DFH - Dream Finders Homes: A Promising Investment Opportunity In The U.S. Homebuilding Industry

2023-12-05 00:23:04 ET

Summary

- Dream Finders Homes is a growing homebuilder in the US with a trusted brand and an asset-light business model.

- The company has maintained a high return on equity and is seeking to reduce its financial leverage.

- DFH shares are significantly undervalued and offer a margin of safety, making them a good investment opportunity.

Introduction

Dream Finders Homes ( DFH ) - with a trusted brand, an asset-light business model, and a focus on expanding into new markets, DFH is well-positioned to capture market share and generate solid returns for investors. Despite the industry's cyclical nature and tough competition, DFH has maintained a high ROE and is seeking to reduce its financial leverage. As a public homebuilder, DFH has greater financial resources and economies of scale than private and smaller homebuilders. This allows DFH to buy land and lots more easily and at better prices, giving it a significant advantage over its competitors. Moreover, I think the firm shares are significantly undervalued. Nevertheless, DFH is less profitable than its competitors and relies on financial leverage to increase its ROE, which inherently increases its risk as an investment.

Business Overview

According to its 10K Report , DFH is a growing homebuilder in the US with operations in Charlotte, Raleigh, Jacksonville, Orlando, Denver, the Washington D.C. metropolitan area, Austin, Dallas, and Houston. It sells houses under the Dream Finders Homes, DF Luxury, Craft Homes, and Coventry Homes brands. Moreover, DFH offers the following ancillary services: title insurance through DF Title, LLC, doing business as Golden Dog Title & Trust, and mortgage banking solutions primarily through its mortgage banking joint venture, Jet Home Loans, LLC.

Owing to its extraordinary growth in the last five years, DFH is the 15th largest homebuilder in the US (by gross revenue) and one of the most trusted homebuilder brands in the US (exactly the fifth), according to 2023 America’s Most Trusted Study .

DFH runs an asset-light business model similar to NVR ( NVR ), so it doesn’t purchase the land; it controls it with options contracts. Thus, the firm can improve capital allocation by not having a large inventory of lands, which increases the risk of write-downs and requires a large quantity of capital.

The company is managed by its founder, CEO, and chairman, Patrick Zalupski, who owns 65% of the outstanding shares and has 99% of his wealth invested in the company. Thus, I believe his interests are aligned with shareholders’ interests. Another critical executive has been its COO, Doug Morgan, who was a crucial part of the team applying the company's growth strategy by entering new markets and acquiring other homebuilders. Furthermore, Doug Morgan was critical in increasing the number of homes sold and the company's overall profitability, according to the 2022 Shareholders Letter .

Housing Industry

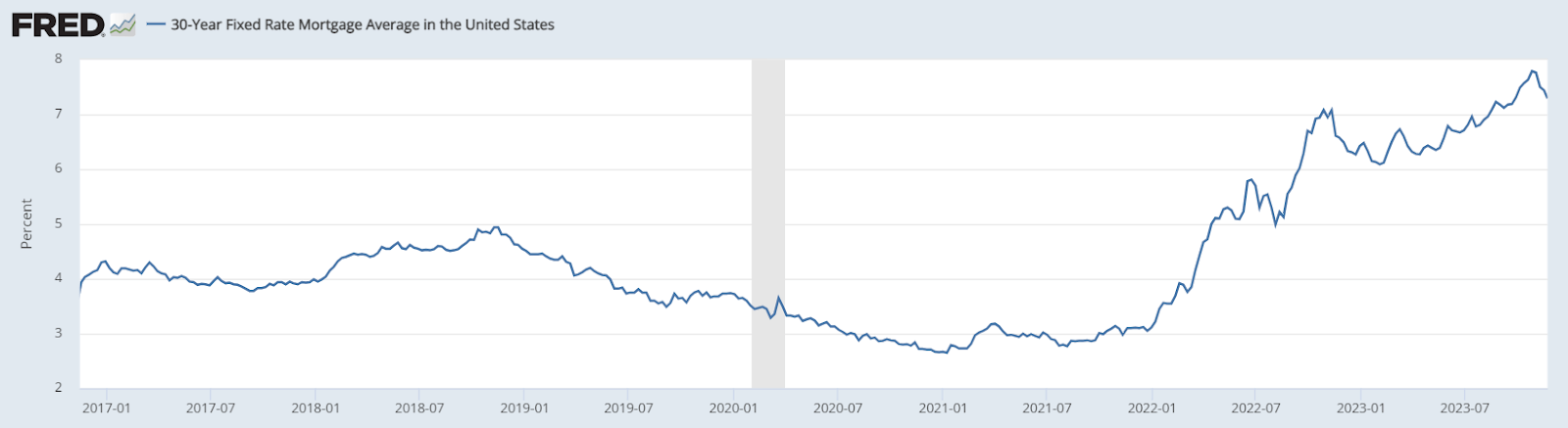

It is one of the most affected industries by the interest rate hikes in the last couple of years. The US's 30-year fixed rate mortgage average skyrocketed after the Fed started to hike its Federal Fund rate and sell assets from its balance sheet. Furthermore, according to Forbes , the hawkish policy of the Fed has stimulated a higher-than-average spread between the 10-year Treasury Yield and 30-year mortgage rate of 300 bps, whereas the long-term average is around 150-200 bps.

{kind=link}

FRED

When writing this article, the 30-year mortgage rate was slightly above 7% after a rapid increase in 2022 and a deceleration in 2023. Consequently, according to the MBA Purchase Index, mortgage applications fell last year. Nonetheless, it seems the demand size is recovering as, in the last months, the index showed a shy reversion. However, I doubt we are close to a significant recovery in the mortgage demand as renting a house is substantially cheaper (by 52% ) than owning a home through a mortgage.

Investing

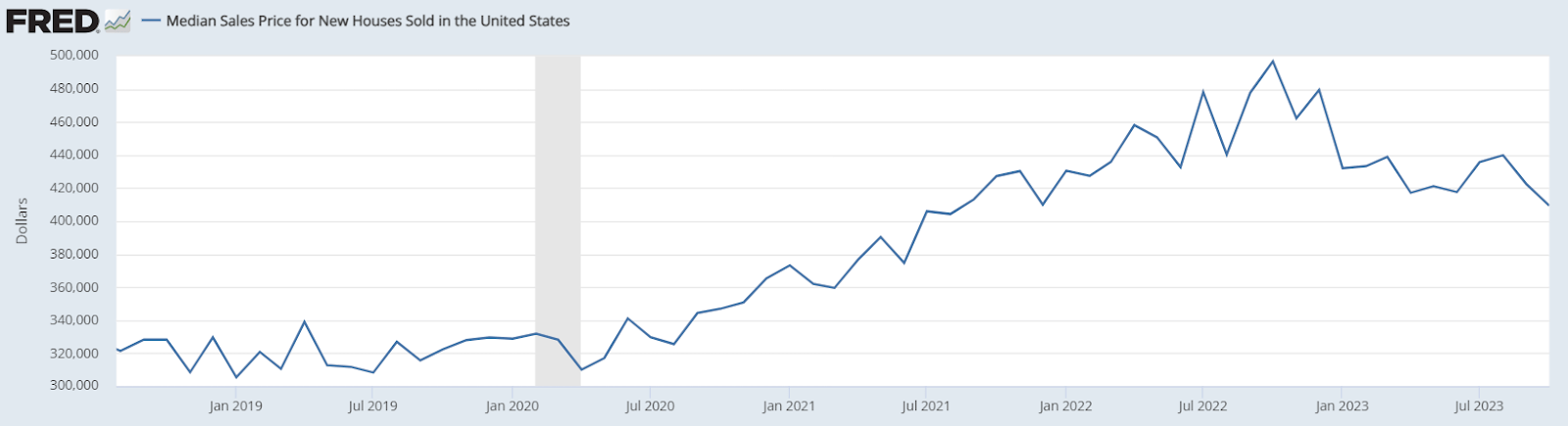

As a product of weak demand, house prices have finally capitulated; the median sales price for a new house is $409,300 , a decrease of $87,500 (-17.61 %) from last year's peak in October 2022.

{kind=link}

FRED

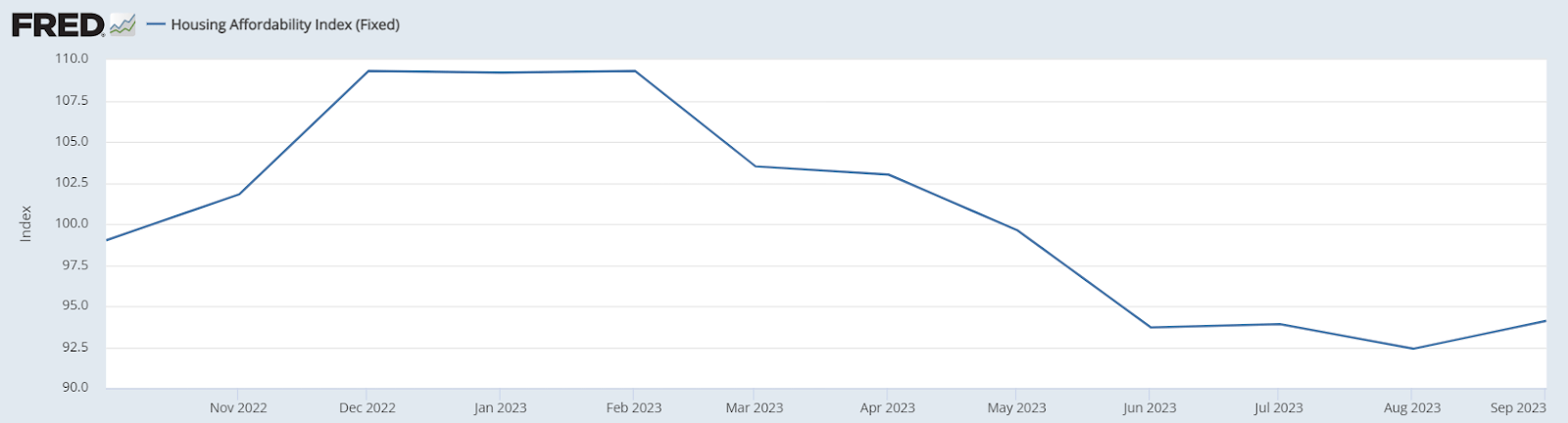

The price decrease has positively affected housing affordability, which dropped due to the high mortgage rates and the rapid increase in house prices. Seeing the Housing Affordability Index data, there was a shy recovery (in line with the recovery in mortgage applications) in September; however, affordability remains lower than 100, meaning that a family with a median income doesn’t qualify for a mortgage on a median-priced home. Hence, the median sales price is still unaffordable for more than half of the US population. Furthermore, according to the Emerging Trends in Real Estate (ETRE) report from PwC, consumers continue to adjust their budget due to inflationary pressures while feeling more financially unsecured (37% of respondents). The former has led home builders to adapt their product mix by offering smaller homes, finding innovative designs, and buying cheaper land; they also are offering mortgage rate buydowns that can reduce mortgage rates as much as 1.5%; moreover, homebuilders expect to keep using this incentive in 2024, however, if mortgage rates continue to rise, it could be too expensive for builders to keep offering them. For instance, a 1.5% buydown can decrease the mortgage amount by 6% at the current mortgage rate.

{kind=link}

FRED

Even so, buydowns are essential to keep demand in the current environment, as mortgage rates above 7% are not attractive for new home buyers, as illustrated in the ETRE. Especially now that consumers continue to cut some costs and the student debt is being repaid again.

PwC

Furthermore, following the ETRE, I expect high interest rates for a more extended period; the decade of free money seems to have ended, as inflationary pressures won’t be offset by deflationary pressures coming from global trade. Consequently, I don’t think mortgage rates will be as low as before.

Finally, it’s noteworthy that roughly 2 million households have been formed annually since 2019, thanks to many factors, such as large pandemic savings, low interest rates, and vigorous economic activity. Thus, given the robust demand, prices reacted with a considerable increase, larger than the inflation rate. Moreover, these increases were more intense in suburban areas thanks to adopting remote working. Also, new buyers valued the space of the house, as their homes became their new offices, increasing the price of new houses.

Nevertheless, the supply side couldn’t keep the pace of demand either in 2021 or the years after the Global Financial Crisis ((GFC)). The housing industry hasn’t recovered from its 2006 peak and is still far from doing so. Furthermore, the number of homes being constructed per 100,000 people remains extremely low compared to the decade before the GFC.

USA Facts

Hence, the National Association of Realtors estimates a home shortage of approximately 5.5 and 6.8 million that is expanding yearly. In addition to weaker construction activity, regulations related to the zoning and building codes have historically limited the construction of new homes. Another consequence of limited building activity is the aging of houses in the US, which is thought to be a critical tailwind for the remodeling market; however, I believe it’s also a very long-term tailwind for the housing industry, as few houses endure more than 90 years, as is illustrated by the following graph by Statista .

Statista

The number of homes built in 2022 was 1,390,500 , a 3.6% YoY growth; however, the number is too low compared to the estimated national shortage of housing units and the household formation in the last three years. In this sense, a crucial statistic to watch is the % of young adults who still live with their parents, 45% or about 23 million Americans, so the shortage of new housing units will likely widen and remain. From my perspective, the current supply problem is a growth opportunity for the industry as the demand still surpasses the supply, so homebuilders can increase their scale and be confident they will sell the additional units.

Nevertheless, homebuilders like DFH face competition from multifamily unit builders and modular and manufactured house companies. Multifamily units are an alternative to detached homes, as some multifamily buildings have more units in the same space than detached houses; thus, they are an alternative for high-density zones and could have lower prices as they are smaller. In this sense, manufactured homes, even if hated by many, are an important alternative to address the affordability problem; however, they face some limitations, such as a shorter useful life and underdeveloped secondary markets for their mortgages.

Competitive Landscape

The competitive landscape has changed recently as public homebuilders took market share from private and smaller homebuilders, especially after the GFC. Public homebuilders retain 41% of the market (measured by homes sold, not by dollar value).

PwC

Public homebuilders have greater financial resources (especially cash) to buy land and lots. In contrast, according to the ETRE, private homebuilders rely more on bank and private equity financing, which became more expensive after higher interest rates. Furthermore, small private homebuilders that don’t have a mortgage issuer subsidiary are playing at a critical disadvantage as they don’t have a complete offer for home buyers and have difficulties offering buydowns.

Large public homebuilders have economies of scale as: (a) they enjoy lower capital costs than private and small homebuilders (which are less diversified and have limited access to financial markets); (b) their larger scale allows them to obtain better prices for materials and subcontractors for land development; (c) they can spread out administrative expense over a greater amount of houses.

Nevertheless, according to JCHS of Harvard University , it’s unlikely that the homebuilding industry will become as concentrated as other industries owing to national scale benefits not translating into local scale benefits, as it’s hard to coordinate several independent operators under different regulations and environments; furthermore, homebuilders rely on local suppliers for material and local subcontractors for land development, so homebuilders’ buying power is only regional.

That’s why DR Horton and Lennar used acquisitions as their growth strategy rather than expanding to new markets, as they are difficult to penetrate due to incumbents’ local economies of scale. Similarly, DFH is using the same strategy to boost revenue. In consequence, I think the market will remain competitive; however, I see it improbable a public homebuilder will go bankrupt or be forced to abandon the market by competition, as they are diversified enough in different regions of the US and local scale benefits will make it hard for new entrants to take market share. Moreover, disruption threat seems unlikely. Additionally, in my opinion, the housing shortage will decrease the level of competition as the market continues to grow to address the scarcity of homes. Consequently, I think DFH will be able to maintain its high ROE.

Lastly, as DFH operates an asset-light model, it holds better inventory turnover than most competitors while having a healthier financial situation, allowing it to carry out expensive acquisitions. Moreover, as the capital is allocated more efficiently, DFH holds better returns for a lower risk than many other homebuilders who don’t apply this strategy.

Financial Performance

Despite the challenging environment in the housing industry, DFH managed to keep growing its sales in the last TTM, similar to PulteGroup ( PHM ), D.R. Horton ( DHI ), and Toll Brothers ( TOL ). However, other homebuilders have experienced a contraction in their sales, like NVR, Lennar ( LEN ), and KB Home ( KBH ). The case of DFH is unique, as the company has grown its sales by double-digit rates in the last three quarters, higher than PHM, DHI, and TOL. Even if the growth has decelerated, it continues to be high, especially in the current conditions.

Author's Elaboration with data from SA

The high growth rates in 2022 were due to the acquisition of McGuyer Homebuilders for $582.8 million (financed by debt, preferred stocks, and common stock issues). The company acquired represented 50% of the size of DFH.

In addition, along with higher revenue growth, DFH enhanced its profitability, as other homebuilders, thanks to shorter cycle time and cheaper raw materials. However, the buydowns and rising interest costs (capitalized in inventories) partially push the margin down, according to the ETRE.

Author's Elaboration with data from SA

Analyzing the net new orders and backlog in the last seven quarters, it seems the worst part is behind, as the net new orders are recovering from the troughs in 3Q22 and 4Q22. Moreover, although the backlog keeps falling, it appears to be stabilizing at around 5,000 thousand units with a total value of $2,410 million (64.96% of TTM sales).

Author's Elaboration with data from 10Q Reports

*Author’s Estimate

In this sense, the cancelation rate decreased in 2023 as mortgage rates stabilized and home buyers digested them. Thus, it seems the worst part is behind, as a weaker demand due to higher mortgage rates stabilizes, and the supply side remains tight and incapable of offering enough new homes.

Author's Elaboration with data from 10Q Reports

*Author’s Estimate

Furthermore, according to the ETRE, the investment prospects in single-family houses are expected to improve in 2024.

PwC

Unlike many other homebuilders, DFH's average sales price decreased slightly in the last quarter and remained higher than the national average. I believe the average sales price will eventually fall as the industry trends downward.

Author's Elaboration with data from 10Q Reports

*I couldn’t find 4Q22 data

Comparing DFH with its peers, DFH has been the fastest grower in the last five years, compounding its revenue by 44.95% annually and its operating profit by 70.39% annually. Of course, the larger scale of peers makes it harder for them to grow as fast as DFH; still, DFH growth is remarkable. I think the growth will slow. However, the housing shortage, the relatively small scale of DFH, and the opportunity for more acquisitions (~60% of the market remains in private homebuilders) will be solid tailwinds for future growth.

Author's Elaboration with data from QuickFS

Furthermore, DFH holds one of the highest ROEs in the industry. Nonetheless, the high ROE results from a high leverage ratio rather than a high ROA, which remains lower than the general industry.

Author's Elaboration with data from QuickFS

Author's Elaboration with data from QuickFS

The low ROA results from low profitability rather than low asset efficiency. DFH has an alarmingly low operating margin compared to its peers. Moreover, even if the DFH margin has increased, the gap has expanded after the pandemic. A possible explanation could be that the company focuses on growth rather than profitability. In the future, we could see a convergence, which may boost operating profit growth, in my opinion.

Author's Elaboration with data from QuickFS

Even so, when it comes to asset efficiency, DFH and NVR are the kings of the industry thanks to their asset-light business model based on controlling the land through options rather than owning the land.

Author's Elaboration with data from QuickFS

Even if DFH lags NVR, the former is better than its peers. In the DFH 2022 Shareholder Letter , the CEO and founder stated that applying a light-asset strategy is not as easy as one may think, as the company needs to develop healthy relationships with developers, land bankers, and land sellers, which takes more energy and effort than just purchasing the land. From my perspective, it’s a valid reason that can explain why many homebuilders still purchase lands instead of controlling them with options, even after the GFC forced them to carry out significant write-downs.

Lastly, I believe it’s worrisome how DFH has a thin operating margin while its houses are sold at a higher price than the national median sales price, as a rapid decrease in its prices (as it’s happening in the industry) could put downward pressure on margins. Furthermore, a price war could force DFH to endure losses in some markets. Still, I consider a national price war unlikely because every regional market has its dynamics, threats, opportunities, and competitors.

Risks

Competition

Not all national-scale benefits translate into local-scale benefits, so the competition keeps being regional, which allows smaller homebuilders to keep competing against big homebuilders, making the market highly competitive. Furthermore, DFH relies on relatively high financial leverage to maintain a high ROE with relatively thin profit margins, so tougher competition could put the company in a fragile financial position where it can only borrow at high-interest rates, which will further deteriorate its margins.

Economic Conditions

The housing market is susceptible to movement in interest rates and overall economic activities, as was noted during the last two years. I think the market has already surpassed the worst part of the crisis; however, predicting the economy with certainty is nearly impossible. Still, some indicators point out that the war against inflation is relaxing; even if inflation remains higher than the FED’s objective of 2%, more interest rates are unlikely to hike similar to what we saw a year ago. Furthermore, bond yields continue falling as the market adapts to an economy with lower inflation, which should put downward pressure on mortgage rates.

Weather Conditions

Bad weather conditions can increase cycle times and lead the company to assume some losses as the construction is delayed. DFH is well-diversified across many markets and plans to keep expanding, so I think the financial impact of this risk will be minimal.

Valuation

Given that the management expects to carry out new acquisitions and keep expanding in new markets, I think DFH has enough opportunities to keep employing capital, so I will assume that the firm won’t pay any dividends. Also, according to the 2022 Shareholder Letter , the management will seek to reduce its financial leverage, so to be conservative, I’ll be using the following ROE in my projection: a weak 2024 with 17.5%, 22.5% in 2025, 21.5% in 2026, and 20% in 2027 and 2028. Notably, these returns are far below the historical average of ~40%. In addition, given the industry's cyclical nature, higher financial leverage, and lower operating margins of DFH relative to its peers, I will use a discount rate of 16.75%. Finally, the terminal value will be a P/E of 12, far lower than the historical P/E ratios of NVR (which has a similar business model), given that DFH still performs poorly, and I’ll assume an EPS of $2.55 in 2023 following analysts.

Author's Elaboration

Given the premises, DFH shares are undervalued and offer a margin of safety equal to 30%, giving enough downside protections. Furthermore, the premises are pretty conservative, in my opinion; consequently, I think DFH is a ‘Buy.’

Conclusion

In conclusion, Dream Finders Homes is a promising homebuilder in the US with a trusted brand and an asset-light business model. Despite the challenges posed by the industry's cyclical nature and tough competition, DFH has maintained a high ROE and is seeking to reduce its financial leverage. Based on conservative projections and a discount rate of 16.75%, DFH shares are undervalued and offer a margin of safety equal to 30%. Therefore, I recommend buying DFH shares, which provide significant upside potential and downside protection.

For further details see:

Dream Finders Homes: A Promising Investment Opportunity In The U.S. Homebuilding Industry