DD - DuPont Stock: We Have Some Highlights Going Into FY23

2023-11-03 07:39:20 ET

Summary

- DuPont's recent underperformance in the market is not due to unattractive results, but rather a mixed bag of performance in different sectors.

- The company has shown solid execution, with margin improvement and strong cash flow performance.

- Despite the current challenges, DuPont is a market-leading company with long-term upside potential. I give DD stock a "BUY" with an $80/share PT.

Dear readers/followers,

DuPont (DD) has been a long-time investment and a long-time hold of mine. I don't have a massive position in the company, nor am I likely to significantly prioritize this for near-term investments, but that is not due to lack of appeal. This company, which I last reviewed back in August of 2023 with a solid "BUY" rating after a 40% RoR in a relatively short time, outperforming the market, recently reported the 3Q23 results. Since that article, DuPont has underperformed - not just going into the negative, but actually underperformed the market as a whole, dropping 11% and some change.

This is not, however, as I see it, due to unattractive results.

Here is the link to my last article and my last thesis, which was a positive one. In this article, I'll show you why I am not changing my thesis for DuPont at this time, even if the valuation isn't as attractive as when I bought the business.

DuPont - Plenty to like, even after a significant drop

To say that DuPont de Nemours was cheap in the fall of -22 would be an understatement. However, many companies were cheap back then, which is why I did unfortunately not add much. I did build out my position a bit over time, but we're still not talking about any sort of massive appeal that would justify a significant "victory lap" on my part. A position is only as good as its size when it comes to counting returns. And this massive RoR compared to the market won't really make a massive difference, unfortunately, given my relatively limited size of the overall stake.

However, we might be in for a second round where we can buy one of the foremost chemical companies on the planet - and if you follow my work on BASF (BASFY), you know I'm all about investing in basic materials and chemicals when this is cheap.

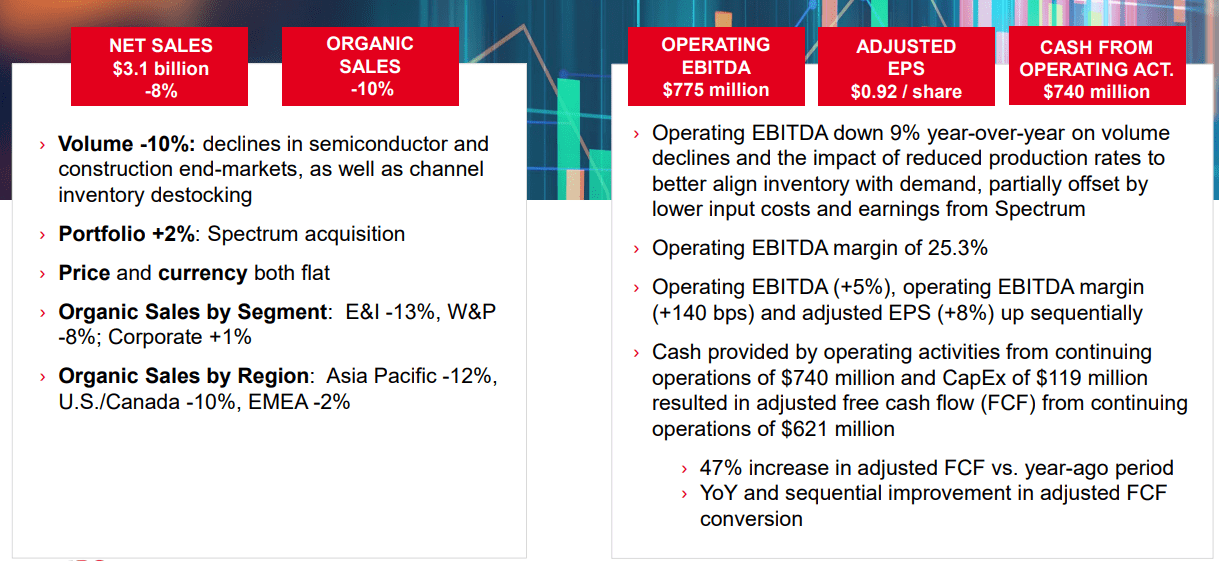

The latest set of results we have to look at are 3Q23 - and those came in more or less at expected levels, with some exceptions. (Source: DD 3Q23 )

Sales were actually <$100M less than expected, coming in above $3B but below the guide, but operating EBITDA was solid at over $770M, and the company reported adjusted EPS of $0.92, which is up more than 10% from the guide number.

What are some of the moving parts of these results?

- Organic sales decline came due to volume pressures in both semi and construction. We've seen this volume pressure and the destocking of inventory channels in many of our other chemical companies as well. However, DuPont, due to its mix, also saw growth in adhesives and continued improvement in interconnect solutions. So while the market may, given the recent set of declines, see the company as weak going into this fourth quarter, I say it's more of a mixed bag.

- The company's EBITDA came in according to guide but was down YoY due to lower volume results, and lower production rates. Much like other chemical companies like Evonik ( OTCPK:EVKIY ) and BASF, Dupont is adjusting production output to demand - which in this case means producing less.

- Importantly however, we saw non-trivial margin improvement for the company here, as well as a strong overall cash flow performance, which tells me that the company is still working quite well, despite these results.

The words "solid execution" are mentioned in the material, and I would, as an analyst, stand behind this sentiment. (Source: DD 3Q23 )

Some housekeeping and M&A. The company finished the Spectrum acquisition in early August. Spectrum is aligned with its Industrial Solutions and is likely to bring further growth here. At the same time, the company divested Delrin, in a deal set to close in November, with a deal structure that's attractive in terms of future value.

Also, the company has completed a significant tranche of share repurchases - over $3.2B, which launched in 2022 at about this time. This is one of the drivers of what we're seeing here - the buybacks are supporting the current share price level range, where we're seeing a 12-month support at the $66/share level, which we haven't gone below in some time.

DuPont is clearly, to me at least, a company in the process of structural improvements in a difficult environment.

{kind=link}

Because I invest so much in the basic materials and chemical sectors, many of the trends we see in DuPont, are trends I see with similar clarity in other companies. So the things that seem to spook at least some investors, judging by the company's share price development, do not really spook me. The EPS bridge developments make sense to me because I see the same thing in other companies. Drag on EPS here are volumetric concerns in areas of electronics/semi-related and the infra/construction sector, while adhesives are at a good trend. Other of my investments do not necessarily have adhesives in their mix, but the remaining trends are ones I would characterize as "macro". (Source: DD 3Q23 )

Inventory destocking, above all, is something we see across the entire board.

The fact that the company in this case has managed to further lower input costs is a feather in its cap.

It's worth noting, however, in trying to be fair, that company EPS improvements are purely a play on share buybacks (less SO), interest income and interest expense, and EGL/NCI. That means the resulting EPS growth is not a result of clear operational improvements or sales improvements, except for the lower input costs. The current macro environment isn't set up for massive increases on the bottom line here - and we can see that across most of the company's sectors. (Source: DD 3Q23 )

DD IR (DD IR)

What you see here are illustrative trends for how most sectors in DD are currently working. We're talking decline in sales and EBITDA in Electronics and in Water & protection, with these two segments constituting what remains of a once-massive conglomerate. DD is still huge, of course, but nowhere near the size it once was.

Like other chemical and basic materials companies, DD has updated its assumptions for 2023 and in this case, slightly revised it downward. What was previously a range of EBITDA has been guided to the lower range of that guidance, just below $3B for the full year, with a mid-point EPS of $3.45/share, due to destocking, underlying demand for electronics, semi, slower industrial water segment demand in China and so forth. Nothing we haven't seen in other companies. As usual, when faced with such trends, the company is planning restructuring actions and savings initiatives beginning in early 2024 to address these trends.

Even the slight accretive M&A from Spectrum has done and will do nothing to really outweigh the significant headwinds from both of the company's key segments both in terms of top-line sales for the full year, but also in terms of bottom-line EBITDA and net.

Once macro turns around, DD will do the same. Until then, and as of right now, the company has been weighed up by share buybacks and other positives/upsides.

DuPont is a market-leading company in key technologies and segments. This is in no way a bad business - and you can expect, just as with some of its peers like BASF, that DuPont is going to be performing well eventually.

{kind=link}

Overall, I remain positive on DuPont, not because of a so-so 3Q, but because of the fundamentals of the company and the long-term upside - much like with my significantly larger investments in companies like BASF.

DD Stock Valuation - the upside here is quite decent, but the yield is sub-par.

There are key reasons why my DD position is small, and my BASF position is quite a bit larger. DD is BBB+ rated, with similar "safety" to BASF in the long term. But BASF is the company with more upside from two perspectives.

First off, despite some of the issues we're seeing with DuPont earnings, the company is still trading at just south of 20x P/E. Don't get me wrong - there is an upside, and given the company's market position I am allowing a higher premium for this business, but I will not call the company "cheap" here, because it's not.

Not historically, and certainly not in this market.

The company, as of right now, yields 2.11%. This might have been acceptable a year ago, but it's not acceptable now - not when you can get 5% easily.

On the longer-term perspective, DuPont tends to trade above 20x P/E normalized. It's currently at 19.8x. The company, unlike other chemical and basic materials businesses, is set to expect significant, double-digit growth in both 2024-2025E as of the current set of forecasts and expectations. Given the company's operational plans over the next 2 years, and once inventory destocking and rationalization are over, I do not have an overall issue with this growth estimate - and because of this, I view the premium as relatively valid here, even if the company cannot be called "cheap".

In my previous piece, I gave the company a PT of $80/share. I maintain this share price target at this time and justify it based on the company quality and estimated growth, which at a 19.8x P/E implies an annualized rate of return of 16.5% per year , fulfilling my minimum demand for the businesses that I invest in, of around 15%.

DuPont, at this time, is estimated to be worth a range from $49 on the low end to $95/share on the high end (Source: S&P Global). 17 analysts follow the company, and out of these 17, 12 are either at "BUY" or "outperform" for the company, coming in at an average PT of $79. My own target is therefore slightly above this, but I use the same justification as these other analysts to see the upside of around 15-16% for the company here.

It's my view that based on fundamental quality, and the prospects for earnings growth expansion from projects and volumes once the macro changes, DD will see earnings growth that will translate into increased valuation, dividend growth, and shareholder outperformance to the market. Based on this assumption and a 2-3 year forecast, my thesis for the company is as follows.

Thesis

My thesis for DuPont is as follows:

- Chemicals/Industrials are still an investable segment, and I continue to invest major capital in businesses such as BASF ( OTCQX:BASFY ), Linde ( LIN ), L'Air Liquide ( OTCPK:AIQUY ), LyondellBasell ( LYB ), Covestro ( OTCPK:COVTY ), and others.

- The company combines the appeal of specialty chemicals with a great market position, excellent fundamentals, and a yield that could double in less than 5 years if the company's growth plan remains intact. I also like the pricing the market is giving some of the options for the company here, which is why I might go for some of them.

- I give DuPont a "BUY" with a PT of $80/share for the longer term, legitimizing some of the company's premium that we see here, but not as much as in my previous article. This is a price downgrade as per my last article a few months ago, but not a rating downgrade for the time being.

- The rating and upside here are actually better than before, and I increase my conviction in "BUY" here.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them.

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

For further details see:

DuPont Stock: We Have Some Highlights Going Into FY23