DXC - DXC Technology: A High-Risk Play For Investors

2023-09-13 16:40:44 ET

Summary

- DXC is a company that helps big companies with their computer systems, offering tech services and managing data.

- In the first quarter of 2024, DXC's revenue decreased by 7% compared to last year, with a decline in both their business services and global infrastructure services.

- The company spent more than it brought in, with negative free cash and a decrease in earnings per share. However, they have a diverse customer base and are trusted by major companies and government groups.

Thesis Statement

DXC Technology ( DXC ), a global tech services company, has recently displayed weakening financials that merit a cautious approach from potential investors. Despite seemingly robust revenue figures, declining trends in key financial indicators, such as revenue, profit, and particularly free cash flow, serve as red flags. Investors need to approach DXC with caution.

Company Overview

Founded as a leader in tech services, DXC Technology has cemented its place as the go-to solution for big organizations looking to manage and update their computer systems effectively. Its reach is not limited to private enterprises; even governments have been known to trust DXC for their tech needs.

Client Trust Factor

DXC has garnered significant trust among Fortune 500 companies and public sector organizations. This trust is predicated on DXC’s track record of delivering high-quality technology services that enhance operational efficiency and customer engagement.

Revenue Streams

DXC has a dual revenue stream, which comprises Business Consulting and Global Infrastructure Services. The former helps organizations optimize their operations through technology, while the latter focuses on the nuts and bolts—hardware and software—ensuring smooth system performance. Geographically, the company has a footprint in key markets, including North America, Europe, Asia, and Australia, and directly sells its services through its global offices.

Takeaway

- Diverse Geographic Footprint : DXC's global presence in North America, Europe, Asia, and Australia means it can leverage multiple markets for growth.

- Wide Range of Services : Their two-pronged approach to service—Consulting and Global Infrastructure—allows them to serve a varied clientele, including private and public sectors.

- Direct Sales Model : The company's direct-to-customer sales strategy not only allows for competitive pricing but also fosters stronger client relationships—a significant strategic advantage.

Key Metrics Overview

Revenue & Profit

DXC Technology reported a Q1 revenue of $3.4 billion , a 7% year-over-year decrease. The decline is most noticeable in organic revenue, which dropped 3.6% compared to the same quarter last year.

Earnings Per Share

The company’s EPS declined significantly to 17 cents in Q1 2024, down from 43 cents in the same period last year.

Adjusted EPS

The adjusted earnings per share for the quarter was 63 cents, a 16% reduction from 75 cents in the corresponding quarter of the previous year.

Cash Flow and Capital Expenditures

The company made $127 million from its core business but spent $202 million on capital expenditures, resulting in negative free cash of $75 million.

Share Buyback

The company utilized $280 million for share buybacks, generally a measure to enhance shareholder value.

Takeaway

- Declining Revenue and Profit : A 7% decline in revenue and a drop from 43 cents to 17 cents in EPS year-over-year could indicate operational inefficiencies and market headwinds.

- Negative Free Cash : The negative $75 million in free cash after capital expenditures could indicate short-term financial struggles.

- Share Buyback : While share buybacks are often a positive signal, they raise questions in this scenario, given the other negative financial indicators.

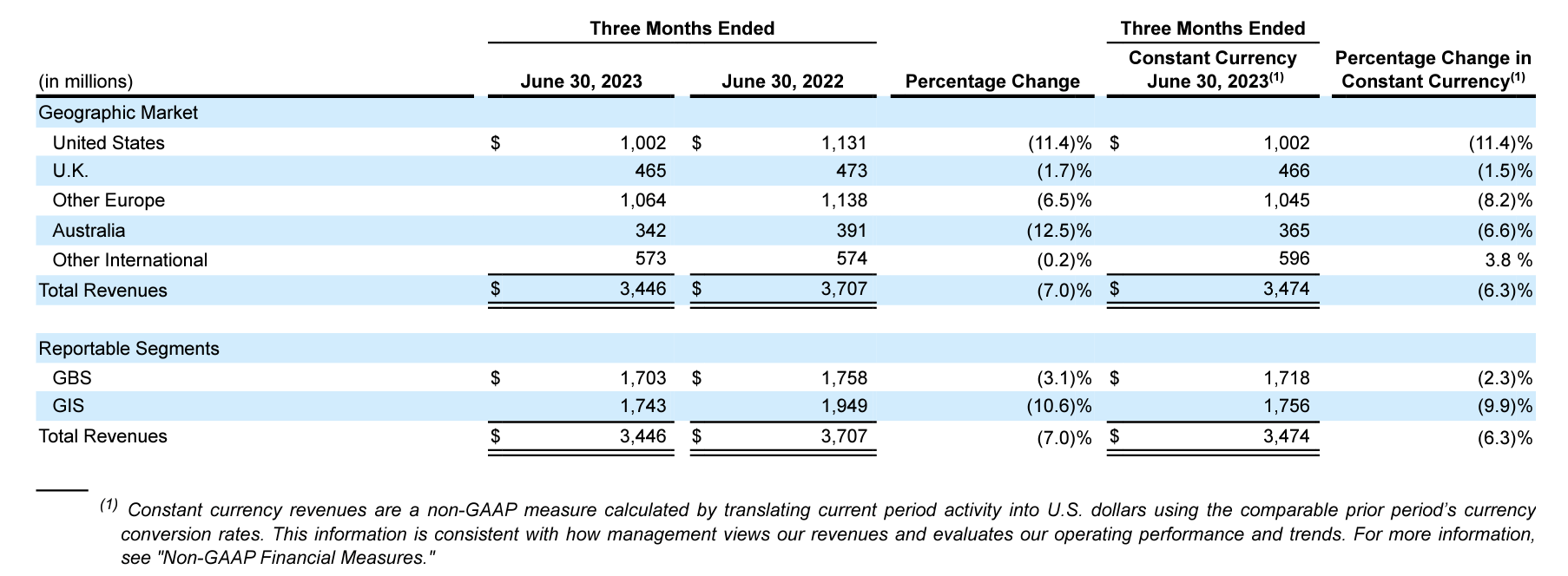

Revenues From Operations

{kind=link}

Overview

In Q1 2024, the company reported total revenues of $3.4 billion, $300 million less than last year's period. Various factors contributed to this decline, ranging from currency fluctuations to divestiture decisions and "organic revenue" shifts.

Currency Fluctuations

Currency value changes had a marginal 0.7% impact on the revenue decline. Specifically, the U.S. dollar's strength against the Australian Dollar unfavourably affected the company's income.

Business Divestitures

The company sold or shut down specific business segments, contributing to a 2.7% decrease in revenue.

Organic Revenues

The largest contributor to the decline was a 3.6% drop in "organic revenue," which comes from the company's core operations.

The Revenue Playbook: GBS vs. GIS

Global Business Services

GBS generated $1.7 billion this quarter, $55 million less than the previous year, marking a 3.1% decline. However, the division grew its core services by 3.3%. GBS now constitutes 49.4% of the company's total revenue, an uptick of 2% from last year.

-

Foreign Currency Impact : A minor 0.8% loss was due to unfavourable foreign currency exchange rates.

-

Business Unit Changes : A 5.6% decline in revenue was due to the business dispositions.

Global Infrastructure Services

GIS also made $1.7 billion but took a harder hit than GBS. The division lost $206 million compared to last year, a 10.6% decrease. GIS contributes 50.6% to the company's total income, 2% less than last year.

-

Core Business Woes : 9.9% of the loss is from their core business activities not performing as expected.

-

Currency Fluctuations : A 0.7% loss was due to currency value changes, echoing the impact on GBS.

Takeaway

- Contrasting GBS and GIS : GBS has managed to grow its core business, while GIS has faltered in its core activities.

-

Foreign Currency is a Factor : Currency changes affected both segments but aren't the main story here.

-

Revenue Share : GBS now makes up a bigger slice of the pie, while GIS accounts for a bit less than last year.

-

Business Reorganization : Both divisions are impacted by reorganization, affecting revenue contributions.

Costs of Services

This quarter, DXC spent $2.7 billion, which is $211 million less than they spent during the same time last year. So, how did they manage to spend less?

-

A favourable currency exchange rate contributed to a savings of $23 million.

-

Reduced hiring of external experts and fewer sales also contributed to the decline in operational costs.

The "gross margin" remained nearly static at 21.1%, only a slight bump from last year's 21.0%.

Selling, General and Administrative Costs

SG&A costs for the quarter stood at $327 million, $22 million less than last year. However, SG&A costs as a percentage of income increased slightly to 9.5%, up by 0.1%.

Savings were achieved through reduced spending on professional services and vendor costs. Conversely, employee salaries saw a moderate increase.

Merger Related Expenses

DXC set aside $11 million this year for "indemnification," a typical practice in mergers and acquisitions. This is marginally higher than the $10 million set aside last year.

Depreciation and Amortization

The company spent $113 million on depreciation and $231 million on amortization. This is a reduction of $25 million and $20 million, respectively, compared to last year. The company finished some contracts with less software to amortize, so they saved some money here.

Restructuring Costs

DXC spent $20 million on restructuring, $13 million less than last year. This year, the sale of smaller business segments resulted in a $5 million loss, contrasting with a $38 million gain last year.

Takeaway

-

Operational Efficiency : DXC has reduced operational and SG&A costs, showing a commitment to improving profitability.

-

Asset Management : Reducing depreciation and amortization expenses suggests better asset management.

-

Strategic Decisions : Increased merger-related expenses and reduced restructuring costs indicate strategic focus, though the impact on the company's future remains to be seen.

Earnings Per Share

DXC Technology reported a Q1 2024 EPS of 17 cents, a significant drop from last year's 43 cents during the same period. The decrease stems from a $66 million fall in total profit.

EPS Breakdown - Q1 2024

- 7 cents was spent on restructuring the company.

- 32 cents was used to account for the loss in value of intangible assets they've acquired, like software.

- 2 cents was lost because they sold off parts of the business ("divestments").

- 3 cents went to writing off bad investments they made.

- 1 cent was used to adjust their taxes.

EPS Breakdown - Q1 2023

- 11 cents were used for restructuring.

- 1 cent went to costs related to deals and mergers.

- 34 cents were for amortizing acquired intangible assets.

- 16 cents were gains they made from selling off parts of the business.

- 3 cents were set aside for costs related to a merger ("indemnification").

Takeaway

-

Increased Amortization Costs : The 32 cents allocated for amortization this quarter isn't a sudden spike year-over-year but still represents a big chunk of the EPS.

-

Restructuring Focus : DXC used 7 cents for restructuring in 2024, compared to 11 cents last year. The reduction suggests that the company is possibly moving past its restructuring phase, which could be positive in the long run.

-

Lack of Divestment Gains : Last year's EPS got a 16-cent boost from divestments; this year, it was a 2-cent loss, meaning they didn't get any one-off financial windfalls this time.

-

Tax and Bad Investment Impact : Adjustments for taxes and writing off bad investments accounted for 4 cents, a relatively minor but still notable part of the EPS drop.

DXC Technology's steep drop in EPS from 43 cents to 17 cents in Q1 2024 may initially appear concerning. However, a closer look reveals that the company is undergoing restructuring and absorbing amortization costs, which are non-recurring expenses. The absence of divestment gains, which boosted last year's EPS, also skewed this year's figure lower.

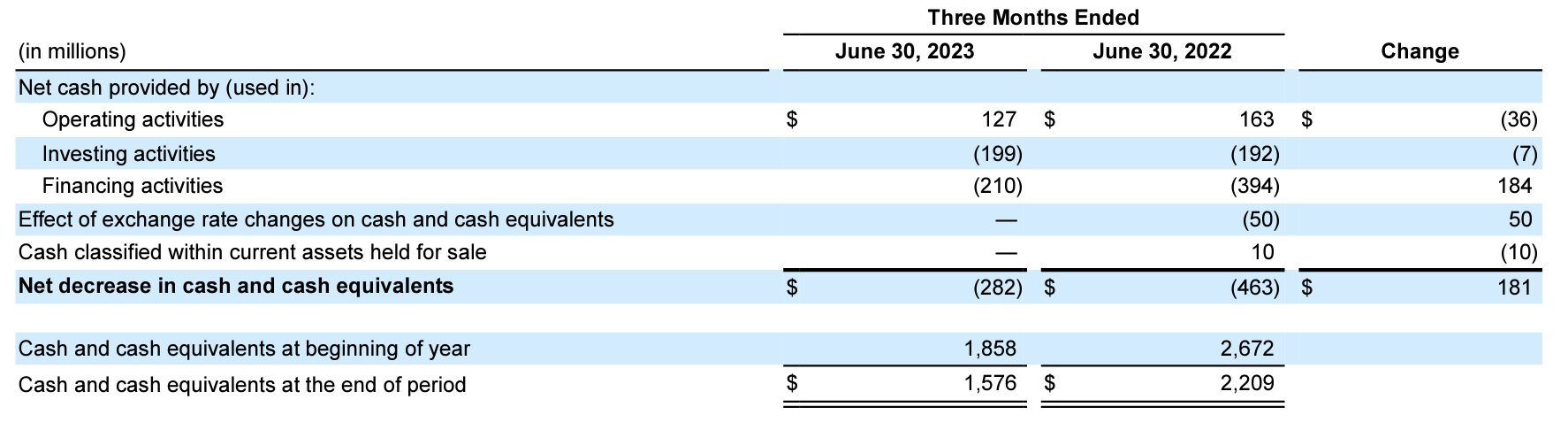

The Liquidity Picture: What The Numbers Tell Us

As of today, DXC Technology holds $1.6 billion in cash, with around $800 million stored overseas. This marks a decrease from March, when they had $1.9 billion in cash, of which $700 million was outside the U.S.

{kind=link}

Cash From Operations

DXC Technology generated $127 million in cash from operations this year, a $36 million drop from last year's $163 million. Notably, earnings fell by $109 million, even after adjustments, which explains much of this decrease.

Working Capital

On a brighter note, working capital showed a robust improvement of $73 million. A significant boost can be attributed to more efficient accounts receivable collections.

Cash Conversion Cycle

Additionally, the cash conversion cycle tightened from 22 days to 20 days. This shows that DXC is converting its expenditures into cash more swiftly than before.

Investment Activities

DXC Technology amped its investments to $199 million this year, marking an increase of $7 million from last year. The changes break down as follows:

- Business Dispositions : $29 million less spent this year.

- Long-Term Investments : An additional $27 million, largely funneled into software.

- Miscellaneous Activities : A cutback of $9 million compared to last year.

Financing Activities

Financing took a sharp dive to $210 million this year from $394 million last year, translating into a whopping $184 million decrease. Key moves include:

- Leasing and Loan Repayments : A reduction of $28 million, signalling a more frugal approach.

- Short-term Loans : DXC padded their finances with an extra $188 million, even after paying off older debts.

- Share Buybacks and Tax Handling : An increase of $35 million in expenditure.

Takeaway

- Earnings and Cash Flow : While the company generated less cash this year, it's essential to note that earnings took a sizable hit. This directly affected the cash from operations, which is a red flag.

- Cash Position : Despite a noticeable decline in cash reserves, DXC Technology can repatriate $800 million back to the U.S. without additional taxation. This could significantly fortify its domestic cash pool.

-

Working Capital and Cash Conversion : The increase in working capital, particularly the proficiency in accounts receivable, is a positive sign that their daily operational cash needs are improving. This could be a signal of better financial management. A reduced cash conversion cycle is always good news. It means the company is more efficient at turning its spending into cash. This could be an indicator of increased operational efficiency.

-

Investment Activities : A $7 million uptick in overall investments is noteworthy. The $27 million allocated to long-term software investments is even more compelling, signalling a calculated pivot towards technological advancement and future growth.

-

Financing Activities : The company has notably cut back on financing activities. Specifically, it saved $28 million on lease and loan repayments, indicating a cautious approach towards debt management.

DXC Technology presents a mixed bag when it comes to liquidity. On the one hand, it has demonstrated working capital and cash conversion efficiencies. Conversely, there's a decrease in cash generated from operations and total cash reserves. However, strategic long-term investments and prudent financial management hint at a cautiously optimistic outlook for the company.

Valuation

{kind=link}

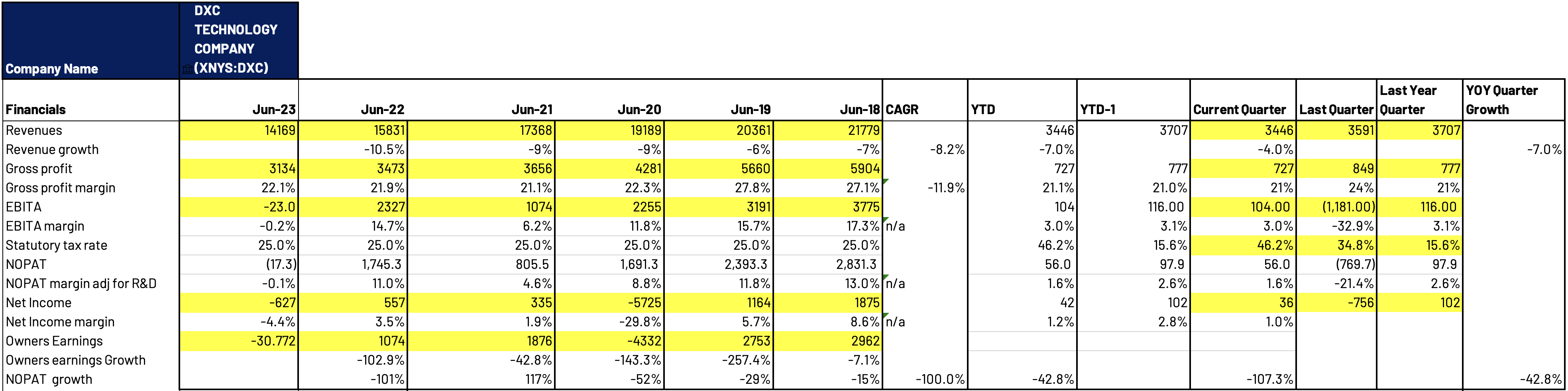

Revenue Decline

DXC Technology has significantly eroded its revenue base over five years. 2018, the company reported an impressive revenue figure of $21.7 billion. However, by 2023, this had sharply declined to $14.1 billion, registering an average annual contraction of 8.2%.

Margin Contraction

Equally alarming is the company's gross margin compression, which has diminished from 27.1% in 2018 to 22.1% in 2023. Furthermore, the Earnings Before Interest, Taxes, and Amortization margin has swung from a robust 17.2% in 2018 to a negative 0.2% in 2023.

Underlying Factors

The erosion in gross margin points towards rising production costs, operational inefficiencies, or pricing pressures that DXC Technology has been unable to mitigate effectively. The downturn in EBITA margin is even more concerning, with the company's core business also underperforming alongside divestitures contributing to this negative trend.

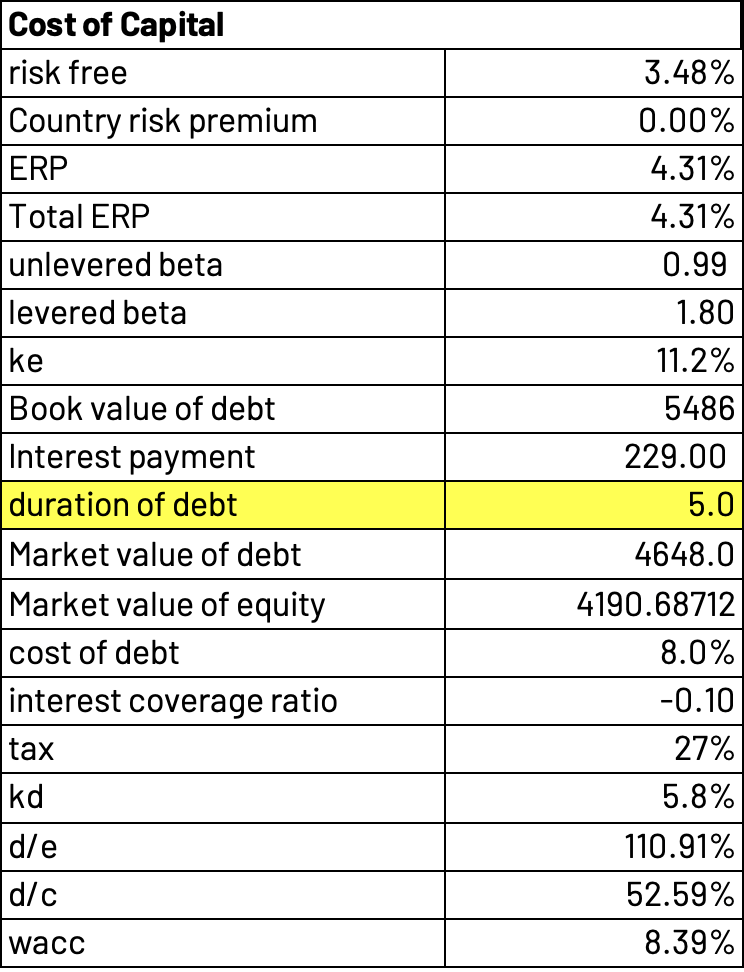

{kind=link}

DXC Technology is grappling with an onerous debt load totalling $5.4 billion. The company must make annual interest payments of $229 million, a burden becoming increasingly problematic given its underperforming core business.

On a positive note, DXC Technology holds a Baa2 credit rating, contributing to a moderate cost of debt at 8%. When considering tax shields, the after-tax cost of this debt is reduced to 5.8%. While the Baa2 rating does offer some comfort, it doesn't completely alleviate the risks signalled by other financial indicators.

Upon examining the company's capital structure, it is revealed that 52.5% of its capital is debt-financed. This ratio leads to an overall weighted average cost of capital of 8.39%.

{kind=link}

Downward Trajectory

DXC Technology is projected to experience a contraction of approximately 2% annually for the ensuing five years. This trend is attributed to the ongoing divestitures and operational restructuring. Over the last five years, the company's revenues have declined by an annual rate of 8.2%, largely due to asset sales. While the rate of divestitures is expected to decelerate, the economic headwinds in the IT services sector could perpetuate this shrinking trend.

Margin Analysis

Contrary to the revenue decline, DXC Technology has successfully upheld its gross margin between 21-22%. Strategic cost-cutting measures, particularly in Selling, General and administrative expenses, are expected to elevate the company’s EBITA margin from 3% next year to potentially 5% in the terminal year.

Capital Turnover

As the company continues its divestiture strategy, its balance sheet becomes less encumbered. The capital turnover ratio is anticipated to remain at 1.8 over the next decade, consistent with last year's performance. This implies a return of $1.80 for every dollar invested.

Valuation Metrics

Utilizing the Discounted Cash Flow model and assuming a tax rate of 25%, the estimated intrinsic value of DXC Technology stands at approximately $24.10 per share, a premium to its current trading price of $20.43.

Uncertainties Ahead

It should be noted that these projections are fraught with uncertainties, hinging on the assumption that DXC Technology will resume growth in approximately five years. Failure in restructuring initiatives could jeopardize these forecasts. Moreover, the company's stock repurchase program suggests a self-perceived undervaluation, signalling a potential entry point for risk-tolerant investors.

Conclusion

DXC Technology's recent financial reports reveal a concerning trend: declining revenues across its main business segments. Despite attempts to streamline operations and boost liquidity, the company hasn't been able to reverse these negative trajectories. An additional concern is the company's considerable debt burden, which poses a serious risk for short-term and long-term stability.

Recommendation

For those comfortable with risk, cautiously acquiring a small position in DXC Technology may be worth considering. The potential for a turnaround exists, but it's not guaranteed.

For investors prioritising safety over high returns, keeping DXC Technology on your watchlist and observing its performance over the next quarter would be prudent. This will give you a better picture of whether or not the company is turning things around.

If you're already invested in DXC Technology, maintaining your current stake could be a reasonable approach. There's still the chance that the company's future growth initiatives may pay off, leading to a reasonable ROI.

Investment Rating : Hold (High Risk)

For further details see:

DXC Technology: A High-Risk Play For Investors