KD - DXC: Not A Buy Even After The 25% Slump

2023-09-12 17:17:21 ET

Summary

- DXC Technology's stock value dropped by more than 25% after the release of its first quarter 2024 results.

- Analysts have reduced their price target, but, it is still higher than the current share price.

- This thesis examines the fundamentals and market positioning of DXC Technology to determine if it is a worthwhile investment.

- It also looks at AI opportunities.

- The stock is a hold.

The over 25% slump after the release of first quarter 2024 results now sees DXC Technology ( DXC ), an IT services company, valued at less than $20.5 per share. Another factor that weighed in was a downgrade by RBC Capital Market with analysts changing their position to hold and reducing their price target to $29 down from $34, which is still $8-$9 higher than the actual price.

However, I do not have a Buy position for reasons I will detail in the thesis with an aim to look at fundamentals, the operating segments, as well as the market positioning in the IT Consultancy and Services industry for a stock with a forward P/E of only 6.46x, or 37% below the IT sector.

For this purpose, I will mostly use information from SEC filings and earnings transcripts for the first quarter of 2024 (Q1) which ended in June.

Changing Industry Perspectives

First, just like other players in the IT services industry including Unisys ( UIS ) and International Business Machines ( IBM ) (before it split out the IT infrastructure business Kyndryl ( KD )), DXC has suffered from the emergence of the public cloud. This suffering is evidenced by the downturn in its quarterly revenues since 2018 which is due to clients migrating their IT workloads to the cloud of hyperscalers like Amazon's ( AMZN ) AWS, in turn diminishing services procured from DXC.

The migration process consisting of moving software applications from the client's servers often located in DXC's data centers to the cloud meant additional revenue for the company, but this was only temporary as eventually with fewer IT assets left to manage, less service revenue made their way to the income statement.

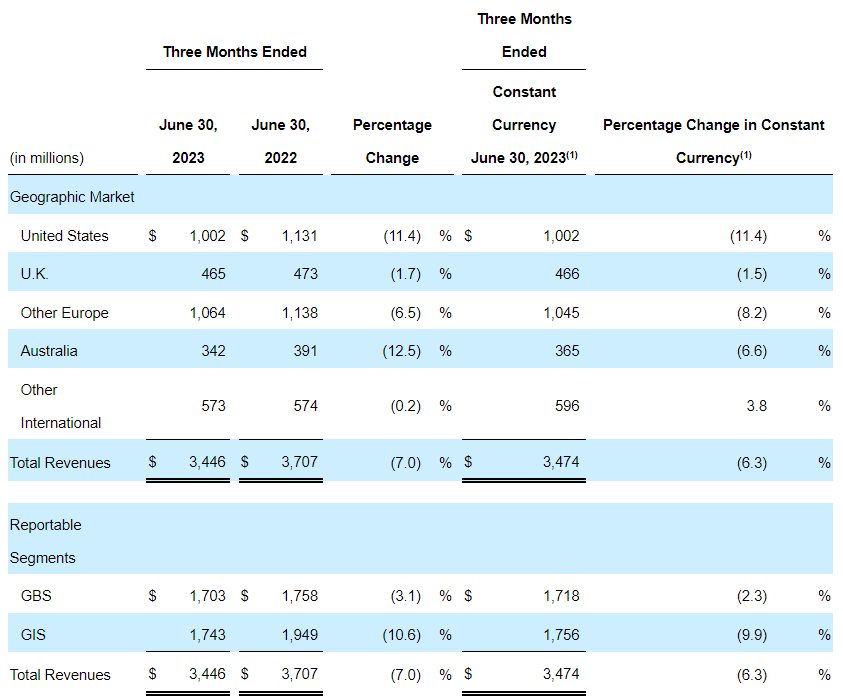

Looking deeper, the company is structured in two segments, GBS (Global Business Services) and GIS (Global Infrastructure Services) as pictured below with both seeing revenue regression of 3.1% and 10.6% respectively in Q1. Part of the reason was the stronger dollar accounting for 0.7% of the headwind, but, there were also actual declines in organic revenue.

{kind=link}

A Mixed Picture with GIS and GBS

Focusing on the weaker GIS which has been more impacted and includes the Cloud Infrastructure and ITO business, it has not performed as per expectations. In line with the industry-level picture provided earlier, the main reason behind this was the weakness of Cloud ITO which is the outsourcing business where the IT infrastructure of other companies is managed.

Again looking at the bigger picture, as part of the secular digital transformation trend, after most companies have migrated services to the cloud, some now operate in a hybrid mode whereby part of their IT workloads are still hosted within data centers owned by DXC. The problem for traditional IT service providers is the public cloud economics model whereby customers pay on a usage basis (as opposed to one where they have to incur large capital expenditures on an upfront basis to deploy their infrastructure), which makes more sense in a high-inflation environment where costs have escalated.

This results in less enthusiasm for DXC’s facilities, which is the reason there is a plan to reduce “underutilized data center” space and move work to the cloud. However, depending on the type of contract, this may involve the IT services company itself having to lease wholesale computing resources on the public clouds, or convincing its customers to do so, as well as customers' willingness to pay the additional migration fees, which will ultimately depend on the execution.

Moving on to GBS, this segment has been relatively less impacted. It includes the IT Security business, which has remained a bright spot as it grew by 6.8% on a non-GAAP basis. However, with its $111 million of revenues, or about 6.3% (111/1743) of GBS's overall sales in Q1, it does not have sufficient weight to meaningfully improve the company's finances by itself.

Looking further, GBS also includes the Insurance Software business, developed when DXC was still part of Hewlett Packard Enterprise's ( HPE ) services arm, before being spun off in March 2017. This is basically software that was created years ago but is still used by many insurance companies, and even banks, because there is a high degree of customization especially carried out for those organizations. Now, moving away from these would imply high switching costs, meaning that the customers are actually almost captive. However, again the Insurance business only constituted 11% of the company's Q1 sales, which is not significant enough to protect it in case of an economic downturn.

This means that despite boasting two sources of strength, DXC is still subject to market realities like weakness in IT spending in an economic environment where monetary conditions remain tight, which are likely to impact corporations across the board. Furthermore, the company's Modern Workspace business has been performing poorly as more people come back to the office, and it also faces challenges in reselling IT equipment that has already been used for certain projects.

Consequently, the organic revenue guidance for the second quarter of 2024 which ends in September has been lowered from -4.5% to -5.5%, and, with this dim outlook, it was no surprise that the market punished the stock, but the question is whether the 25% loss of value which now puts the market cap at $4.22 billion was not an overreaction.

Undervalued but not a Buy

For this matter, one of its peers Kyndryl comes with a $3.87 billion market cap, generates more revenues, but less cash flow, and delivers lower gross margins. This means that from a valuation standpoint, they are more or less similar in my view, implying that DXC's approximately four billion dollar market cap seems to be a fair value.

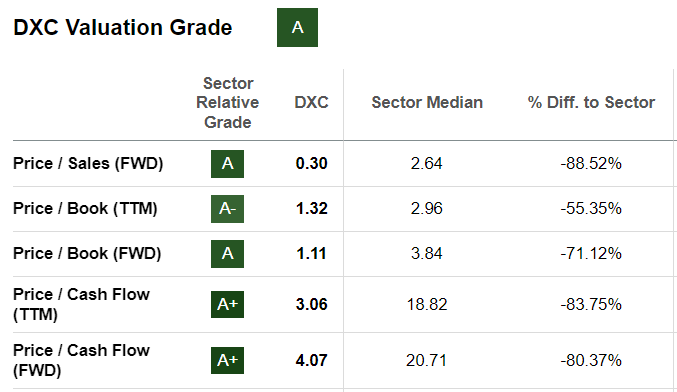

Now, some may argue that with a valuation grade of A and a trailing Price/Cash flow which is more than 80% below the median for the IT sector, the company trades at a significant discount.

{kind=link}

However, the problem is that a lot of the operating cash flow generated has been consumed as capital expenses and stock buybacks. In this regard, an optimization of the working capital management process is in place, including faster (revenue) collections from customers. At the same time, in order to reduce the real estate footprint, new lease commitments are scrutinized more in-depth before being approved. Thus, progress can be expected in driving better free cash flow, but no specific time period has been provided for such an improvement.

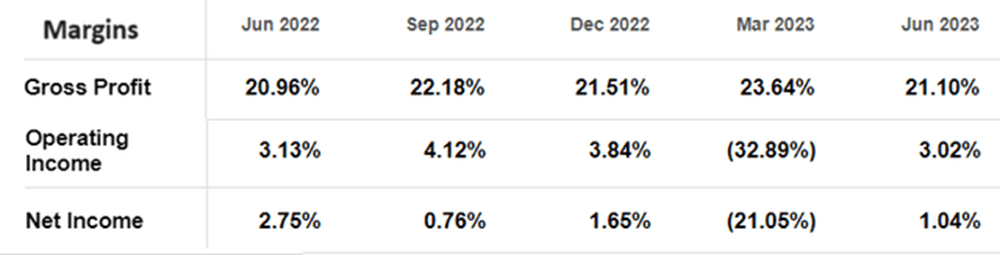

Looking at profitability, one of DXC's strengths is that its GBS segment generates double-digit margins and generates about 50% of overall sales. As a result, looking at profitability, despite sales going down, margins have remained mostly positive during the last five quarters as shown below.

Quarterly Income Statement (seekingalpha.com)

{kind=link}

To this effect, the strategy to focus on deriving better productivity out of the teams driving service revenues, namely by reducing project overheads should help, but, provided that the gains are not offset by higher restructuring costs where the company fine-tunes its new operating model to better manage supply and demand conditions. This was the case in Q1.

However, with a slowdown in customer expenditures, and wage inflation remaining high in a still-tight labor market, it may not be easy to sustain positive margins. Then, depending on how the news hits the market, the share price could see further periods of volatility in my view, especially when second-quarter results are announced in the first week of November.

Still, for those with the patience to monitor the stock for the longer term, there are certain things to watch out for.

What to Look For

First, it could win major contracts for its AI-led product offerings.

One of them is Platform X, co-developed with ServiceNow ( NOW ) so that clients can have visibility on their IT parks of equipment which now not only are located in their offices but also in the clouds of Microsoft ( MSFT ) or Salesforce ( CRM ).

Now, Platform X was precisely the reason I was bullish on DXC back in January this year. My thesis emphasized the platform approach which is synonymous with wider reach compared to traditional methods of deploying software applications while at the same time consuming less effort or money. Thus, based on the company's lower earnings multiple, I had a 20% upside target, which did not materialize. Instead, the stock is down by around 28%.

Two reasons that explain the discrepancy between my prediction and what actually happened are firstly, the company has been spending more than expected on its new operating model. Secondly, while there is a lot of talk about Platform X, there appears to be insufficient traction for the product which forms part of the GIS segment. This can possibly be explained by companies focusing on another flavor of artificial intelligence: Generative AI and related innovations like ChatGPT.

In this respect, some analysts have warned about risks posed to conventional IT, as spending gets diverted to Nvidia ( NVDA ) which manufactures GPU chips, or big cloud providers like Amazon which are building AI infrastructures. Now, DXC does have an Analytics business, but it will depend on how it positions itself to harvest AI opportunities. One option could be leveraging its experience in building the data foundations which are the prerequisites for intelligent algorithms to function optimally.

In conclusion, amid a few bright spots and potential AI prospects, this thesis has shown that DXC is not a Buy despite analysts having a higher price target, as it is likely to continue facing testing times ahead unless it manages to bag many other contracts similar to the one with AT&T ( T ) to offset the mounting losses in its GIS segment. This means that its share price should continue to be under pressure, but, nonetheless, share buybacks which amounted to $686 million in the fiscal year 2023 alone, could provide some support for the stock.

For further details see:

DXC: Not A Buy, Even After The 25% Slump