DKNG - DraftKings: Increasing Competition Pushes Back Path To Profitability

2023-08-23 07:14:48 ET

Summary

- DraftKings' stock price has more than doubled YTD due to strong revenue growth and upgraded guidance, but the rally may be overdone.

- Increasing competition from new entrants like Fanatics and ESPN pose risks to DraftKings' market share.

- DraftKings' revenue growth is unsustainable in the long run, relying on expansion into new states and increasing the holding rate, which may lead to customer churn.

Executive Summary

DraftKings' (DKNG) share price has more than doubled since the beginning of the year. This has been driven by strong revenue growth and an upgrade to full-year guidance. In conjunction with their Q2 earnings release, DraftKings increased their full year 2023 revenue guidance to $3.5 billion which represents an impressive 56% growth rate versus 2022. They also said they expect to generate substantial positive adjusted EBITDA in 2024. With such bullish guidance, it's unsurprising that DraftKings' stock has performed well. But I think the rally has gotten ahead of itself.

My main concern is increasing competition with two new competitors set to enter the market this year. In July of 2023 Fanatics acquired the US operations of PointsBet for $225 million . Fanatics is one of the largest sports apparel manufacturers in the world. Their wealth of proprietary customer data from their existing apparel business will make them a formidable competitor. Separately, in August of 2023 PENN Entertainment (PENN) signed a $1.5 billion deal with ESPN to launch an ESPN-branded sportsbook which is expected to launch this fall. PENN Entertainment used to operate the Barstool Sportsbook which has languished, only representing ~2% of US sports betting market share . Given ESPN's strong brand power and their ability to promote on ESPN's cable television channels, the new ESPN sportsbook will likely be a much more formidable competitor.

With these two new market entrants I believe the US sports betting market is still many years away from maturity and DraftKings will likely need to continue spending aggressively on sales and marketing to maintain its market share.

DraftKings

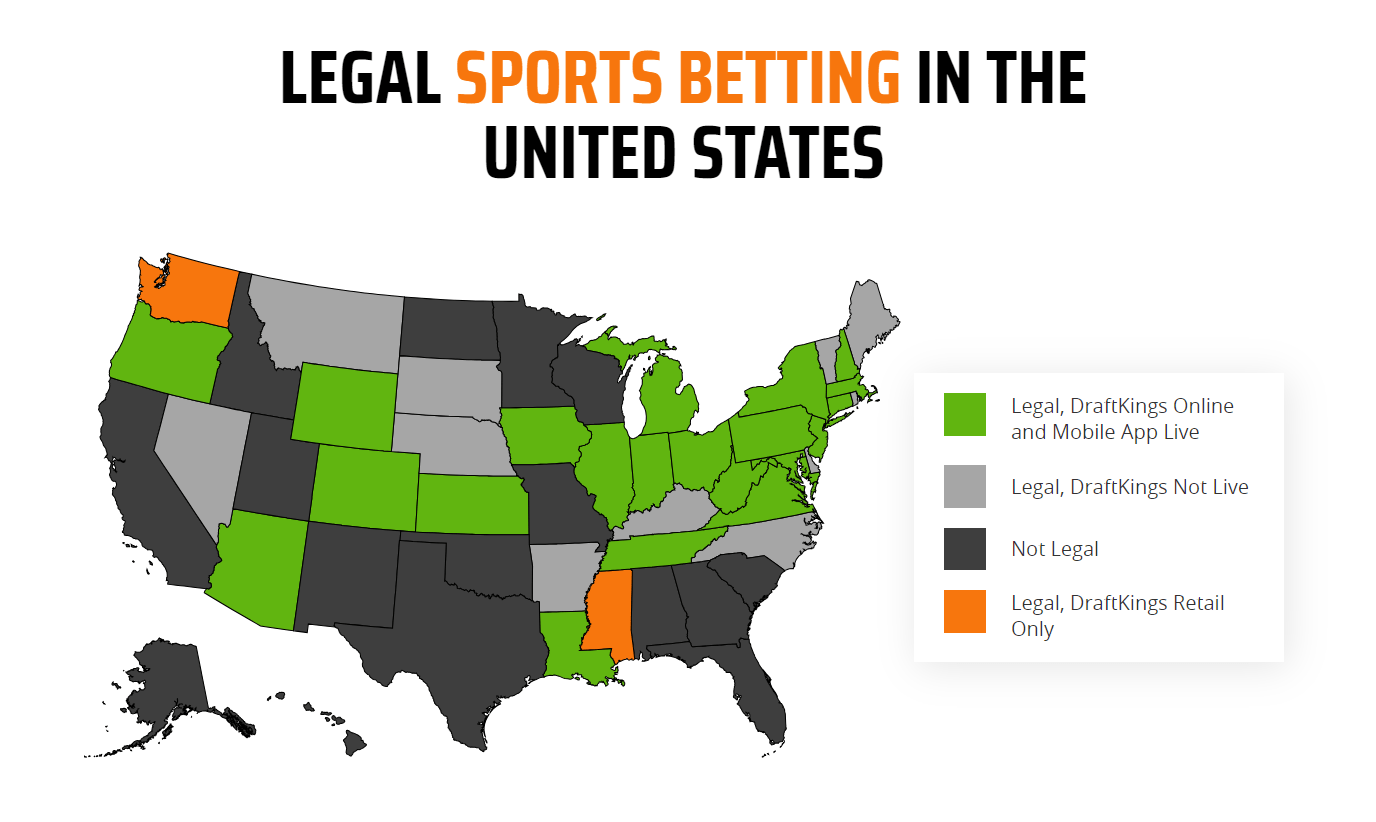

After a 2018 Supreme Court decision legalized online sports betting at the federal level, many states have legalized online sports betting. DraftKings got into the online sports betting business in 2018, making it one of the first movers. As more and more states legalized online sports betting, DraftKings wasted little time expanding. They currently operate in 23 states representing ~44% of the US population according to US census bureau data.

States where DraftKings operates (DraftKings)

{kind=link}

The online sports betting market has become extremely competitive with traditional casino companies like MGM Resorts (MGM) and Caesars Entertainment (CZR) entering the space. Digital-only operators like DraftKings and Flutter Entertainment (PDYPY) owned FanDuel have also entered the market. According to iGaming Business , FanDuel currently has the largest market share at ~43%. DraftKings is in the second place at ~25% and everyone else is 10% or less.

US Online Sports Betting Market Share (iGaming Business)

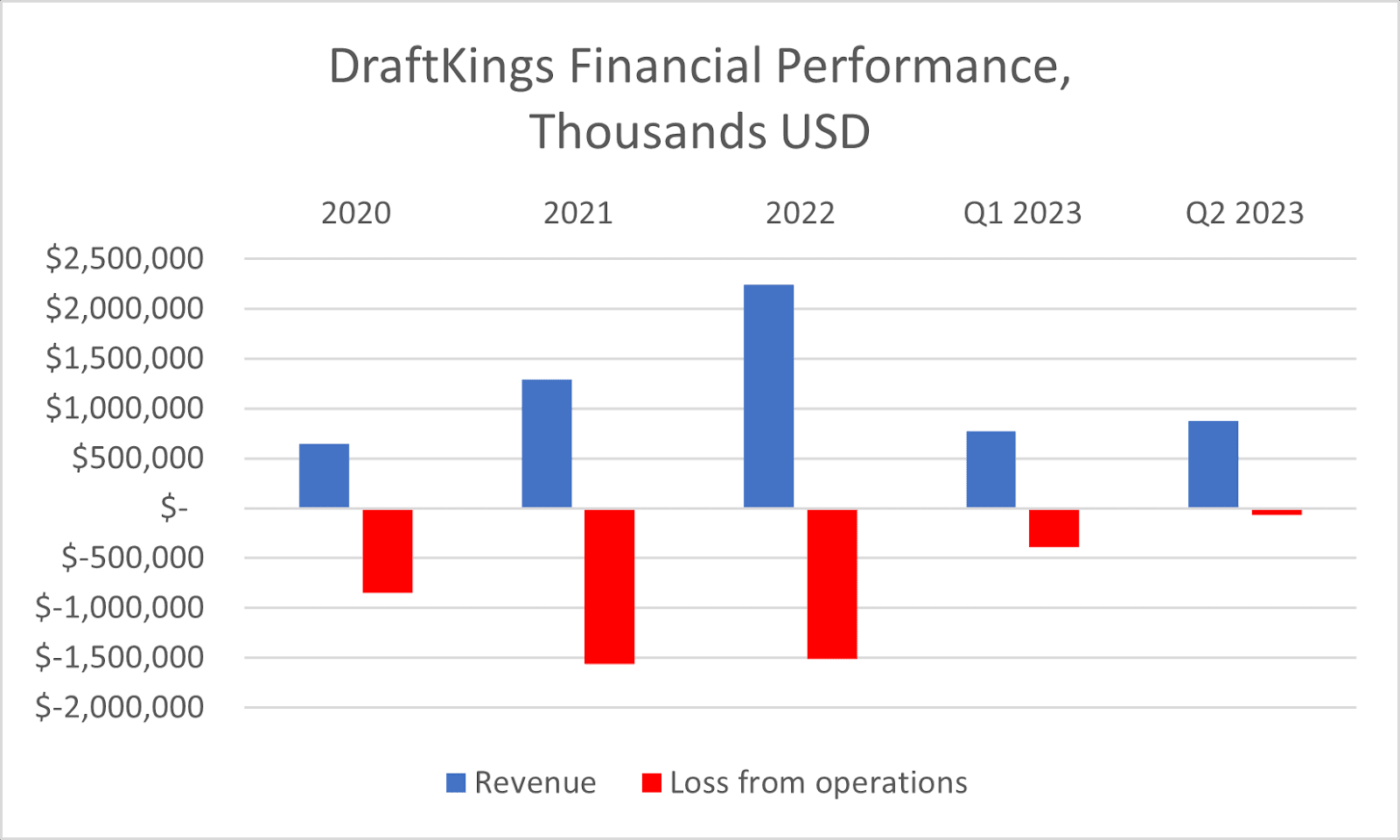

Since going public, DraftKings has posted very impressive revenue growth. From 2020 through 2022, revenue more than tripled from $643 million to $2.24 billion. Their full-year guidance of $3.5 billion of revenue in 2023 represents a 56% increase over 2022.

DraftKings Financial Performance (company filings, compiled by author)

{kind=link}

Revenue Growth Is Likely Unsustainable

While DraftKings' revenue growth is surely impressive, it's important to dig into the sources of growth. Revenue is recognized as money bet on the platform minus customer winnings. The odds for any casino are tilted slightly in the house's favor so on average the house wins. In the industry, revenue as a percentage of gross betting volume is called the holding rate.

Based on my analysis, the majority of DraftKings' revenue growth has come from two sources, expanding into new states and increasing their holding rate.

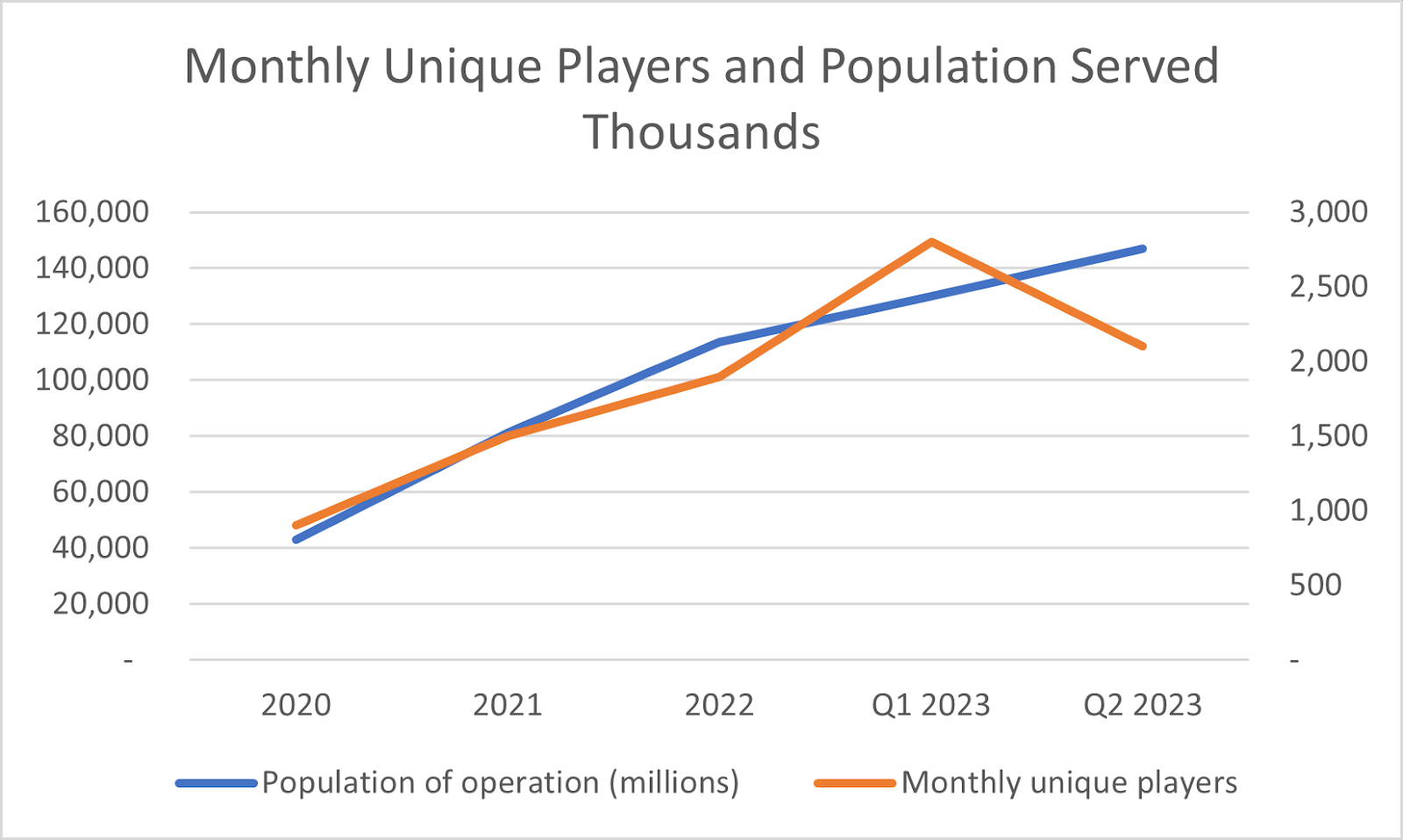

As more states legalized gambling, DraftKings' total addressable market has increased commensurately. In 2020, DraftKings had an average of 0.9 million monthly unique players. By Q2 2023, this has increased 133% to 2.1 million. In 2020, DraftKings was available to on average 43 million people. This is based on when they launched in each state. By Q2 2023, DraftKings was available to 147 million people, a 241% increase since 2020. The population served has grown faster than DraftKings' monthly unique players.

Monthly unique players and population served (company filings, US Census Bureau, compiled by author)

{kind=link}

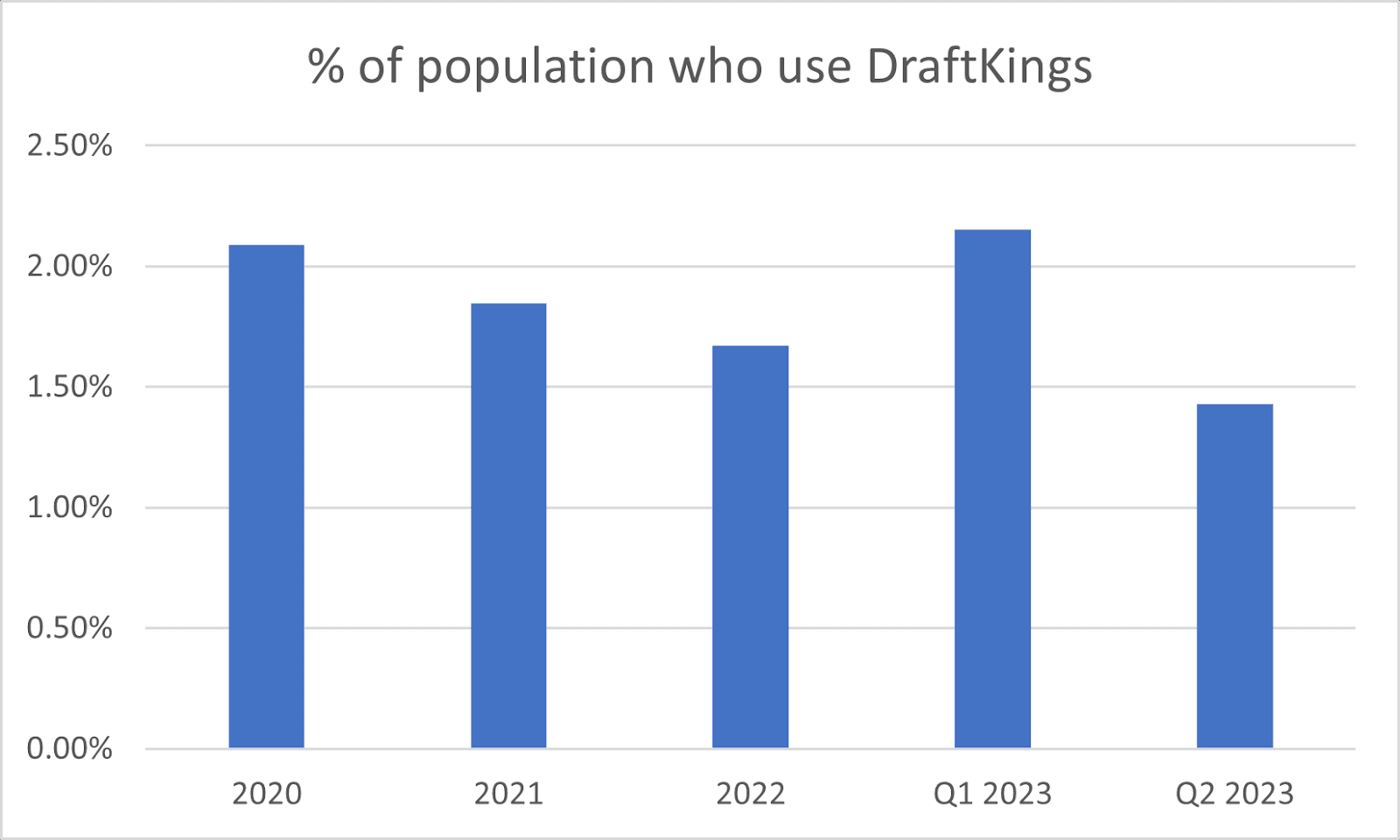

Another way to look at it is as a percentage. In 2020, 2.1% of people who lived in a state where DraftKings was available used DraftKings. By Q2 of 2023, this percentage has decreased to 1.4%. There was a boost in Q1 2023 likely due to the Super Bowl. But other than that, the trend is clearly downward.

% of available population using DraftKings (company filings, US Census Bureau, compiled by author)

{kind=link}

This suggests DraftKings has problems with customer churn. When they launch in a new state, they attract a lot of users partly as a result of generous new user promotions. But over time, customers stop using the platform. The customer churn has been masked by DraftKings receiving an influx of new users every time they launch in a new state. But there are only 50 states in the union. Eventually, they will run out of states to expand into and their user growth will likely flatline.

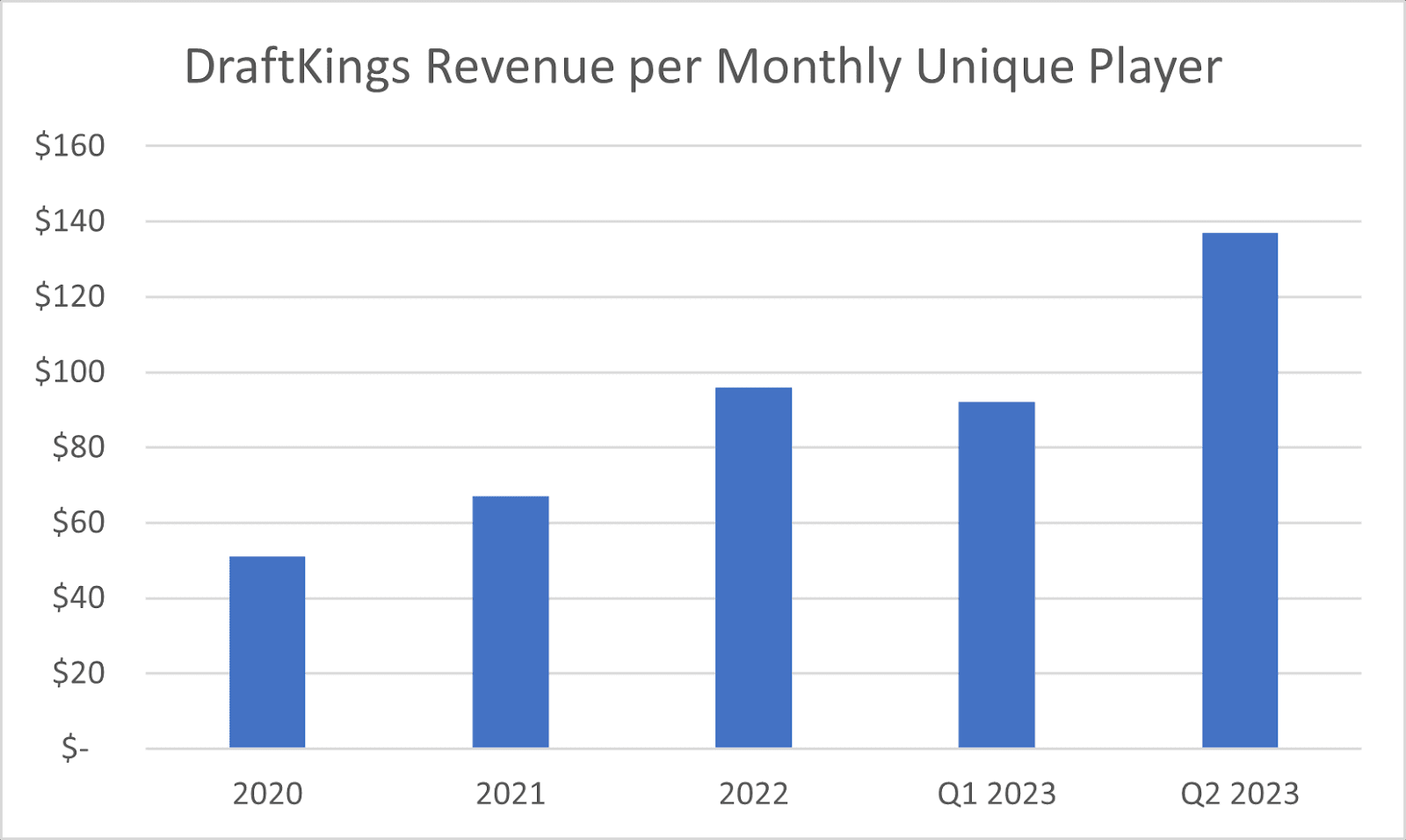

The second way DraftKings has increased its revenue is by increasing revenue per player. In 2020, they generated $51 per monthly unique player. By Q2 2023, this has more than doubled to $137 on an annualized basis.

DraftKings Annualized Revenue per Monthly Unique Player (company filings, compiled by author)

{kind=link}

There are two ways revenue per player can increase. Either the gross betting volume per player can increase or the holding rate can increase. DraftKings does not disclose its gross betting volume or holding rate. But I believe the increase is primarily driven by increasing the holding rate. Typically, simple bets such as whether or not a team wins a game have lower holding rates. More complex bets such as parlays have higher holding rates. This is because players can easily calculate the holding rate with simple bets and they won't take the bet if the holding rate is too high. For parlays, it is much more complicated to calculate so sportsbooks can get away with setting higher holding rates. During an investor conference in May of 2023, DraftKings CEO Jason Robins said:

We've seen no decline in demand as we've increased the hold rate. The important thing is we're not increasing it by making the odds any worse for customers. It's just by pushing more parlay mix and things like that.

Pushing more parlays and other complicated bets is great for revenue in the short-term. But it is a risky strategy in the long-term. Customers will lose more money on average which could eventually cause them to leave the platform. Thus, I don't view this as a sustainable strategy to grow revenue.

Steady-State Revenue And Margins

In 2023, DraftKings expects to generate $3.5 billion of revenue. They also plan to launch in Kentucky, North Carolina, Vermont, and Puerto Rico . That would bring them up to 165 million people served or 50% of the US population. If we assume all states will eventually legalize online sports betting, DraftKings' revenue could double to ~$7 billion. This is a best-case scenario of all 50 states legalizing sports betting, which may or may not ever happen. So how much profits could DraftKings make on $7 billion of annual revenue?

Perhaps the best precedent to use is Flutter Entertainment, which owns FanDuel in the US as well as Betfair and PaddyPower, two of the leading online sportsbooks in the UK and Ireland. Online sports betting is a mature industry in the UK and Ireland, so we can use this as a gauge of what steady-state margins will look like in the US once the industry matures. However, there is a major difference. Tax rates in the US are much higher. Many of the states which legalized sports betting did so primarily as a way of generating tax revenue. For example, New York imposed a 51% tax on online gaming revenue . These gambling taxes are recorded within cost of goods sold on the income statement. DraftKings and Flutter have not disclosed how much gambling taxes they pay. But we can see it is significant based on the fact that Flutter's US gross margins are substantially lower than their UK & Ireland gross margins.

Flutter Entertainment and DraftKings gross margins (company filings, compiled by author)

In the first half of 2023, Flutter's US gross margin was 50% compared to 69% for the UK & Ireland. DraftKings' gross margin was even lower at 37%. To be fair, some of this difference may be the result of Flutter setting lower holding rates in the US in an effort to gain market share. However, in their 2030 target, they still assume gross margins will stay around 50%. This leads me to believe the main driver of lower gross margins in the US is gambling taxes, which are not expected to change.

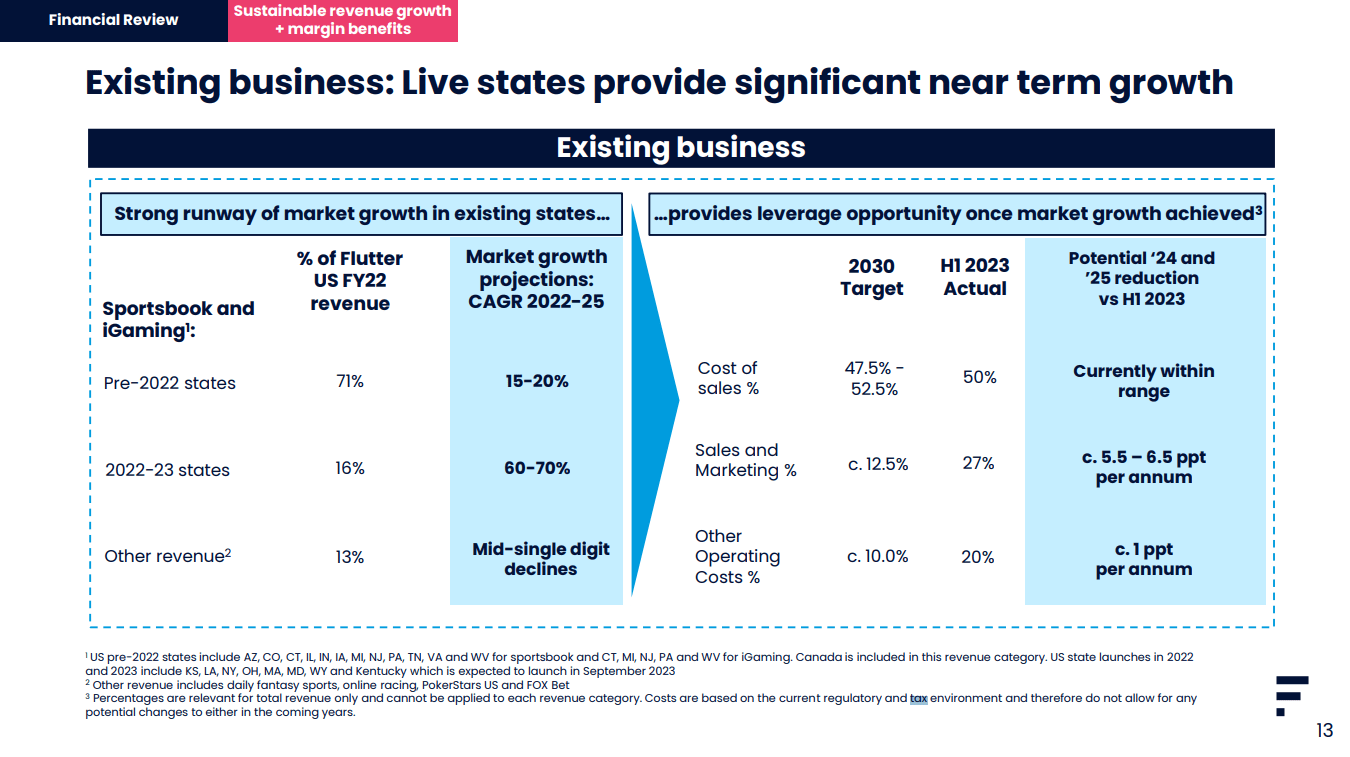

Flutter Entertainment 2030 margin targets (Flutter Entertainment)

{kind=link}

Flutter is targeting for their sales and marketing expense to decrease to 12.5% of revenue by 2030 and other operating costs to decrease to 10%. In my opinion, these targets are too optimistic. In the UK and Ireland, Flutter spent 18% of revenue on sales and marketing in the first half of 2023 and 16% on other operating expenses. Given that the UK and Ireland is already a mature market, I don't see why the costs would be lower in the US. A more realistic assumption for mature US margins would be 50% cost of revenue, 18% on sales and marketing, and 16% other which yields an operating margin of 16%. DraftKings has not published long-term margin targets but we can assume they will be similar. Based on my assumption of $7 billion in annual revenue, DraftKings could generate ~$1.1 billion of operating profit at maturity or ~$900 million of net income assuming a 21% corporate income tax rate. So how much should DraftKings be worth today based on $900 million of steady-state net income some years down the road?

Valuation

DraftKings currently has a share price of $26.57 and 488 million fully diluted shares outstanding, giving them a fully diluted market cap of ~$13 billion. They also have about $100 million of net debt. They posted a net loss of more than $1 billion in every one of the last three years and an almost $500 million loss in the first 6 months of 2023. The cash outflow was much less than this as they heavily utilize stock-based compensation. Since DraftKings went public their fully diluted share count has increased almost 40% from 352 million to 488 million. From my perspective, I don't really care whether the losses are cash or share based as either way this is a real cost to investors. That's why I prefer to look at net income instead of adjusted EBITDA. In the second quarter of 2023, DraftKings' operating loss improved substantially to -$69 million. This improvement was mostly attributable to a $181 million sequential decrease in sales and marketing expense as well as a higher holding rate which boosted revenue. Given the looming competitive threats of Penn's new ESPN branded sportsbook as well as Fanatics, DraftKings will likely be forced to increase sales and marketing, decrease its holding rate, or both to maintain its current market share.

We're still many years away from reaching market maturity. Let's assume that 5 years from now in 2028 the market consolidates around a few players with DraftKings being one of them. DraftKings' profitability has been improving but it will likely get worse over the next couple years due to the two new market entrants. Let's assume DraftKings loses $500 million per year over the next 5 years. This is less than half of their average annual losses over the prior 3 years. So by 2028 they will have lost another $2.5 billion which will most likely be funded by equity issuances and / or stock-based compensation. Based on the current share price, that would push their fully diluted shares outstanding to ~580 million. Based on my assumption of $900 million steady-state net income, they would make ~$1.55 of EPS in 2028. If we apply a 20x multiple, we get ~$31 per share. But this is 5 years in the future. If we discount that back to today at a 10% discount rate, we get $18.30 per share, far less than the current share price.

Risks To Bear Thesis

There are two major risks to my bearish thesis. Firstly, if the new ESPN and Fanatics sportsbooks flop, the competitive situation will be far more favorable. Secondly, DraftKings may be able to continue increasing its holding rate by pushing more parlays and other exotic bet types. I will be closely monitoring the performance of the new ESPN and Fanatics sportsbooks as well as DraftKings' average revenue per player. If the performance of the new competitors is worse than expected or if DraftKings' average revenue per player continues to increase over the coming quarters, I may adjust my bearish view.

For further details see:

DraftKings: Increasing Competition Pushes Back Path To Profitability