DKNG - DraftKings: Watch Out For Another Sugar High Rally Ending Badly

2023-07-14 10:32:08 ET

Summary

- Coming good earnings release or not, DraftKings Inc. is still far away from becoming a profit machine in the dreams of breathless analysts.

- We're guiding HOLD for DraftKings, unless you bought in cheap and can take a nice gain off the table now.

- DraftKings' market share remains a strong second place to FanDuel, but the smaller sites will continue chipping away at the leaders in the sector.

"It's déjà vu all over again…." Yogi Berra.

Apparently the analyst race to the pom pom warehouse is on again for DraftKings Inc. (DKNG) shares. More than a few are out there twirling again, salivating at the prospect of another insane run up to the 70s-once occupied by DKNG.

Hold on. This speedway needs a red light .

DraftKings stock has tripled over the 52-week range and sits as of this writing at $31. The story being retailed now is that DKNG, imminently releasing ( Q2 earnings expected August 3) what could be a solid performance in sales growth and more critically, a dramatic decline in marketing costs, will translate once more to dizzying price targets ("PTs") some analysts say could near the crazy highs of 2021. We don't dispute the whisper numbers. ~August 3 rd we'll find out whether to bring out the pom poms or the crying towels.

But what is clear regardless is the growing consensus among some analysts, who should know better, that DKNG is once more at the cusp of a runaway growth of trees to the sky, This is not in any way to suggest that the 2Q23 numbers will not bring a few happy grins from holders.

We do expect losses ~ ($0.77), but probably more, and estimated full year losses of -(1.86). In my view, they could be greater, we'll see. But that's beside my point. What is the point is to add to the view that the run up to date is already overstretching a bull scenario. Several sites estimating the discounted cash flow ("DFC") value of the shares hover in around $13.83.

That puts DKNG shares overvalued by 55% at this moment.

For 2024, we do expect continuing improvement, with an operating loss declining to $(0.97). After a long session with our industry colleagues about the overall prospects of the sports betting verticals, we found most of our panel of 15 thinking that DKNG probably won't turn profitable until the 2026/7 years-that's an opinion only. All agreed their revenue will see sales growth in the 43% to 62% range during that period. But so will its leading competitors. In brief, the consensus among our inside-the-industry observers goes against the grain of current pomp om twirlers and settles in at what is believed to be a more realistic upside limit for the stock in the $28 to $36 range.

{kind=link}

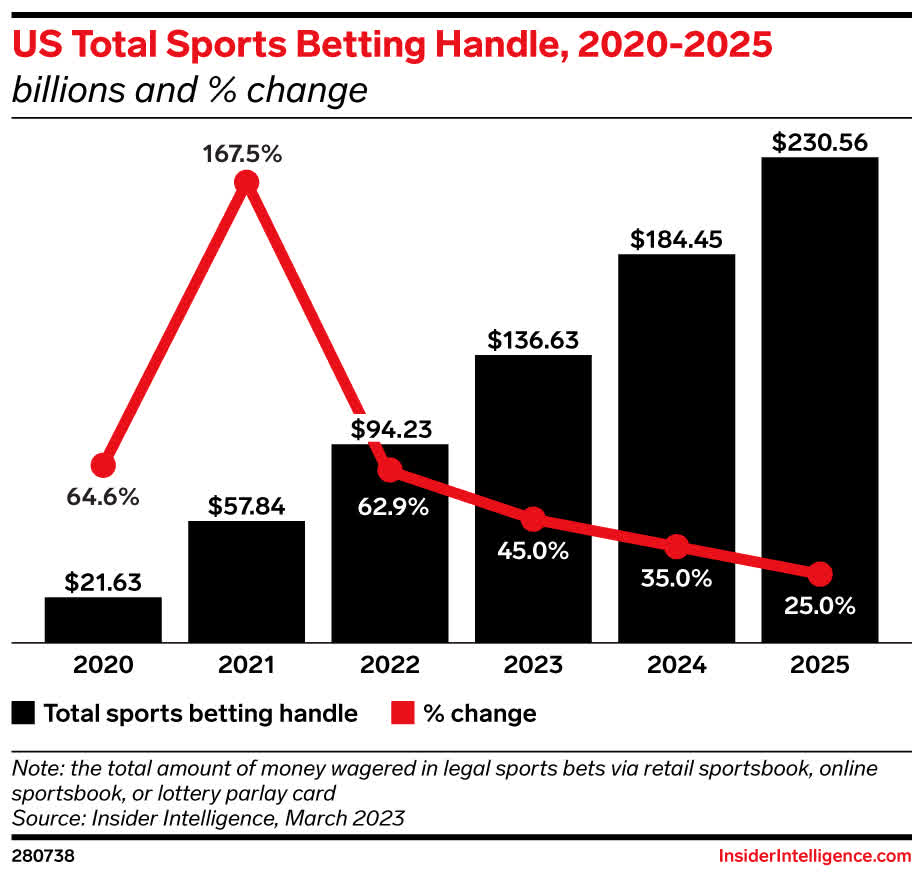

Above: Growth of handle will begin to slow as states still left and imminent to go legal are small. Texas and California are still far away.

Ants at the DKNG picnic

Stipulation: DKNG holds the second-leading share of market in the sector behind FanDuel, and we expect that status to remain in place. It's a solid, aggressive competitor, with a good customer-facing site and a customer retention level commensurate with its nearest peers. It is also alive to opportunities for transactions as either a buyer or a seller. So with an estimated 37% overall market share as compared with leader FanDuel at near 50%, they will continue to own the lion's share of the market to come. There has been a crazed guessing game among industry watchers and platforms as to just how much growth the sector has ahead.

DKNG's last four month's share of market is estimated at:

March: 31%

April: 32%

May: 33%

June: 37%.

During that same period, FanDuel has hovered around 50%.

2023YTD U.S. sports betting handle: $47.4b.

2023 Revenue YTD: $4.5b.

Revenue: $19.1b.

YTD hold percentage: 9.94% indicating that the sites have played on the lucky side of a standard long-term norm of 7%, and this is part of the reason that DKNG will show a nice revenue move for 2Q. But we always look at gaming GGR, whether casino or online, as normalized to well-worn mathematically-proven hold percentages. And 7% is where the ultimate win percentage will find a home give or take decimals.

google

Source: CNBC: DKNG is getting attention again from options players and pom pom twirlers looking for a quick hit. No problem, but still beware.

New markets

DKNG pomp pom twirlers have persistently overrated the value of pending new states revenue as they fall into place. As of now, states like Maine and Nebraska will do okay, but like most of the remaining states not yet in the legal fold are chump change compared with those already in the game.

The two big kahunas, Texas and California, remain in long-term what if territory as various bills slosh around their legislatures with pro and anti-factions fighting it out. Baking in these two potential giants into a what if CAGR scenario is misleading to investors until those initiatives gain some real momentum. A realistic forecast for U.S. sports betting revenue by 2030 comes closer to ~$40 to $50m. That still makes a nice case for DKNG, but not one anywhere near the pomp pom twirler PTs.

{kind=link}

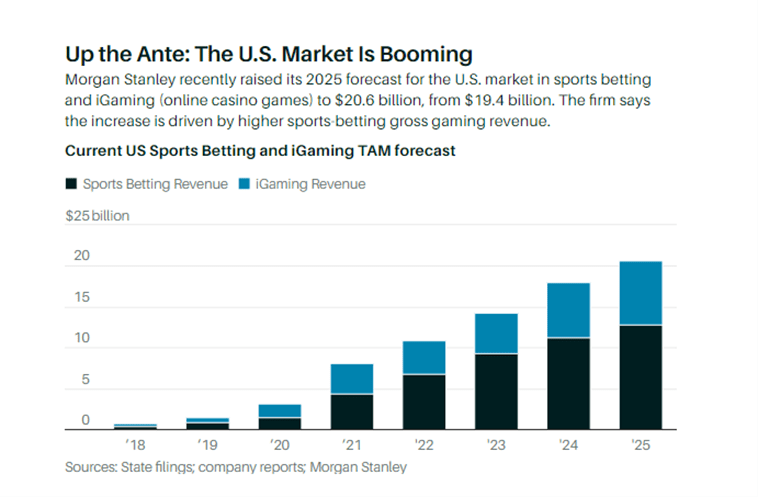

Above: Projections are a moving target. Morgan Stanley (MS) has upped its estimate many times as new states unfold but their market growth is much more realistic than many observers who have delved into triple digit billions.

What really lies in the weeds in the entire space is the absolute certainty that by 2030 we will not be looking at a sector comprised of 14 to 17 platforms. Consolidation will begin slowly but start catching momentum by the early part of 2024, and that is where bets on DKNG with a generous upside potential begin to make more sense than the dizzying numbers we are beginning to see ascribed to the stock again.

Enter Fanatics in an already crowded sector

Privately held sports gear distributor Fanatics is headed by Mr. Mitch Rubin, who has been bloviating about his entry into the sports betting space for two years. He is on the record as predicting that Fanatics with its 62m customers will evolve into a sector revenue leader. That won't happen.

The eventual positioning of Fanatics is similar to that of PENN Entertainment's ( PENN ) acquisition of Barstool Sports with its 55m or more "stoolies" as a made-in-heaven market for sports betting. Penn management living in the real world has long positioned its sports betting goals not by chasing overheated revenue spend, but by moving as quickly as positive into profit territory to bring accretive EBITDA into its results. Barstool Sports book has an estimated 5.5% of volume and is on its way to profitability both in its U.S. platform as well as its Canadian operation. Our point being: DKNG, a solid competitor, does not operate in a vacuum.

Fanatics, just at the toe dip phase of its move, will acquire the U.S. business of PointsBet Holdings, the Australia-based site with an existing business. Last month, Fanatics in Maryland launched bringing $1.6m in handle, but spending 40% in promotional cost. It has a long way to go. But its PointsBet buy can bring it into 12 states. The likelihood of its leapfrogging over the next leaders after DKNG and FanDuel, Caesars ( CZR ) and BetMGM ( MGM ) is dim. It is likely to find a home somewhere in the low single digit share of market.

But the rub here is this: There will be the "puppy dog yipping at the heels" factor of Fanatics and the hoard of others in this crowded space of chipping away small bits of business from leaders in various markets. When you aggregate the combined chippings of all the marginal players in the space you have the logic that DKNG will stay as a leader, but its prospects for wild, exponential sales growth in share are challengeable.

Conclusion

Frantic sentiment can once again propel DKNG stock and begin trading its way beyond its real-world value even given its improving financial performance. There is just too much going on in the sector by competitors old and new for anyone to experience breakaway upsides as we had seen in 2021.

Taking a broad industry view, including the continuing aggressive positions of all DraftKings Inc.'s competitors big and small, we think its hold value sits somewhere in the $23 to $26 range. It's a good operator, its tentacles are strong, but there are just far too many stop signs in the way to produce a runaway upside ahead as we saw in 2021. We must take into account, of course, that a certain segment of the hot take investing population will see trees rising to the skies all over again and jump in from this point forward. But the endgame, in our view, will much resemble the crash and burn we've seen in this stock before.

For further details see:

DraftKings: Watch Out For Another Sugar High Rally Ending Badly