DD - DuPont: A 40% RoR Since October But The Upside Is Now Smaller

2023-08-30 12:00:00 ET

Summary

- DuPont's investment in the fall of '22 has paid off, doubling the market and showing good growth in key segments.

- The company's growth pillars and attractive operating segments make it a strong player in the industry.

- However, the company's valuation is no longer as attractive, and caution should be exercised when considering an investment.

Dear readers/followers,

To say that DuPont de Nemours ( DD ) was cheap in the fall of -22 would be an understatement. However, many companies were cheap back then, which is why I did unfortunately not add much. There were plenty of good companies on sale at the time, and while I bought DD, I also bought plenty of other cheap companies in greater amounts. So, I'm very happy to report that my "bet" taken with DuPont paid off in spades. It's doubled the market in the meantime, and this is always a bit of a feather in the cap for any value-oriented investor...

Seeking Alpha DuPont (Seeking Alpha)

But at the same time, a position is only as good as its size when it comes to counting returns. And this massive RoR compared to the market won't really make a massive difference, unfortunately, given my relatively limited size of the overall stake.

Still, it's enough for where I am now providing an update on the investment and giving you my take on where DD is moving on a forward basis.

DuPont - Plenty to like about a storied company, despite the issues.

It's clear that the company is in the midst of its transformation, even now - though much of what you see below is now done.

DD IR (DD IR)

The company's growth pillars are working well - and the company's operating segments are some of the most attractive in the industry, with a nice sales split between Electronics (the largest), Water, Protection, Industrial Tech, and Next Gen Automotive.

The company also remains one of the better chemical companies in terms of margins. DD has a gross margin level of 35%, EBIT at 15%+, and a very attractive overall net margin. It's not the best company in the industry when it comes to cash, debt, or interest coverage, but it "works".

It shouldn't be a surprise to you, or to anyone, that after a 40%+ RoR in less than a year, this could make a company materially less attractive. That is definitely the case for DD. The company is from a perspective of fundamentals and historicals potentially still buyable, but materially less attractive -more on that in a while.

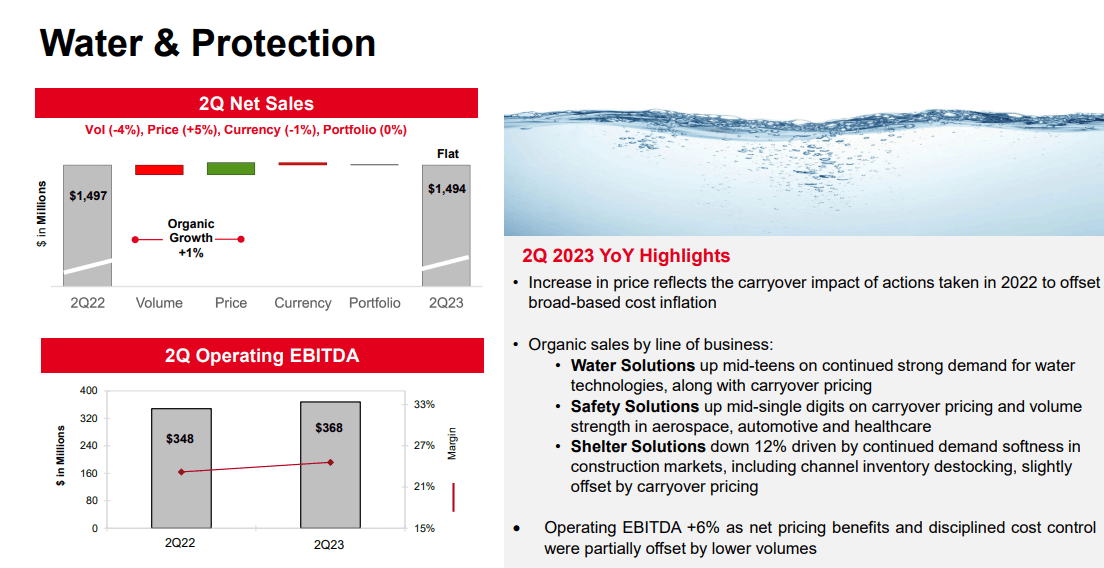

Results first. We have 2Q23 results in August, and those are decent. Top-line organic sales decline was expected due to volume pressures and macro, but the company reported sales increase in key attractive segments - such as water, interconnect, and other end markets. In essence, if it's not electronics, it went fairly well. Because Electronics was poor.

This also led to a decline in company EBITDA on an operating level, based on lower margins (not weighed up by pricing) and lower production rates.

Overall, execution was decent in a difficult environment. This is the picture most of the chemical companies currently convey to investors, and it's basically "the truth" here.

DD-specific trends include key M&As, such as the completed Spectrum Plastics M&A, and the company I am integrating that. The importance here is due to the fact that we're seeing the total revenue in high-growth healthcare to 10% of the total portfolio. Also, the company's Delrin divestiture is still expected to close in this fiscal.

Part of the company's share price appreciation is certainly its buybacks. DD has bought back almost $5B worth of shares until November of 2023.

Also, one of the more significant trends for the company in terms of liability has been the water district settlement regarding PFAS claims. This was done in June, and obviously, this took some stress from not only DuPont but from Corteva and from Chemours ( CC ) as well.

{kind=link}

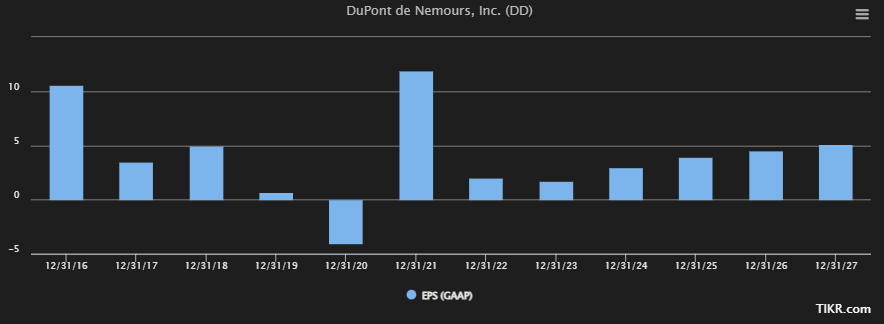

Earnings trends/EPS bridge are not in any way poor, but the trends there reflect the trends in other chemical companies of the macro environment. We're seeing negatives from volumes in electronics/construction, which are sectors that are currently very volatile.

Growth for DuPont comes from a few sources, as we move forward into 2024 and beyond. The company, of course, can push prices through its market-leading position in key markets, and it has - but this is not enough.

Aside from this, the company also has one of the leanest cost structures in the entire industry, coming in at less than <1% of annual revenues, and the management team that pushes DD is one of the best in the industrial sector.

So, we're already in a good position, and while this quarter doesn't show massive improvements, it also doesn't show massive declines. You have to look at the segments that are growing to see some of the upside - especially where we're growing EBITDA faster than top-line.

{kind=link}

The company has also provided 3Q and FY Guidance, with the expectation being steady demand in most key segments and a full-year adjusted EPS of around $3.5/share, moderated down from around $3.7/share. This is not that meaningful an adjustment given the GAAP trends we're looking at. Namely, we're looking at GAAP EPS growth.

{kind=link}

Even if only a part of this, or the very trend materializes, we're still talking about significant improvement from an otherwise impairment/liability-riddled recent past. DD isn't a yield monster, and that yield has even dropped below 2% since I started investing, which needs to be highlighted here - but growth is still possible, if we look at these trends.

Debt is still favorable - below $12B, with very good overall maturities, most of it well beyond 2024, and over 80% of it is long-term with much of it at fixed rates. Cleanup work, which I referenced in my last article, found here, is still something DD needs to work with - but the company has just in the course of a year come quite a distance.

What to look at for DuPont here, I would consider ensuring that no single segment crashes in terms of margins. It's the same thing I look for in the rest of the basic materials sector. If things turn sour on a macro level, some of these names which include DD, could see fundamental deterioration- and this is now more likely given the levels we're currently at.

DuPont isn't the best or cheapest chemicals company anymore. It was about a year ago - that's why I invested in it. Today though, I would be more careful making any such assertion.

DuPont, in the end, is a great business despite many of its issues we've seen and the controversial involvements in a whole lot of subjects, including PFAS. But on the whole it, the company is leveraged no more than 23.48% of LT debt/Cap, and this makes it one of the best names in the industry. It also comes in at BBB+, and while the forecast accuracy for this company leaves things to be desired, there is an upside to be had here.

Just not enough.

DuPont - only Premiumization makes the case for an investment here.

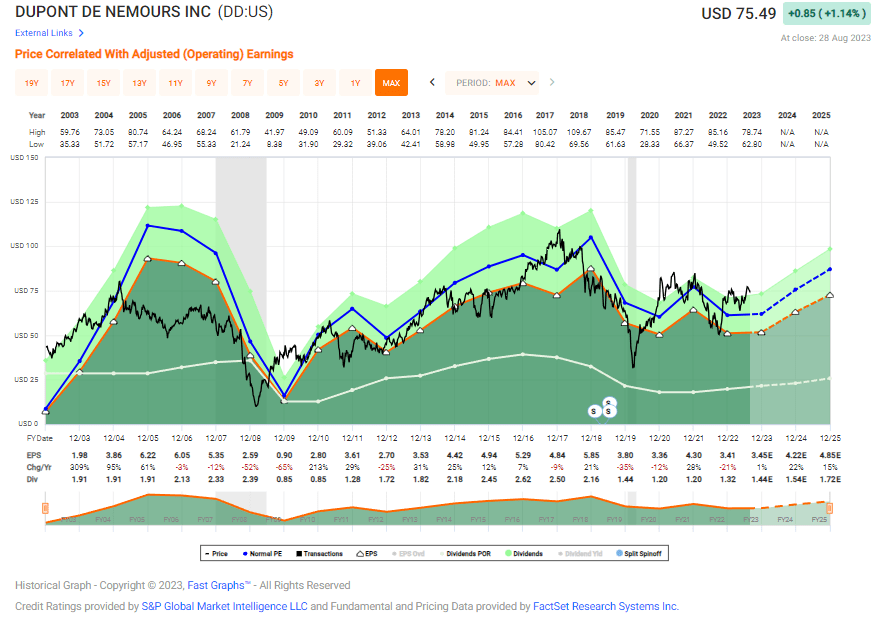

When I bought the company, it traded at below 15x P/E. That was a superb level to buy DuPont. That this company is volatile needs only a short illustration.

{kind=link}

Everything you see here highlights the importance of considering valuation. The company tendentially does crash back down when going too high, though usually in the case of revised guidance or less earnings. Going forward, I expect the volatility of DD to somewhat lessen.

In my original article, I gave the company a PT of $85/share. This would imply that the company is still a "BUY" here, but I want to be very clear that I am no longer buying the company . The reason, despite an upside of double digits, is that those double digits are based on a premiumized valuation.

In order to get double digits from DD here, you need to at least expect for the company to trade at 19-20x P/E. At 19x, the company has a return of 11.3% per year based on current estimates, of 28.5% in total RoR. Compared to most other chemical companies and basic materials businesses, this means that DD would trade at close to twice their multiples, and that is not a level I consider even close to relevant or fair value here.

The most I would give the company is around 16-17x P/E, which would put us below 8% per year, or well below my current return demands.

What I look for is a 15% annualized rate of return, and that's only possible at above 21x P/E for this company - a level I would put no basic materials company at.

Because of this, I believe sector valuation trends will eventually cause the multiple to compress here, resulting in a better entry. Or if not, it results at least in not as low an upside as we're currently seeing.

The fact is, because the upside to any fair value is so poor here, I'm electing to lower my price target to $80/share based on future prospects and may look at alternatives here. This might seem harsh - but in this environment, I don't want to sit on anything that's expected to perform less than what I expect. The saving grace for this company and why I haven't acted yet is safety. BBB+ and the company's operations mean that any fundamental deterioration here is unlikely.

But with S&P Global analysts averaging a PT of $81/share from $49 to $95/share range, and only 7 out of 18 analysts still at a "BUY", we can see why some are now less certain about how much upside there is left in this business.

I say the combined upside of optimization, divestments, buybacks, and positive quality still justifies holding on for now - but I'll likely revisit the topic towards the end of the year when it's time to look at portfolio rebalancing.

For now, I'm still at a "BUY" - it's double digits, but that's only possible with some premiumization, or expecting the company to outperform.

I did for a long time consider a rating change but won't do it now - I may however do so in the next article.

Questions?

Let me know!

Thesis

My thesis for DuPont is as follows:

- Chemicals/Industrials are still an investable segment, and I continue to invest major capital in businesses such as BASF (BASFY), Linde (LIN), L'Air Liquide (AIQUY), LyondellBasell (LYB), Covestro (COVTY), and others.

- The company combines the appeal of specialty chemicals with a great market position, excellent fundamentals, and a yield that could double in less than 5 years if the company's growth plan remains intact. I also like the pricing the market is giving some of the options for the company here, which is why I might go for some of them.

- I give DuPont a "BUY" with a PT of $80/share for the longer term, legitimizing some of the company's premium that we see here, but not as much as in my previous article. This is a price downgrade, but not a rating downgrade for the time being.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them.

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

For further details see:

DuPont: A 40% RoR Since October, But The Upside Is Now Smaller