DASH - DoorDash: The Real Potential Of On-Demand Platforms Beyond Inflation Worries

2023-04-17 14:16:57 ET

Summary

- We believe anxiety over inflation is leading investors to overlook opportunities.

- The market fails to see the potential of domestic and international online grocery markets.

- DoorDash offers the same potential as Uber but it is trading at a discount to Uber.

Investment Thesis

If investors only worry about inflation, they can't see the forest for the trees. If investors concentrate solely on Uber's impressive quarterly growth numbers, they may overlook the fact that DoorDash, Inc. ( DASH ) has the same potential.

The company was able to manage costs to grow in this challenging environment. Its business model is responsive and adaptable.

We think the market has not fully priced in the huge potential of domestic and international grocery markets, and so this growth stock looks really cheap.

Moreover, we believe that DoorDash's stock is currently priced at a significant discount compared to Uber's (UBER) considering its potential. As a result, we rate DoorDash as a "Strong Buy".

Company Profile

DoorDash is a food delivery platform that connects customers with local restaurants and independent delivery drivers. Founded in 2013, DoorDash operates in over 4,000 cities across the United States, Canada, and Australia. As of December 31, 2022, the company had over 16,800 employees worldwide.

Growth Drivers

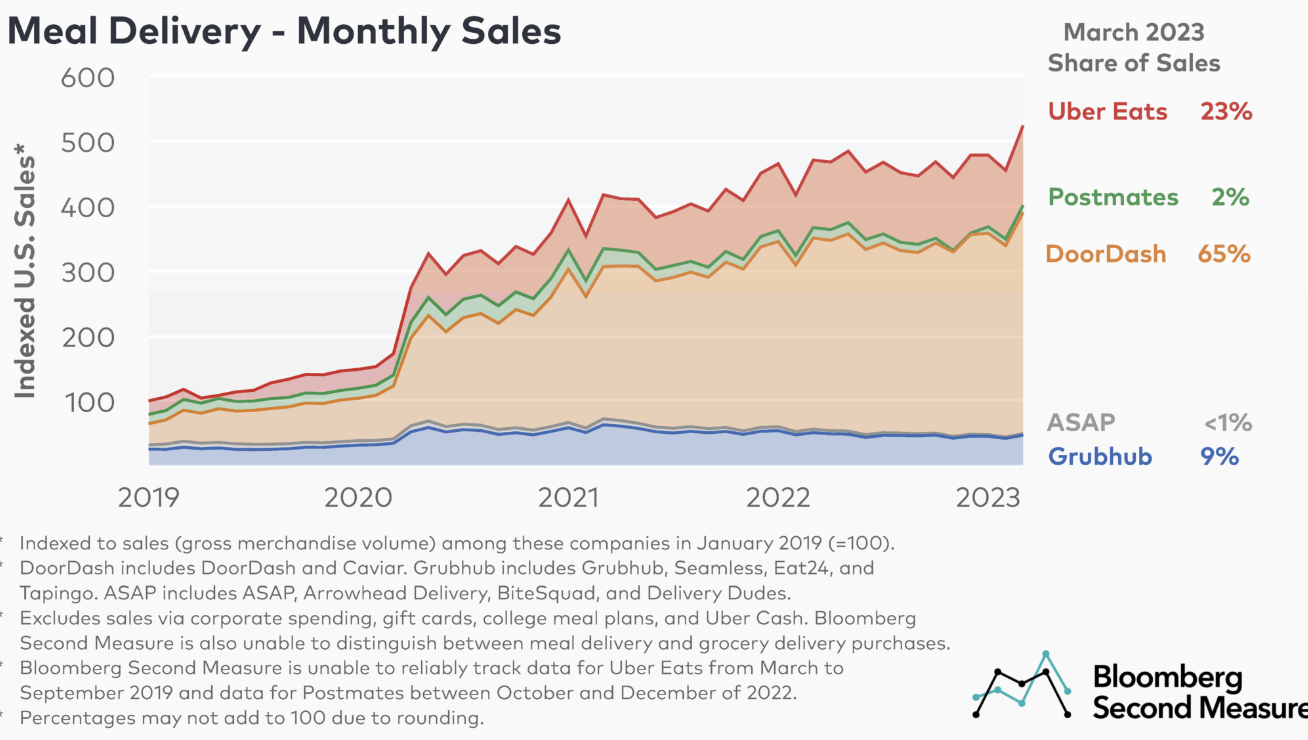

DoorDash started with a niche focus on meal-delivery services. Though Uber launched UberEats in 2014, DoorDash was able to maintain its first-mover advantage and continued to have a dominate position in U.S. meal delivery service.

Meal Delivery - Monthly Sales (Bloomberg)

{kind=link}

DoorDash

-

U.S. On-Demand Grocery Delivery Business

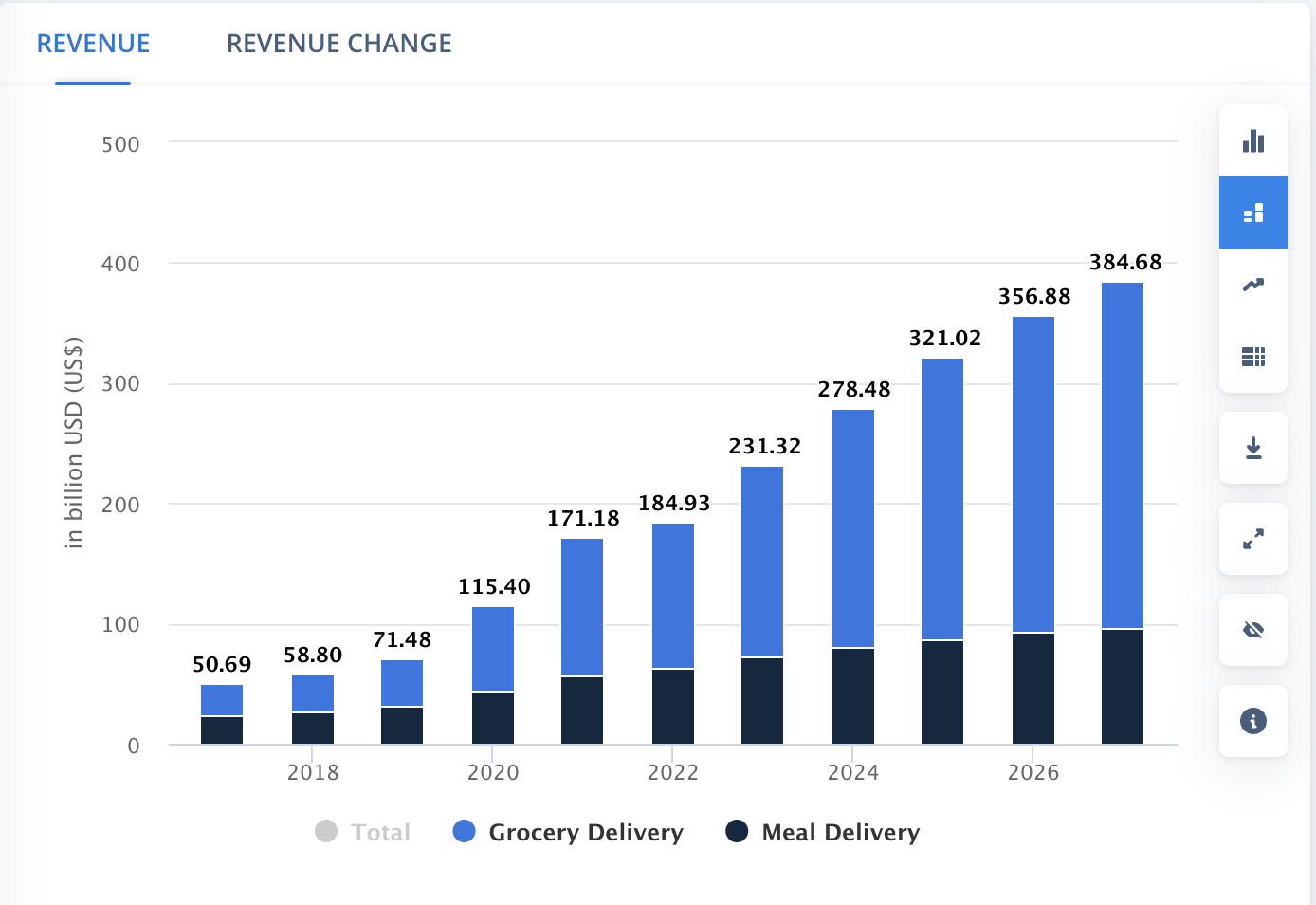

DoorDash started to expand into the grocery delivery business in 2020. Grocery delivery is a much larger market than meal delivery. According to Statista , Revenue in the online food delivery market is projected to reach US$231.30 billion in 2023. The grocery delivery segment is expected to grow by 24.2% in 2024.

{kind=link}

-

International Expansion

DoorDash also entered the international market, primarily in Europe and Asia through the acquisition of Wolt in 2022. According to Statista , online food delivery in Europe is also a large and growing market. Revenue in the Europe online food delivery market is projected to reach US$113.70 billion in 2023. The market's largest segment is grocery delivery with a projected market of $73.16 billion in 2023.

Recent trends in the industry

-

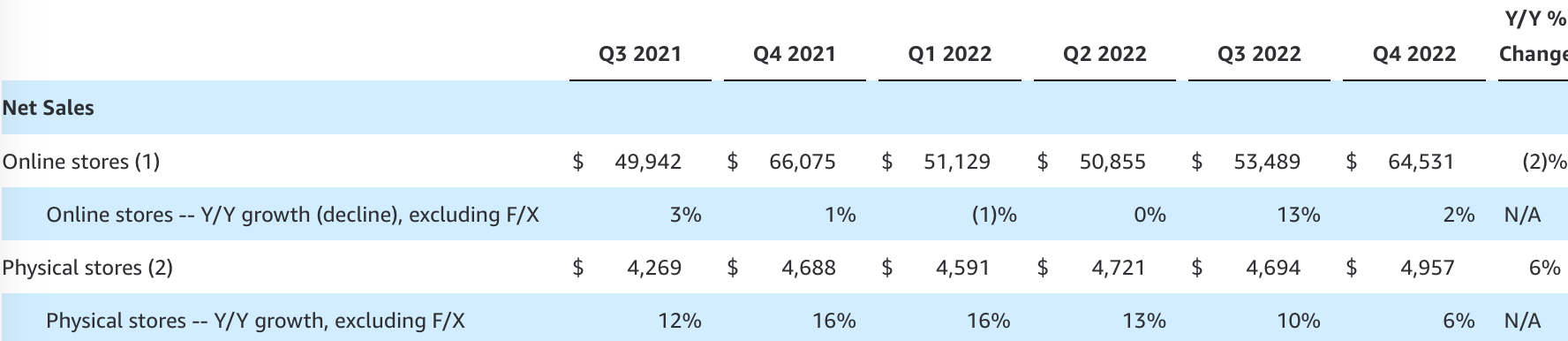

On-Demand Grocery Delivery Platforms Gained Market Share Over Amazon

On-demand grocery delivery platforms seem to have a competitive advantage over Amazon with high-value consumers who prioritize speedy delivery and are less concerned with delivery costs. Uber and DoorDash grew their delivery business by 30% and 35% in 2022, respectively.

Amazon's (NASDAQ: AMZN ) online store grew at a low to a flat rate in 2022. The growth of its physical stores, WholeFoods, slowed down on a quarterly basis. This suggests that DoorDash grabbed more share in the grocery space in 2022.

Amazon revenues growth (Amazon)

{kind=link}

Valuation

We first dig into the TAM of Uber.

-

International Expansion

According to Statista , revenue in the Europe ride-sharing segment was projected to reach $69 billion in 2023 and was expected to grow at a CAGR of 2.4% to reach $76 billion in 2027. Uber entered Europe in 2011 and started its ride-sharing business. UberEats launched in 2016, starting in Amsterdam, Netherlands. Since then, it has expanded to operate in many countries across the continent, including the United Kingdom, France, Germany, Spain, Italy, and many others.

Uber established its footprint in Europe and thus has an early mover advantage compared to DoorDash in the Europe online food delivery business.

-

U.S. Grocery Business

According to Statista , Revenue in the online food delivery market is projected to reach US$231.30 billion in 2023. Uber took advantage of its delivery network and infrastructure to launch its on-demand grocery delivery service in 2020. It grew its delivery service by 114% and 30% in 2021 and 2022.

DoorDash Matching Uber's Market Potential

The total market value for food delivery in the United States and Europe was $231 billion and $113 billion. The total market value for ride-sharing in the United States and Europe was $71 billion and $69 billion, respectively.

Uber held a dominant position in the $253 billion combined ride-sharing and online food delivery markets in the United States and Europe. DoorDash only enjoyed a competitive advantage in the $231 billion US online food delivery market.

Since two businesses were vying for the same market, let's assume in 10 years they both will have a 10% market share in the markets they already dominated and a 5% market share in the markets they didn't. Then, DoorDash's revenue may exceed $35.7 billion, while Uber's may exceed $36.8 billion in 10 years, implying a CAGR of 18.4% and 4.2%, respectively.

Uber presently has a market cap of $63 billion, whereas DoorDash is valued at $24.2 billion. This suggests that the current market value to expected revenues ratios for DoorDash and Uber, respectively, are 0.68x and 1.6x.

Both businesses expanded internationally and were expected to do so at double-digit rates in 2023. We believe this implies the delivery market is under-penetrated.

Take a look at the valuation of their competitors:

Chinese on-demand delivery platform Meituan (MPNGF): The company was projected to grow at double digits and has a market cap of HKD 808.2 trillion ($102.9 billion) with a P/S ratio of 3.18x.

E-commerce rival Amazon: The company was projected to grow low single digits and has a market cap of $1.05 trillion with a P/S ratio of 1.89x.

We think considering the competitive advantage of the on-demand delivery platforms and its growth prospects, DoorDash is very attractive.

Catalysts

Q1 and 2023 outlook (DoorDash)

{kind=link}

DoorDash projected its gross booking to grow by 13%-18% in 2023 and 22%-26% in Q1 2023.

If the company can maintain its double-digit growth rate in the U.S., or successfully penetrate the international market through the acquisition of Wolt, then the market will likely recognize the potential for the grocery delivery segment. This can convince investors that the company can continue to grow in this under-penetrated market despite of the inflation environment.

Risks

Grocery Competition From Amazon

Although Amazon has likely lost some market share to on-demand delivery platforms, it still poses a significant threat to these platforms in the long term. With its food delivery arm, and Whole Foods, Amazon is able to compete on factors such as food quality and low delivery costs, which could potentially impact the success of on-demand delivery platforms in the market.

While DoorDash has attempted to build its own warehouses, it is unclear whether this strategy will be successful in the face of Amazon's competition. Investors should closely monitor Amazon's future moves in the food delivery market.

Summary

We believe the market is concerned about how a recession would affect on-demand platforms. DoorDash is able to manage costs to grow in this challenging environment. Its business model is responsive and adaptable. We think the market has not fully priced in the huge potential of domestic and international grocery markets. Compared to the existing players, We think the stock is cheap.

After considering that DoorDash and Uber have similar projected revenues in the areas they dominate, we believe that DoorDash's stock is currently priced at a significant discount compared to Uber's. As a result, we rate DoorDash as a "Strong Buy".

For further details see:

DoorDash: The Real Potential Of On-Demand Platforms Beyond Inflation Worries