PDYPF - DraftKings: Being Outdone By Competition?

Summary

- DraftKings operates in a potentially lucrative market.

- But currently the company is spending too much money compared to the competition.

- Therefore, I believe that a competitor is a more attractive investment option at present.

Thesis

I strongly believe that the online sports betting industry offers promising prospects for generating substantial returns. However, considering certain drawbacks and vulnerabilities, I believe there is a more suitable option than DraftKings ( DKNG ) to invest in this market. In the following points, I will articulate my viewpoint. It's important to note that the online sports betting and iGaming landscape is dynamic and subject to change, so it's possible that market conditions could shift in favor of DraftKings in the future.

Short Introduction

DraftKings is a leading American daily fantasy sports and sports betting platform. It was founded in 2012 and is headquartered in Boston, Massachusetts. DraftKings offers contests in various sports such as NFL, NBA, MLB, NHL, golf, MMA and more. Users can enter contests and draft virtual teams using real-life player stats, with the chance to win prizes based on their teams' performances. In addition to daily fantasy sports, DraftKings also offers traditional sports betting and iGaming in multiple states where it is legal.

Analysis

DraftKings is set to release its 4th quarter report for 2022 in the next two weeks. I anticipate that they will surpass revenue projections, owing to the boost from the Soccer World Cup. However, I believe that the issues that plagued their performance in the 3rd quarter are likely to persist.

{kind=link}

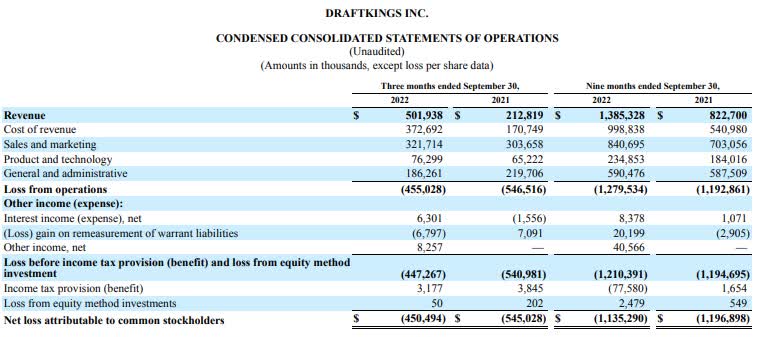

The above screenshot shows that the revenues have increased by 68.4% compared to the 9-month period in the previous year. The problem is, however, that in the same period, the cost of revenue has increased by 84.6%. DraftKings actually has a cost problem. Unlike competitor FanDuel (DUEL), they have higher marketing expenses and still achieve lower revenues. Furthermore, it takes them 2-3 years to reach profitability in a new state , while FanDuel takes less than 18 months to generate a profit . Another reason why FanDuel is better positioned is that they currently have better margins. This is also due to the fact that there is no real competitive advantage for DraftKings, except maybe the first mover advantage. However, in the past, other markets have shown that this is not the strongest moat, compared to, for example, network effects.

10-Q

The graph shows a notable increase in shares outstanding, which has diluted the ownership value for existing shareholders by nearly 10% this year. DraftKings aims to achieve EBITDA profitability by 2024, utilizing their current cash balance of $1.4 billion. If this objective is not met, the company may need to secure loans or issue additional shares, potentially lowering the value per share. Conversely, FanDuel has a more favorable outlook, targeting profitability in 2023 and benefiting from a strong financial partner in Flutter ( PDYPY ), which boasts extensive experience in the gambling industry.

{kind=link}

This chart illustrates the tremendous potential of the online gaming industry, with an anticipated 4.5x increase in revenue over the next seven years, offering substantial profits. Currently, DraftKings, FanDuel, and BetMgM hold a combined 80% of the total market share , with DraftKings and FanDuel occupying the top two spots. FanDuel has a slight advantage in the OSB market, while DraftKings is ahead in iGaming, where the margins are more favorable. Despite the impressive growth potential, only 11% of the American population has access to iGaming, while OSB is accessible to 45% of the population.

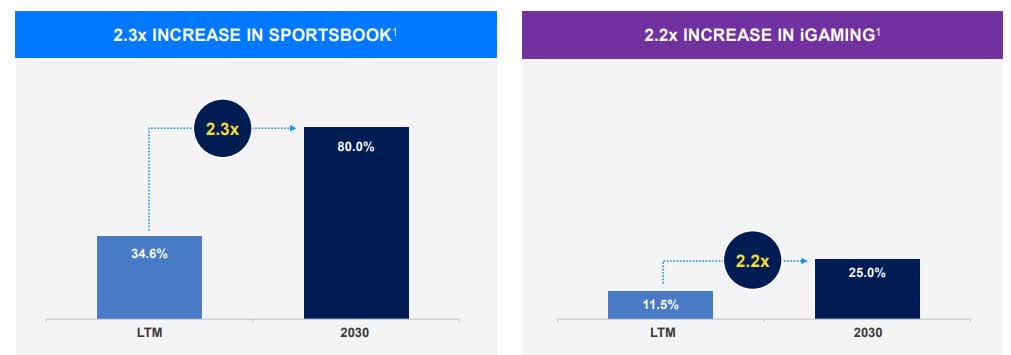

Unfortunately, both companies face a setback with California, home to 12% of the American population, initially voting against online gaming. The following chart depicts FanDuel's expectations of OSB being available to 80% of the population and iGaming to 25% by 2030.

{kind=link}

The question now is whether it is possible to generate other sources of income. Because it looks like the expansion into new states will slow down, and then it comes down to being more profitable than the competition. Here, DraftKings has Reignmakers, an NFT game similar to Sorare and their Fantasy Sports NFT game. Sorare was valued at $4.3 billion in 2021 and recently entered into a partnership with the world's largest soccer league, the Premier League. How these NFT games will develop remains to be seen as the NFT hype has greatly subsided.

Expanding to Europe will also be difficult for DraftKings, as established OSB providers already exist there, some of which have already been operating in these markets for several years. An advantage that DraftKings has over conventional casinos is that they don't have to maintain expensive real estate assets. However, they also can't cross-finance their business activities through other business segments.

Gambling is a product that carries the risk of addiction, yet it offers the potential for substantial returns, similar to the successful model established by Altria ( MO ) in the cigarette market. While a gambling provider may not be able to build a brand as iconic as Marlboro, it's possible for a market structure like S&P ( SPGI ), Moody's ( MCO ), and Fitch to emerge in the industry. A market dominated by three companies would be favorable, allowing them to concentrate on maximizing margins and driving revenue growth. However, it's likely that other companies, such as Fanatics ( FANA ), will attempt to enter the market and compete in the future.

If we take a look at the valuation of FanDuel, we see that it was valued at $22B with $3B in revenue, which corresponds to a multiplier of 7.3x. If we now assume that DraftKings is currently less well positioned, I think we can use a multiplier of 5x for them. With an estimated revenue of $2.1B, we would now arrive at a valuation of $10.5B. Since the market value is currently $7.57B, this could mean an undervaluation of almost 38%. However, the market's perception of the validity of this value is also contingent upon the possibility of another recession in 2023, as well as the market's response to the Federal Reserve's actions and the impact of inflation in the future.

Conclusion

Currently, the risk-reward balance appears to be more favorable for FanDuel compared to DraftKings. This is due to its stronger financial footing and recent economic performance. However, it's important to acknowledge the risk that DraftKings's $1.4B cash reserve may not be enough to achieve profitability. The company's tendency to overspend also adds to this risk. If these issues can be effectively addressed, the outlook for DraftKings may improve.

In conclusion, I believe that FanDuel/Flutter represents a better investment opportunity at present. It might be worth considering a small initial investment that has the potential to grow into a larger position. However, it's important to keep in mind that even for FanDuel, there's no guarantee of a stronger position in the next five years.

For further details see:

DraftKings: Being Outdone By Competition?