PTEN - Dril-Quip: Ready For Liftoff

2023-11-24 08:00:00 ET

Summary

- Dril-Quip, Inc. is a company focused on complementary operations and sales items in deepwater, carbon capture, and offshore wind farms.

- The company's stock is at a recent low after missing on the bottom line in the recent quarter.

- Dril-Quip has a long runway for growth and may be a buy at current levels, especially if there is a major upcycle in offshore operations that we anticipate.

- We are calling a buy on Dril-Quip, Inc. at current levels for risk-tolerant investors.

Introduction

We haven't written up Dril-Quip, Inc. (DRQ) previously, and that's a regrettable oversight on our part. It's a company with which I used to be very familiar due to their focus on deepwater connectors and liner hangers...the bits and bobs that make deepwater operations possible.

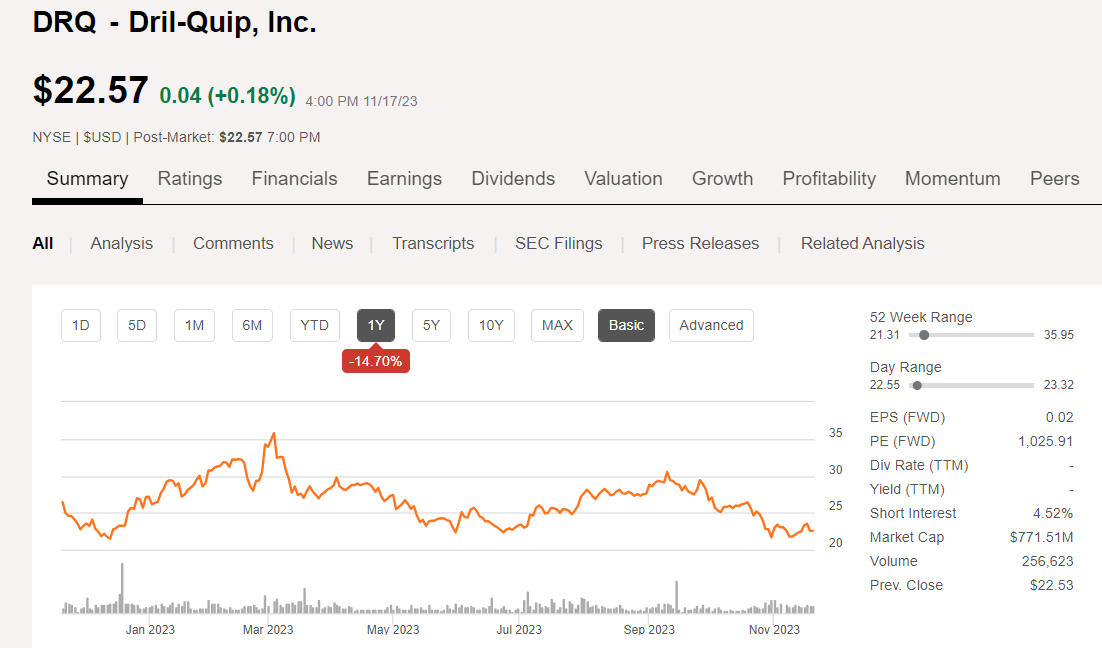

DRQ price chart (Seeking Alpha)

{kind=link}

DRQ is at a recent low after missing on the bottom line in the recent quarter, due to factors beyond its control.

The company is thinly covered by the seagulls, with only four following the stock. There is one buy, one hold, and two sells on DRQ among this worthy crew , resulting in an Underweight rating - the first one I've seen. It's hard not to chuckle at the price targets that generate this rating. They range from a low of $23 and a high of $44.00. The median is $25, suggesting three out of the four of this intrepid bunch of prognosticators don't see a lot of upside.

Here's the thing. If we are indeed in for a major upcycle in offshore, particularly deepwater, DRQ is a buy right now. I believe we are headed toward better days in this category. The major OSD companies are nearing a half million a day for 7th gen drillships, and claim fixtures are extremely tight in this ultra-capable category. In that scenario, DRQ should prosper if operators hold to their investment plans in the new year.

The thesis for DRQ

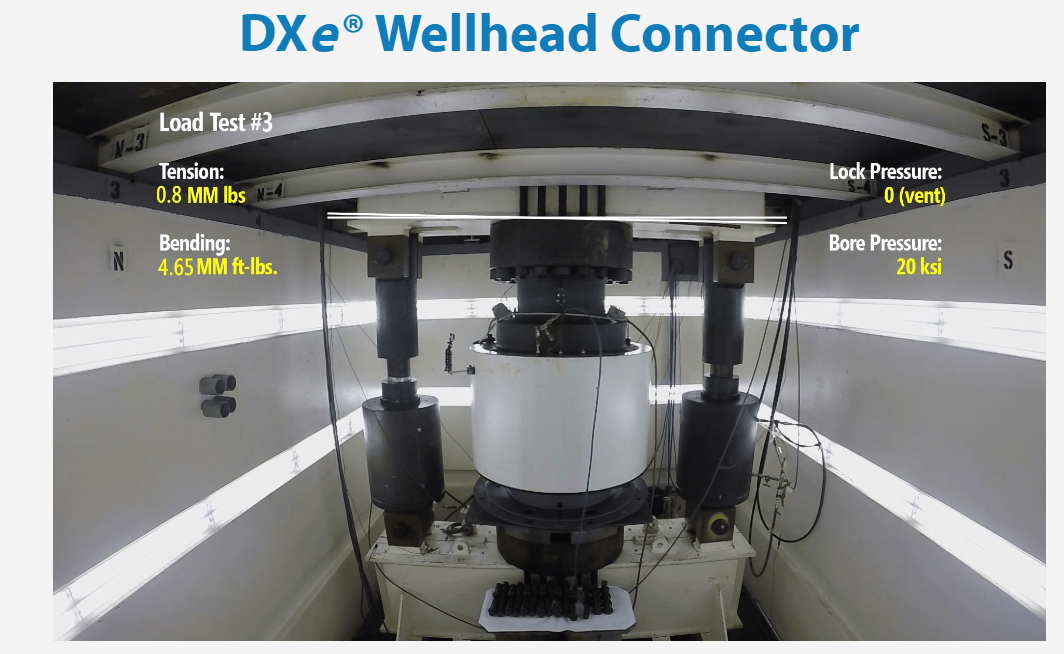

Dril-Quip is good at the little stuff that doesn't make the cut in bigger companies. I know them from working in deepwater and relying on DRQ connectors to latch up the riser with the subsea wellhead. Here is a picture of premium DRQ wellhead connector. This may not seem like much to you. Let...

{kind=link}

me describe the challenge. Imagine you are trying to locate a fishing weight into a coffee cup from a height of-heck, let's use 200'. Imagine also that the wind is blowing 3-5 mph and the weight begins to gyrate as the line plays out. How much success do you suppose you will have landing out in the coffee cup? Un-hunh.

Now, this is not a perfect analogy. In the case of a wellhead connector we are attached to a marine riser that's a heck of a lot more stable than a fishing line. But still, there are currents that must be dealt with to successfully latch up. We must also mention that this task is aided by subsea robots known as Remotely Operated Vehicles-ROV's , without which the task would be impossible. Your takeaway here is that the experience and product quality that DRQ is known for, and is a definite asset to their performance in a supportive market.

Risers, Wellheads, Liner hangers are other DRQ specialties. ( Have a look at their products page for more entries .)

Wrapping this up, DRQ is also making inroads into related offshore industries, FPSO hook ups, wind farms-although this may turn into a flash in the pan , and carbon capture initiatives that will use many of the same skillsets that deepwater operations require.

In short, DRQ has a long runway and may be a buy at current levels.

DRQ's Q3 2023 and guidance

Q3 revenue came in at $117.2 million, an increase of 33% year-over-year and 31% sequentially, driven by strong organic growth of 11% sequentially, led by Subsea Products and with the addition of Great North , which added another 17% or $15.5 million Q-on-Q.

Subsea Products revenue increased 15% compared to the prior year and 25% sequentially, which was driven by the delivery of certain customer milestones in the quarter in Europe. Subsea Services revenue increased 6% year-over-year and was up 3% sequentially. This segment was expected to grow double digits sequentially, but, rig availability for certain customers has moved drilling schedules to the right.

Increased activity in Brazil offset some weather and customer schedule delays in the Gulf of Mexico and Asia Pacific.

The Well Construction segment grew 117% year-over-year and 76% sequentially, reflecting the addition of Great North and activity increases in Latin America, Saudi Arabia, Brazil and West Africa.

Gross margins during the second quarter were 27%, up approximately 150 basis points year-over-year. The improvement in gross margin is largely due to the addition of Great North and the ongoing initiatives across the organization to drive operational efficiency.

Adjusted EBITDA for the quarter was $12.4 million, an increase of $5.3 million from 1 year ago and up $3.6 million sequentially. OCF was $26.8 million in the third quarter, an improvement of $15.5 million sequentially and $26 million from the prior year. Free cash flow for the third quarter came in at a positive $21.4 million, which is our second consecutive quarter of positive free cash flow and the highest figure since 2017.

Inventory was a consumed cash in the period as they continue to stage materials in anticipation of upcoming growth. CapEx in the third quarter was $5.4 million, largely driven by rental tools bound for work already secured. $86 million in the quarter was used to complete the acquisition of Great North,.

Ending cash, cash equivalents and investments were $190 million at quarter end. The company has ample liquidity to fund operations and to evaluate incremental high return capital allocation opportunities

Guidance for Q4

DRQ expects fourth quarter revenue to be in the range of $115 million to $125 million. Fourth quarter bookings are expected to be in the range of $75 million to $100 million. The top end of that range includes 6 subsea trees, comprising over $50 million in potential bookings in the fourth quarter.

In summary, Q3 results were below expectations largely due to rig delays, which had a direct impact on revenue mix, which impacted profitability. Heading into Q4, DRQ expects a strong revenue ramp with a full quarter of Great North and sequential growth in the higher-margin Subsea Services business. CRQ expects Q4 to be a solid free cash flow quarter to close out the year, with cash builds pumping up an already clean balance sheet.

Source .

Risks to the thesis

The obvious risk is commodity prices, which have been subjected to a "push me, pull you" effect in Q4, and trending down. This is at just at the time E&P's are firming up capital budgets, and too much time in the $70's for WTI (CL1:COM) could convince them to delay projects in search of quicker paybacks on ROCE.

Your takeaway

Dril-Quip, Inc. is a pure play on oilfield-mostly offshore activity building and working on existing wells. The company is in an enviable position generating nearly $100 mm in cash from operations on a Q3 results-NTM basis, and no LT debt.

The EV/OCF multiple is 7.5X, which should improve still further as Jeff Bird, CEO noted in the Q3 call:

Dril-Quip is set up to enter 2024 with a strengthened foundation and ability to capitalize on the growth of a continuing upcycle. While there may be some near-term product mix challenges that we will navigate as our customers refine their drilling schedules, we are confident in our ability to provide long-term profitable return on capital.

The company is trading in a sideways channel pattern now between $22-23.50, after bouncing off resistance at $22.00, and is well below its 200 Day SMA. Clearly a victim of the current downward volatility in oil prices. What price should it trade for in a less volatile market?

Contract driller Patterson-UTI Energy (PTEN) is trading at 11X EV/OCF, and OSD Valaris Limited (VAL) is trading at 30X EV/OCF. Perhaps a better comparison is with Oceaneering International (OII) - a company we will write up soon , now trading at 5.5X OCF. OII has a strong balance sheet , with enough cash on the books to pay off its long-term debt if it chose to do so.

If we give DRQ a 10X multiple, the shares should support a $30 price tag. That doesn't seem unreasonable given that it was just there in September, and in the past nine months shares have traded above $35!

I think investors looking for growth in the coming year may find Dril-Quip, Inc. shares attractive at current prices.

For further details see:

Dril-Quip: Ready For Liftoff