XLU - DPG And DNP: Big Distribution Cut From One Warning For The Other

2023-06-20 11:00:00 ET

Summary

- DNP Select Income and Duff & Phelps Utility and Infrastructure Fund Inc are two popular income closed-end funds.

- While their longer-term trends are not identical, they have a lot in common when you examine recent pricing and 3-year performance.

- One just delivered a massive distribution cut, is the other next?

It is surprising that investors get "surprised" when a fund cuts its distributions. 99 times out of 100 the red flags are there and investors tend to ignore it. Sure, there are some that have red flags and don't cut for prolonged periods. But everyone that does cut, has a tell. Today we look at two funds, from the same family and go over the recent price action and distributions.

Duff & Phelps Utility and Infrastructure Fund Inc. (DPG) & DNP Select Income Fund (DNP)

The two funds are from the same Duff and Phelps family even though the DNP name does not mention it. DPG is focused on utilities and infrastructure as the name implies. Utilities are about 61% of the total and the rest is midstream and telecommunications.

DPG Website

DNP again sounds like it is being coy about what it does, but the fund's description gets us that information.

The primary investment objective is current income and long-term growth of income. Capital appreciation is a secondary objective. The Fund primarily invests in a diversified portfolio of equity and fixed-income securities of companies in the public utilities industry. Under normal market conditions, more than 65% of the Fund's total assets will be invested in securities of public utility companies engaged in the production, transmission or distribution of electric energy, gas or telephone services.

Source: DNP Website

The "more than 65%" part has traditionally meant 65% in utilities and the remaining in midstream and telecommunication sectors.

DNP Website

The similarities do not end there. Both have been using the similar levels of leverage with DNP at 26.74%.

CEF Connect - DNP

DPG is a bit ahead at 31.26% but we can call this in the same zip code.

CEF Connect-DPG

One notable difference here is that while sector allocation and leverage levels are the same , the funds do have different sets of managers. This is visible in the 10 top holdings. DPG's holdings are shown below. Note the concentrated exposure here with 50% of the fund in the top 10 assets.

CEF Connect-DPG

DNP's choices are shown below. There is some overlap but concentration is far lower.

CEF Connect - DNP

Outlook

Why are we talking about these two today? Well DPG did drop the hammer on investors by cutting its distribution by 40%.

At its June meeting, the Board of Directors voted to maintain the Fund's Managed Distribution Plan, but to decrease the quarterly distribution rate from its previous level of $0.35 per share to a new level of $0.21 per share. This represents a decrease in the annual distribution level from $1.40 per share to $0.84 per share. The 40% decrease in the distribution reflects the increase in the Fund's cost of leverage, current and expected earnings, and overall market conditions. The Fund's investment adviser and Board of Directors believe that the new distribution level should be more sustainable over time and thus that the new level is in the long-term interest of shareholders.

Source: Seeking Alpha

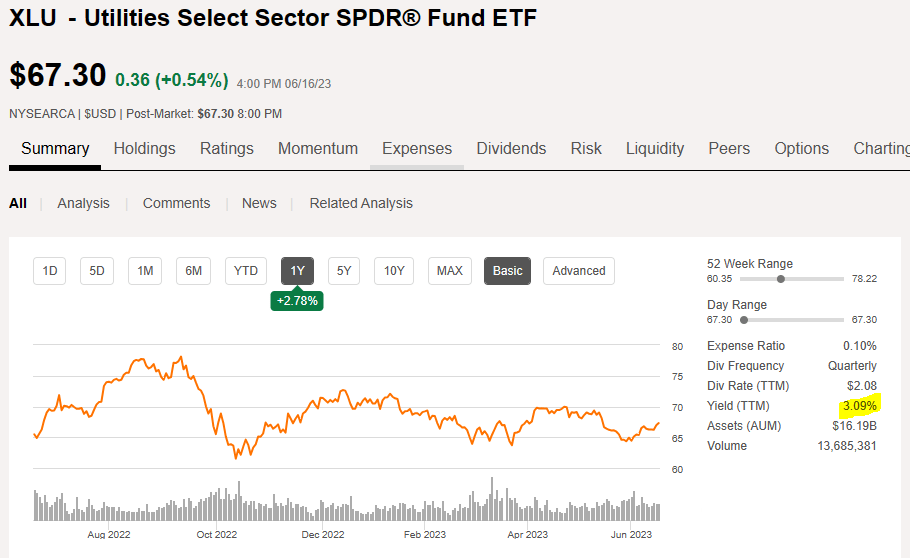

The comments section of the press release is full of disbelief. The fund was distributing 12.4% on the NAV of $11.24. That really appeared sustainable to people? The utilities sector as represented by the Utilities Select Sector SPDR ( XLU ) has a distribution of 3.09%.

{kind=link}

Notice how the one year chart shows a complete absence of price gains. The midstream sector generates about 8%-9% on average but you have to weigh those two at the ratios in the fund, adjust for leverage and management fees, you get a 5% yield. So when the fund is distributing 12.4% on NAV you have to believe in fairies and pixie dust to think that is something you are pocketing risk-free. That leap of faith might be warranted if you were getting the fund at a big discount. You could possibly still have solid total returns (less than 12.4% but more than 5%). But investors had rushed to pay a premium for this. To be clear, this inane behavior was relatively recent. After years of holding the fund at an appropriate discount we saw a sudden rush to go all-in.

{kind=link}

The first question investors must have is whether this is done. The answer most probably is "no". You will likely push this to a bigger discount over the next few weeks. On the plus side the utilities sector as described in our market commentary , is relatively better priced today versus the broader market, so that helps. The second question would be whether the new distribution is sustainable and the answer is "probably". The yield is 7.47% on NAV and we think that can be sustained over the long term. The fund can possibly deliver 4-8% total annual returns from here based on the sectors they hold, so that can work out. The final question would be, whether we would buy it. The answer is a hard "no." We are avoiding all leverage vehicles at this point as we think the fallout here from the economic slowdown is not over. DPG could be ok, but we have no desire to bet on that. Our composite pain scale rating is as follows.

{kind=link}

How Does This Relate To DNP?

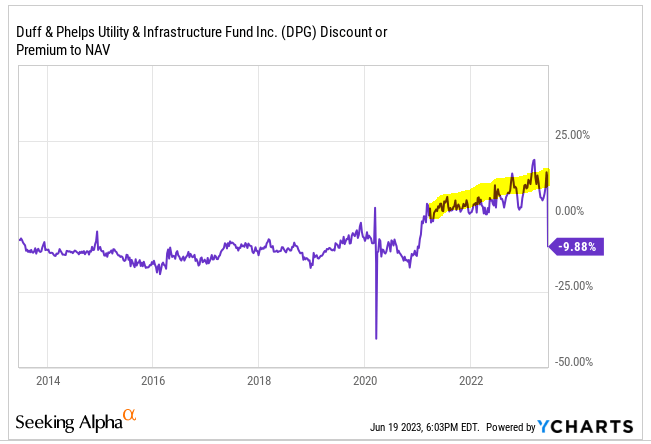

While The euphoria behind DPG was a relatively new concept, DNP has traded at a premium for the bulk of the last 10 years.

Here is the kicker. Below is the return for DNP on NAV. Note the recent NAV returns.

{kind=link}

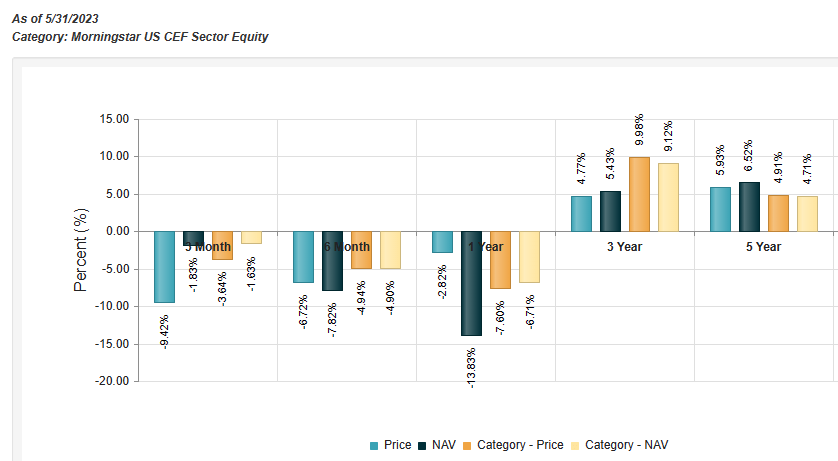

DNP is distributing $0.065 per month which works to a 7.63% yield. But that is on the current price. The yield on NAV is 9.15%. So across 1, 3 and 5 years, total return has not covered the current yield. The bulk of that time was the ZIRP (zero interest rate policy) funded. So investors are again betting a very rosy outcome in a 5% Fed Funds rate environment that would allow the big premium to be sustained. If you get two more years where the fund NAV produces flat returns and the fund has to cut the distribution what will your returns be? Visualize this trading at a 15% discount. It will be a painful journey. Yes, DNP has handily done better than DPG over the long term, but over the last three years, DPG outperformed on NAV returns.

We would just look the other way if DNP was a standard closed end fund trading at a 5-10% discount. But you have a 20% premium and a sister fund that just showed willingness to kill the sacred cow. The risk-reward looks awful. Our composite pain scale rating is as follows.

{kind=link}

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

DPG And DNP: Big Distribution Cut From One, Warning For The Other