relatively simple use cases has made customers less responsive to premium offerings, which is why customers could be looking to switch to Adobe due to more favorable pricing. With DocuSign's core business facing pressure and its potential growth areas like Contract Lifecycle Management still in the early stages, it is unlikely to see a meaningful acceleration of growth in the near to medium term that would support a high free cash flow multiple in the 20s.

DocuSign has acknowledged a more challenging macro environment, stating that it has not improved and might have even worsened. This aligns with expectations of a moderation in growth for the broader eSignature market compared to the elevated levels during the pandemic. Specific verticals, such as VC-based fundraising and real estate, which heavily rely on document workflows, are experiencing pockets of softness due to the macro impact. DocuSign's business reflects these challenges through a decline in dollar net retention and an increase in the number of customers with an annual contract value ((ACV)) greater than $300,000, albeit at a slower pace.

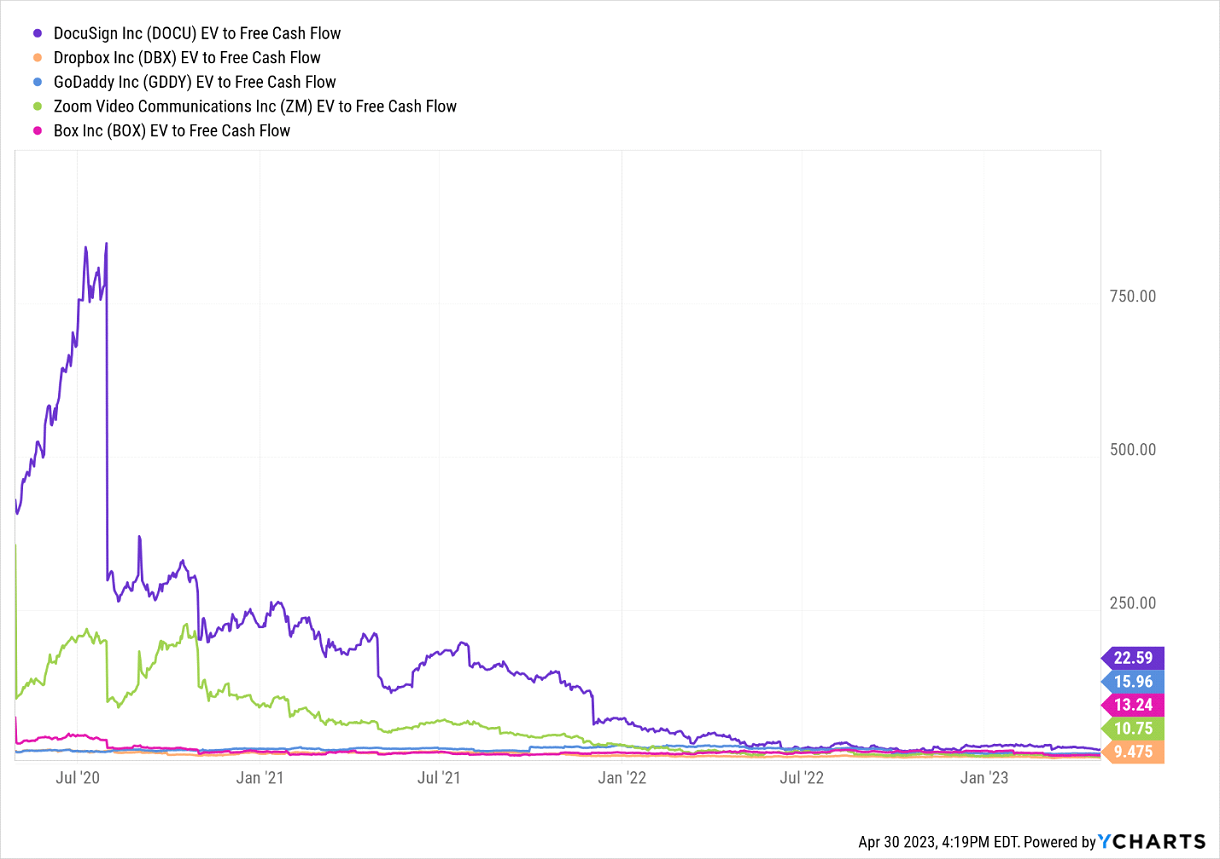

Considering the current valuation levels, there are downside risks for DocuSign. Comparable companies trade at lower cash flow multiples for the calendar year 2023 while offering similar resilience in their top lines or superior free cash flow profiles. Some examples include Dropbox, Inc. ( DBX ), GoDaddy Inc. ( GDDY ), Zoom Video Communications, Inc. ( ZM ), Box, Inc. ( BOX ), among others. Additionally, there are durable compounders that trade at lower growth-adjusted multiples, such as Salesforce, Inc. ( CRM ), HubSpot, Inc. ( HUBS ), ServiceNow, Inc. ( NOW ), ZoomInfo Technologies Inc. ( ZI ), and others. Overall, the risk/reward setup for DocuSign shares is perceived as unfavorable in the near term, as the company needs time to demonstrate the effectiveness of its investments and regain investor confidence.

{kind=link}

Weak Economic Activity Leads to Lower Billings

DocuSign's billings growth could slow to low- to mid-single digits in 2023 after averaging 15% in the past two quarters, stemming from lower economic activity. Given that DocuSign's product is priced on usage (or activity), any drop in the pace of transactions hurts sales growth. Elongation of sales cycles is another factor that could hurt new-business signings. DocuSign's billings growth spiked during the pandemic as enterprises rushed to embrace digital-signature capabilities. This led to a considerable pull-forward in demand for its products.

DocuSign could experience a steady decline in its net dollar retention rate over the next year, which is a key driver of billings and sales growth. This metric is a good indicator of client retention and expansion and spiked from a historical average of 114-119% to around 125% during the pandemic. In the past two quarters, it has averaged 109%, but I expect it to fall even more, to about 105%, over the next four quarters. As macroeconomic conditions improve, the rate could rebound to 110- 115%, most likely in fiscal 2025.

Company's Presentation

Risks

DocuSign's growth in customers with high annual contract values has slowed down as it faces tough comparisons and undergoes a sales reorganization. However, there is potential for a reacceleration in large customer additions if the company executes well on demand generation post-pandemic and effectively upsells its core eSignature offering by expanding into wider use cases and improving penetration of new products. This could lead to increased sales diversification, reducing reliance on the cyclicality of small business spending patterns.

Furthermore, DocuSign aims to achieve greater revenue diversification by expanding its suite of contract-lifecycle management offerings. This broader platform approach could enhance customer retention and increase average revenue per user. The company estimates that its Agreement Cloud, which encompasses eSignature, CLM, insight, document generation, and platform solutions, has a total addressable market of over $50 billion. The breakdown includes approximately $26 billion attributed to eSignature, $4 billion to broader signing offerings, $17 billion to the broader Agreement Cloud, and $3 billion to Platform solutions.

Final Thoughts

DocuSign is a leading application software company that has dominated the contract-lifecycle management market, primarily driven by its eSignature offering, which holds the biggest market share. However, as the pandemic-induced tailwinds subside, DocuSign's future growth relies on successfully upselling its existing customer base and expanding the adoption of its broader suite of Agreement Cloud products. While DocuSign is still in the early stages of tapping into its vast $50 billion total addressable market, its short-term billings and revenue growth may face challenges as it seeks to establish a sustainable growth trajectory in a post-pandemic environment. DocuSign's core eSignature business, which accounts for over 90% of its revenue, is facing a challenging competitive landscape. The market for electronic signatures is becoming commoditized, with customers showing less responsiveness to premium offerings. As a result, customers are increasingly considering switching to Adobe for more favorable pricing. I believe the risk/reward ratio at this point is tilted toward the downside, and hence keep a sell rating on the stock.

For further details see:

DocuSign: Risk Reward Remains Skewed To The Downside