DFH - Dream Finders Homes: Getting Cheaper

Summary

- Dream Finders Homes has taken quite a tumble in recent months, even as sales and cash flows rise materially.

- This may be perplexing to some investors, but leading indicators show that pain lies ahead.

- For now, the company is looking more interesting than it did previously, but it's not cheap enough to warrant an upgrade.

To many investors, the home building space is more or less off-limits at this point in time. Significant inflationary pressures pushed home prices higher and rising interest rates aimed at offsetting inflation are now set to make borrowing more expensive and to reduce the demand for homes, all else being the same. Naturally, this will all have a negative impact for the companies that operate in this space. But this doesn't mean that investors shouldn't be looking for opportunities here. The fact of the matter is that shares of many of the companies in the home building market look incredibly cheap at this point in time. One interesting prospect to consider is Dream Finders Homes ( DFH ), an enterprise that specializes in building homes in high-growth markets like Charlotte, Raleigh, Jacksonville, Orlando, and other locations. In recent months, shares of the company have taken a beating as cancellation rates of home buyers have risen and as net new orders shrink. That pain is likely to increase from here. At this moment, shares of the company are looking to be more appealing though from a fundamental perspective. And as such, I've decided to increase my rating on the company from a ‘hold’ to a soft ‘buy’ to reflect my view that it is likely to outperform the broader market for the foreseeable future.

Building wealth for your portfolio

Back in the middle of August of 2022, I wrote an article discussing the investment worthiness of Dream Finders Homes. In that article, I talked about how exceptionally robust the company's performance had been in the prior years. Top line and bottom line performance continued throughout much of the 2022 fiscal year and backlog data for the company was promising. Shares of the company were also cheap. On the other hand, however, it was showing some signs of weakness that I felt would likely continue for the foreseeable future. Although I recognize that the future for the company is not going to be as bright as its recent past has been, I felt as though shares were priced low enough to at least avoid a bearish rating. But because of how the stock was priced and because of the uncertainty associated with the market, I ultimately rated the company a ‘hold’ to reflect my view that shares should generate upside or downside more or less in line with what the S&P 500 should. Since then, the market has been considerably more bearish than I have been. While the S&P 500 is down 5.5%, shares of Dream Finders Homes have generated a loss of 12%.

{kind=link}

Author - SEC EDGAR Data

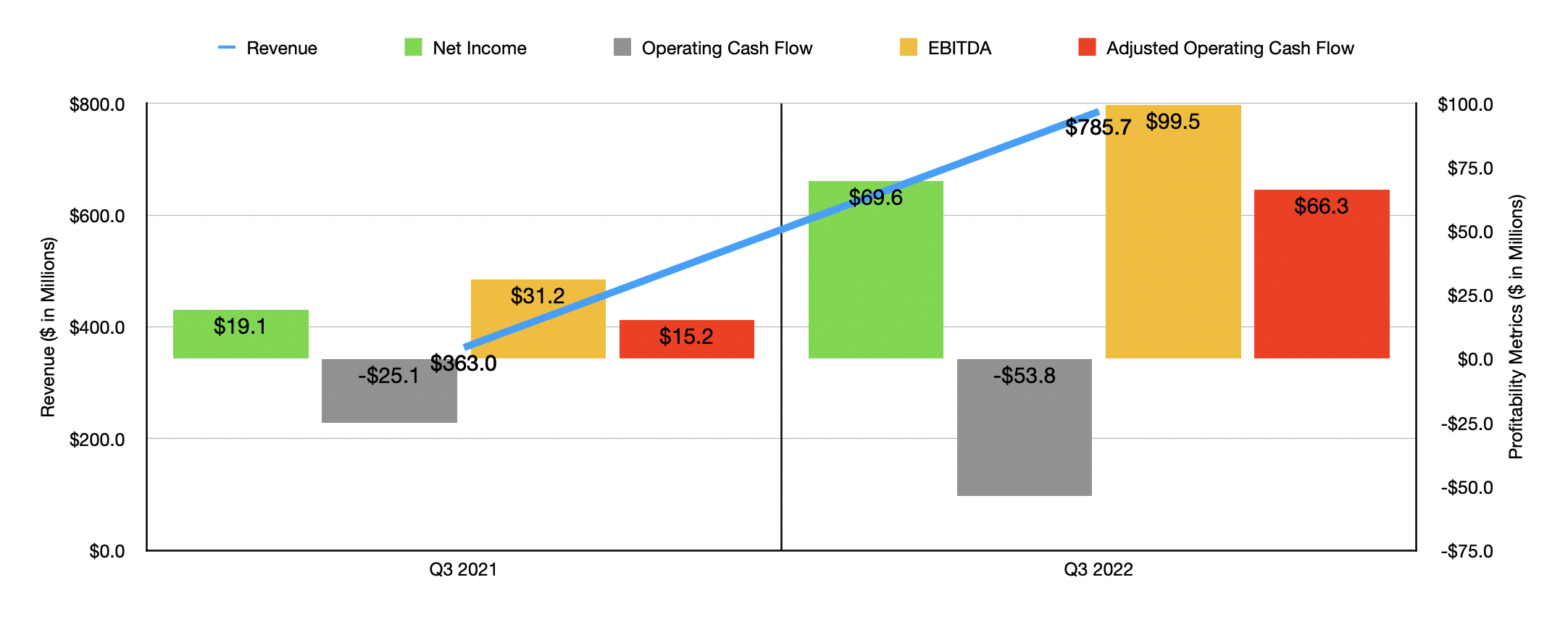

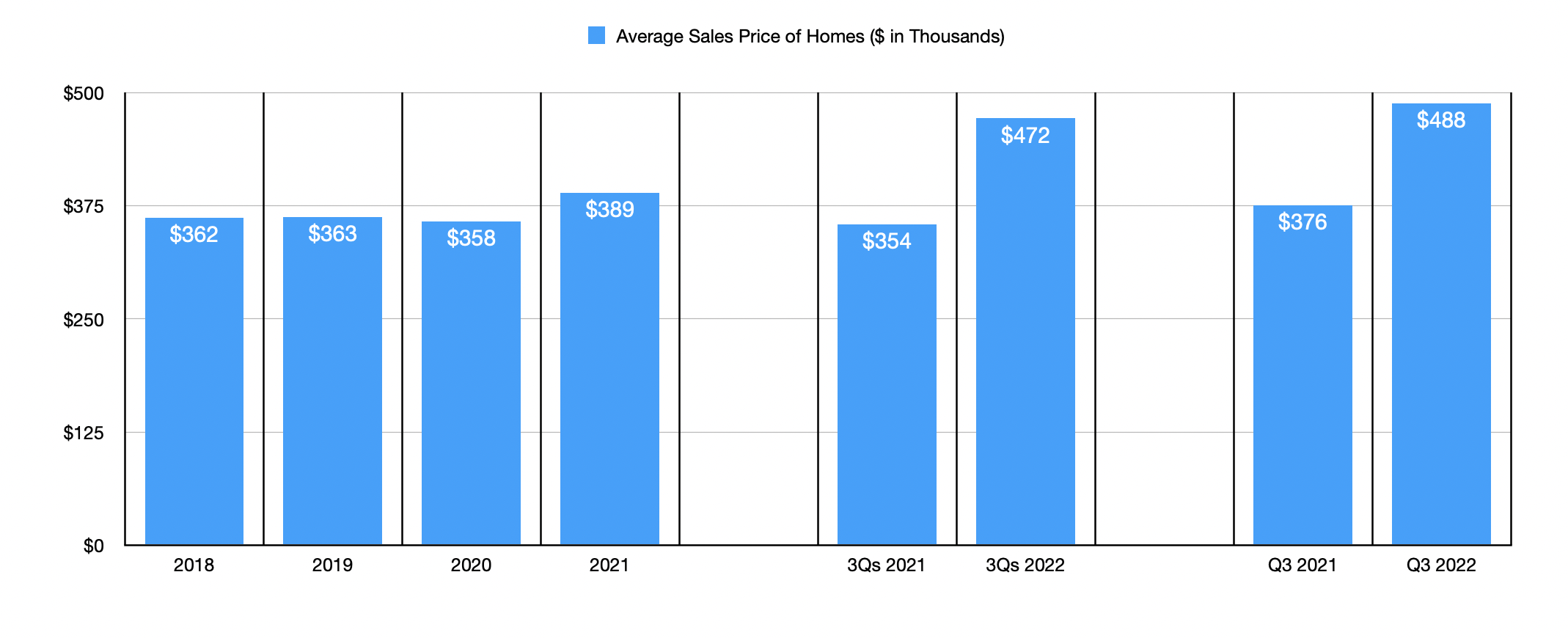

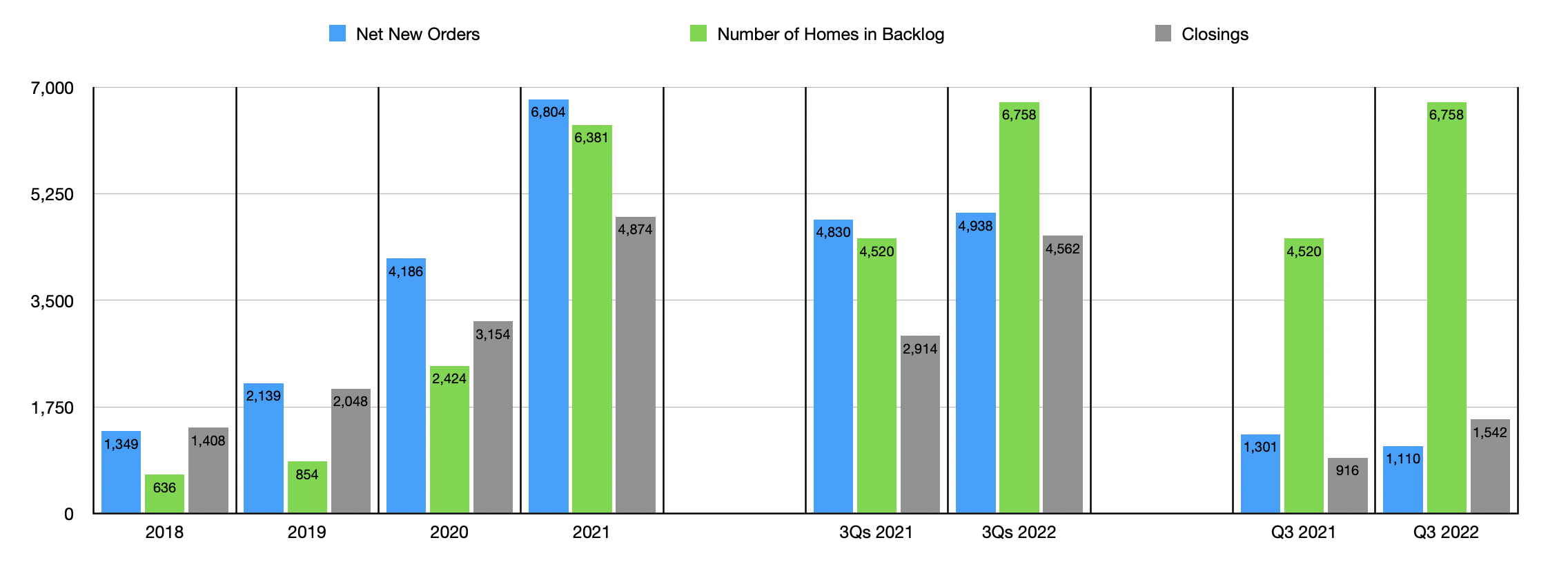

For those looking at just the headline numbers, it may be perplexing why shares are down so much relative to the market. Consider, for instance, data covering the third quarter of the company's 2022 fiscal year. Sales for that time came in at $785.7 million. That's significantly higher than the $363 million reported one year earlier. This surge in revenue came as the number of closings for the company shot up from 916 to 1,542. The company also benefited from an increase in the average price of a closing from $375,693 to $487,852. On top of this, overall backlog totaled 6,758 properties. That stacks up favorably against the 4,520 properties reported in backlog one year earlier.

{kind=link}

Author - SEC EDGAR Data

{kind=link}

Author - SEC EDGAR Data

{kind=link}

Author - SEC EDGAR Data

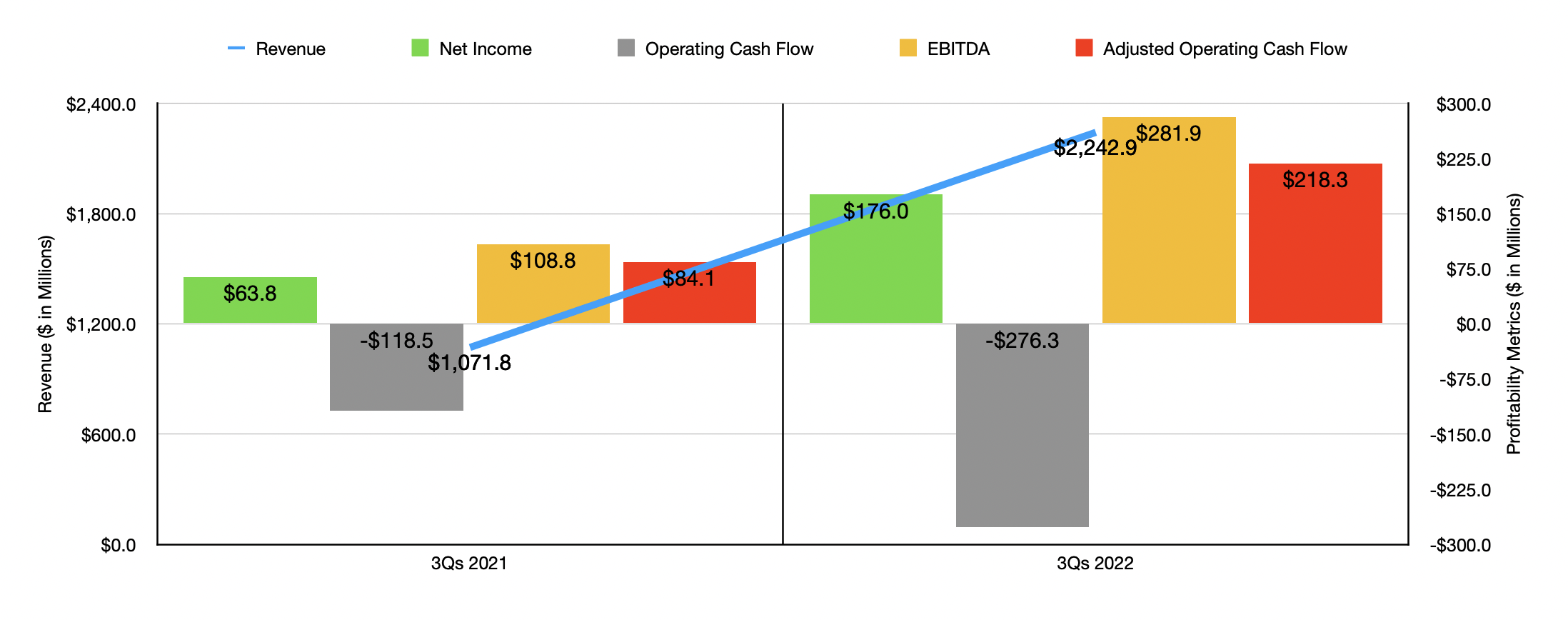

The company also boasted strong results on the bottom line. Net income of $69.6 million dwarfed the $19.1 million reported one year earlier. Although operating cash flow went from negative $25.1 million to negative $53.8 million, that picture changes considerably if we adjust for changes in working capital. On this basis, the metric rose from $15.2 million to $66.3 million. Meanwhile, EBITDA more than tripled from $31.2 million to $99.5 million. By all accounts, things should be going great for the company. This is especially true when you consider that the third quarter was not the only strong quarter for the company. For the first nine months of 2022 as a whole, revenue came out to $2.24 billion. That's more than double the $1.07 billion reported one year earlier. Net income shot up from $63.8 million to $176 million. Operating cash flow went from negative $118.5 million to negative $276.3 million. But on an adjusted basis, it shot up from $84.1 million to $218.3 million. And finally, EBITDA for the enterprise rose from $108.8 million to $281.9 million.

{kind=link}

Author - SEC EDGAR Data

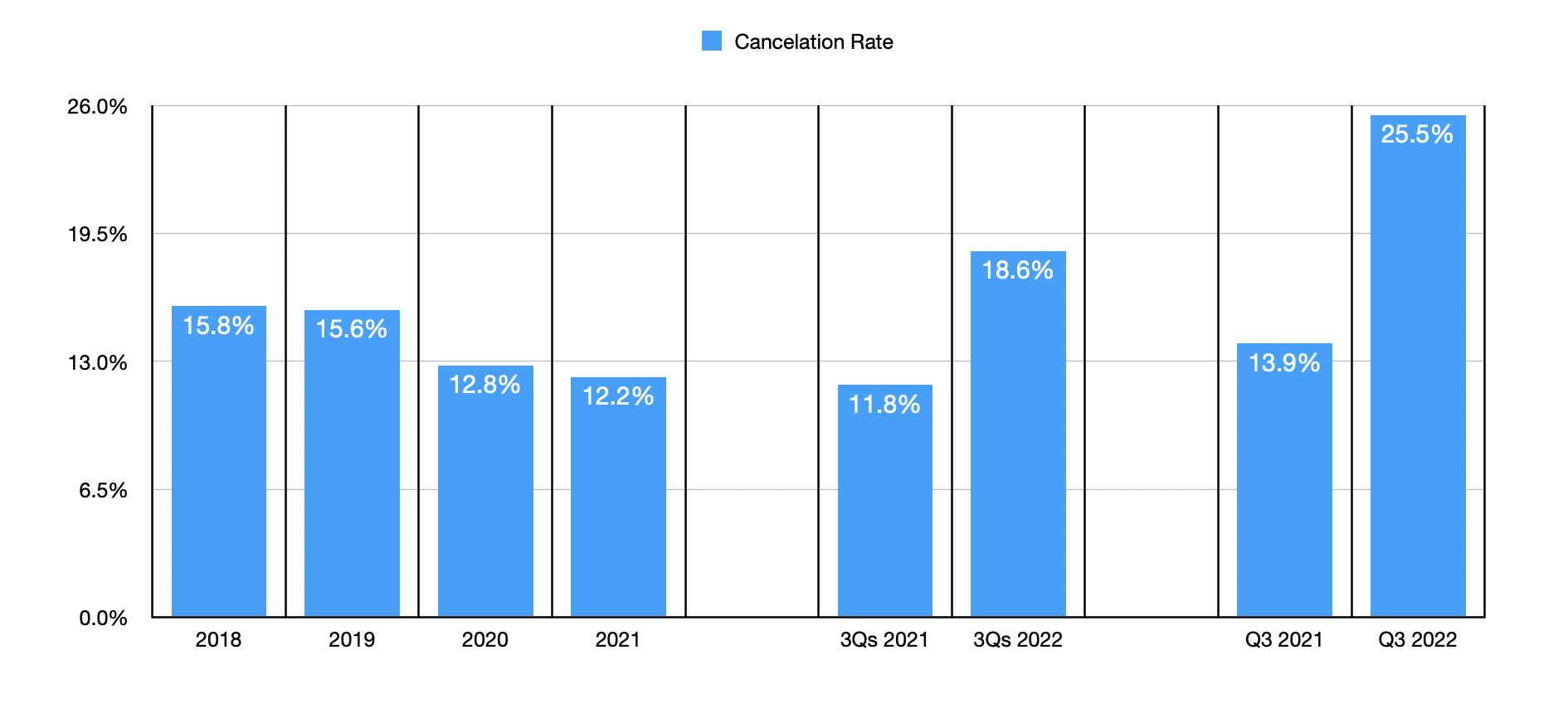

The real trouble for the company comes not from its historical performance data or anything else of that nature. Instead, it comes from two particular metrics. The first of these would be net new orders. Net new orders represent the number of new orders the company has for properties net of any order cancellations. If this number increases, that means the backlog will grow and both revenue and cash flow should grow over time. And if it shrinks, the opposite should occur. For the first nine months of 2022, this number came in at 4,938. That's a slight increase over the 4,830 reported for the first nine months of 2021. But when you look at the third quarter alone, the 1,110 reported was lower than the 1,301 experienced the same time one year earlier. In addition to this, the company also reported a rise in its cancellation rate. This is the percent of orders that are ultimately canceled by customers. For the first nine months of 2021, this totaled 11.8%. For the first nine months of 2022, that number had risen to 18.6%. Unfortunately, the trend is getting even worse. For the third quarter of 2021, the number came out to 13.9%. In the third quarter of 2022, it was an astounding 25.5%.

{kind=link}

Author - SEC EDGAR Data

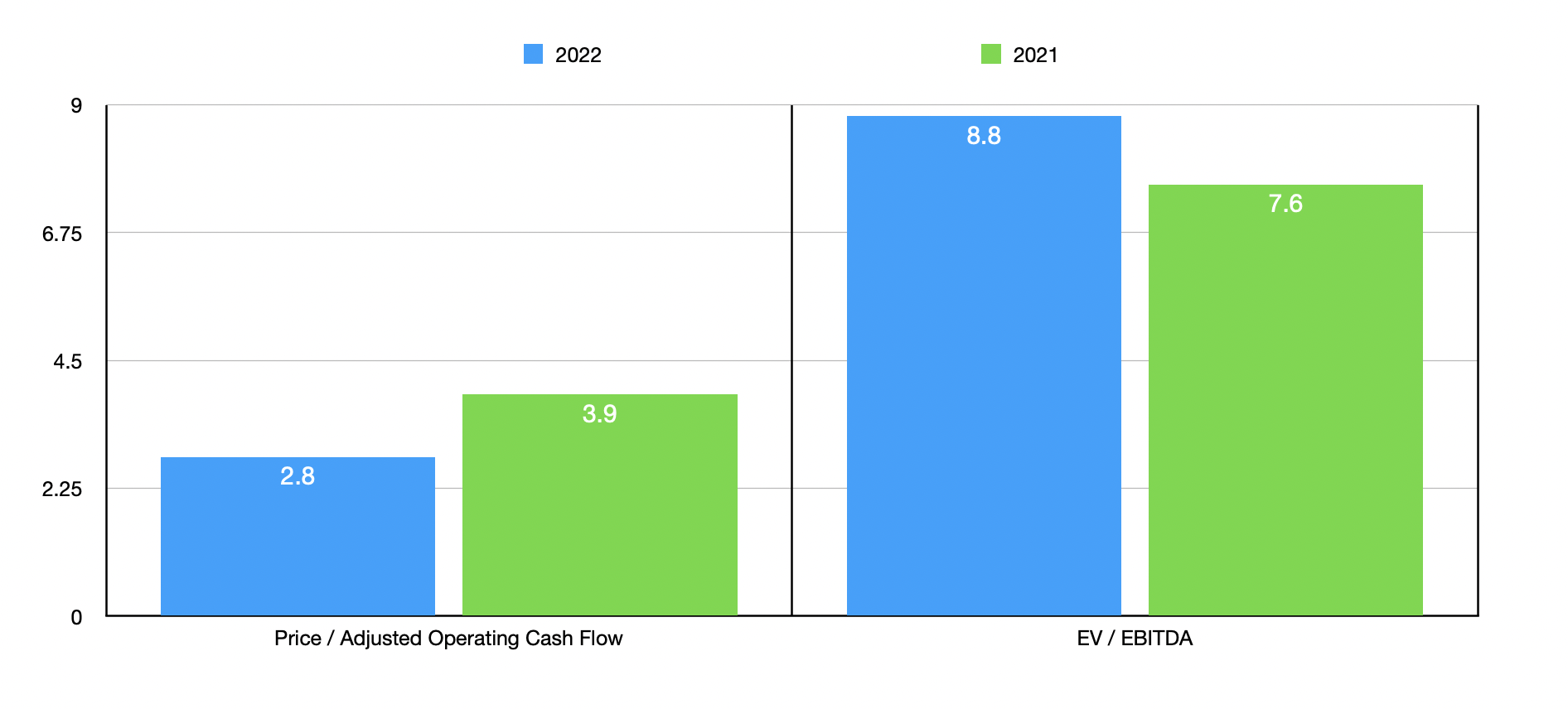

When it comes to valuing the company, I did decide to take the data from the first nine months of 2022 and annualize it. Doing this, we would expect net income for the year of $295.4 million, adjusted operating cash flow of $383.9 million, and EBITDA of $522.1 million. Based on these figures, the company would be trading at a price-to-earnings multiple of 3.7, a price to adjusted operating cash flow multiple of 2.8, and an EV to EBITDA multiple of 3.9. This is incredibly cheap. But with the decline in net new orders and the fact that the trend there is worsening, it's very likely that the company's fundamental performance will eventually worsen. Because of this, I also decided to value the company based on data from 2020 and 2021. As you can see in the chart above, the firm does look much cheaper using the 2022 data than if we were to use data from either of those years. But even in the event that financial performance was to revert back to what it was in 2020, you would be hard-pressed to say that the company is overpriced. As part of my analysis of the company, I also compared it to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 2.2 to a high of 5. Three of the five firms were cheaper than our prospect. Using the price to operating cash flow approach, the range was from 6 to 504.8, with our target being the cheapest of the four firms with positive results. And finally, using the EV to EBITDA approach, the range was from 3.9 to 5. In this scenario, Dream Finders Homes was tied as the cheapest of the group.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Dream Finders Homes |

| 3.7 |

| 2.8 |

| 3.9 |

| M/l Homes ( MHO ) |

| 3.6 |

| 504.8 |

| 3.9 |

| Green Brick Partners ( GRBK ) |

| 5.0 |

| 27.8 |

| 5.0 |

| Century Communities ( CCS ) |

| 3.4 |

| N/A |

| 4.0 |

| Beazer Homes USA ( BZH ) |

| 2.2 |

| 6.0 |

| 4.4 |

| Tri Pointe Homes ( TPH ) |

| 4.4 |

| 66.2 |

| 4.6 |

Takeaway

When it comes to companies that are highly reliant on things like interest rates and inflation, it's important to look at the leading indicators or else you risk buying into a business that's at the tipping point between improving fundamentals and deteriorating fundamentals. Clearly, Dream Finders Homes is starting to see some worsening and that trend is almost certain to continue for the foreseeable future. This does not mean, however, that the company makes for a bad prospect. Given how much the stock has fallen, I am definitely more drawn to it now than I was previously. However, I don't think the stock is quite cheap enough yet given the high cancellation rates we are seeing and the weakening net new orders. But if the stock falls much further from here, I could see myself eventually upgrading it.

For further details see:

Dream Finders Homes: Getting Cheaper