DD - DuPont: Less Future Potential (Rating Downgrade)

2024-01-18 04:23:06 ET

Summary

- DuPont has solid execution potential with good margin improvement prospects. It's a storied company with plenty of upside at the right price and can outperform the market by double digits.

- The company has outperformed the broader market, but the price is now higher.

- DD has above-average profitability and return metrics, but the potential upside may be limited. I change my rating for the company in this article.

Dear readers/followers,

You may recall my work on DuPont ( DD ), a company which I've covered a few times over the past 2 years. I have a position in the company, alongside many of the other basic materials and chemical majors. This company, under the right circumstances, has solid execution potential with good margin improvement prospects.

Granted, the last year of performance has left some things to be desired - but in my last article when I considered the company a "BUY", I will argue that it was actually a very good time to buy DuPont.

You can find that article here, and this is the performance we've seen since then.

Seeking Alpha DuPont RoR (Seeking Alpha DuPont RoR)

As you can see, the company has, albeit with a slim margin, outperformed the broader market. In my last article, I gave the company an $80/share price and a "BUY". The company is now materially above the sub-$70/share price that we saw in my last piece, and is above $75/share, which offers a decent prospect for the business - but maybe not as good as it needs to be to invest in.

It's time for an upside on DuPont, and for me to show you where I stand - here is my last article on the company.

DuPont - Plenty to like, but the price is now higher

Why would you invest in DuPont, you might ask?

Well, I'm assuming you, as an investor, like investing in above-quality companies. By that, I mean that the company in question manages above-average profitability and peer-average outperformance return metrics. In layman's terms, it's better than other chemical businesses , and this can be proven.

The company manages an above-average gross margin level, coming up to above 34%, but even more outperforms when it comes to the net margins, where it's above the 85th percentile in the sector (Source: GuruFocus).

Beyond that, the company is well above-average in RoE RoA, and other return metrics.

It can be argued that the company's appeal has been much-changed since only a few months back. The company is now more expensive and at a much lower comparative appeal. The yield is far lower, the upside is lower as well, and the company hasn't really materialized some sort of higher long-term upside.

No, DD and companies like this one tend to grow relatively slowly. Anything close to double digits is considered very good, unless we're talking about a significant reversal from a downturn - which of course, given the overall cyclicality, does happen and does not happen seldom either.

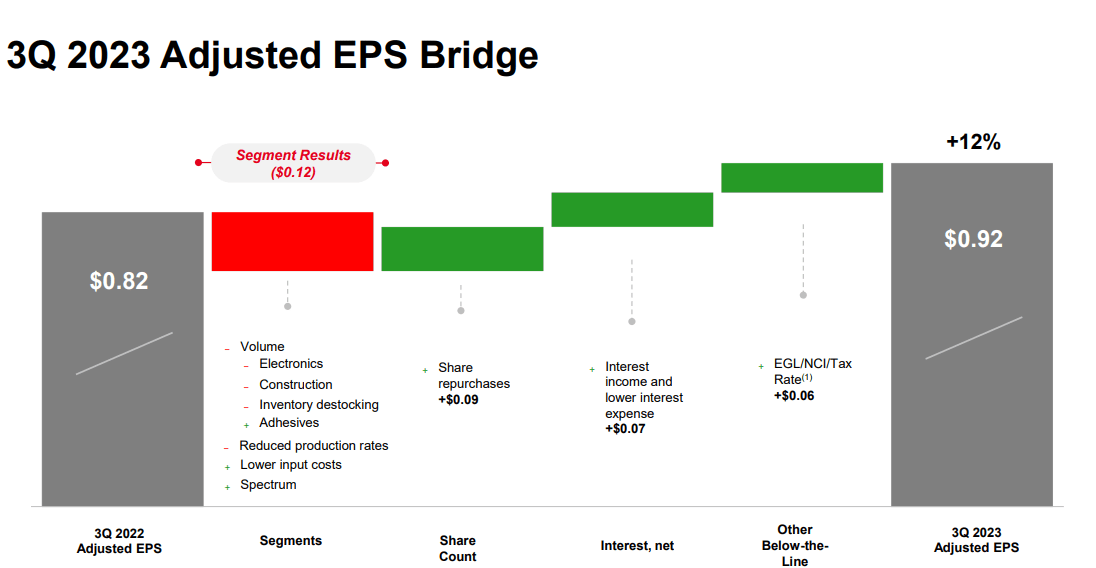

The last set of results we have to look at and estimate from are the 3Q23 results. These are pretty old at this point - but I'll provide an update on this with full-year results, with new estimates when these come out. For now, we'll estimate the company with 2024E, at current results.

DuPont, despite the trajectory of the company's share price, has seen a fair amount of share operational and macro pressure for the past few months. The company recorded a significant, double-digit top-line sales decline due to pressures above all in the semi and construction market. The upside in sub-sectors like adhesives and interconnect solutions were not enough to weigh up what was a continued downturn in main operations.

This also resulted in pressure on the company's EBITDA as the company not only saw volume pressure but also lowered production to match demand to supply.

On the positive side, the company had a strong overall cash flow.

And on the strategic side, we have a few successes as well. The company completed the Spectrum M&A in August, and its divestiture of Delrin, with a very attractive overall deal structure for Dupont.

The company also, when the company's shares were cheap (not now), bought back a significant number of shares and continues to expect to use a significant amount of cash proceeds in 2023 for share repurchases in 2024. We can therefore realistically expect a significant level of support for the company's share price at current, or even higher levels.

This doesn't improve the macro outlook - and in my view, actually makes the company less appealing to invest in, because I don't view the potential upside from share buybacks as something secure enough to invest in.

On a strategic fundamental side, the company's leverage remains at a low level, and the company has no maturities until late 2025, at least none that can be considered significant.

It's important to note that this volume decline the company saw, is despite the overall upside from the pricing initiatives that Dupont has been doing. And unlike some basic materials companies, the decline in sales was broad-based, across the entire world. The least impacted was EMEA, which only dropped 2%.

Here's the relevant bridge for the company for these results.

{kind=link}

The downturn that we're seeing in every segment here should not, in my view, be reflective of the company's fundamental appeal. Following the divestments, spin and sales of most of what I would consider risky from DuPont, I view the segments of W&P and E&I as some very attractive overall operations.

The company's guidance also isn't "bad" as such - it's a decline in both sales and earnings, albeit a very small one in earnings (or none at all if the company's results come in at a decent baseline level). An increased EPS is even within the realm of overall possibility for the business.

The problem that DuPont faces isn't operational - its demand softness. This is an integral part of the sales cycle of any cyclical company - and Dupont is one such.

As long as you understand these tendencies and invest in accordance with them, such cyclicality isn't a problem for me. We have in fact been on a downcycle for a few years, and trends are strong that the potential for an upcycle exists in the next 5-10 years. If this materializes, then Dow is an extremely attractive potential opportunity, and we might have to raise the price target a bit.

Let's look at what the risks and the upside are for this company, and why being careful could be an idea here - but why some analysts at least consider DuPont to be a buy here.

Risks & Upside for DuPont

If we go by analyst targets, DuPont has been undervalued for quite some time. One of the more obvious risks is the PFAS litigation. A recent set of news concerns the agreement with the state of Ohio, where the company has reached a settlement. Other than PFAS, I would characterize the following risks as the largest ones for DuPont - and keep in mind that most of these are high-level, and not something I would characterize as unique for this company.

DuPont is facing softening demand which, given the state of the industry and supply, might result in pricing pressure. So too is the potential impact of a global recession - cyclical companies always get the short end of the stick in that sort of environment, and I don't expect this time to be different.

Secondly, if you look at the company ratios, one thing stands out - the company is underinvesting R&D/Internal investments. A company can only do so much with its profit and cash. Instead of using it more towards internal growth or R&D, the company is focusing on buybacks. I do not find this to be the best capital allocation priority, and I believe that DuPont should at least match the industry average here.

On the flip side, and with the upside, DuPont has owned and still owns some of the most attractive chemical and materials businesses in the world. We're talking about things like Kevlar and other really storied businesses.

The company's operational history/legacy as well as its top-line potential growth in its new iteration, that's the primary upside I see here.

Valuation for DuPont

So, two ways to view the company here - and several reasons to be somewhat more sanguine and conservative here than before, when I bought my shares in Dupont.

First of all, the fundamentals are still very solid. BBB+, less than 25% long-term debt to cap, still all good. But the company has less than 2% yield and the main upside comes in part from the extensive share buybacks , which when performed will increase EPS and as the company hopes, valuation.

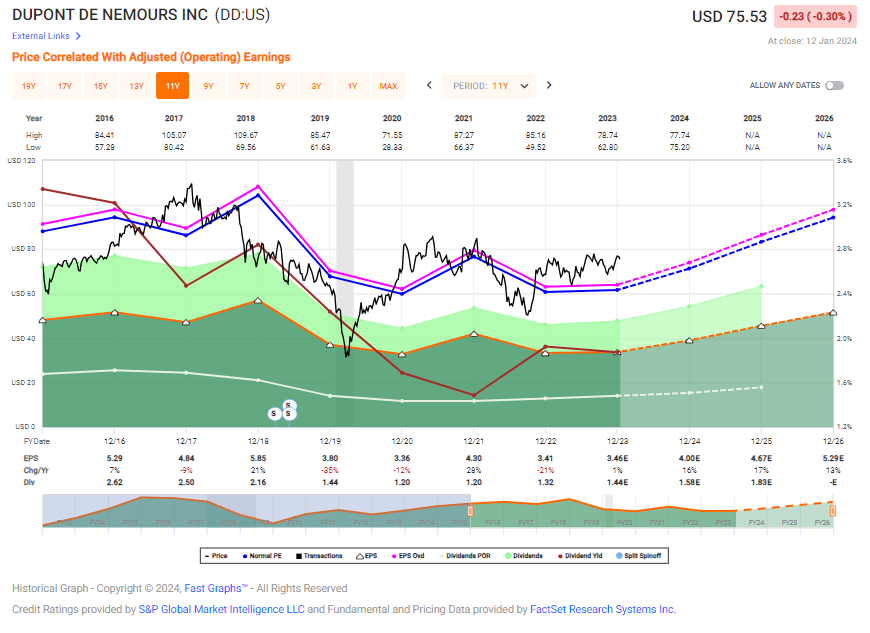

That's what you're seeing in the forecasts here.

DuPont Upside (F.A.S.T graphs)

{kind=link}

DuPont is still at a relatively high price target here, taking into account those buybacks. The company's average share price from S&P Global analysts comes very close to my own, with ranges starting at $49 but going all the way to almost $95/share with averages of around $81. My former share price target was around $80/share, and I'm not switching this target as of this article.

In order to stay positive here you need to expect the company to achieve a better valuation at least in part due to the company's planned buybacks. If you don't believe that this is likely due to headwinds from the operational side of things, like the one we've seen in this latest quarter, then I would say it could be time to become more careful about this company.

At the very least, I don't believe this company has the potential to outperform significantly from here on. Even if we assume a high premium of 19x P/E, that's not even 12% per year inclusive of dividends - more around 11.5%. This might be good enough for you, given the company's other operational qualities, but it is not good enough for me here. And if we forecast closer to 15-16x P/E, the company is more likely to generate returns of 3-4% per year from here on - again, not good enough - at least not for what I'm looking for, which is around 15% per year conservatively.

Sometimes things happen in the interim while you submit and write an article. In this case, the company dropped down from right around $75 to $73/share. A valid question might be if the thesis at $73 is materially different or still justifies my rating change on the company. Given that the thesis at this point still requires the company to trade at over 19.7x P/E to annualize at above 15%, there's no material change to my thesis here, and I still say "HOLD".

Overall, I think that there's now a lot more downside or market-performing likelihood rather than outperforming. This has resulted in me changing my rating for the company to a "HOLD", because even maintaining my PT and saying that this company is indeed worth $80/share, the upside to $80/share is now, for new investors, less than I what I would personally consider going in at.

For that reason, here is my thesis on DuPont as it stands for 2024 and as it stands until we know more about the operational results for FY23.

Thesis

My thesis for DuPont is as follows:

- Chemicals/Industrials are still an investable segment, and I continue to invest major capital in businesses such as BASF ( OTCQX:BASFY ), Linde ( LIN ), L'Air Liquide ( OTCPK:AIQUY ), LyondellBasell ( LYB ), Covestro ( OTCPK:COVTY ), and others.

- The company combines the appeal of specialty chemicals with a great market position, excellent fundamentals, and a yield that could double in less than 5 years if the company's growth plan remains intact. I also like the pricing the market is giving some of the options for the company here, which is why I might go for some of them.

- I now give DuPont a "HOLD" with a PT of $80/share for the longer term, legitimizing some of the company's premium that we see here, but not as much as in my previous article. This is a price downgrade as per my last article a few months ago, and now also a rating downgrade.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them.

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansions/reversions.

The company no longer has a high enough realistic upside, and I would not be interested in adding at this price, even if I am interested in "HOLD" here.

For further details see:

DuPont: Less Future Potential (Rating Downgrade)